Biesse SWOT Analysis

Make Insightful Decisions Backed by Expert Research

Biesse’s core strengths—advanced automation, diversified product lines, and strong global distribution—position it well in the growing woodworking and glass machinery markets, but supply-chain exposure and cyclicality pose clear risks; our full SWOT unpacks strategic opportunities, financial implications, and competitive threats to guide decisions. Purchase the complete SWOT analysis for a professionally formatted, editable report and Excel model to plan, pitch, or invest with confidence.

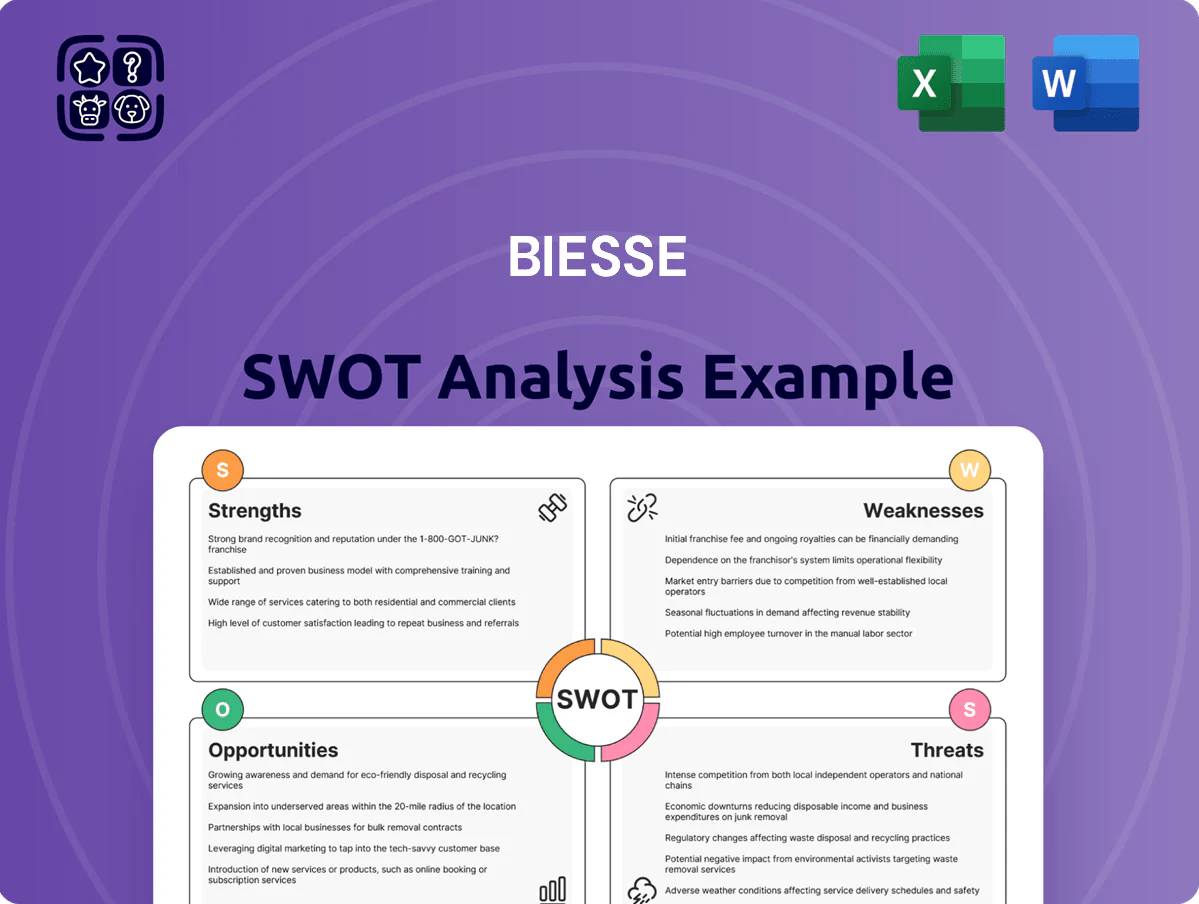

Strengths

Multi-material processing expertise

Biesse holds a competitive edge by supplying specialized machinery across five material sectors—wood, glass, stone, plastic, and metal—supporting its 2024 group revenue of €970.8 million and global install base in 2024 of ~60,000 units. This diversification lowers exposure to sector downturns like furniture or construction, which accounted for ~45% of revenues in 2024. Cross-sector engineering lets Biesse offer integrated, high-tech solutions few rivals match, sustaining a 2024 R&D spend of €51.3 million (5.3% of sales).

