Biocon Marketing Mix

Go Beyond the Snapshot—Get the Full Strategy

Discover how Biocon’s product innovation, tiered pricing, targeted distribution, and scientific promotions combine to drive growth—this concise preview highlights key tactics and market positioning. The full 4P’s Marketing Mix Analysis delivers an editable, presentation-ready deep dive with data, examples, and strategic recommendations to save time and power decisions—get instant access to apply these insights to business planning or coursework.

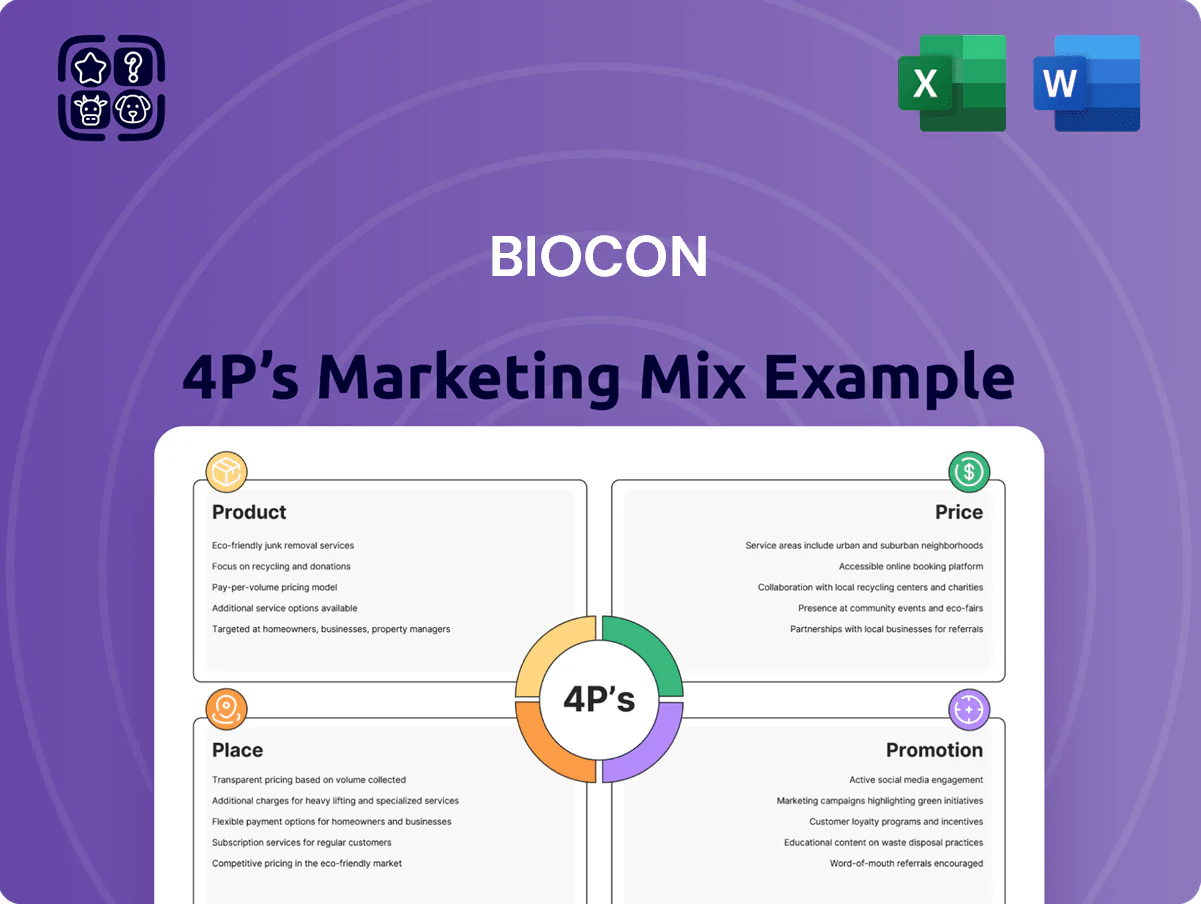

Product

Comprehensive Biosimilars Portfolio

Biocon’s Comprehensive Biosimilars Portfolio includes recombinant human insulin, insulin glargine, and oncology/immunology monoclonal antibodies; by Dec 31, 2025 it added advanced pipeline assets bDenosumab and bUstekinumab, growing biosimilars revenue to ~INR 2,400 crore (FY2025) and serving 50+ countries with lower-cost alternatives to innovator biologics for chronic care.

