Bidvest PESTLE Analysis

Your Shortcut to Market Insight Starts Here

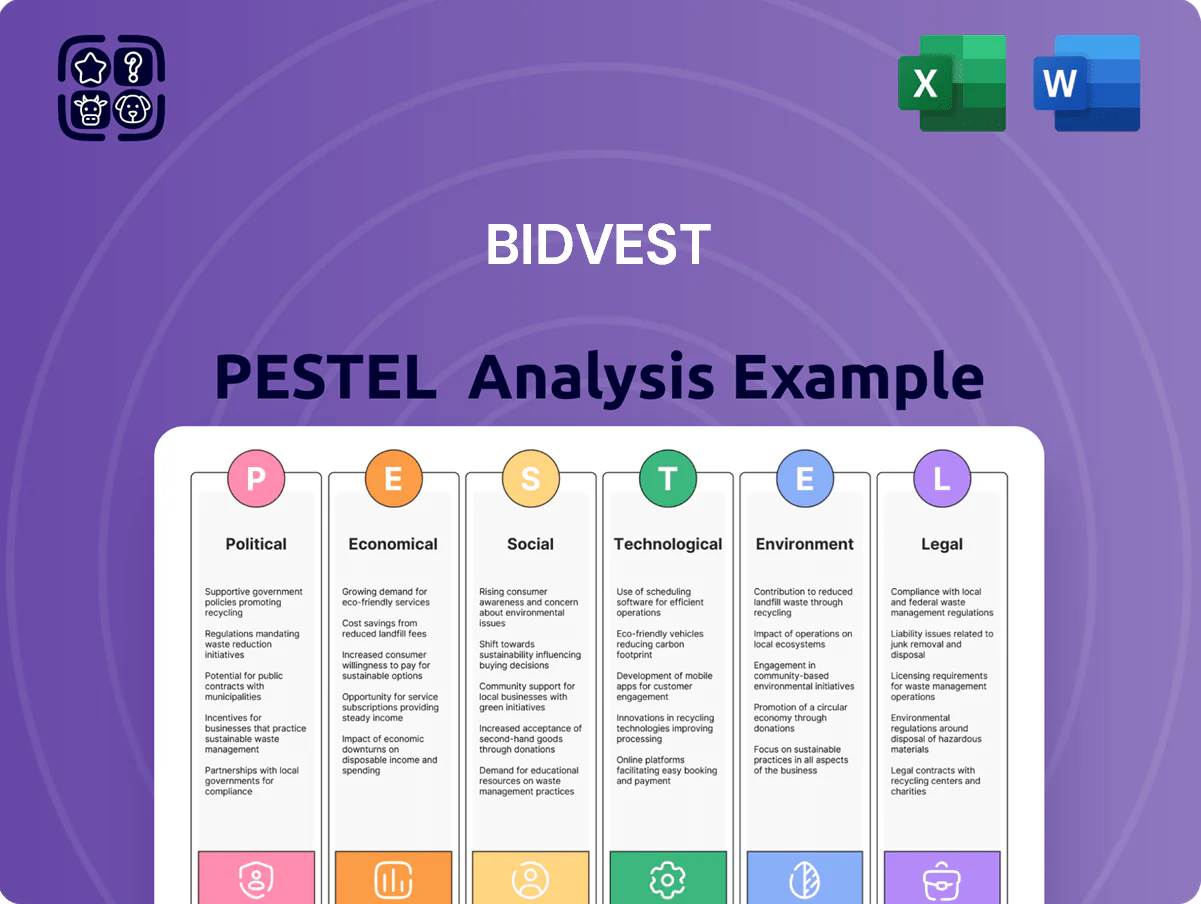

Gain a strategic edge with our PESTLE Analysis of Bidvest—identifying political, economic, social, technological, legal, and environmental forces shaping its prospects and risks; ideal for investors and strategists seeking concise, actionable intelligence. Purchase the full report for a complete, editable breakdown you can use immediately to inform decisions and forecasts.