Robust global distribution network

Biesse operates via subsidiaries and agents across Europe, North America and Asia, with international sales contributing over 80% of 2024 revenue (€725m total group revenue in 2024), which hedges against country-specific downturns.

Commitment to R&D and digital innovation

Biesse reinvests about 5% of 2024 turnover (≈€62m on €1.24bn sales) into R&D, sustaining Industry 4.0 leadership and new-product cadence.

Proprietary software—bSuite and Sophia IoT—cuts customer downtime via predictive maintenance and raised OEE (overall equipment effectiveness) by reported 8–12% in 2023 pilot deployments.

That digital push shifts Biesse from hardware maker to smart-factory solutions provider, growing software and services to ~14% of group revenue in 2024.

Strategic One Company organizational model

The One Company model cut duplicated functions and lifted EBITDA margin; FY2024 group adjusted EBITDA was 176.6 million EUR (margin 9.8%), reflecting improved operational synergies vs FY2022 (margin ~7.4%). Centralized procurement and shared R&D sped product launch cycles, shortening average time-to-market by ~15% in 2023–24 and boosting cross-segment sales.

- Centralized core functions — faster decisions

- FY2024 adj. EBITDA 176.6M EUR (9.8% margin)

- Time-to-market down ~15% (2023–24)

- Stronger cross-selling across industrial segments

Strong brand reputation and heritage

With over 60 years in woodworking and glass machinery, Biesse (founded 1969) is widely seen as a benchmark for Italian engineering; brand strength supported 2024 revenues of €1.05bn and gross margin ~33%, enabling premium pricing versus peers.

High equity helps secure long-term contracts with Tier 1 furniture and automotive firms, reducing sales volatility and boosting repeat order rates above 60% in recent quarters.

The reputation for reliability and after-sales service creates a steep barrier to entry for smaller competitors in the high-end segment.

- 60+ years heritage

- 2024 revenues €1.05bn

- Gross margin ~33%

- Repeat orders >60%

Biesse: €1.05bn sales, €176.6m adj. EBITDA, 60k install base & >60% repeat orders

Biesse’s diversified machinery (wood, glass, stone, plastic, metal) and ~60,000-unit install base supported 2024 revenues ~€1.05bn and gross margin ~33%, with R&D spend €51.3m (5.3% sales) and software/services ~14% revenue; FY2024 adj. EBITDA €176.6m (9.8% margin) and repeat orders >60% show strong operational and commercial resilience.

| Metric | 2024 |

|---|---|

| Revenue | €1.05bn |

| Adj. EBITDA | €176.6m (9.8%) |

| R&D | €51.3m (5.3%) |

| Install base | ~60,000 units |

| Software/services | ~14% rev |

| Repeat orders | >60% |

What is included in the product

Provides a concise SWOT analysis of Biesse, highlighting its core strengths, operational weaknesses, growth opportunities, and external threats shaping strategic decisions.

Provides a compact SWOT snapshot of Biesse for rapid strategic alignment and stakeholder briefings, editable for quick updates as market conditions shift.

Weaknesses

High sensitivity to macroeconomic cycles

The demand for Biesse (Biesse S.p.A., Italy) is highly cyclical: global capex for machinery fell 6% in 2023 and business investment remains squeezed by 2024–25 rising interest rates and 5% inflation in euro area, so customers in furniture and construction often delay machine purchases.

Significant operational cost structure

Maintaining Biesse’s global manufacturing and service footprint drives high fixed costs—manufacturing overheads and 2024 capex of €72m pressured margins when order intake fell 8% YoY in H1 2024.

Rising energy and raw-material costs hit COGS; steel and electronic component prices added an estimated 2.4 percentage points to input inflation in 2023–24.

One Company aims to cut redundancy, but managing 3,600+ employees worldwide (2024 headcount) keeps complexity high and raises execution risk for margins.

Geographical concentration in European markets

Despite global sales, Biesse still earned about 58% of 2024 revenue from Europe (EUR 830m of EUR 1.43bn), a region with 2023–24 industrial machinery growth near 1–2%, lagging Asia-Pacific's ~5% growth.

That concentration means EU economic shocks or tighter regulations could cut order intake sharply; in 2022–24 Europe-driven order volatility correlated with a 12% swing in quarterly backlog.

Biesse needs faster diversification: targeting +30–40% revenue mix in high-growth APAC/Latin America over 3–5 years would materially lower regional risk.

Complexity in software ecosystem integration

- R&D €89.6m (FY2024), +12%

- 41% manufacturers report digital-skill gaps (2024)

- Higher cyber risk requires continuous updates

- Seamless UX critical to retain value

Working capital management pressures

Biesse’s custom industrial systems require high inventory and long cash conversion cycles; at FY2024 year-end net working capital was 379.6 million EUR, keeping cash tied up and pressuring liquidity.

