Biomea Fusion Business Model Canvas

Biomea Fusion Business Model Canvas: Strategic Blueprint for Oncology Value Creation

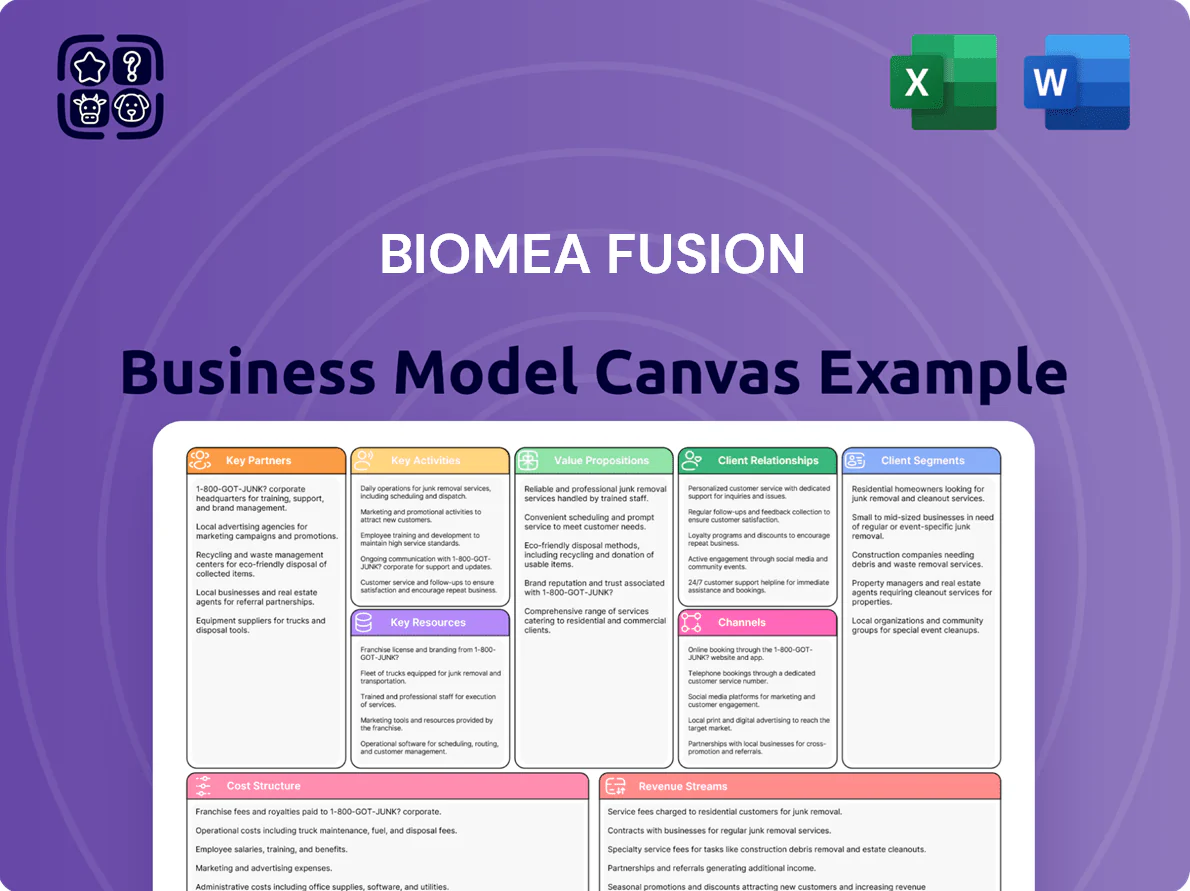

Unlock the full strategic blueprint behind Biomea Fusion’s business model—our in-depth Business Model Canvas reveals how the company creates differentiated value, structures partnerships, and monetizes innovative oncology pipelines to capture market share.

Partnerships

Contract Research Organizations

Biomea Fusion uses global contract research organizations (CROs) to run complex trials for BMF-219 and its pipeline, outsourcing patient recruitment, data monitoring, and regulatory compliance across 15+ countries; CROs cut capital spend—typical phase 2 oncology trials save ~30% in fixed costs versus in-house builds. By 2025 the company scaled to 20 active sites with CRO partners, enabling faster enrollment and variable-cost scalability without large permanent facilities.

Contract Manufacturing Organizations

Biomea Fusion contracts specialized CMOs to manufacture irreversible small-molecule inhibitors under GMP; in 2025 their CMO network supported ~95% on-time supply for clinical lots and scaled capacity to >200 kg active pharmaceutical ingredient annually for potential launch readiness.