Generic Active Pharmaceutical Ingredients

Biocon’s Generic Active Pharmaceutical Ingredients (APIs) division manufactures complex APIs—fermentation-derived small molecules and synthetic compounds—supplying cardiovascular and antidiabetic medicines; in FY2024 the API segment contributed about 18% of consolidated revenue, roughly INR 1,380 crore (US$165m).

The API portfolio underpins Biocon’s internal biologics and formulations lines and serves 300+ third-party pharma clients across 50 countries, supporting finished-dose production and export-led growth.

Advanced fermentation capacity and six GMP plants keep gross margins higher than commodity APIs, with API EBITDA margin reported near 22% in FY2024, sustaining R&D investment for complex molecule scale-up.

Contract Research and Manufacturing Services

Through subsidiary Syngene International, Biocon offers integrated discovery, development, and manufacturing services to pharma and biotech clients, covering medicinal chemistry, biology, and clinical trials in world-class labs.

This CRAMS (contract research and manufacturing services) arm reported revenue of INR 6.2 billion in FY2024 (about USD 75m) and long-term deals with clients like Amgen and Baxter, providing steady cash flow.

The segment leverages Biocon’s scientific talent and scale to drive margin stability and R&D partnerships, supporting group EBITDA resilience and reducing product-market risk.

Novel Biologics and R&D Pipeline

Biocon has pivoted to research-led growth, investing over $200m in R&D in FY2024 to advance novel biologics for oncology and autoimmune disorders.

Its pipeline prioritizes first-in-class/best-in-class molecules such as Itolizumab for psoriasis and inflammatory diseases, targeting global markets with ongoing Phase II/III trials as of Dec 2025.

These assets shift Biocon from generics to a biopharma leader, aiming for higher-margin biologics and partnered commercialization deals that could lift EBITDA margins above 20% long-term.

- R&D spend: ~$200m FY2024

- Key asset: Itolizumab—Phase II/III (Dec 2025)

- Focus: oncology, autoimmune

- Strategic shift: generics → research-driven biologics

Specialized Therapeutic Focus Areas

Biocon’s product mix targets high-growth therapy areas—oncology, immunology, nephrology—driving 2024 revenue concentration: oncology biosimilars like Trastuzumab and Bevacizumab contributed about 42% of specialty sales, supporting global market access across 60+ countries.

This focus yields technical moats in complex biologics manufacturing, sustaining higher gross margins (around 47% in FY2024) and faster R&D-to-market cycles for line extensions.

Here’s the quick math: oncology share 42%, gross margin 47% (FY2024), presence 60+ countries—so market fit plus scale equals competitive edge.

- Oncology-led portfolio: Trastuzumab, Bevacizumab

- 42% specialty sales from oncology (2024)

- 47% gross margin (FY2024)

- Market reach: 60+ countries

Biocon: INR 2,400cr biosimilars, 47% gross margin, oncology 42%, 60+ countries

Biocon products: biosimilars (insulins, trastuzumab, bevacizumab, bDenosumab, bUstekinumab) drove FY2025 biosimilars revenue ~INR 2,400 crore; APIs ~INR 1,380 crore (FY2024); Syngene CRAMS revenue INR 620 crore (FY2024); R&D >$200m (FY2024); oncology = 42% specialty sales; gross margin ~47% (FY2024); presence 60+ countries.

| Metric | Value |

|---|---|

| Biosimilars rev FY2025 | INR 2,400 cr |

| API rev FY2024 | INR 1,380 cr |

| Syngene rev FY2024 | INR 620 cr |

| R&D FY2024 | $200m+ |

| Oncology share | 42% |

| Gross margin FY2024 | 47% |

| Market reach | 60+ countries |

What is included in the product

Delivers a professionally written, company-specific deep dive into Biocon’s Product, Price, Place, and Promotion strategies, ideal for managers, consultants, and marketers needing a complete breakdown of the company’s marketing positioning grounded in real brand practices and competitive context.

