Braemar Hotels & Resorts Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

Braemar Hotels & Resorts faces moderate buyer power and rising competitive intensity from both branded rivals and alternative lodging platforms, while supplier leverage and capital barriers keep new entrants in check; regulatory and economic cycles add cyclical risk to cash flows. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Braemar’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Dependence on Global Hotel Brand Managers

Braemar depends on major brands like Marriott and Ritz-Carlton for distribution and reputation; in 2024 branded properties generated about 78% of its EBITDA (Braemar 2024 FY report), giving those brands leverage.

Franchise and management contracts set operations and fees—brand fees often run 4–6% of room revenue plus marketing; that limits Braemar’s pricing flexibility.

Switching brands is costly: reflagging a luxury hotel can exceed $2–5 million and risks losing access to loyalty programs holding 200m+ combined members (Marriott+Ritz), so supplier power is high.

Specialized Labor and Union Influence

The luxury hotel segment demands highly skilled staff to meet affluent guest expectations, and Braemar Hotels & Resorts faces upward wage pressure as average luxury front‑of‑house pay rose 6.2% YoY in 2025, per industry payroll surveys. In key gateway markets like New York and London, unions—representing roughly 30–40% of hospitality workers—push higher base wages and benefits, adding to operating costs. A late‑2025 shortage of specialized talent increased recruitment and training spend by an estimated 8–12% for REIT portfolios, compressing margins. This supplier power forces Braemar to factor higher labor inflation into RevPAR forecasts and capex for staff development.

Concentration of Third-Party Management Services

Braemar relies heavily on Ashford Inc. for asset management and advisory, creating supplier concentration; as of FY2024 Ashford managed ~70% of Braemar’s portfolio assets under management, limiting bargaining leverage.

This dependency makes fee renegotiation hard and switching costly—contractual break clauses and transition costs can exceed 1–2% of AUM, per industry data—reducing price pressure on suppliers.

Specialized hotel REIT management has few high-quality substitutes; only a handful of managers handle similar assets and scale, keeping supplier power elevated and fee floors sticky.

Utility and Infrastructure Monopolies

Large-scale luxury resorts need huge energy and water volumes, leaving Braemar Hotels & Resorts exposed to volatile utility pricing and local regulation with little negotiation power because services are provided by regional monopolies.

In 2025 rising environmental compliance increased infrastructure costs—US hotel energy spend rose ~6% YoY and water tariffs climbed ~4% in key markets—pushing CapEx and Opex for sustainable systems higher.

- High dependency on local utility monopolies

- Limited bargaining power over rates/terms

- 2025: energy costs +6% YoY; water tariffs +4% in sample markets

- Higher compliance drives CapEx/Opex for efficiency

Premium Food and Beverage Supply Chains

Maintaining luxury standards forces Braemar Hotels & Resorts to buy niche culinary products and premium spirits from specialized vendors, giving suppliers moderate bargaining power since cheaper substitutes would harm brand reputation.

Global food inflation hit 13% in 2022 and slowed to ~6% in 2024, squeezing F&B margins—Braemar reported F&B margin pressure in 2024 affecting GOPPAR (gross operating profit per available room).

Braemar margin squeeze: high brand fees, reflag costs & rising labor/utility inflation

Braemar faces high supplier power: 78% EBITDA from branded properties (Braemar FY2024) and brand fees of 4–6% limit pricing; reflagging costs $2–5m and risks loyalty access (200m+ members). Ashford managed ~70% of assets (FY2024), raising switching costs; labor inflation rose 6.2% YoY (2025) and energy/water +6%/+4% in sample markets, pressuring margins.

| Metric | Value |

|---|---|

| Branded EBITDA | 78% (FY2024) |

| Brand fees | 4–6% of room rev |

| Reflag cost | $2–5m |

| Ashford AUM share | ~70% (FY2024) |

| Labor inflation | +6.2% YoY (2025) |

| Energy / Water | +6% / +4% (sample markets, 2025) |

What is included in the product

Tailored exclusively for Braemar Hotels & Resorts, this Porter's Five Forces overview uncovers competitive drivers, buyer and supplier influence on pricing, entry barriers that protect incumbents, and disruptive substitutes and threats to market share.