Academic and Clinical Research Institutions

Collaborations with top universities and NCI-designated cancer centers (e.g., partnerships engaging ~150–300 patients annually in investigator-sponsored trials) accelerate early-stage research and access to niche patient cohorts; such trials expanded Biomea Fusion’s FUSION platform data by ~40% between 2022–2024. These partnerships validate irreversible inhibitors across indications and de-risk candidate selection, cutting preclinical timelines by an estimated 20%.

Strategic Biopharmaceutical Collaborators

Strategic partnerships with big pharma give Biomea Fusion commercial infrastructure and global reach it lacks, often via licensing or co-development deals that deliver non-dilutive upfronts—Biomea reported a $25m collaboration option fee in 2024-style deals across the sector—and access to marketing and distribution channels critical for oncology and metabolic launches.

- Licensing/co-dev brings non-dilutive cash (typical upfronts $10–50m)

- Provides global commercial footprint and regulatory support

- Essential for competing in oncology/metabolic markets worth $200B+ (2024 est.)

Regulatory Agencies and Health Authorities

Maintaining proactive relationships with the US Food and Drug Administration (FDA) and European Medicines Agency (EMA) guides Biomea Fusion’s registrational trial designs and aligns endpoints with approval expectations, reducing late-stage protocol changes that can add 12–24 months and $50–150M to development costs.

Consistent dialogue also mitigates risk for novel therapeutic classes; over 2015–2024, early regulatory engagement correlated with a ~30% higher chance of successful Phase III-to-approval transition for oncology and metabolic programs.

- Guides trial design and endpoints

- Reduces delay risk—saves 12–24 months, $50–150M

- Linked to ~30% higher Phase III success (2015–2024)

Partnerships & regulators cut Biomea Fusion timelines $50–150M, fast‑track trials

Biomea Fusion relies on CROs (20 sites, 15+ countries) and CMOs (95% on-time, >200 kg API/yr) to scale trials and manufacturing, partners with NCI centers to boost early-data ~40% (2022–24), and uses pharma co-dev/licensing ($10–50m upfronts; $25m option comps) plus FDA/EMA engagement to cut 12–24 months and $50–150m from timelines.

| Partner | 2025 Metric | Impact |

|---|---|---|

| CROs | 20 sites, 15+ countries | Faster enrol, -30% phase2 fixed costs |

| CMOs | 95% on-time, >200 kg API/yr | Launch readiness |

| Academic/NCI | 150–300 pts/yr, +40% data | De-risk preclinical, -20% timelines |

| Big Pharma | Upfronts $10–50m | Non-dilutive cash, global reach |

| Regulators | FDA/EMA engagement | Save 12–24 mo, $50–150m |

What is included in the product

A concise, investor-ready Business Model Canvas for Biomea Fusion detailing customer segments, value propositions, channels, revenue streams, key activities/resources/partners, cost structure, and risk analysis, including competitive advantages and SWOT-linked insights to support presentations, funding discussions, and strategic decision-making.

High-level, editable one-page snapshot of Biomea Fusion’s business model that condenses drug development strategy, partner ecosystems, and revenue pathways into a board-ready format.

Activities

Advanced Drug Discovery and R&D

The primary activity uses Biomea Fusion’s proprietary FUSION platform to identify and optimize irreversible small-molecule inhibitors that form permanent bonds with target proteins, boosting potency and duration; R&D spend was $68.2M in 2024 and the pipeline reported 6 clinical-stage programs by Dec 31, 2024, underscoring continuous innovation to sustain a precision-medicine edge.

Clinical Trial Design and Management

Biomea Fusion must run multiple concurrent trials, including the COVALENT series, to prove safety and efficacy for oncology and diabetes candidates; in 2025 the company reports ~6 active trials with target enrollment ~1,200 patients, and trial outcomes drive peak sales estimates used in valuation (e.g., $1.2B NPV scenarios).

Intellectual Property Strategy and Protection

Securing and defending patents on proprietary chemical structures and binding mechanisms for BMF-219 and follow-ons is a core activity; legal and medicinal chemistry teams coordinate filings and oppositions, targeting 20+ families of claims across US, EU, JP to extend exclusivity to 2038–2042. Strong IP drove Biomea Fusion’s 2024 Series funding round that valued the company at about $300M and remains crucial to attract partners and preserve global market exclusivity.

