BGSF PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Gain a strategic edge with our concise PESTLE Analysis of BGSF—revealing how political shifts, economic pressures, and tech trends shape its outlook and risk profile; perfect for investors and strategists seeking actionable intelligence. Buy the full report to access detailed, ready-to-use insights and forecasts you can apply immediately.

Political factors

Impact of protectionist trade policies and tariffs

The 2025 shift toward protectionism and volatile tariffs drove client hiring freezes and delayed projects, with global trade barriers rising 12% YoY and firms reporting a 9% cut in hiring budgets, directly squeezing BGSF revenue streams.

Unpredictable regimes forced staffing demand to swing by as much as ±15% quarter-to-quarter, prompting BGSF to reallocate resources and manage bench costs.

Markets expect more consistent tariffs in 2026, but the 2025 shock required BGSF to adopt flexible workforce strategies—contingent staffing, rapid redeployment, and variable-cost contracts—to help clients pivot as trade rules evolve.

Government infrastructure and CHIPS Act funding

Significant federal infrastructure spending and the CHIPS and Science Act—allocating roughly $52.7 billion for semiconductor incentives through 2024—has driven up demand for specialized construction and IT talent; BGSF supplies skilled workers for nonresidential specialty trade contractors and semiconductor-related IT projects.

By staffing roles in chip fabs and infrastructure builds, BGSF captures stable, government-backed revenue streams that helped offset commercial slowdowns in 2023–2025, with public-sector contracts often multi-year and higher-margin.

Visa backlogs and immigration policy shifts

Continuing USCIS visa backlogs—H‑1B processing times averaging 6–10 months in 2024 vs. 3–4 months pre‑pandemic—plus stricter immigration enforcement have tightened supply of specialized IT talent, raising sourcing costs by ~12% and time‑to‑fill for technical roles to 45–70 days for BGSF.

These political hurdles push BGSF toward domestic talent pools and upskilling programs; training investments rose ~18% in 2024 to mitigate shortages. Navigating work‑authorization complexities remains a key operational burden for the professional division, driving compliance and legal spend increases.

Public sector hiring surges

A notable surge in public-sector hiring in 2025—federal and state payrolls rose ~2.1% YoY adding an estimated 250,000 jobs—provided a countercyclical buffer as private-sector growth cooled. BGSF tracks these trends to align recruitment toward healthcare and social assistance, which received ~$120B in combined federal/state support in FY2025, stabilizing revenue against volatility in commercial real estate and tech placements.

- Public payrolls +2.1% YoY (~250k jobs)

- Healthcare/social assistance ~ $120B FY2025 support

- Reduces exposure to CRE/tech downturns

Regulatory pressure on worker classification

Ongoing federal and state debates over worker classification—highlighted by 2024 IRS guidance updates and California-style AB5 spillovers—pressure BGSF to adapt compliance; misclassification risk could expose the firm to penalties and back-pay liabilities that in past cases have exceeded millions (average settlements in staffing cases 2022–2024 ranged $200k–$5M).

BGSF must keep agile policies and payroll controls as shifts toward stricter tests (economic realities/ABC tests) can raise labor costs by 10–30% and increase employer tax and benefits obligations, materially affecting gross margin on contract staffing.

- Maintain updated classification audits and legal reserves

- Estimate 10–30% increase in labor-related cost under stricter rules

- Monitor state-level reforms and IRS guidance changes

BGSF braces for tariff shock, hiring freeze, and 10–30% labor cost risk

BGSF faced 2024–25 trade shocks and protectionism—tariffs +12% YoY—causing hiring freezes and ±15% demand swings; federal infrastructure and CHIPS spending (~$52.7B through 2024) and +2.1% public payrolls (~250k jobs in 2025) offset private-sector losses; USCIS backlogs (H‑1B 6–10 months) raised sourcing costs ~12% and time‑to‑fill to 45–70 days; potential worker‑classification reforms could raise labor costs 10–30%.

