Ballarpur Industries Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

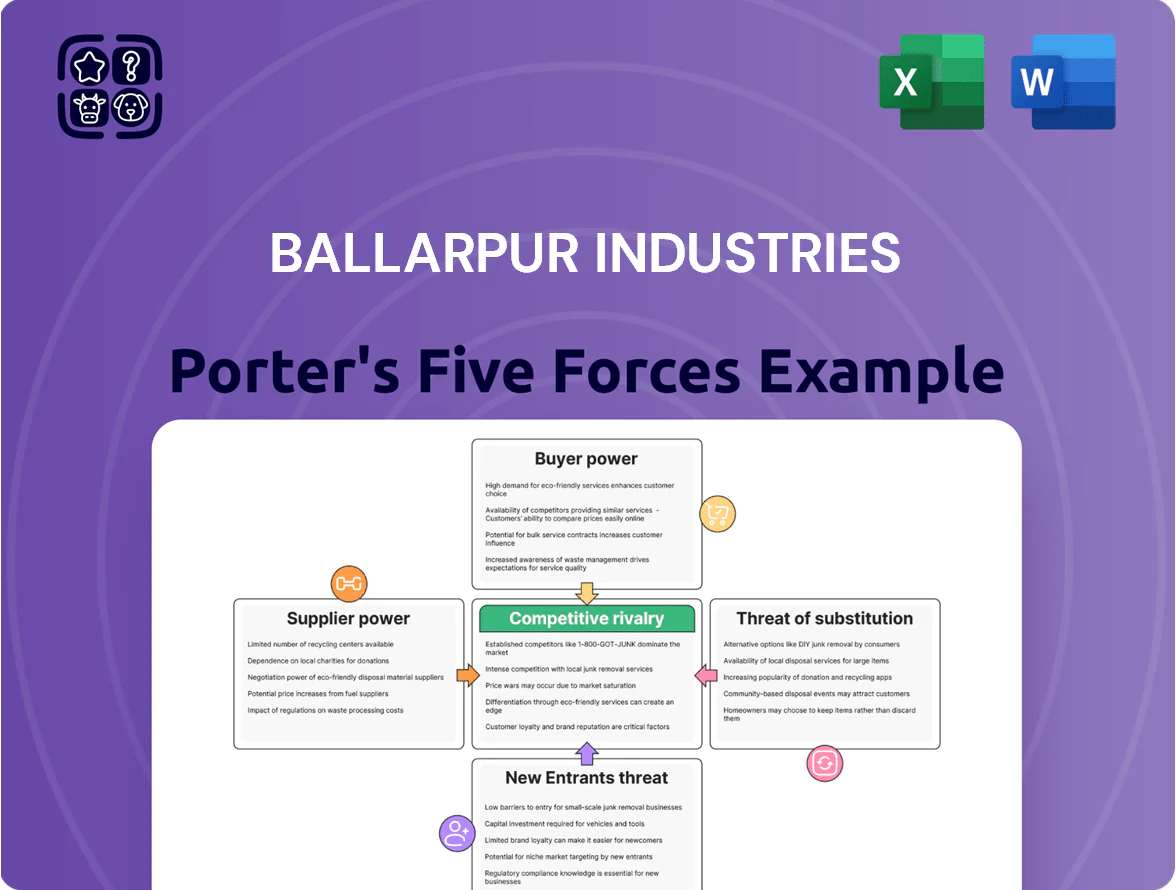

Ballarpur Industries faces moderate buyer leverage and concentrated raw-material supplier risks, while capital intensity and regulatory hurdles raise barriers for some new entrants; competitive rivalry is high amid price sensitivity in the paper sector.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Ballarpur Industries’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Raw Material Scarcity

Raw material scarcity: availability of wood pulp and waste paper is highly volatile due to tightening environmental rules and supply-chain shifts through 2025; global pulp prices rose ~18% year-on-year in 2024–25, pressuring margins. BILT depends on a few certified timber sources and international pulp suppliers, giving vendors pricing leverage—top 3 suppliers account for roughly 65% of input volumes. Disruptions in chemical additives or specialty pulp can raise variable costs by 6–10% and halt lines, cutting quarterly capacity by up to 12%.

Energy and Fuel Dependency

Paper making is energy-heavy, needing steady coal, grid power and gas; suppliers thus wield strong bargaining power since large mills in India lack cheap alternatives. BILT (Ballarpur Industries Ltd) faced input-cost pressure in 2025 as global thermal coal rose ~18% YTD and LNG spot prices averaged $12/MMBtu through Q3, forcing mill-level fuel costs up ~12–15% and compressing margins.

