Hangzhou Binjiang Real Estate Group Co.Ltd Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

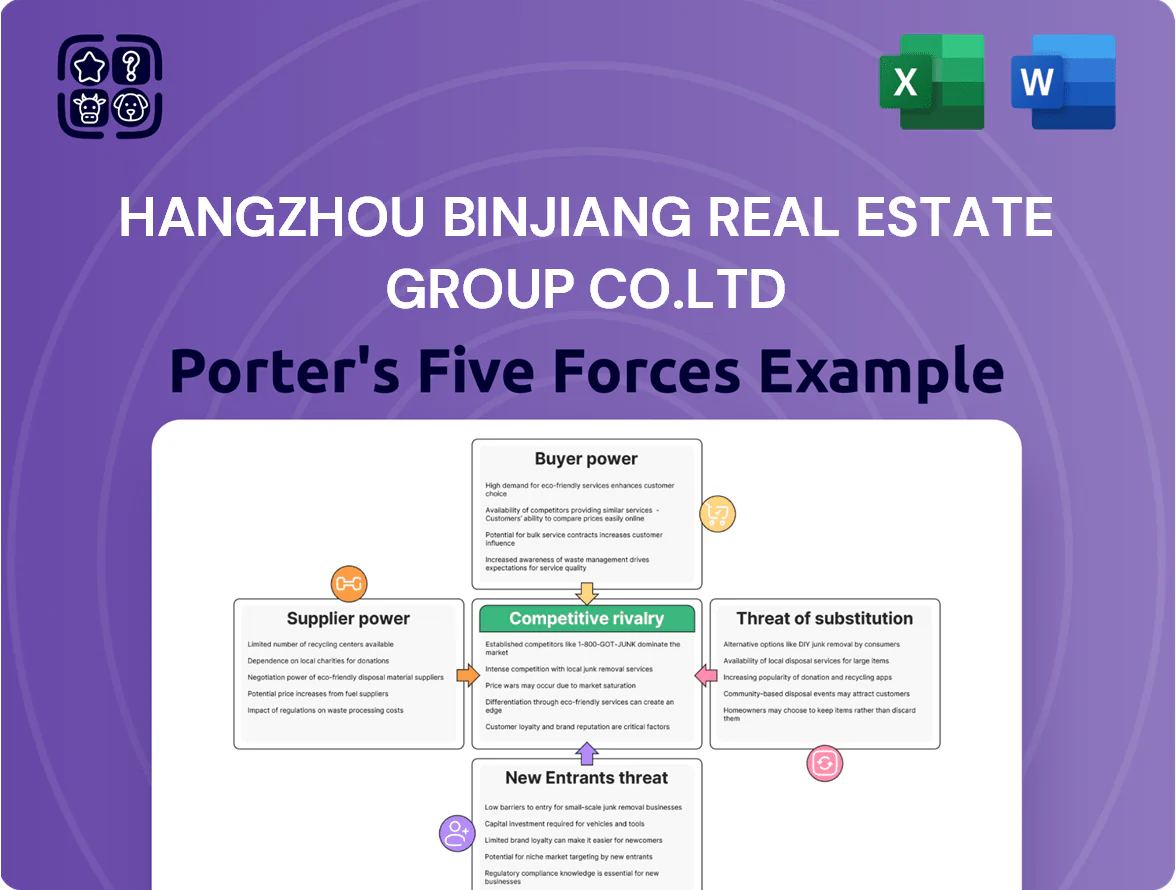

Hangzhou Binjiang Real Estate Group faces intense competitive rivalry and strong buyer sensitivity in China’s crowded property sector, while regulatory shifts and supplier constraints shape margins and project timelines.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Hangzhou Binjiang Real Estate Group Co.Ltd’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Government Control Over Land Supply

The Hangzhou and Zhejiang governments control >95% of developable land via state land auctions, setting price floors that made municipal land revenues in Zhejiang 2024 reach RMB 320 billion, so Binjiang is forced to accept auctioned prices and timing.

Centralized land allocation and strict auction rules compress Binjiang’s margin: average land premium rates in Hangzhou rose to ~22% in 2024, leaving developers as price takers with limited negotiation power.