| Metric | Value |

|---|---|

| Tariff change 2025 | +12% YoY |

| CHIPS funding | $52.7B (through 2024) |

| Public payrolls 2025 | +2.1% (~250k) |

| H‑1B processing | 6–10 months |

| Sourcing cost rise | ~12% |

| Labor cost risk | +10–30% |

What is included in the product

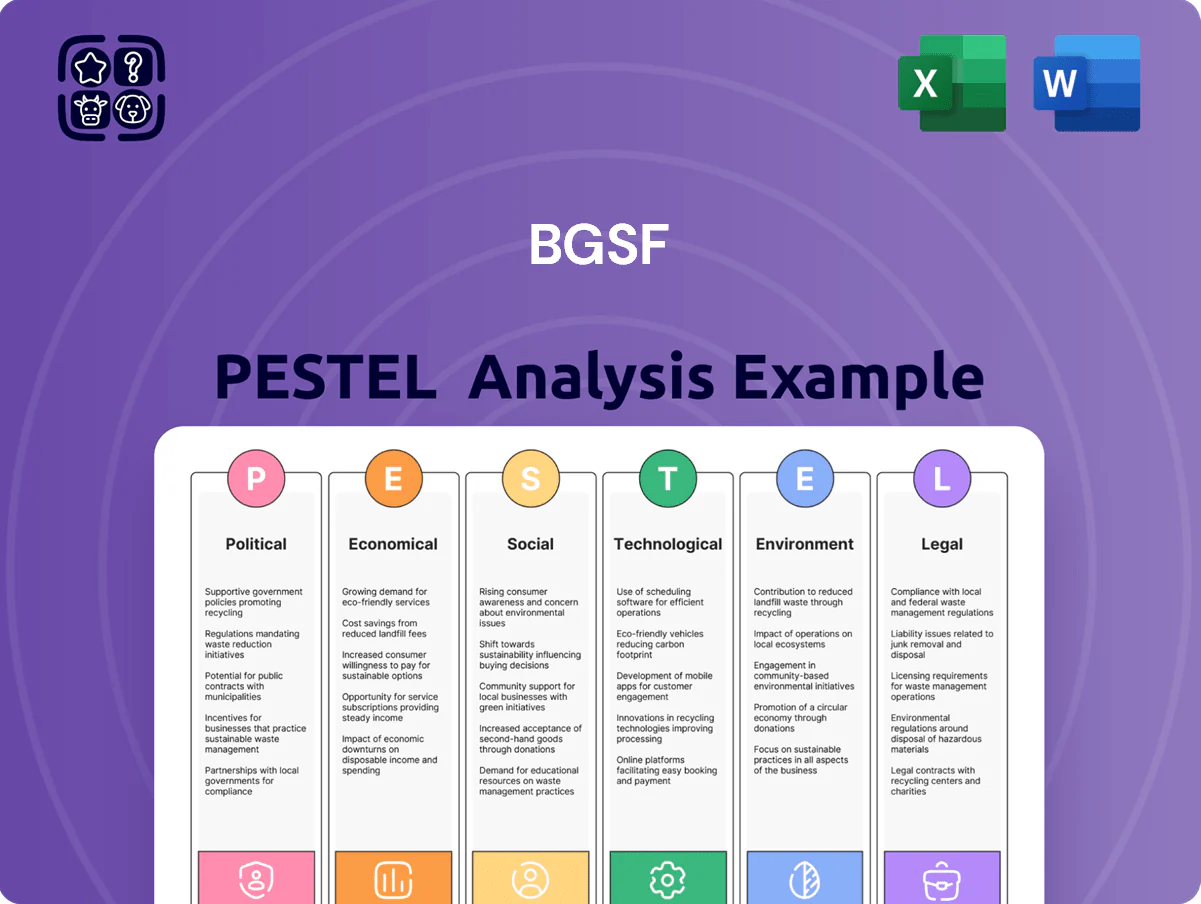

Explores how macro-environmental factors—Political, Economic, Social, Technological, Environmental, and Legal—uniquely impact BGSF, with each section backed by data and current trends to identify threats and opportunities for executives, consultants, and entrepreneurs.