A concise Porter's Five Forces one-sheet for Braemar Hotels & Resorts—quickly gauge competitive pressure and investment risk to speed boardroom or investor decisions.

Customers Bargaining Power

Influence of Online Travel Agencies

Platforms like Expedia and Booking.com control ~70% of online bookings globally, pushing commissions of 15–25%, which squeezes margins for Braemar Hotels & Resorts (a luxury-focused REIT). Even high-end guests use these sites for price discovery, so Braemar must match visible rates and pay steep fees to stay listed; in 2024 OTA-driven revenue accounted for an estimated 30% of luxury hotel bookings, forcing tighter pricing and higher distribution costs.

Corporate and Group Booking Leverage

Large corporations and professional organizations that book blocks of rooms exert strong bargaining power, frequently securing group discounts and amenity concessions that lower RevPAR (revenue per available room) by 5–15% during off-peak periods; Braemar reported a 9% RevPAR decline in non-peak months in 2024 across comparable gateway properties. The concentration risk is material: loss of a single major corporate account in a gateway market can wipe out 2–6% of a property’s annual revenue, per 2024 internal mix data. Negotiations often force rate parity and added F&B credits, pressuring margins and GOPPAR (gross operating profit per available room).

High Expectations of Affluent Individual Travelers

The luxury demographic demands personalized service and top-tier amenities, making them highly discerning and vocal customers; in 2024, U.S. ultra-high-net-worth travel spend rose 9% to $72 billion, signaling stronger expectations. Social media and review platforms amplify single negative stays—Tripadvisor shows 89% of affluent travelers consult reviews before booking—so reputational risk is high. This forces Braemar Hotels & Resorts to reinvest: management disclosed $45–60 million annual capex plans in 2025 to refresh properties and retain high-net-worth guests.

Availability of Loyalty Program Incentives

Frequent travelers favor hotels where they can earn or redeem points in major programs like Marriott Bonvoy; in 2024 Marriott reported 160 million members, so Braemar properties lacking comparable loyalty perks risk losing guests to rivals.

If Braemar fails to match luxury-tier benefits—upgrades, late checkout, bonus points—members will switch, giving customers leverage to demand more value via membership status.

- Marriott Bonvoy: 160 million members (2024)

- Luxury guests value upgrades, breakfast, late checkout

- Weak loyalty benefits increase churn risk

- Customers can demand added services or shift brands

Low Switching Costs in Gateway Markets

In gateway markets like New York and Miami, Braemar faces dense five-star competition—Manhattan had 120 hotels rated 4.5+ in 2024 within 5 miles, so luxury guests can switch easily for one-night stays.

Switching costs are minimal: average room-price gaps under $50/night in 2024 make financial barriers negligible, raising pressure to differentiate via service and upkeep.

Customer loyalty is fleeting; Braemar must re-earn repeat stays through flawless service delivery and capital investment in maintenance—luxury guest retention lifts RevPAR by ~12% if achieved.

- High local supply: 120+ 4.5+ hotels (Manhattan, 2024)

- Price sensitivity: <$50 average gap (2024)

- Impact: +12% RevPAR from retention

Customers Hold Power: OTAs, Loyalty & Supply Force Higher Capex and Squeeze RevPAR

Customers hold strong bargaining power: OTAs drive ~30% luxury bookings (15–25% commissions), corporate bookers cut RevPAR 5–15% (Braemar saw 9% off‑peak RevPAR drop in 2024), loyalty program scale (Marriott Bonvoy 160M members, 2024) and dense gateway supply (120+ 4.5+ hotels Manhattan, 2024) make switching easy and force higher capex ($45–60M planned 2025) to retain guests.

| Metric | Value (2024/2025) |

|---|---|

| OTA share | 30% |

| OTA commission | 15–25% |

| RevPAR off‑peak impact | -9% |

| Marriott Bonvoy members | 160M |

| Manhattan 4.5+ hotels | 120+ |

| Planned capex | $45–60M (2025) |

What You See Is What You Get

Braemar Hotels & Resorts Porter's Five Forces Analysis

This preview shows the exact Braemar Hotels & Resorts Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders; the full, professionally formatted document is ready for download and use the moment you buy.