Access to Institutional Capital and Financing

Financial institutions and bond markets supply crucial liquidity for capital-heavy projects; in 2024 Binjiang raised about CNY 6.2 billion via bonds and bank loans, giving suppliers pricing power.

Binjiang’s credit sits above many provincial peers—onshore bond spreads averaged ~220 bps in 2024—but macro‑prudential caps and PBOC policy rates limit its ability to demand looser terms.

Tighter sector lending rules since 2021 mean banks set strict covenants and loan-to-value ratios, so lenders retain meaningful leverage over project financing.

Fluctuations in Raw Material Costs

Suppliers of steel, cement and glass face commodity cycles and China's 2024–25 environmental curbs raised domestic cement prices ~12% YoY and steel HRC spot up ~18% in 2025, squeezing margins for developers.

Binjiang, positioned as a high-end developer, needs premium specs and has low switching ability, so supplier leverage is high.

Upstream cost spikes are hard to pass to buyers because pre-sale price caps and down-payment regulations limit immediate price increases.

Availability of Skilled Construction Labor

The aging construction workforce in China and rising demand for finer craftsmanship have tightened supply; by 2024, skilled construction labor shortages were cited by 62% of Chinese developers, raising bid wages ~8–12% in Zhejiang province.

Binjiang depends on contractor networks facing these pressures for complex projects, so established firms and specialist crews hold moderate bargaining power over timelines and fees.

- 62% developers report skilled shortages (2024)

- Zhejiang bid wages up 8–12% (2023–24)

- Moderate supplier power on timelines and fees

Dependency on Specialized Design and Architecture Firms

To keep luxury appeal, Binjiang relies on a handful of elite design firms; in 2024 top-tier architects drove 8–12% higher average selling prices on comparable Hangzhou projects, so these firms hold pricing leverage.

Their IP, showroom projects, and brand cachet raise marketing lift and give suppliers bargaining power over fees, timelines, and exclusivity clauses—Binjiang faces limited supplier substitution.

- Top design firms = 8–12% price uplift

- Few firms → higher contract leverage

- IP/brand drives marketing value

Zhejiang land boom, rising input costs and tight finance squeeze developers

State-controlled land auctions and 2024 Zhejiang municipal land receipts of RMB 320bn force Binjiang to accept prices; Hangzhou land premiums ~22% (2024). Bond/bank funding CNY 6.2bn (2024) and 220bps average onshore spreads give financiers leverage; tighter lending caps and LTVs persist. Commodity spikes (cement +12% 2024, steel HRC +18% 2025) plus skilled labor shortages (62% developers, wages +8–12% Zhejiang) raise supplier power.

| Metric | Value |

|---|---|

| Zhejiang municipal land revenue 2024 | RMB 320bn |

| Hangzhou land premium rate 2024 | ~22% |

| Binjiang financing 2024 | CNY 6.2bn |

| Onshore bond spreads avg 2024 | ~220 bps |

| Cement price change 2024 | +12% YoY |

| Steel HRC spot change 2025 | +18% YoY |

| Developers reporting skilled shortages 2024 | 62% |

| Zhejiang bid wage rise 2023–24 | +8–12% |

What is included in the product

Tailored Porter's Five Forces analysis for Hangzhou Binjiang Real Estate Group Co.Ltd, uncovering competitive drivers, buyer/supplier power, entry barriers, substitutes, and disruptive threats that shape pricing, profitability, and strategic positioning within the Chinese real estate market.

A concise Porter's Five Forces snapshot for Hangzhou Binjiang Real Estate Group—quickly highlights competitive intensity, supplier/buyer leverage, threat of new entrants and substitutes to inform capital allocation and strategic moves.

Customers Bargaining Power

Impact of Government Purchase Restrictions

Individual homebuyers in Tier 1 and hot Tier 2 Chinese cities face strict eligibility rules and minimum down payments often 30%–50%, which cut the buyer pool by an estimated 20%–35% versus 2019 levels (China Real Estate Association, 2024).

That smaller, qualified group gains pricing leverage, raising negotiation power and pressuring margins on Binjiang launches; in 2024 Binjiang saw 12% slower sell-through in restricted cities.