Condenses BGSF's full PESTLE into a clean, shareable summary that highlights key external risks and opportunities by category for quick insertion into presentations, team briefings, or client reports.

Economic factors

The Great Recalibration of the labor market

The 2026 labor market shows a low-hire, low-fire mentality after benchmark revisions erased 1.02 million jobs from 2024–25 payrolls, tightening the available talent pool and intensifying competition for specialized roles relevant to BGSF and clients. Vacancy-to-unemployment ratios rose to 1.8 in Q1 2026, driving higher sourcing costs and longer fill times; firms prioritize quality and retention over rapid headcount growth, benefiting BGSF’s specialty staffing margins.

Interest rate sensitivity and cost of capital

Elevated U.S. interest rates through 2025 pushed corporate borrowing costs above 6%, raising clients’ weighted average cost of capital and prompting a 7–10% reduction in contingent labor spend and delays in contractor-led projects for BGSF.

Potential Fed rate cuts in 2026 could reaccelerate project starts, but near-term pressure forces BGSF to enforce disciplined pricing and tighten treasury management to preserve margins and liquidity.

High rates also inflated property insurance and financing costs, contributing to a 12% slowdown in new multifamily starts in 2025 and compressing demand in BGSF’s property management segment.

Wage inflation and bill rate spreads

Persistent wage growth around 4–5% in 2024–25 has forced BGSF to reprice contracts to defend gross margins as input pay outpaces client budgets; bill rates rose an estimated 6–10% year-over-year, compressing bill rate–pay spreads and necessitating real-time market intelligence for successful negotiations. Clients are more selective, prioritizing retention and candidate quality over speed to offset rising hiring costs and reduce churn.

Temporary help as a leading indicator

Temporary help services began showing modest growth in early 2026, with US temporary staffing employment up 2.1% year-over-year in Q1 2026, signaling green shoots for recovery.

Conservative employers favor BGSF’s contract and project-based solutions to retain agility, delaying full-time hiring and boosting billable hours and margin stability.

This positioning lets BGSF capture early-stage demand ahead of a shift back to direct-hire placements.

- Q1 2026 temp staffing +2.1% YoY

- Higher utilization of contract roles

- Early revenue capture before direct-hire rebound

Sectoral demand dispersion

Growth is uneven: global IT spending is approaching $5 trillion in 2025 (Gartner), while commercial real estate faces rising vacancy and maintenance pressures, with U.S. office vacancy near 16% in 2024 (CBRE).

BGSF shifts capital into countercyclical niches and resilient healthcare staffing, targeting stable revenue streams to offset cyclical commercial and property-market volatility.

- IT spending ≈ $5T (2025)

- U.S. office vacancy ≈ 16% (2024)

- Focus: healthcare staffing, countercyclical niches

- Goal: revenue stabilization via diversification

Labor tightness, rising wages and rates reshape hiring: temp growth vs compressed spreads

Macroeconomic tightness in 2024–25 cut payrolls by 1.02M, vacancy/unemployment 1.8 (Q1 2026); temp staffing +2.1% YoY (Q1 2026); wage inflation 4–5% drove bill rates +6–10% and compressed spreads; corporate borrowing >6% through 2025 reduced contingent spend 7–10%; IT spend ≈ $5T (2025), US office vacancy ≈16% (2024).

| Metric | Value |

|---|---|

| Payroll revisions | -1.02M (2024–25) |

| Vacancy/Unemp | 1.8 (Q1 2026) |

| Temp staffing | +2.1% YoY (Q1 2026) |

| Wage growth | 4–5% (2024–25) |

| Bill rates | +6–10% YoY |

| Borrowing costs | >6% (through 2025) |

| IT spend | $5T (2025) |

| US office vacancy | ≈16% (2024) |

Preview Before You Purchase

BGSF PESTLE Analysis

The preview shown here is the exact BGSF PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for analysis and decision-making.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Plan Smarter. Present Sharper. Compete Stronger.

Gain a strategic edge with our concise PESTLE Analysis of BGSF—revealing how political shifts, economic pressures, and tech trends shape its outlook and risk profile; perfect for investors and strategists seeking actionable intelligence. Buy the full report to access detailed, ready-to-use insights and forecasts you can apply immediately.