Concentration of Chemical Suppliers

Specialty coating and bleaching chemicals for paper come from a handful of specialist firms, giving suppliers strong bargaining power over BILT; global specialty chemical concentration is high—about 70% of supply for these grades is controlled by top 10 players as of 2024.

Technical locks and reformulation risk create high switching costs: a trial change can cut whiteness or tensile strength by 5–15%, so BILT rarely pressures prices.

The niche market and limited alternatives cap BILT’s negotiation leverage, keeping supplier-driven input cost inflation near the sector average of 3–6% annually in 2023–24.

Logistics and Transport Costs

Logistics and rail consolidation in India leaves Ballarpur Industries (BILT) reliant on a few large carriers; freight rate hikes and fuel surcharges raised transport costs by about 8–12% in FY2025, squeezing BILT’s pulp and paper gross margins by an estimated 120–180 bps.

Heavy loads mean limited modal alternatives, so logistics providers keep bargaining power high, reducing BILT’s ability to pass costs to end customers during 2024–25 demand softness.

- FY2025 freight/fuel +8–12%

- Estimated margin hit 120–180 bps

- Few rail/logistics providers = high supplier power

- Low modal flexibility for heavy loads

Import Dependence for High-Grade Pulp

BILT depends on high-quality long-fiber pulp mainly from North America and Scandinavia; in 2025 imports made up ~65% of its specialty pulp needs, raising supplier leverage.

Late-2025 currency swings (INR vs USD down ~8% YTD) and import duties (effective rise ~3 percentage points) boosted exporter pricing power and input-cost volatility.

That import reliance leaves BILT exposed to geopolitical risk and trade-policy shifts that can spike pulp costs and squeeze margins.

- ~65% specialty pulp imported (2025)

- INR down ~8% vs USD, 2025 YTD

- Import duty impact ≈ +3 pp late-2025

- High supplier leverage; geopolitics risk

Supplier concentration + fuel/currency shocks lift input inflation 3–6%, cut margins 120–180bps

Suppliers hold strong power: top 3 pulp vendors supply ~65% of inputs, specialty-chemical top-10 share ~70%, and imports cover ~65% of specialty pulp (2025), while coal/LNG fuel costs rose ~18% YTD and INR fell ~8% YTD—together lifting input inflation ~3–6% and cutting margins ~120–180 bps in FY2025.

| Metric | Value (2025) |

|---|---|

| Top-3 supplier share | ~65% |

| Specialty chemical top-10 | ~70% |

| Specialty pulp imports | ~65% |

| Coal/LNG price change (YTD) | ~+18% |

| INR vs USD (YTD) | ~-8% |

| Input inflation range | 3–6% |

| Estimated margin hit | 120–180 bps |

What is included in the product

Tailored exclusively for Ballarpur Industries, this Porter's Five Forces analysis uncovers key competitive drivers, supplier and buyer power, threats from substitutes and new entrants, and strategic levers to protect market share and profitability.

A concise Porter's Five Forces snapshot for Ballarpur Industries—instantly shows supplier/buyer leverage, competitive rivalry, threats from substitutes and entrants to speed strategic responses.

Customers Bargaining Power

Consolidation of Large Publishers

The publishing sector has consolidated: the top 5 Indian publishers now buy roughly 40% of domestic printing paper, creating a few large buyers that demand bulk discounts and 60–90+ day credit, cutting BILT’s margins by an estimated 150–300 bps in 2024.

Price Sensitivity in Education Sector

Low Switching Costs for Standard Grades

For commodity-grade uncoated paper, BILT faces low switching costs: product specs match peers so customers can move to ITC or JK Paper with minimal technical or financial friction. In FY2024 BILT’s domestic market-share in uncoated woodfree fell to ~14%, while ITC and JK Paper held ~18% and ~12% respectively, underscoring weak brand stickiness. That commoditization gives buyers clear leverage in price talks, squeezing margins.

Availability of Cheap Imports

Institutional buyers push BILT on price by threatening to switch to cheaper Southeast Asian paper; imports from Vietnam and Indonesia often undercut domestic quotes by 8–15% in 2025.

Low-duty imports surged 22% year-on-year in 2025, widening buyer choice and capping BILT’s pricing power to near global CIF benchmarks.