Condenses Biocon’s 4P insights into a concise, leadership-ready snapshot that simplifies product, price, place, and promotion strategy for quick decision-making and stakeholder alignment.

Place

Global Manufacturing and Supply Chain

Biocon runs state-of-the-art manufacturing in Bangalore and a large insulin plant in Malaysia, with combined capacity supporting global sales to 100+ countries; in FY2024 Biocon's Biologics segment reported revenue of INR 2,160 crore (≈USD 260m) driven by insulin and biosimilars. Both sites hold approvals from US FDA and EMA and clear routine audits, enabling a resilient supply chain that reduced lead times by ~15% after 2022 logistics upgrades.

Integration of Viatris Biosimilars Business

The integration of the Viatris biosimilars unit expanded Biocon Biologics' commercial reach into the US and EU, adding ~$350m of incremental annualized revenue run-rate by 2024 and increasing branded biosimilar presence across 12 new markets.

Owning front-end commercialization and distribution gives Biocon direct control over pricing, launch sequencing, and payer negotiations, cutting third-party margins and improving gross-to-net by an estimated 3–5 percentage points.

Full value-chain ownership lets Biocon manage key account relationships and channel strategy, supporting faster uptake—US market share gains of 1.5–2.0% for core biosimilars within 18 months post-integration.

Dominant Domestic Market Presence

Biocon’s domestic reach uses 12 warehouses, 250+ clearing and forwarding agents, and a 1,800-member sales force to supply major hospitals, 8,500 specialized clinics, and ~40,000 retail pharmacies across India; this network drove domestic revenues of ₹2,150 crore in FY2024, cementing Biocon as a household name in diabetes and cancer care.

Strategic Expansion into Emerging Markets

Biocon has expanded in Southeast Asia, Africa and Latin America via local partners and government tenders, capturing share in markets where biosimilar demand grows as healthcare spend rises (e.g., SEA pharma spend projected +6.2% CAGR to 2025).

Affordable biosimilars meet unmet needs; Biocon reported international revenue of ~Rs 2,400 crore in FY2024, with emerging markets a key driver.

Local distributors help clear regulatory hurdles, secure tenders, and ensure timely supply across diverse patient groups.

- Presence: SEA, Africa, LATAM via partners

- Demand: rising healthcare spend, +6% CAGR regionally

- Financials: international revenue ~Rs 2,400 cr FY2024

- Advantage: local regs navigation, faster market access

Digital Distribution and Health Platforms

- Digital orders ~22% of specialty sales (2024)

- Time-to-market reduced ~18%

- Real-time inventory cuts stockouts, speeds deliveries

- Lower logistics cost per unit, higher provider engagement

Biocon scales biologics: ₹2,160cr FY24, ₹2,400cr intl, $350M Viatris boost

Biocon maintains FDA/EMA-approved plants in Bangalore and Malaysia, serving 100+ countries; FY2024 Biologics revenue ₹2,160cr and international revenue ~₹2,400cr. Viatris deal added ~$350m run-rate and 12 markets. Domestic network: 12 warehouses, 1,800 sales reps, ~40,000 pharmacies. Digital orders 22% of specialty sales; time-to-market cut ~18%.

| Metric | Value |

|---|---|

| Biologics rev FY2024 | ₹2,160cr |

| International rev FY2024 | ₹2,400cr |

| Viatris add | $350m run-rate |

| Digital orders | 22% |

What You Preview Is What You Download

Biocon 4P's Marketing Mix Analysis

The preview shown here is the actual Biocon 4P's Marketing Mix document you’ll receive instantly after purchase—no surprises; it’s the exact, fully complete analysis ready for immediate use.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Snapshot—Get the Full Strategy

Discover how Biocon’s product innovation, tiered pricing, targeted distribution, and scientific promotions combine to drive growth—this concise preview highlights key tactics and market positioning. The full 4P’s Marketing Mix Analysis delivers an editable, presentation-ready deep dive with data, examples, and strategic recommendations to save time and power decisions—get instant access to apply these insights to business planning or coursework.