Political factors

Impact of protectionist trade policies and tariffs

The 2025 shift toward protectionism and volatile tariffs drove client hiring freezes and delayed projects, with global trade barriers rising 12% YoY and firms reporting a 9% cut in hiring budgets, directly squeezing BGSF revenue streams.

Unpredictable regimes forced staffing demand to swing by as much as ±15% quarter-to-quarter, prompting BGSF to reallocate resources and manage bench costs.

Markets expect more consistent tariffs in 2026, but the 2025 shock required BGSF to adopt flexible workforce strategies—contingent staffing, rapid redeployment, and variable-cost contracts—to help clients pivot as trade rules evolve.

Government infrastructure and CHIPS Act funding

Significant federal infrastructure spending and the CHIPS and Science Act—allocating roughly $52.7 billion for semiconductor incentives through 2024—has driven up demand for specialized construction and IT talent; BGSF supplies skilled workers for nonresidential specialty trade contractors and semiconductor-related IT projects.

By staffing roles in chip fabs and infrastructure builds, BGSF captures stable, government-backed revenue streams that helped offset commercial slowdowns in 2023–2025, with public-sector contracts often multi-year and higher-margin.

Visa backlogs and immigration policy shifts

Continuing USCIS visa backlogs—H‑1B processing times averaging 6–10 months in 2024 vs. 3–4 months pre‑pandemic—plus stricter immigration enforcement have tightened supply of specialized IT talent, raising sourcing costs by ~12% and time‑to‑fill for technical roles to 45–70 days for BGSF.

These political hurdles push BGSF toward domestic talent pools and upskilling programs; training investments rose ~18% in 2024 to mitigate shortages. Navigating work‑authorization complexities remains a key operational burden for the professional division, driving compliance and legal spend increases.

Public sector hiring surges

A notable surge in public-sector hiring in 2025—federal and state payrolls rose ~2.1% YoY adding an estimated 250,000 jobs—provided a countercyclical buffer as private-sector growth cooled. BGSF tracks these trends to align recruitment toward healthcare and social assistance, which received ~$120B in combined federal/state support in FY2025, stabilizing revenue against volatility in commercial real estate and tech placements.

- Public payrolls +2.1% YoY (~250k jobs)

- Healthcare/social assistance ~ $120B FY2025 support

- Reduces exposure to CRE/tech downturns

Regulatory pressure on worker classification

Ongoing federal and state debates over worker classification—highlighted by 2024 IRS guidance updates and California-style AB5 spillovers—pressure BGSF to adapt compliance; misclassification risk could expose the firm to penalties and back-pay liabilities that in past cases have exceeded millions (average settlements in staffing cases 2022–2024 ranged $200k–$5M).

BGSF must keep agile policies and payroll controls as shifts toward stricter tests (economic realities/ABC tests) can raise labor costs by 10–30% and increase employer tax and benefits obligations, materially affecting gross margin on contract staffing.

- Maintain updated classification audits and legal reserves

- Estimate 10–30% increase in labor-related cost under stricter rules

- Monitor state-level reforms and IRS guidance changes

BGSF braces for tariff shock, hiring freeze, and 10–30% labor cost risk

BGSF faced 2024–25 trade shocks and protectionism—tariffs +12% YoY—causing hiring freezes and ±15% demand swings; federal infrastructure and CHIPS spending (~$52.7B through 2024) and +2.1% public payrolls (~250k jobs in 2025) offset private-sector losses; USCIS backlogs (H‑1B 6–10 months) raised sourcing costs ~12% and time‑to‑fill to 45–70 days; potential worker‑classification reforms could raise labor costs 10–30%.

| Metric | Value |

|---|---|

| Tariff change 2025 | +12% YoY |

| CHIPS funding | $52.7B (through 2024) |

| Public payrolls 2025 | +2.1% (~250k) |

| H‑1B processing | 6–10 months |

| Sourcing cost rise | ~12% |

| Labor cost risk | +10–30% |

What is included in the product

Explores how macro-environmental factors—Political, Economic, Social, Technological, Environmental, and Legal—uniquely impact BGSF, with each section backed by data and current trends to identify threats and opportunities for executives, consultants, and entrepreneurs.