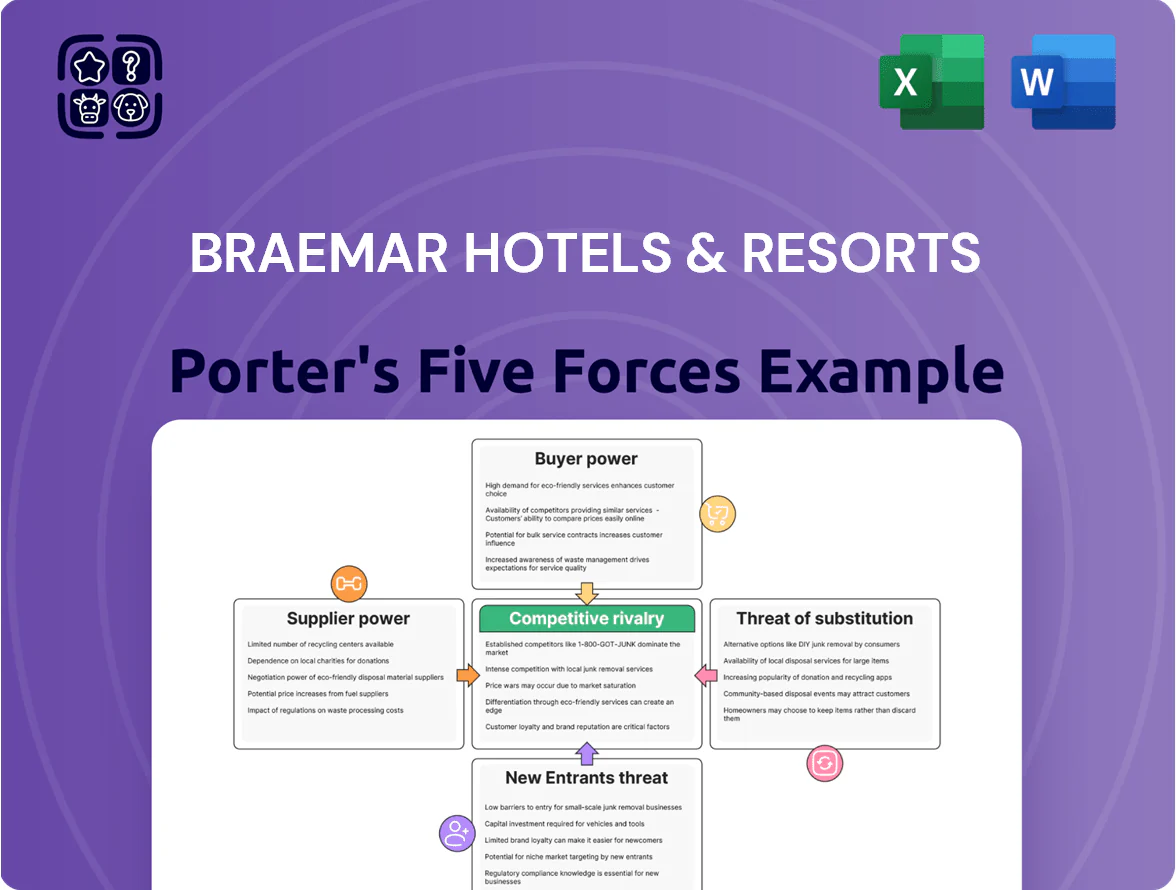

You're viewing the actual deliverable: a complete, ready-to-use assessment covering supplier power, buyer power, competitive rivalry, threat of substitutes, and barriers to entry, available instantly upon payment.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

Braemar Hotels & Resorts faces moderate buyer power and rising competitive intensity from both branded rivals and alternative lodging platforms, while supplier leverage and capital barriers keep new entrants in check; regulatory and economic cycles add cyclical risk to cash flows. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Braemar’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Dependence on Global Hotel Brand Managers

Braemar depends on major brands like Marriott and Ritz-Carlton for distribution and reputation; in 2024 branded properties generated about 78% of its EBITDA (Braemar 2024 FY report), giving those brands leverage.