Binjiang must align pricing, financing offers, and presales timing to policy shifts to maintain >70% first-year absorption on new projects.

Increased Price Sensitivity and Market Sentiment

Following mid-2020s property volatility, Chinese buyers have grown data-driven and cautious; 2024 surveys show 62% of urban homebuyers list developer solvency and delivery record as top purchase criteria, boosting customer price sensitivity.

Buyers now demand stronger guarantees, higher build quality, and better amenities, shifting negotiation power and pressuring Binjiang to offer tighter contractual delivery terms and warranties.

To win discerning investors, Binjiang must boost brand trust and transparency; its 2023 liability-to-asset ratio of ~68% and slower cash collection raise scrutiny, so clearer reporting and third-party audits are needed.

Availability of Secondary Market Alternatives

Rising pre-owned inventory in Hangzhou—estimated at 78,000 resale units in 2024, up 12% year-on-year—gives buyers a ready alternative to Binjiang’s new projects, widening choice and bargaining leverage.

Buyers weigh immediate occupancy and proven neighborhood services of secondary homes versus paying a 8–12% premium for new builds, pressuring Binjiang on pricing and incentives in mature urban districts.

Information Transparency and Digital Platforms

The rise of data platforms (eg. Fang, Anjuke, Lianjia) lets buyers compare price/sqm, historical appreciation and developer track records; in 2024 online listings influenced 42% of Chinese home purchases, raising buyer bargaining power.

Transparency cuts developer-favored information asymmetry, so Binjiang must align pricing with market benchmarks and publish clear product specs to avoid markdowns and slower sell-through.

- 2024: 42% purchases influenced by online listings

- Compare: price/sqm, 5-yr appreciation, developer rating

- Action: transparent pricing, clear specs, faster disclosures

Influence of Mortgage Rates and Credit Availability

Customer bargaining power for Hangzhou Binjiang Real Estate Group hinges on mortgage costs and bank lending: China benchmark one-year loan prime rate (LPR) was 3.55% as of Dec 2025, and local mortgage approval quotas tightened in 2024–25, cutting effective demand and pushing developers to offer cash discounts or extended payment plans.

In low-rate periods buyers have more buying power but stay selective, prioritizing developers with stronger warranties, completed projects, or higher rental yield — Binjiang must compete on quality, not just price.

- High rates/low credit → lower demand, more discounts

- Dec 2025 LPR 3.55% → cheaper borrowing vs 2023 peaks

- Buyers in low-rate cycle focus on long-term value

- Binjiang advantage: completed inventory and warranty strength

Binjiang must boost transparency, warranties & financing to secure 70%+ first-year sales

Buyers have high bargaining power: tighter mortgage rules and 3.55% LPR (Dec 2025) shrink demand, 62% cite developer solvency (2024), resale supply in Hangzhou +12% y/y (78,000 units, 2024), online listings influenced 42% purchases (2024); Binjiang must boost transparency, warranties, and flexible financing to keep >70% first-year absorption.

| Metric | Value |

|---|---|

| LPR (Dec 2025) | 3.55% |

| Buyer solvency concern (2024) | 62% |

| Hangzhou resale stock (2024) | 78,000 (+12%) |

| Online influence (2024) | 42% |

What You See Is What You Get

Hangzhou Binjiang Real Estate Group Co.Ltd Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Hangzhou Binjiang Real Estate Group Co. Ltd you'll receive—no placeholders, no samples, fully formatted and ready for immediate download after purchase.

The document covers supplier power, buyer power, competitive rivalry, threat of substitutes, and barriers to entry with concise industry-specific insights and actionable implications for strategy and valuation.

You're viewing the final deliverable; once you complete your purchase, this identical file will be available for instant use in reports, presentations, or decision-making.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

Hangzhou Binjiang Real Estate Group faces intense competitive rivalry and strong buyer sensitivity in China’s crowded property sector, while regulatory shifts and supplier constraints shape margins and project timelines.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Hangzhou Binjiang Real Estate Group Co.Ltd’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Government Control Over Land Supply

The Hangzhou and Zhejiang governments control >95% of developable land via state land auctions, setting price floors that made municipal land revenues in Zhejiang 2024 reach RMB 320 billion, so Binjiang is forced to accept auctioned prices and timing.