Condenses BGSF's full PESTLE into a clean, shareable summary that highlights key external risks and opportunities by category for quick insertion into presentations, team briefings, or client reports.

Economic factors

The Great Recalibration of the labor market

The 2026 labor market shows a low-hire, low-fire mentality after benchmark revisions erased 1.02 million jobs from 2024–25 payrolls, tightening the available talent pool and intensifying competition for specialized roles relevant to BGSF and clients. Vacancy-to-unemployment ratios rose to 1.8 in Q1 2026, driving higher sourcing costs and longer fill times; firms prioritize quality and retention over rapid headcount growth, benefiting BGSF’s specialty staffing margins.

Interest rate sensitivity and cost of capital

Elevated U.S. interest rates through 2025 pushed corporate borrowing costs above 6%, raising clients’ weighted average cost of capital and prompting a 7–10% reduction in contingent labor spend and delays in contractor-led projects for BGSF.

Potential Fed rate cuts in 2026 could reaccelerate project starts, but near-term pressure forces BGSF to enforce disciplined pricing and tighten treasury management to preserve margins and liquidity.

High rates also inflated property insurance and financing costs, contributing to a 12% slowdown in new multifamily starts in 2025 and compressing demand in BGSF’s property management segment.

Wage inflation and bill rate spreads

Persistent wage growth around 4–5% in 2024–25 has forced BGSF to reprice contracts to defend gross margins as input pay outpaces client budgets; bill rates rose an estimated 6–10% year-over-year, compressing bill rate–pay spreads and necessitating real-time market intelligence for successful negotiations. Clients are more selective, prioritizing retention and candidate quality over speed to offset rising hiring costs and reduce churn.

Temporary help as a leading indicator

Temporary help services began showing modest growth in early 2026, with US temporary staffing employment up 2.1% year-over-year in Q1 2026, signaling green shoots for recovery.

Conservative employers favor BGSF’s contract and project-based solutions to retain agility, delaying full-time hiring and boosting billable hours and margin stability.

This positioning lets BGSF capture early-stage demand ahead of a shift back to direct-hire placements.

- Q1 2026 temp staffing +2.1% YoY

- Higher utilization of contract roles

- Early revenue capture before direct-hire rebound

Sectoral demand dispersion

Growth is uneven: global IT spending is approaching $5 trillion in 2025 (Gartner), while commercial real estate faces rising vacancy and maintenance pressures, with U.S. office vacancy near 16% in 2024 (CBRE).

BGSF shifts capital into countercyclical niches and resilient healthcare staffing, targeting stable revenue streams to offset cyclical commercial and property-market volatility.

- IT spending ≈ $5T (2025)

- U.S. office vacancy ≈ 16% (2024)

- Focus: healthcare staffing, countercyclical niches

- Goal: revenue stabilization via diversification

Labor tightness, rising wages and rates reshape hiring: temp growth vs compressed spreads

Macroeconomic tightness in 2024–25 cut payrolls by 1.02M, vacancy/unemployment 1.8 (Q1 2026); temp staffing +2.1% YoY (Q1 2026); wage inflation 4–5% drove bill rates +6–10% and compressed spreads; corporate borrowing >6% through 2025 reduced contingent spend 7–10%; IT spend ≈ $5T (2025), US office vacancy ≈16% (2024).

| Metric | Value |

|---|---|

| Payroll revisions | -1.02M (2024–25) |

| Vacancy/Unemp | 1.8 (Q1 2026) |

| Temp staffing | +2.1% YoY (Q1 2026) |

| Wage growth | 4–5% (2024–25) |

| Bill rates | +6–10% YoY |

| Borrowing costs | >6% (through 2025) |

| IT spend | $5T (2025) |

| US office vacancy | ≈16% (2024) |

Preview Before You Purchase

BGSF PESTLE Analysis

The preview shown here is the exact BGSF PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for analysis and decision-making.