Product

Comprehensive Biosimilars Portfolio

Biocon’s Comprehensive Biosimilars Portfolio includes recombinant human insulin, insulin glargine, and oncology/immunology monoclonal antibodies; by Dec 31, 2025 it added advanced pipeline assets bDenosumab and bUstekinumab, growing biosimilars revenue to ~INR 2,400 crore (FY2025) and serving 50+ countries with lower-cost alternatives to innovator biologics for chronic care.

Generic Active Pharmaceutical Ingredients

Biocon’s Generic Active Pharmaceutical Ingredients (APIs) division manufactures complex APIs—fermentation-derived small molecules and synthetic compounds—supplying cardiovascular and antidiabetic medicines; in FY2024 the API segment contributed about 18% of consolidated revenue, roughly INR 1,380 crore (US$165m).

The API portfolio underpins Biocon’s internal biologics and formulations lines and serves 300+ third-party pharma clients across 50 countries, supporting finished-dose production and export-led growth.

Advanced fermentation capacity and six GMP plants keep gross margins higher than commodity APIs, with API EBITDA margin reported near 22% in FY2024, sustaining R&D investment for complex molecule scale-up.

Contract Research and Manufacturing Services

Through subsidiary Syngene International, Biocon offers integrated discovery, development, and manufacturing services to pharma and biotech clients, covering medicinal chemistry, biology, and clinical trials in world-class labs.

This CRAMS (contract research and manufacturing services) arm reported revenue of INR 6.2 billion in FY2024 (about USD 75m) and long-term deals with clients like Amgen and Baxter, providing steady cash flow.

The segment leverages Biocon’s scientific talent and scale to drive margin stability and R&D partnerships, supporting group EBITDA resilience and reducing product-market risk.

Novel Biologics and R&D Pipeline

Biocon has pivoted to research-led growth, investing over $200m in R&D in FY2024 to advance novel biologics for oncology and autoimmune disorders.

Its pipeline prioritizes first-in-class/best-in-class molecules such as Itolizumab for psoriasis and inflammatory diseases, targeting global markets with ongoing Phase II/III trials as of Dec 2025.

These assets shift Biocon from generics to a biopharma leader, aiming for higher-margin biologics and partnered commercialization deals that could lift EBITDA margins above 20% long-term.

- R&D spend: ~$200m FY2024

- Key asset: Itolizumab—Phase II/III (Dec 2025)

- Focus: oncology, autoimmune

- Strategic shift: generics → research-driven biologics

Specialized Therapeutic Focus Areas

Biocon’s product mix targets high-growth therapy areas—oncology, immunology, nephrology—driving 2024 revenue concentration: oncology biosimilars like Trastuzumab and Bevacizumab contributed about 42% of specialty sales, supporting global market access across 60+ countries.

This focus yields technical moats in complex biologics manufacturing, sustaining higher gross margins (around 47% in FY2024) and faster R&D-to-market cycles for line extensions.

Here’s the quick math: oncology share 42%, gross margin 47% (FY2024), presence 60+ countries—so market fit plus scale equals competitive edge.

- Oncology-led portfolio: Trastuzumab, Bevacizumab

- 42% specialty sales from oncology (2024)

- 47% gross margin (FY2024)

- Market reach: 60+ countries

Biocon: INR 2,400cr biosimilars, 47% gross margin, oncology 42%, 60+ countries

Biocon products: biosimilars (insulins, trastuzumab, bevacizumab, bDenosumab, bUstekinumab) drove FY2025 biosimilars revenue ~INR 2,400 crore; APIs ~INR 1,380 crore (FY2024); Syngene CRAMS revenue INR 620 crore (FY2024); R&D >$200m (FY2024); oncology = 42% specialty sales; gross margin ~47% (FY2024); presence 60+ countries.

| Metric | Value |

|---|---|

| Biosimilars rev FY2025 | INR 2,400 cr |

| API rev FY2024 | INR 1,380 cr |

| Syngene rev FY2024 | INR 620 cr |

| R&D FY2024 | $200m+ |

| Oncology share | 42% |

| Gross margin FY2024 | 47% |

| Market reach | 60+ countries |

What is included in the product

Delivers a professionally written, company-specific deep dive into Biocon’s Product, Price, Place, and Promotion strategies, ideal for managers, consultants, and marketers needing a complete breakdown of the company’s marketing positioning grounded in real brand practices and competitive context.