Demand for Sustainable Packaging

- 62% of CPG buyers prioritize supplier sustainability (2024)

- Key certifications: FSC, PEFC, ISO 14001

- Contract loss could cut 15–30% revenue

- One large contract ≈ INR 2.5–4.0 billion/year

BILT margins squeezed as concentrated buyers, imports and local mills bite pricing

Buyers are concentrated: top-5 publishers buy ~40% of domestic printing paper, forcing 60–90+ day credit and bulk discounts that cut BILT’s margins ~150–300 bps in 2024. About 45% of FY2024 revenue is price-sensitive notebook/textbook paper; a 5–8% price rise in 2024 caused peer volume declines and boosts switching to unbranded local mills (12% share in 2023). Low switching costs shrink BILT’s uncoated woodfree share to ~14% in FY2024 vs ITC 18%, JK 12%, giving buyers clear price leverage. Imports rose +22% in 2025 and undercut domestic prices by 8–15%, capping pricing to global CIF levels.

| Metric | Value |

|---|---|

| Top-5 buyer share | ~40% (printing paper) |

| BILT revenue exposure | ~45% (FY2024) |

| Unbranded local share | ~12% (2023) |

| BILT uncoated woodfree share | ~14% (FY2024) |

| Import rise | +22% (2025) |

| Import price gap | 8–15% (2025) |

| Margin pressure | ~150–300 bps (2024) |

Preview Before You Purchase

Ballarpur Industries Porter's Five Forces Analysis

This preview shows the exact Ballarpur Industries Porter’s Five Forces analysis you’ll receive—no placeholders, no samples—fully formatted and ready for immediate download upon purchase.

The document displayed is the complete, professionally written analysis, offering supplier power, buyer power, rivalry, threat of substitution, and entry barriers insights that you can use right away.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

Ballarpur Industries faces moderate buyer leverage and concentrated raw-material supplier risks, while capital intensity and regulatory hurdles raise barriers for some new entrants; competitive rivalry is high amid price sensitivity in the paper sector.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Ballarpur Industries’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Raw Material Scarcity

Raw material scarcity: availability of wood pulp and waste paper is highly volatile due to tightening environmental rules and supply-chain shifts through 2025; global pulp prices rose ~18% year-on-year in 2024–25, pressuring margins. BILT depends on a few certified timber sources and international pulp suppliers, giving vendors pricing leverage—top 3 suppliers account for roughly 65% of input volumes. Disruptions in chemical additives or specialty pulp can raise variable costs by 6–10% and halt lines, cutting quarterly capacity by up to 12%.

Energy and Fuel Dependency

Paper making is energy-heavy, needing steady coal, grid power and gas; suppliers thus wield strong bargaining power since large mills in India lack cheap alternatives. BILT (Ballarpur Industries Ltd) faced input-cost pressure in 2025 as global thermal coal rose ~18% YTD and LNG spot prices averaged $12/MMBtu through Q3, forcing mill-level fuel costs up ~12–15% and compressing margins.

Concentration of Chemical Suppliers

Specialty coating and bleaching chemicals for paper come from a handful of specialist firms, giving suppliers strong bargaining power over BILT; global specialty chemical concentration is high—about 70% of supply for these grades is controlled by top 10 players as of 2024.

Technical locks and reformulation risk create high switching costs: a trial change can cut whiteness or tensile strength by 5–15%, so BILT rarely pressures prices.

The niche market and limited alternatives cap BILT’s negotiation leverage, keeping supplier-driven input cost inflation near the sector average of 3–6% annually in 2023–24.

Logistics and Transport Costs

Logistics and rail consolidation in India leaves Ballarpur Industries (BILT) reliant on a few large carriers; freight rate hikes and fuel surcharges raised transport costs by about 8–12% in FY2025, squeezing BILT’s pulp and paper gross margins by an estimated 120–180 bps.

Heavy loads mean limited modal alternatives, so logistics providers keep bargaining power high, reducing BILT’s ability to pass costs to end customers during 2024–25 demand softness.

- FY2025 freight/fuel +8–12%

- Estimated margin hit 120–180 bps

- Few rail/logistics providers = high supplier power

- Low modal flexibility for heavy loads

Import Dependence for High-Grade Pulp

BILT depends on high-quality long-fiber pulp mainly from North America and Scandinavia; in 2025 imports made up ~65% of its specialty pulp needs, raising supplier leverage.

Late-2025 currency swings (INR vs USD down ~8% YTD) and import duties (effective rise ~3 percentage points) boosted exporter pricing power and input-cost volatility.