Political factors

South African Government Stability

The 2024 elections led to a Government of National Unity, improving investor sentiment and reducing sovereign risk premiums; South Africa’s GDP growth forecast for 2025 was revised to about 1.6% by the SARB, supporting demand for Bidvest’s domestic services (2024 revenue: R76.9bn across the group). Progress on infrastructure reforms and PPPs—R300bn pipeline announced for ports/roads through 2026—will directly affect growth in Bidvest’s freight and services divisions.

Geopolitical Volatility in International Markets

As Bidvest expands in the UK, Ireland and Spain, shifting geopolitical alliances and trade policies threaten margins in its hygiene and facility management segments; UK goods exports to the EU fell 15% in 2023, highlighting border frictions that can raise logistics costs for Bidvest’s £350m UK distribution operations.

Public Sector Procurement Policies

A substantial portion of Bidvest’s revenue—roughly 20–25% of group turnover in FY2024—comes from state-owned enterprises and government contracts across multiple jurisdictions, making public procurement policy shifts material to earnings.

Changes to South Africa’s preferential procurement frameworks and B-BBEE targets, tightened in 2023–2024, require ongoing alignment to retain contract eligibility and avoid revenue erosion.

Rising political moves toward localization and insourcing in 2024 pose a direct threat to Bidvest’s outsourced services model, potentially reducing market access and margins if enacted broadly.

Global Trade and Tariff Regulations

The group’s automotive and trading divisions are highly sensitive to international trade agreements and tariff structures; in FY2025 Bidvest reported automotive revenue of ZAR 22.1bn, making margin exposure to tariffs material.

Political decisions on import duties for vehicles and components can compress margins and reduce consumer demand; a 10% tariff hike could erode segment EBITDA by an estimated 3–5% based on 2024 margins.

With global protectionism rising, Bidvest must navigate complex customs regulations and compliance costs—non-tariff barriers increased shipping delays by 12% in 2024, raising logistics spend.

- Automotive revenue FY2025: ZAR 22.1bn

- Estimated EBITDA hit from 10% tariff: 3–5%

- 2024 shipping delays up 12%, increasing logistics costs

Labor Union Relations and Political Influence

- 138 000 employees (2024)

- ~1 200 national strike days (2024)

- Minimum wage/law changes risk raising labour costs

- Active union/policy engagement mitigates disruption

Post‑2024 political lift boosts domestic demand; strikes, shipping hikes squeeze margins

Political shifts post-2024 elections improved investor sentiment; SARB 2025 GDP +1.6% supports domestic demand (Group revenue 2024: R76.9bn). Trade frictions hit UK/EU flows (UK goods to EU -15% in 2023), raising logistics costs after 2024 shipping delays +12%. State contracts ~20–25% of turnover; 2024 strike days ~1 200 with 138 000 employees increasing labor cost risk.

| Metric | Value |

|---|---|

| Group revenue FY2024 | R76.9bn |

| Automotive revenue FY2025 | ZAR22.1bn |

| State contract share | 20–25% |

| 2024 strike days | ~1 200 |

| Employees (2024) | ~138 000 |

| Shipping delays increase (2024) | +12% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Bidvest across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—using region- and industry-specific data and trends to identify risks and opportunities.

A concise, visually segmented PESTLE summary tailored to Bidvest that can be dropped into presentations or shared across teams, helping stakeholders quickly align on external risks and market positioning during strategic planning.

Economic factors

Interest Rate Fluctuations

The high-interest-rate environment through 2025 raised South Africa's repo rate to 8.25% by Dec 2024, increasing Bidvest’s borrowing costs and dampening consumer discretionary spend.

For Bidvest’s automotive and financial services, higher credit costs compressed volumes and weighed on the loan book, with vehicle finance delinquencies up in 2024 versus 2023.

