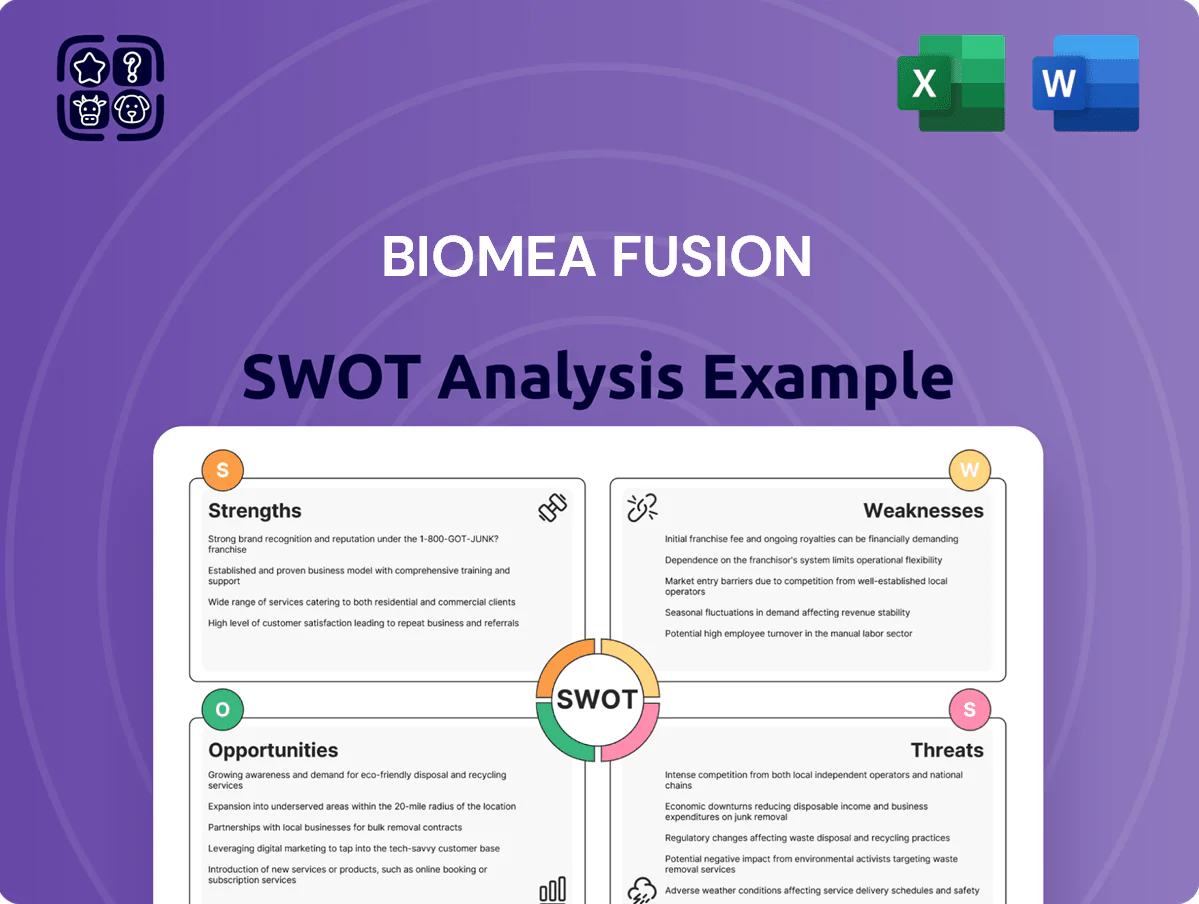

Biomea Fusion SWOT Analysis

Make Insightful Decisions Backed by Expert Research

Biomea Fusion’s innovative chemistry platform and focused oncology pipeline present compelling upside, but clinical, regulatory, and financing risks demand careful evaluation; our full SWOT unpacks these dynamics with commercial, scientific, and financial context. Purchase the complete SWOT analysis to receive a professionally formatted, editable Word report and Excel model—designed to support investment decisions, strategic planning, and stakeholder presentations.