Centralized land allocation and strict auction rules compress Binjiang’s margin: average land premium rates in Hangzhou rose to ~22% in 2024, leaving developers as price takers with limited negotiation power.

Access to Institutional Capital and Financing

Financial institutions and bond markets supply crucial liquidity for capital-heavy projects; in 2024 Binjiang raised about CNY 6.2 billion via bonds and bank loans, giving suppliers pricing power.

Binjiang’s credit sits above many provincial peers—onshore bond spreads averaged ~220 bps in 2024—but macro‑prudential caps and PBOC policy rates limit its ability to demand looser terms.

Tighter sector lending rules since 2021 mean banks set strict covenants and loan-to-value ratios, so lenders retain meaningful leverage over project financing.

Fluctuations in Raw Material Costs

Suppliers of steel, cement and glass face commodity cycles and China's 2024–25 environmental curbs raised domestic cement prices ~12% YoY and steel HRC spot up ~18% in 2025, squeezing margins for developers.

Binjiang, positioned as a high-end developer, needs premium specs and has low switching ability, so supplier leverage is high.

Upstream cost spikes are hard to pass to buyers because pre-sale price caps and down-payment regulations limit immediate price increases.

Availability of Skilled Construction Labor

The aging construction workforce in China and rising demand for finer craftsmanship have tightened supply; by 2024, skilled construction labor shortages were cited by 62% of Chinese developers, raising bid wages ~8–12% in Zhejiang province.

Binjiang depends on contractor networks facing these pressures for complex projects, so established firms and specialist crews hold moderate bargaining power over timelines and fees.

- 62% developers report skilled shortages (2024)

- Zhejiang bid wages up 8–12% (2023–24)

- Moderate supplier power on timelines and fees

Dependency on Specialized Design and Architecture Firms

To keep luxury appeal, Binjiang relies on a handful of elite design firms; in 2024 top-tier architects drove 8–12% higher average selling prices on comparable Hangzhou projects, so these firms hold pricing leverage.

Their IP, showroom projects, and brand cachet raise marketing lift and give suppliers bargaining power over fees, timelines, and exclusivity clauses—Binjiang faces limited supplier substitution.

- Top design firms = 8–12% price uplift

- Few firms → higher contract leverage

- IP/brand drives marketing value

Zhejiang land boom, rising input costs and tight finance squeeze developers

State-controlled land auctions and 2024 Zhejiang municipal land receipts of RMB 320bn force Binjiang to accept prices; Hangzhou land premiums ~22% (2024). Bond/bank funding CNY 6.2bn (2024) and 220bps average onshore spreads give financiers leverage; tighter lending caps and LTVs persist. Commodity spikes (cement +12% 2024, steel HRC +18% 2025) plus skilled labor shortages (62% developers, wages +8–12% Zhejiang) raise supplier power.

| Metric | Value |

|---|---|

| Zhejiang municipal land revenue 2024 | RMB 320bn |

| Hangzhou land premium rate 2024 | ~22% |

| Binjiang financing 2024 | CNY 6.2bn |

| Onshore bond spreads avg 2024 | ~220 bps |

| Cement price change 2024 | +12% YoY |

| Steel HRC spot change 2025 | +18% YoY |

| Developers reporting skilled shortages 2024 | 62% |

| Zhejiang bid wage rise 2023–24 | +8–12% |

What is included in the product

Tailored Porter's Five Forces analysis for Hangzhou Binjiang Real Estate Group Co.Ltd, uncovering competitive drivers, buyer/supplier power, entry barriers, substitutes, and disruptive threats that shape pricing, profitability, and strategic positioning within the Chinese real estate market.

A concise Porter's Five Forces snapshot for Hangzhou Binjiang Real Estate Group—quickly highlights competitive intensity, supplier/buyer leverage, threat of new entrants and substitutes to inform capital allocation and strategic moves.