A shift to monetary easing—markets pricing ~150bp cuts by end-2025—would likely boost demand for high-value assets and lower the group’s interest expense.

Currency Exchange Rate Volatility

Bidvest, as a multinational, sees reported earnings swing with ZAR volatility versus GBP, EUR, USD; in FY2024 FX translation added roughly R1.2bn to headline earnings per Bidvest reporting trends where a 10% ZAR weakening lifted offshore translation but raised import costs.

Weaker Rand benefits translation yet inflates costs for trading and automotive—imports rose ~15% in 2024 in unit-cost terms—pressuring margins.

Bidvest uses hedging and natural offsets; by 2024 it held forward cover and currency swaps covering a portion of near-term exposures, but persistent long-term ZAR volatility remains a material economic risk.

Inflationary Pressure on Operating Costs

Persistent inflation in energy, fuel and labour raised Bidvest’s input costs, with South African CPI at 5.6% in 2025 and diesel up ~18% YoY in 2024, squeezing margins across its diversified services and distribution businesses.

In freight and services, contractual price escalations have preserved margins where present; Bidvest reported gross margin resilience in H1 FY2025 partly due to escalators in logistics contracts.

Economic stagnation in key markets—South Africa GDP growth ~0.8% in 2024—limits customers’ willingness to accept increases, forcing targeted cost containment and efficiency drives to protect operating profit.

GDP Growth in Emerging Markets

The group’s performance is closely tied to macroeconomic health in South Africa and other emerging markets; South Africa’s GDP grew 0.6% in 2024 after 1.9% in 2023, constraining industrial activity and infrastructure spend and weighing on Bidvest’s freight and commercial services.

Low GDP growth limits demand for logistics and supplier markets, while a rebound in mining (copper and platinum demand up in 2024) and manufacturing provides a tailwind for Bidvest’s logistics and industrial supply units.

- South Africa GDP: 0.6% (2024 est); 1.9% (2023)

- Mining/manufacturing recovery boosts freight volumes and industrial supplies

- Slower infrastructure spend depresses commercial services revenue

Consumer Confidence and Spending Power

The retail-facing arms of Bidvest, notably travel and automotive, are sensitive to household disposable income; South African real disposable income fell 0.6% y/y in 2024, pressuring demand for discretionary services.

Economic uncertainty and elevated unemployment—32.9% official rate in Q4 2024—suppress consumer confidence, reducing transaction volumes across nonessential segments.

Diversification into essentials such as hygiene and facilities management (Bidvest’s services contributed ~35% of group revenue in FY2024) offers a defensive buffer against cyclical consumer spending shocks.

- Disposable income down 0.6% y/y (2024)

- Unemployment 32.9% (Q4 2024)

- Services/essentials ~35% of FY2024 revenue

High rates, weak GDP and FX swings squeeze earnings—services provide defensive cushion

Higher rates to 8.25% (Dec 2024) and CPI ~5.6% (2025) raised borrowing and input costs; GDP 0.6% (2024) and unemployment 32.9% cut demand, hurting retail/automotive; ZAR volatility added ~R1.2bn to FY2024 headline earnings translation but lifted import costs ~15% (2024); services (~35% revenue FY2024) provided defensive stability.

| Metric | Value |

|---|---|

| Repo rate | 8.25% (Dec 2024) |

| CPI | 5.6% (2025) |

| GDP | 0.6% (2024) |

| Unemployment | 32.9% (Q4 2024) |

| FX translation | +R1.2bn (FY2024) |

| Services revenue | ~35% (FY2024) |

What You See Is What You Get

Bidvest PESTLE Analysis

The preview shown here is the exact Bidvest PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use; no placeholders or teasers. What you see in layout, content, and structure is the final file available for instant download upon payment. This version is complete and suitable for presentation, research, or strategic planning.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Gain a strategic edge with our PESTLE Analysis of Bidvest—identifying political, economic, social, technological, legal, and environmental forces shaping its prospects and risks; ideal for investors and strategists seeking concise, actionable intelligence. Purchase the full report for a complete, editable breakdown you can use immediately to inform decisions and forecasts.