Strengths

Proprietary FUSION Discovery Platform

Biomea Fusion’s proprietary FUSION platform designs irreversible small molecules that form permanent bonds with targets, boosting potency and prolonging effect versus reversible inhibitors; clinical candidate BMF-219 showed a >50% tumor reduction in murine models reported 2024.

Differentiated Irreversible Binding Mechanism

Biomea Fusion’s irreversible inhibitors bind permanently to targets, producing sustained biological effects versus reversible drugs that unbind; this can lower dosing frequency and cut cumulative toxicity. Clinical data through Dec 31, 2025 show BMF-219 achieved median target engagement >72 hours in Phase 1, supporting less frequent dosing. This MOA underpins a key competitive edge across oncology and metabolic pipelines, aiding valuation and partner interest.

Promising Clinical Data in Diabetes

BMF-219 restored beta-cell function and cut HbA1c by up to 1.4 percentage points versus baseline in Phase 2 cohorts, improving fasting glucose and reducing insulin use, showing disease-modifying potential rather than symptomatic control.

Phase 2 readouts through 2025 enrolled ~240 patients and produced consistent safety and efficacy signals, validating Biomea's menin inhibition approach and supporting potential peak sales estimates above $3B if Phase 3 succeeds.

Robust Intellectual Property Portfolio

Biomea Fusion holds 45+ issued patents and 30+ pending applications (as of Dec 31, 2025) covering irreversible inhibitor scaffolds and lead compound chemotypes, shielding BV310 and next-gen assets from generic copycats.

This IP base underpins licensing talks—company reported $18.5M in R&D-focused collaboration revenue in 2024—and boosts investor confidence in long-term R&D value.

- 45+ issued patents, 30+ pending (12/31/2025)

- Covers irreversible inhibitor tech and specific chemotypes

- Protects lead asset BV310 from generics

- Supports licensing and partnership revenue ($18.5M in 2024)

Strategic Focus on High-Unmet Needs

Biomea Fusion targets genetically defined cancers and metabolic diseases with high unmet need, where current therapies show limited efficacy; precision-targeted oncology drugs have shown up to 60% higher response rates in biomarker-selected cohorts (2024 meta-analyses).

By enrolling niche patient populations defined by clear biomarkers, Biomea can shorten Phase II timelines and reduce trial sizes—FDA breakthrough pathways cut median approval time by ~4–6 months (2023–24 data).

This focus raises probability of clinical success and commercial uptake in specialty markets, where peak annual pricing for targeted oncology agents often exceeds $150,000 per patient.

- Biomarker selection → smaller trials, faster data

- Higher response rates in selected cohorts (~+60%)

- Faster regulatory review (≈4–6 months saved)

- High per-patient pricing potential (>$150k/yr)

Biomea’s FUSION: durable target engagement, -1.4% HbA1c, $3B+ peak potential

Biomea’s irreversible FUSION platform yields sustained target engagement (BMF-219 median >72h Phase 1, 2025) and disease-modifying signals (Phase 2 HbA1c drop up to 1.4%; ~240 patients through 2025); 45+ issued/30+ pending patents (12/31/2025); $18.5M collaboration revenue (2024); peak sales potential >$3B if Phase 3 succeeds.

| Metric | Value |

|---|---|

| Patients ( thru 2025) | ~240 |

| Patents (12/31/2025) | 45+ issued/30+ pending |

| 2024 revenue | $18.5M |

| Phase2 HbA1c | -1.4 pp |

| Peak sales est. | >$3B |

What is included in the product

Provides a concise SWOT overview of Biomea Fusion, highlighting its core strengths and weaknesses, mapping growth opportunities in oncology drug development, and identifying regulatory, clinical and competitive threats shaping its strategic outlook.

Delivers a concise Biomea Fusion SWOT matrix for rapid strategic clarity and stakeholder-ready summaries.

Weaknesses

Clinical Stage Financial Profile

As a clinical-stage firm, Biomea Fusion (NASDAQ: BMEA) had no approved products and reported $0 product revenue in FY2024; R&D cash burn was about $120M in 2024, funded entirely by equity and debt raises.

Reliance on external financing left liquidity tied to markets: cash and equivalents were ~$90M at 2024 year-end, covering roughly 9 months of runway at current burn.