Franchise and management contracts set operations and fees—brand fees often run 4–6% of room revenue plus marketing; that limits Braemar’s pricing flexibility.

Switching brands is costly: reflagging a luxury hotel can exceed $2–5 million and risks losing access to loyalty programs holding 200m+ combined members (Marriott+Ritz), so supplier power is high.

Specialized Labor and Union Influence

The luxury hotel segment demands highly skilled staff to meet affluent guest expectations, and Braemar Hotels & Resorts faces upward wage pressure as average luxury front‑of‑house pay rose 6.2% YoY in 2025, per industry payroll surveys. In key gateway markets like New York and London, unions—representing roughly 30–40% of hospitality workers—push higher base wages and benefits, adding to operating costs. A late‑2025 shortage of specialized talent increased recruitment and training spend by an estimated 8–12% for REIT portfolios, compressing margins. This supplier power forces Braemar to factor higher labor inflation into RevPAR forecasts and capex for staff development.

Concentration of Third-Party Management Services

Braemar relies heavily on Ashford Inc. for asset management and advisory, creating supplier concentration; as of FY2024 Ashford managed ~70% of Braemar’s portfolio assets under management, limiting bargaining leverage.

This dependency makes fee renegotiation hard and switching costly—contractual break clauses and transition costs can exceed 1–2% of AUM, per industry data—reducing price pressure on suppliers.

Specialized hotel REIT management has few high-quality substitutes; only a handful of managers handle similar assets and scale, keeping supplier power elevated and fee floors sticky.

Utility and Infrastructure Monopolies

Large-scale luxury resorts need huge energy and water volumes, leaving Braemar Hotels & Resorts exposed to volatile utility pricing and local regulation with little negotiation power because services are provided by regional monopolies.

In 2025 rising environmental compliance increased infrastructure costs—US hotel energy spend rose ~6% YoY and water tariffs climbed ~4% in key markets—pushing CapEx and Opex for sustainable systems higher.

- High dependency on local utility monopolies

- Limited bargaining power over rates/terms

- 2025: energy costs +6% YoY; water tariffs +4% in sample markets

- Higher compliance drives CapEx/Opex for efficiency

Premium Food and Beverage Supply Chains

Maintaining luxury standards forces Braemar Hotels & Resorts to buy niche culinary products and premium spirits from specialized vendors, giving suppliers moderate bargaining power since cheaper substitutes would harm brand reputation.

Global food inflation hit 13% in 2022 and slowed to ~6% in 2024, squeezing F&B margins—Braemar reported F&B margin pressure in 2024 affecting GOPPAR (gross operating profit per available room).

Braemar margin squeeze: high brand fees, reflag costs & rising labor/utility inflation

Braemar faces high supplier power: 78% EBITDA from branded properties (Braemar FY2024) and brand fees of 4–6% limit pricing; reflagging costs $2–5m and risks loyalty access (200m+ members). Ashford managed ~70% of assets (FY2024), raising switching costs; labor inflation rose 6.2% YoY (2025) and energy/water +6%/+4% in sample markets, pressuring margins.

| Metric | Value |

|---|---|

| Branded EBITDA | 78% (FY2024) |

| Brand fees | 4–6% of room rev |

| Reflag cost | $2–5m |

| Ashford AUM share | ~70% (FY2024) |

| Labor inflation | +6.2% YoY (2025) |

| Energy / Water | +6% / +4% (sample markets, 2025) |

What is included in the product

Tailored exclusively for Braemar Hotels & Resorts, this Porter's Five Forces overview uncovers competitive drivers, buyer and supplier influence on pricing, entry barriers that protect incumbents, and disruptive substitutes and threats to market share.

A concise Porter's Five Forces one-sheet for Braemar Hotels & Resorts—quickly gauge competitive pressure and investment risk to speed boardroom or investor decisions.