Political factors

South African Government Stability

The 2024 elections led to a Government of National Unity, improving investor sentiment and reducing sovereign risk premiums; South Africa’s GDP growth forecast for 2025 was revised to about 1.6% by the SARB, supporting demand for Bidvest’s domestic services (2024 revenue: R76.9bn across the group). Progress on infrastructure reforms and PPPs—R300bn pipeline announced for ports/roads through 2026—will directly affect growth in Bidvest’s freight and services divisions.

Geopolitical Volatility in International Markets

As Bidvest expands in the UK, Ireland and Spain, shifting geopolitical alliances and trade policies threaten margins in its hygiene and facility management segments; UK goods exports to the EU fell 15% in 2023, highlighting border frictions that can raise logistics costs for Bidvest’s £350m UK distribution operations.

Public Sector Procurement Policies

A substantial portion of Bidvest’s revenue—roughly 20–25% of group turnover in FY2024—comes from state-owned enterprises and government contracts across multiple jurisdictions, making public procurement policy shifts material to earnings.

Changes to South Africa’s preferential procurement frameworks and B-BBEE targets, tightened in 2023–2024, require ongoing alignment to retain contract eligibility and avoid revenue erosion.

Rising political moves toward localization and insourcing in 2024 pose a direct threat to Bidvest’s outsourced services model, potentially reducing market access and margins if enacted broadly.

Global Trade and Tariff Regulations

The group’s automotive and trading divisions are highly sensitive to international trade agreements and tariff structures; in FY2025 Bidvest reported automotive revenue of ZAR 22.1bn, making margin exposure to tariffs material.

Political decisions on import duties for vehicles and components can compress margins and reduce consumer demand; a 10% tariff hike could erode segment EBITDA by an estimated 3–5% based on 2024 margins.

With global protectionism rising, Bidvest must navigate complex customs regulations and compliance costs—non-tariff barriers increased shipping delays by 12% in 2024, raising logistics spend.

- Automotive revenue FY2025: ZAR 22.1bn

- Estimated EBITDA hit from 10% tariff: 3–5%

- 2024 shipping delays up 12%, increasing logistics costs

Labor Union Relations and Political Influence

- 138 000 employees (2024)

- ~1 200 national strike days (2024)

- Minimum wage/law changes risk raising labour costs

- Active union/policy engagement mitigates disruption

Post‑2024 political lift boosts domestic demand; strikes, shipping hikes squeeze margins

Political shifts post-2024 elections improved investor sentiment; SARB 2025 GDP +1.6% supports domestic demand (Group revenue 2024: R76.9bn). Trade frictions hit UK/EU flows (UK goods to EU -15% in 2023), raising logistics costs after 2024 shipping delays +12%. State contracts ~20–25% of turnover; 2024 strike days ~1 200 with 138 000 employees increasing labor cost risk.

| Metric | Value |

|---|---|

| Group revenue FY2024 | R76.9bn |

| Automotive revenue FY2025 | ZAR22.1bn |

| State contract share | 20–25% |

| 2024 strike days | ~1 200 |

| Employees (2024) | ~138 000 |

| Shipping delays increase (2024) | +12% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Bidvest across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—using region- and industry-specific data and trends to identify risks and opportunities.

A concise, visually segmented PESTLE summary tailored to Bidvest that can be dropped into presentations or shared across teams, helping stakeholders quickly align on external risks and market positioning during strategic planning.

Economic factors

Interest Rate Fluctuations

The high-interest-rate environment through 2025 raised South Africa's repo rate to 8.25% by Dec 2024, increasing Bidvest’s borrowing costs and dampening consumer discretionary spend.