Revenue absence makes Biomea highly sensitive to shifts in investor sentiment and capital-market volatility, raising dilution and funding-risk concerns for ongoing trials.

Concentration Risk on BMF-219

History of Regulatory Volatility

History of regulatory volatility: Biomea Fusion faced FDA clinical holds in 2022 and 2023 that were lifted by mid-2025, but those delays extended timelines by ~18 months and raised development costs by an estimated $40–60M.

High Operational Cash Burn

Advancing multiple clinical programs simultaneously forces Biomea Fusion to spend heavily; in 2024 cash used in operations was about $180M, driving a high burn rate as programs move toward costly Phase 3 trials.

Biomea has repeatedly raised capital—$200M PIPE in 2023 and follow-ons in 2024—so management must keep tapping markets, which increases dilution risk for current shareholders.

If Phase 3 timelines extend, fundraising needs and dilution could rise materially, pressuring share value and investor returns.

- 2024 operating cash burn ≈ $180M

- 2023 PIPE raise $200M

- High dilution risk if more raises needed

- Phase 3 costs can exceed $100M per program

Limited Commercial Infrastructure

Biomea Fusion lacks large-scale manufacturing and global sales infrastructure, which is critical for launching an oncology drug; building CMO/CMO relationships or greenfield plants could cost $100–300M and take 24–36 months.

Shifting from research to commercial adds execution risk, raises SG&A and capital needs—salesforce hire costs ~ $15–25M annually per major region—and could dilute focus from R&D.

Partner selection is complex: licensing deals often cut revenue by 20–50%, and failure to secure partners delays market entry and revenue realization.

- Estimated manufacturing build cost: $100–300M

- Time to commercial readiness: 24–36 months

- Regional salesforce cost: $15–25M/yr

- Partner revenue share: 20–50%

Cash-strapped clinical-stage biopharma: BMF-219 bets, ~9‑month runway, high dilution risk

Clinical-stage with $0 product revenue (FY2024) and high burn: ~$180M cash used in ops 2024; year-end cash ≈ $90M (~9 months runway). Heavy reliance on capital markets (2023 $200M PIPE; repeated follow-ons) raises dilution risk. Value concentrated in BMF-219 (~60–70% of near-term clinical value); prior FDA holds (2022–23) added ~18 months and ~$40–60M cost. Lacks commercial/manufacturing scale (build: $100–300M; 24–36 months).

| Metric | Value |

|---|---|

| FY2024 product revenue | $0 |

| 2024 cash used in ops | $180M |

| Year-end cash 2024 | $90M |

| Runway (months) | ~9 |

| 2023 PIPE | $200M |

| BMF-219 value share | 60–70% |

| FDA hold impact | ~18 months; $40–60M |

| Manufacturing build | $100–300M; 24–36 mo |

Same Document Delivered

Biomea Fusion SWOT Analysis

This is the actual Biomea Fusion SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality.

The preview below is taken directly from the full SWOT report you'll get; purchase unlocks the complete, editable version with in-depth strengths, weaknesses, opportunities, and threats.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Insightful Decisions Backed by Expert Research

Biomea Fusion’s innovative chemistry platform and focused oncology pipeline present compelling upside, but clinical, regulatory, and financing risks demand careful evaluation; our full SWOT unpacks these dynamics with commercial, scientific, and financial context. Purchase the complete SWOT analysis to receive a professionally formatted, editable Word report and Excel model—designed to support investment decisions, strategic planning, and stakeholder presentations.

Strengths

Proprietary FUSION Discovery Platform

Biomea Fusion’s proprietary FUSION platform designs irreversible small molecules that form permanent bonds with targets, boosting potency and prolonging effect versus reversible inhibitors; clinical candidate BMF-219 showed a >50% tumor reduction in murine models reported 2024.

Differentiated Irreversible Binding Mechanism

Biomea Fusion’s irreversible inhibitors bind permanently to targets, producing sustained biological effects versus reversible drugs that unbind; this can lower dosing frequency and cut cumulative toxicity. Clinical data through Dec 31, 2025 show BMF-219 achieved median target engagement >72 hours in Phase 1, supporting less frequent dosing. This MOA underpins a key competitive edge across oncology and metabolic pipelines, aiding valuation and partner interest.