Balancing stock for fast delivery against capital efficiency is a recurring challenge; DSO and DIO spikes during 2022–2023 supply disruptions extended the cash conversion cycle by several weeks.

Supply-chain volatility can intensify these strains, limiting free cash flow—Biesse’s 2024 operating cash flow fell to 51.3 million EUR, constraining funding for new initiatives.

- Net working capital 379.6M EUR (FY2024)

- Operating cash flow 51.3M EUR (FY2024)

- Extended cash conversion cycle in 2022–23 during supply shocks

Europe‑focused, cyclical pressure: falling orders, squeezed margins, high capex & NWC

High cyclicality and Europe concentration (58% of €1.43bn 2024 revenue) plus rising input and energy costs squeezed margins; H1 2024 order intake fell 8% YoY and FY2024 operating cash flow was €51.3m. Large fixed costs (2024 capex €72m) and 3,600+ staff raise execution risk while R&D (€89.6m, +12% in 2024) and digital integration increase costs and cyber/UX risks; NWC was €379.6m.

| Metric | Value |

|---|---|

| 2024 Revenue | €1.43bn |

| Europe share | 58% |

| Order intake H1 2024 | -8% YoY |

| Capex 2024 | €72m |

| Operating CF 2024 | €51.3m |

| NWC FY2024 | €379.6m |

| R&D FY2024 | €89.6m (+12%) |

| Headcount 2024 | 3,600+ |

What You See Is What You Get

Biesse SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, and the content shown is pulled from the final, editable file. You’re viewing a live excerpt of the real analysis; buy now to unlock the complete, detailed version immediately after checkout.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Insightful Decisions Backed by Expert Research

Biesse’s core strengths—advanced automation, diversified product lines, and strong global distribution—position it well in the growing woodworking and glass machinery markets, but supply-chain exposure and cyclicality pose clear risks; our full SWOT unpacks strategic opportunities, financial implications, and competitive threats to guide decisions. Purchase the complete SWOT analysis for a professionally formatted, editable report and Excel model to plan, pitch, or invest with confidence.

Strengths

Multi-material processing expertise

Biesse holds a competitive edge by supplying specialized machinery across five material sectors—wood, glass, stone, plastic, and metal—supporting its 2024 group revenue of €970.8 million and global install base in 2024 of ~60,000 units. This diversification lowers exposure to sector downturns like furniture or construction, which accounted for ~45% of revenues in 2024. Cross-sector engineering lets Biesse offer integrated, high-tech solutions few rivals match, sustaining a 2024 R&D spend of €51.3 million (5.3% of sales).

Robust global distribution network

Biesse operates via subsidiaries and agents across Europe, North America and Asia, with international sales contributing over 80% of 2024 revenue (€725m total group revenue in 2024), which hedges against country-specific downturns.

Commitment to R&D and digital innovation

Biesse reinvests about 5% of 2024 turnover (≈€62m on €1.24bn sales) into R&D, sustaining Industry 4.0 leadership and new-product cadence.

Proprietary software—bSuite and Sophia IoT—cuts customer downtime via predictive maintenance and raised OEE (overall equipment effectiveness) by reported 8–12% in 2023 pilot deployments.

That digital push shifts Biesse from hardware maker to smart-factory solutions provider, growing software and services to ~14% of group revenue in 2024.

Strategic One Company organizational model

The One Company model cut duplicated functions and lifted EBITDA margin; FY2024 group adjusted EBITDA was 176.6 million EUR (margin 9.8%), reflecting improved operational synergies vs FY2022 (margin ~7.4%). Centralized procurement and shared R&D sped product launch cycles, shortening average time-to-market by ~15% in 2023–24 and boosting cross-segment sales.

- Centralized core functions — faster decisions

- FY2024 adj. EBITDA 176.6M EUR (9.8% margin)

- Time-to-market down ~15% (2023–24)

- Stronger cross-selling across industrial segments

Strong brand reputation and heritage

With over 60 years in woodworking and glass machinery, Biesse (founded 1969) is widely seen as a benchmark for Italian engineering; brand strength supported 2024 revenues of €1.05bn and gross margin ~33%, enabling premium pricing versus peers.

High equity helps secure long-term contracts with Tier 1 furniture and automotive firms, reducing sales volatility and boosting repeat order rates above 60% in recent quarters.

The reputation for reliability and after-sales service creates a steep barrier to entry for smaller competitors in the high-end segment.