For Bidvest’s automotive and financial services, higher credit costs compressed volumes and weighed on the loan book, with vehicle finance delinquencies up in 2024 versus 2023.

A shift to monetary easing—markets pricing ~150bp cuts by end-2025—would likely boost demand for high-value assets and lower the group’s interest expense.

Currency Exchange Rate Volatility

Bidvest, as a multinational, sees reported earnings swing with ZAR volatility versus GBP, EUR, USD; in FY2024 FX translation added roughly R1.2bn to headline earnings per Bidvest reporting trends where a 10% ZAR weakening lifted offshore translation but raised import costs.

Weaker Rand benefits translation yet inflates costs for trading and automotive—imports rose ~15% in 2024 in unit-cost terms—pressuring margins.

Bidvest uses hedging and natural offsets; by 2024 it held forward cover and currency swaps covering a portion of near-term exposures, but persistent long-term ZAR volatility remains a material economic risk.

Inflationary Pressure on Operating Costs

Persistent inflation in energy, fuel and labour raised Bidvest’s input costs, with South African CPI at 5.6% in 2025 and diesel up ~18% YoY in 2024, squeezing margins across its diversified services and distribution businesses.

In freight and services, contractual price escalations have preserved margins where present; Bidvest reported gross margin resilience in H1 FY2025 partly due to escalators in logistics contracts.

Economic stagnation in key markets—South Africa GDP growth ~0.8% in 2024—limits customers’ willingness to accept increases, forcing targeted cost containment and efficiency drives to protect operating profit.

GDP Growth in Emerging Markets

The group’s performance is closely tied to macroeconomic health in South Africa and other emerging markets; South Africa’s GDP grew 0.6% in 2024 after 1.9% in 2023, constraining industrial activity and infrastructure spend and weighing on Bidvest’s freight and commercial services.

Low GDP growth limits demand for logistics and supplier markets, while a rebound in mining (copper and platinum demand up in 2024) and manufacturing provides a tailwind for Bidvest’s logistics and industrial supply units.

- South Africa GDP: 0.6% (2024 est); 1.9% (2023)

- Mining/manufacturing recovery boosts freight volumes and industrial supplies

- Slower infrastructure spend depresses commercial services revenue

Consumer Confidence and Spending Power

The retail-facing arms of Bidvest, notably travel and automotive, are sensitive to household disposable income; South African real disposable income fell 0.6% y/y in 2024, pressuring demand for discretionary services.

Economic uncertainty and elevated unemployment—32.9% official rate in Q4 2024—suppress consumer confidence, reducing transaction volumes across nonessential segments.

Diversification into essentials such as hygiene and facilities management (Bidvest’s services contributed ~35% of group revenue in FY2024) offers a defensive buffer against cyclical consumer spending shocks.

- Disposable income down 0.6% y/y (2024)

- Unemployment 32.9% (Q4 2024)

- Services/essentials ~35% of FY2024 revenue

High rates, weak GDP and FX swings squeeze earnings—services provide defensive cushion

Higher rates to 8.25% (Dec 2024) and CPI ~5.6% (2025) raised borrowing and input costs; GDP 0.6% (2024) and unemployment 32.9% cut demand, hurting retail/automotive; ZAR volatility added ~R1.2bn to FY2024 headline earnings translation but lifted import costs ~15% (2024); services (~35% revenue FY2024) provided defensive stability.

| Metric | Value |

|---|---|

| Repo rate | 8.25% (Dec 2024) |

| CPI | 5.6% (2025) |

| GDP | 0.6% (2024) |

| Unemployment | 32.9% (Q4 2024) |

| FX translation | +R1.2bn (FY2024) |

| Services revenue | ~35% (FY2024) |

What You See Is What You Get

Bidvest PESTLE Analysis

The preview shown here is the exact Bidvest PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use; no placeholders or teasers. What you see in layout, content, and structure is the final file available for instant download upon payment. This version is complete and suitable for presentation, research, or strategic planning.