That import reliance leaves BILT exposed to geopolitical risk and trade-policy shifts that can spike pulp costs and squeeze margins.

- ~65% specialty pulp imported (2025)

- INR down ~8% vs USD, 2025 YTD

- Import duty impact ≈ +3 pp late-2025

- High supplier leverage; geopolitics risk

Supplier concentration + fuel/currency shocks lift input inflation 3–6%, cut margins 120–180bps

Suppliers hold strong power: top 3 pulp vendors supply ~65% of inputs, specialty-chemical top-10 share ~70%, and imports cover ~65% of specialty pulp (2025), while coal/LNG fuel costs rose ~18% YTD and INR fell ~8% YTD—together lifting input inflation ~3–6% and cutting margins ~120–180 bps in FY2025.

| Metric | Value (2025) |

|---|---|

| Top-3 supplier share | ~65% |

| Specialty chemical top-10 | ~70% |

| Specialty pulp imports | ~65% |

| Coal/LNG price change (YTD) | ~+18% |

| INR vs USD (YTD) | ~-8% |

| Input inflation range | 3–6% |

| Estimated margin hit | 120–180 bps |

What is included in the product

Tailored exclusively for Ballarpur Industries, this Porter's Five Forces analysis uncovers key competitive drivers, supplier and buyer power, threats from substitutes and new entrants, and strategic levers to protect market share and profitability.

A concise Porter's Five Forces snapshot for Ballarpur Industries—instantly shows supplier/buyer leverage, competitive rivalry, threats from substitutes and entrants to speed strategic responses.

Customers Bargaining Power

Consolidation of Large Publishers

The publishing sector has consolidated: the top 5 Indian publishers now buy roughly 40% of domestic printing paper, creating a few large buyers that demand bulk discounts and 60–90+ day credit, cutting BILT’s margins by an estimated 150–300 bps in 2024.

Price Sensitivity in Education Sector

Low Switching Costs for Standard Grades

For commodity-grade uncoated paper, BILT faces low switching costs: product specs match peers so customers can move to ITC or JK Paper with minimal technical or financial friction. In FY2024 BILT’s domestic market-share in uncoated woodfree fell to ~14%, while ITC and JK Paper held ~18% and ~12% respectively, underscoring weak brand stickiness. That commoditization gives buyers clear leverage in price talks, squeezing margins.

Availability of Cheap Imports

Institutional buyers push BILT on price by threatening to switch to cheaper Southeast Asian paper; imports from Vietnam and Indonesia often undercut domestic quotes by 8–15% in 2025.

Low-duty imports surged 22% year-on-year in 2025, widening buyer choice and capping BILT’s pricing power to near global CIF benchmarks.

Demand for Sustainable Packaging

- 62% of CPG buyers prioritize supplier sustainability (2024)

- Key certifications: FSC, PEFC, ISO 14001

- Contract loss could cut 15–30% revenue

- One large contract ≈ INR 2.5–4.0 billion/year

BILT margins squeezed as concentrated buyers, imports and local mills bite pricing

Buyers are concentrated: top-5 publishers buy ~40% of domestic printing paper, forcing 60–90+ day credit and bulk discounts that cut BILT’s margins ~150–300 bps in 2024. About 45% of FY2024 revenue is price-sensitive notebook/textbook paper; a 5–8% price rise in 2024 caused peer volume declines and boosts switching to unbranded local mills (12% share in 2023). Low switching costs shrink BILT’s uncoated woodfree share to ~14% in FY2024 vs ITC 18%, JK 12%, giving buyers clear price leverage. Imports rose +22% in 2025 and undercut domestic prices by 8–15%, capping pricing to global CIF levels.

| Metric | Value |

|---|---|

| Top-5 buyer share | ~40% (printing paper) |

| BILT revenue exposure | ~45% (FY2024) |

| Unbranded local share | ~12% (2023) |

| BILT uncoated woodfree share | ~14% (FY2024) |

| Import rise | +22% (2025) |

| Import price gap | 8–15% (2025) |

| Margin pressure | ~150–300 bps (2024) |

Preview Before You Purchase

Ballarpur Industries Porter's Five Forces Analysis

This preview shows the exact Ballarpur Industries Porter’s Five Forces analysis you’ll receive—no placeholders, no samples—fully formatted and ready for immediate download upon purchase.

The document displayed is the complete, professionally written analysis, offering supplier power, buyer power, rivalry, threat of substitution, and entry barriers insights that you can use right away.