Customers Bargaining Power

Influence of Online Travel Agencies

Platforms like Expedia and Booking.com control ~70% of online bookings globally, pushing commissions of 15–25%, which squeezes margins for Braemar Hotels & Resorts (a luxury-focused REIT). Even high-end guests use these sites for price discovery, so Braemar must match visible rates and pay steep fees to stay listed; in 2024 OTA-driven revenue accounted for an estimated 30% of luxury hotel bookings, forcing tighter pricing and higher distribution costs.

Corporate and Group Booking Leverage

Large corporations and professional organizations that book blocks of rooms exert strong bargaining power, frequently securing group discounts and amenity concessions that lower RevPAR (revenue per available room) by 5–15% during off-peak periods; Braemar reported a 9% RevPAR decline in non-peak months in 2024 across comparable gateway properties. The concentration risk is material: loss of a single major corporate account in a gateway market can wipe out 2–6% of a property’s annual revenue, per 2024 internal mix data. Negotiations often force rate parity and added F&B credits, pressuring margins and GOPPAR (gross operating profit per available room).

High Expectations of Affluent Individual Travelers

The luxury demographic demands personalized service and top-tier amenities, making them highly discerning and vocal customers; in 2024, U.S. ultra-high-net-worth travel spend rose 9% to $72 billion, signaling stronger expectations. Social media and review platforms amplify single negative stays—Tripadvisor shows 89% of affluent travelers consult reviews before booking—so reputational risk is high. This forces Braemar Hotels & Resorts to reinvest: management disclosed $45–60 million annual capex plans in 2025 to refresh properties and retain high-net-worth guests.

Availability of Loyalty Program Incentives

Frequent travelers favor hotels where they can earn or redeem points in major programs like Marriott Bonvoy; in 2024 Marriott reported 160 million members, so Braemar properties lacking comparable loyalty perks risk losing guests to rivals.

If Braemar fails to match luxury-tier benefits—upgrades, late checkout, bonus points—members will switch, giving customers leverage to demand more value via membership status.

- Marriott Bonvoy: 160 million members (2024)

- Luxury guests value upgrades, breakfast, late checkout

- Weak loyalty benefits increase churn risk

- Customers can demand added services or shift brands

Low Switching Costs in Gateway Markets

In gateway markets like New York and Miami, Braemar faces dense five-star competition—Manhattan had 120 hotels rated 4.5+ in 2024 within 5 miles, so luxury guests can switch easily for one-night stays.

Switching costs are minimal: average room-price gaps under $50/night in 2024 make financial barriers negligible, raising pressure to differentiate via service and upkeep.

Customer loyalty is fleeting; Braemar must re-earn repeat stays through flawless service delivery and capital investment in maintenance—luxury guest retention lifts RevPAR by ~12% if achieved.

- High local supply: 120+ 4.5+ hotels (Manhattan, 2024)

- Price sensitivity: <$50 average gap (2024)

- Impact: +12% RevPAR from retention

Customers Hold Power: OTAs, Loyalty & Supply Force Higher Capex and Squeeze RevPAR

Customers hold strong bargaining power: OTAs drive ~30% luxury bookings (15–25% commissions), corporate bookers cut RevPAR 5–15% (Braemar saw 9% off‑peak RevPAR drop in 2024), loyalty program scale (Marriott Bonvoy 160M members, 2024) and dense gateway supply (120+ 4.5+ hotels Manhattan, 2024) make switching easy and force higher capex ($45–60M planned 2025) to retain guests.

| Metric | Value (2024/2025) |

|---|---|

| OTA share | 30% |

| OTA commission | 15–25% |

| RevPAR off‑peak impact | -9% |

| Marriott Bonvoy members | 160M |

| Manhattan 4.5+ hotels | 120+ |

| Planned capex | $45–60M (2025) |

What You See Is What You Get

Braemar Hotels & Resorts Porter's Five Forces Analysis

This preview shows the exact Braemar Hotels & Resorts Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders; the full, professionally formatted document is ready for download and use the moment you buy.

You're viewing the actual deliverable: a complete, ready-to-use assessment covering supplier power, buyer power, competitive rivalry, threat of substitutes, and barriers to entry, available instantly upon payment.