Customers Bargaining Power

Impact of Government Purchase Restrictions

Individual homebuyers in Tier 1 and hot Tier 2 Chinese cities face strict eligibility rules and minimum down payments often 30%–50%, which cut the buyer pool by an estimated 20%–35% versus 2019 levels (China Real Estate Association, 2024).

That smaller, qualified group gains pricing leverage, raising negotiation power and pressuring margins on Binjiang launches; in 2024 Binjiang saw 12% slower sell-through in restricted cities.

Binjiang must align pricing, financing offers, and presales timing to policy shifts to maintain >70% first-year absorption on new projects.

Increased Price Sensitivity and Market Sentiment

Following mid-2020s property volatility, Chinese buyers have grown data-driven and cautious; 2024 surveys show 62% of urban homebuyers list developer solvency and delivery record as top purchase criteria, boosting customer price sensitivity.

Buyers now demand stronger guarantees, higher build quality, and better amenities, shifting negotiation power and pressuring Binjiang to offer tighter contractual delivery terms and warranties.

To win discerning investors, Binjiang must boost brand trust and transparency; its 2023 liability-to-asset ratio of ~68% and slower cash collection raise scrutiny, so clearer reporting and third-party audits are needed.

Availability of Secondary Market Alternatives

Rising pre-owned inventory in Hangzhou—estimated at 78,000 resale units in 2024, up 12% year-on-year—gives buyers a ready alternative to Binjiang’s new projects, widening choice and bargaining leverage.

Buyers weigh immediate occupancy and proven neighborhood services of secondary homes versus paying a 8–12% premium for new builds, pressuring Binjiang on pricing and incentives in mature urban districts.

Information Transparency and Digital Platforms

The rise of data platforms (eg. Fang, Anjuke, Lianjia) lets buyers compare price/sqm, historical appreciation and developer track records; in 2024 online listings influenced 42% of Chinese home purchases, raising buyer bargaining power.

Transparency cuts developer-favored information asymmetry, so Binjiang must align pricing with market benchmarks and publish clear product specs to avoid markdowns and slower sell-through.

- 2024: 42% purchases influenced by online listings

- Compare: price/sqm, 5-yr appreciation, developer rating

- Action: transparent pricing, clear specs, faster disclosures

Influence of Mortgage Rates and Credit Availability

Customer bargaining power for Hangzhou Binjiang Real Estate Group hinges on mortgage costs and bank lending: China benchmark one-year loan prime rate (LPR) was 3.55% as of Dec 2025, and local mortgage approval quotas tightened in 2024–25, cutting effective demand and pushing developers to offer cash discounts or extended payment plans.

In low-rate periods buyers have more buying power but stay selective, prioritizing developers with stronger warranties, completed projects, or higher rental yield — Binjiang must compete on quality, not just price.

- High rates/low credit → lower demand, more discounts

- Dec 2025 LPR 3.55% → cheaper borrowing vs 2023 peaks

- Buyers in low-rate cycle focus on long-term value

- Binjiang advantage: completed inventory and warranty strength

Binjiang must boost transparency, warranties & financing to secure 70%+ first-year sales

Buyers have high bargaining power: tighter mortgage rules and 3.55% LPR (Dec 2025) shrink demand, 62% cite developer solvency (2024), resale supply in Hangzhou +12% y/y (78,000 units, 2024), online listings influenced 42% purchases (2024); Binjiang must boost transparency, warranties, and flexible financing to keep >70% first-year absorption.

| Metric | Value |

|---|---|

| LPR (Dec 2025) | 3.55% |

| Buyer solvency concern (2024) | 62% |

| Hangzhou resale stock (2024) | 78,000 (+12%) |

| Online influence (2024) | 42% |

What You See Is What You Get

Hangzhou Binjiang Real Estate Group Co.Ltd Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Hangzhou Binjiang Real Estate Group Co. Ltd you'll receive—no placeholders, no samples, fully formatted and ready for immediate download after purchase.

The document covers supplier power, buyer power, competitive rivalry, threat of substitutes, and barriers to entry with concise industry-specific insights and actionable implications for strategy and valuation.

You're viewing the final deliverable; once you complete your purchase, this identical file will be available for instant use in reports, presentations, or decision-making.