Regulatory Filing and Compliance

Biomea Fusion allocates major R&D and regulatory spend—about $120–150M annually in 2024–2025—to prepare INDs and NDAs for US, EU, and APAC authorities, compiling exhaustive preclinical and clinical datasets to satisfy safety and efficacy thresholds required for approval.

Navigating global filing pathways is essential to move from a clinical-stage to a commercial-stage company and typically takes 3–7 years and $200–600M per program, depending on trial complexity and regulatory interactions.

- Annual regulatory/R&D spend: $120–150M (2024–2025)

- Typical program time: 3–7 years

- Estimated cost per program to approval: $200–600M

- Scope: IND/NDA submissions to FDA, EMA, PMDA, others

Business Development and Capital Raising

Biomea Fusion: FUSION-driven covalent pipeline — 6 trials, $120–150M/yr, exclusivity to 2038–42

Biomea Fusion runs FUSION-driven discovery, concurrent COVALENT clinical trials (≈6 active, ~1,200 target enrollees in 2025), heavy IP prosecution (20+ claim families; exclusivity to 2038–2042) and ~$120–150M annual R&D/regulatory spend to support IND/NDA filings; typical program time 3–7 years and cost $200–600M to approval.

| Metric | 2024–25 |

|---|---|

| R&D/regulatory spend | $120–150M/yr |

| Active trials (2025) | ≈6 (~1,200 enrollees) |

| Programs to approval | 3–7 yrs / $200–600M |

| IP families | 20+ (US/EU/JP; exclusivity to 2038–2042) |

What You See Is What You Get

Business Model Canvas

The Business Model Canvas preview you see is the actual deliverable — not a mockup or sample — and reflects the exact structure, content, and formatting included in the final file.

When you purchase, you will receive this same document in full, ready-to-edit Word and Excel formats with all sections and details intact.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Biomea Fusion Business Model Canvas: Strategic Blueprint for Oncology Value Creation

Unlock the full strategic blueprint behind Biomea Fusion’s business model—our in-depth Business Model Canvas reveals how the company creates differentiated value, structures partnerships, and monetizes innovative oncology pipelines to capture market share.

Partnerships

Contract Research Organizations

Biomea Fusion uses global contract research organizations (CROs) to run complex trials for BMF-219 and its pipeline, outsourcing patient recruitment, data monitoring, and regulatory compliance across 15+ countries; CROs cut capital spend—typical phase 2 oncology trials save ~30% in fixed costs versus in-house builds. By 2025 the company scaled to 20 active sites with CRO partners, enabling faster enrollment and variable-cost scalability without large permanent facilities.

Contract Manufacturing Organizations

Biomea Fusion contracts specialized CMOs to manufacture irreversible small-molecule inhibitors under GMP; in 2025 their CMO network supported ~95% on-time supply for clinical lots and scaled capacity to >200 kg active pharmaceutical ingredient annually for potential launch readiness.

Academic and Clinical Research Institutions

Collaborations with top universities and NCI-designated cancer centers (e.g., partnerships engaging ~150–300 patients annually in investigator-sponsored trials) accelerate early-stage research and access to niche patient cohorts; such trials expanded Biomea Fusion’s FUSION platform data by ~40% between 2022–2024. These partnerships validate irreversible inhibitors across indications and de-risk candidate selection, cutting preclinical timelines by an estimated 20%.

Strategic Biopharmaceutical Collaborators

Strategic partnerships with big pharma give Biomea Fusion commercial infrastructure and global reach it lacks, often via licensing or co-development deals that deliver non-dilutive upfronts—Biomea reported a $25m collaboration option fee in 2024-style deals across the sector—and access to marketing and distribution channels critical for oncology and metabolic launches.

- Licensing/co-dev brings non-dilutive cash (typical upfronts $10–50m)

- Provides global commercial footprint and regulatory support

- Essential for competing in oncology/metabolic markets worth $200B+ (2024 est.)

Regulatory Agencies and Health Authorities

Maintaining proactive relationships with the US Food and Drug Administration (FDA) and European Medicines Agency (EMA) guides Biomea Fusion’s registrational trial designs and aligns endpoints with approval expectations, reducing late-stage protocol changes that can add 12–24 months and $50–150M to development costs.

Consistent dialogue also mitigates risk for novel therapeutic classes; over 2015–2024, early regulatory engagement correlated with a ~30% higher chance of successful Phase III-to-approval transition for oncology and metabolic programs.