Condenses Biocon’s 4P insights into a concise, leadership-ready snapshot that simplifies product, price, place, and promotion strategy for quick decision-making and stakeholder alignment.

Place

Global Manufacturing and Supply Chain

Biocon runs state-of-the-art manufacturing in Bangalore and a large insulin plant in Malaysia, with combined capacity supporting global sales to 100+ countries; in FY2024 Biocon's Biologics segment reported revenue of INR 2,160 crore (≈USD 260m) driven by insulin and biosimilars. Both sites hold approvals from US FDA and EMA and clear routine audits, enabling a resilient supply chain that reduced lead times by ~15% after 2022 logistics upgrades.

Integration of Viatris Biosimilars Business

The integration of the Viatris biosimilars unit expanded Biocon Biologics' commercial reach into the US and EU, adding ~$350m of incremental annualized revenue run-rate by 2024 and increasing branded biosimilar presence across 12 new markets.

Owning front-end commercialization and distribution gives Biocon direct control over pricing, launch sequencing, and payer negotiations, cutting third-party margins and improving gross-to-net by an estimated 3–5 percentage points.

Full value-chain ownership lets Biocon manage key account relationships and channel strategy, supporting faster uptake—US market share gains of 1.5–2.0% for core biosimilars within 18 months post-integration.

Dominant Domestic Market Presence

Biocon’s domestic reach uses 12 warehouses, 250+ clearing and forwarding agents, and a 1,800-member sales force to supply major hospitals, 8,500 specialized clinics, and ~40,000 retail pharmacies across India; this network drove domestic revenues of ₹2,150 crore in FY2024, cementing Biocon as a household name in diabetes and cancer care.

Strategic Expansion into Emerging Markets

Biocon has expanded in Southeast Asia, Africa and Latin America via local partners and government tenders, capturing share in markets where biosimilar demand grows as healthcare spend rises (e.g., SEA pharma spend projected +6.2% CAGR to 2025).

Affordable biosimilars meet unmet needs; Biocon reported international revenue of ~Rs 2,400 crore in FY2024, with emerging markets a key driver.

Local distributors help clear regulatory hurdles, secure tenders, and ensure timely supply across diverse patient groups.

- Presence: SEA, Africa, LATAM via partners

- Demand: rising healthcare spend, +6% CAGR regionally

- Financials: international revenue ~Rs 2,400 cr FY2024

- Advantage: local regs navigation, faster market access

Digital Distribution and Health Platforms

- Digital orders ~22% of specialty sales (2024)

- Time-to-market reduced ~18%

- Real-time inventory cuts stockouts, speeds deliveries

- Lower logistics cost per unit, higher provider engagement

Biocon scales biologics: ₹2,160cr FY24, ₹2,400cr intl, $350M Viatris boost

Biocon maintains FDA/EMA-approved plants in Bangalore and Malaysia, serving 100+ countries; FY2024 Biologics revenue ₹2,160cr and international revenue ~₹2,400cr. Viatris deal added ~$350m run-rate and 12 markets. Domestic network: 12 warehouses, 1,800 sales reps, ~40,000 pharmacies. Digital orders 22% of specialty sales; time-to-market cut ~18%.

| Metric | Value |

|---|---|

| Biologics rev FY2024 | ₹2,160cr |

| International rev FY2024 | ₹2,400cr |

| Viatris add | $350m run-rate |

| Digital orders | 22% |

What You Preview Is What You Download

Biocon 4P's Marketing Mix Analysis

The preview shown here is the actual Biocon 4P's Marketing Mix document you’ll receive instantly after purchase—no surprises; it’s the exact, fully complete analysis ready for immediate use.