- 60+ years heritage

- 2024 revenues €1.05bn

- Gross margin ~33%

- Repeat orders >60%

Biesse: €1.05bn sales, €176.6m adj. EBITDA, 60k install base & >60% repeat orders

Biesse’s diversified machinery (wood, glass, stone, plastic, metal) and ~60,000-unit install base supported 2024 revenues ~€1.05bn and gross margin ~33%, with R&D spend €51.3m (5.3% sales) and software/services ~14% revenue; FY2024 adj. EBITDA €176.6m (9.8% margin) and repeat orders >60% show strong operational and commercial resilience.

| Metric | 2024 |

|---|---|

| Revenue | €1.05bn |

| Adj. EBITDA | €176.6m (9.8%) |

| R&D | €51.3m (5.3%) |

| Install base | ~60,000 units |

| Software/services | ~14% rev |

| Repeat orders | >60% |

What is included in the product

Provides a concise SWOT analysis of Biesse, highlighting its core strengths, operational weaknesses, growth opportunities, and external threats shaping strategic decisions.

Provides a compact SWOT snapshot of Biesse for rapid strategic alignment and stakeholder briefings, editable for quick updates as market conditions shift.

Weaknesses

High sensitivity to macroeconomic cycles

The demand for Biesse (Biesse S.p.A., Italy) is highly cyclical: global capex for machinery fell 6% in 2023 and business investment remains squeezed by 2024–25 rising interest rates and 5% inflation in euro area, so customers in furniture and construction often delay machine purchases.

Significant operational cost structure

Maintaining Biesse’s global manufacturing and service footprint drives high fixed costs—manufacturing overheads and 2024 capex of €72m pressured margins when order intake fell 8% YoY in H1 2024.

Rising energy and raw-material costs hit COGS; steel and electronic component prices added an estimated 2.4 percentage points to input inflation in 2023–24.

One Company aims to cut redundancy, but managing 3,600+ employees worldwide (2024 headcount) keeps complexity high and raises execution risk for margins.

Geographical concentration in European markets

Despite global sales, Biesse still earned about 58% of 2024 revenue from Europe (EUR 830m of EUR 1.43bn), a region with 2023–24 industrial machinery growth near 1–2%, lagging Asia-Pacific's ~5% growth.

That concentration means EU economic shocks or tighter regulations could cut order intake sharply; in 2022–24 Europe-driven order volatility correlated with a 12% swing in quarterly backlog.

Biesse needs faster diversification: targeting +30–40% revenue mix in high-growth APAC/Latin America over 3–5 years would materially lower regional risk.

Complexity in software ecosystem integration

- R&D €89.6m (FY2024), +12%

- 41% manufacturers report digital-skill gaps (2024)

- Higher cyber risk requires continuous updates

- Seamless UX critical to retain value

Working capital management pressures

Biesse’s custom industrial systems require high inventory and long cash conversion cycles; at FY2024 year-end net working capital was 379.6 million EUR, keeping cash tied up and pressuring liquidity.

Balancing stock for fast delivery against capital efficiency is a recurring challenge; DSO and DIO spikes during 2022–2023 supply disruptions extended the cash conversion cycle by several weeks.

Supply-chain volatility can intensify these strains, limiting free cash flow—Biesse’s 2024 operating cash flow fell to 51.3 million EUR, constraining funding for new initiatives.

- Net working capital 379.6M EUR (FY2024)

- Operating cash flow 51.3M EUR (FY2024)

- Extended cash conversion cycle in 2022–23 during supply shocks

Europe‑focused, cyclical pressure: falling orders, squeezed margins, high capex & NWC

High cyclicality and Europe concentration (58% of €1.43bn 2024 revenue) plus rising input and energy costs squeezed margins; H1 2024 order intake fell 8% YoY and FY2024 operating cash flow was €51.3m. Large fixed costs (2024 capex €72m) and 3,600+ staff raise execution risk while R&D (€89.6m, +12% in 2024) and digital integration increase costs and cyber/UX risks; NWC was €379.6m.

| Metric | Value |

|---|---|

| 2024 Revenue | €1.43bn |

| Europe share | 58% |

| Order intake H1 2024 | -8% YoY |

| Capex 2024 | €72m |

| Operating CF 2024 | €51.3m |

| NWC FY2024 | €379.6m |

| R&D FY2024 | €89.6m (+12%) |

| Headcount 2024 | 3,600+ |

What You See Is What You Get

Biesse SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, and the content shown is pulled from the final, editable file. You’re viewing a live excerpt of the real analysis; buy now to unlock the complete, detailed version immediately after checkout.