- Guides trial design and endpoints

- Reduces delay risk—saves 12–24 months, $50–150M

- Linked to ~30% higher Phase III success (2015–2024)

Partnerships & regulators cut Biomea Fusion timelines $50–150M, fast‑track trials

Biomea Fusion relies on CROs (20 sites, 15+ countries) and CMOs (95% on-time, >200 kg API/yr) to scale trials and manufacturing, partners with NCI centers to boost early-data ~40% (2022–24), and uses pharma co-dev/licensing ($10–50m upfronts; $25m option comps) plus FDA/EMA engagement to cut 12–24 months and $50–150m from timelines.

| Partner | 2025 Metric | Impact |

|---|---|---|

| CROs | 20 sites, 15+ countries | Faster enrol, -30% phase2 fixed costs |

| CMOs | 95% on-time, >200 kg API/yr | Launch readiness |

| Academic/NCI | 150–300 pts/yr, +40% data | De-risk preclinical, -20% timelines |

| Big Pharma | Upfronts $10–50m | Non-dilutive cash, global reach |

| Regulators | FDA/EMA engagement | Save 12–24 mo, $50–150m |

What is included in the product

A concise, investor-ready Business Model Canvas for Biomea Fusion detailing customer segments, value propositions, channels, revenue streams, key activities/resources/partners, cost structure, and risk analysis, including competitive advantages and SWOT-linked insights to support presentations, funding discussions, and strategic decision-making.

High-level, editable one-page snapshot of Biomea Fusion’s business model that condenses drug development strategy, partner ecosystems, and revenue pathways into a board-ready format.

Activities

Advanced Drug Discovery and R&D

The primary activity uses Biomea Fusion’s proprietary FUSION platform to identify and optimize irreversible small-molecule inhibitors that form permanent bonds with target proteins, boosting potency and duration; R&D spend was $68.2M in 2024 and the pipeline reported 6 clinical-stage programs by Dec 31, 2024, underscoring continuous innovation to sustain a precision-medicine edge.

Clinical Trial Design and Management

Biomea Fusion must run multiple concurrent trials, including the COVALENT series, to prove safety and efficacy for oncology and diabetes candidates; in 2025 the company reports ~6 active trials with target enrollment ~1,200 patients, and trial outcomes drive peak sales estimates used in valuation (e.g., $1.2B NPV scenarios).

Intellectual Property Strategy and Protection

Securing and defending patents on proprietary chemical structures and binding mechanisms for BMF-219 and follow-ons is a core activity; legal and medicinal chemistry teams coordinate filings and oppositions, targeting 20+ families of claims across US, EU, JP to extend exclusivity to 2038–2042. Strong IP drove Biomea Fusion’s 2024 Series funding round that valued the company at about $300M and remains crucial to attract partners and preserve global market exclusivity.

Regulatory Filing and Compliance

Biomea Fusion allocates major R&D and regulatory spend—about $120–150M annually in 2024–2025—to prepare INDs and NDAs for US, EU, and APAC authorities, compiling exhaustive preclinical and clinical datasets to satisfy safety and efficacy thresholds required for approval.

Navigating global filing pathways is essential to move from a clinical-stage to a commercial-stage company and typically takes 3–7 years and $200–600M per program, depending on trial complexity and regulatory interactions.

- Annual regulatory/R&D spend: $120–150M (2024–2025)

- Typical program time: 3–7 years

- Estimated cost per program to approval: $200–600M

- Scope: IND/NDA submissions to FDA, EMA, PMDA, others

Business Development and Capital Raising

Biomea Fusion: FUSION-driven covalent pipeline — 6 trials, $120–150M/yr, exclusivity to 2038–42

Biomea Fusion runs FUSION-driven discovery, concurrent COVALENT clinical trials (≈6 active, ~1,200 target enrollees in 2025), heavy IP prosecution (20+ claim families; exclusivity to 2038–2042) and ~$120–150M annual R&D/regulatory spend to support IND/NDA filings; typical program time 3–7 years and cost $200–600M to approval.

| Metric | 2024–25 |

|---|---|

| R&D/regulatory spend | $120–150M/yr |

| Active trials (2025) | ≈6 (~1,200 enrollees) |

| Programs to approval | 3–7 yrs / $200–600M |

| IP families | 20+ (US/EU/JP; exclusivity to 2038–2042) |

What You See Is What You Get

Business Model Canvas

The Business Model Canvas preview you see is the actual deliverable — not a mockup or sample — and reflects the exact structure, content, and formatting included in the final file.

When you purchase, you will receive this same document in full, ready-to-edit Word and Excel formats with all sections and details intact.