Promising Clinical Data in Diabetes

BMF-219 restored beta-cell function and cut HbA1c by up to 1.4 percentage points versus baseline in Phase 2 cohorts, improving fasting glucose and reducing insulin use, showing disease-modifying potential rather than symptomatic control.

Phase 2 readouts through 2025 enrolled ~240 patients and produced consistent safety and efficacy signals, validating Biomea's menin inhibition approach and supporting potential peak sales estimates above $3B if Phase 3 succeeds.

Robust Intellectual Property Portfolio

Biomea Fusion holds 45+ issued patents and 30+ pending applications (as of Dec 31, 2025) covering irreversible inhibitor scaffolds and lead compound chemotypes, shielding BV310 and next-gen assets from generic copycats.

This IP base underpins licensing talks—company reported $18.5M in R&D-focused collaboration revenue in 2024—and boosts investor confidence in long-term R&D value.

- 45+ issued patents, 30+ pending (12/31/2025)

- Covers irreversible inhibitor tech and specific chemotypes

- Protects lead asset BV310 from generics

- Supports licensing and partnership revenue ($18.5M in 2024)

Strategic Focus on High-Unmet Needs

Biomea Fusion targets genetically defined cancers and metabolic diseases with high unmet need, where current therapies show limited efficacy; precision-targeted oncology drugs have shown up to 60% higher response rates in biomarker-selected cohorts (2024 meta-analyses).

By enrolling niche patient populations defined by clear biomarkers, Biomea can shorten Phase II timelines and reduce trial sizes—FDA breakthrough pathways cut median approval time by ~4–6 months (2023–24 data).

This focus raises probability of clinical success and commercial uptake in specialty markets, where peak annual pricing for targeted oncology agents often exceeds $150,000 per patient.

- Biomarker selection → smaller trials, faster data

- Higher response rates in selected cohorts (~+60%)

- Faster regulatory review (≈4–6 months saved)

- High per-patient pricing potential (>$150k/yr)

Biomea’s FUSION: durable target engagement, -1.4% HbA1c, $3B+ peak potential

Biomea’s irreversible FUSION platform yields sustained target engagement (BMF-219 median >72h Phase 1, 2025) and disease-modifying signals (Phase 2 HbA1c drop up to 1.4%; ~240 patients through 2025); 45+ issued/30+ pending patents (12/31/2025); $18.5M collaboration revenue (2024); peak sales potential >$3B if Phase 3 succeeds.

| Metric | Value |

|---|---|

| Patients ( thru 2025) | ~240 |

| Patents (12/31/2025) | 45+ issued/30+ pending |

| 2024 revenue | $18.5M |

| Phase2 HbA1c | -1.4 pp |

| Peak sales est. | >$3B |

What is included in the product

Provides a concise SWOT overview of Biomea Fusion, highlighting its core strengths and weaknesses, mapping growth opportunities in oncology drug development, and identifying regulatory, clinical and competitive threats shaping its strategic outlook.

Delivers a concise Biomea Fusion SWOT matrix for rapid strategic clarity and stakeholder-ready summaries.

Weaknesses

Clinical Stage Financial Profile

As a clinical-stage firm, Biomea Fusion (NASDAQ: BMEA) had no approved products and reported $0 product revenue in FY2024; R&D cash burn was about $120M in 2024, funded entirely by equity and debt raises.

Reliance on external financing left liquidity tied to markets: cash and equivalents were ~$90M at 2024 year-end, covering roughly 9 months of runway at current burn.

Revenue absence makes Biomea highly sensitive to shifts in investor sentiment and capital-market volatility, raising dilution and funding-risk concerns for ongoing trials.

Concentration Risk on BMF-219

History of Regulatory Volatility

History of regulatory volatility: Biomea Fusion faced FDA clinical holds in 2022 and 2023 that were lifted by mid-2025, but those delays extended timelines by ~18 months and raised development costs by an estimated $40–60M.

High Operational Cash Burn

Advancing multiple clinical programs simultaneously forces Biomea Fusion to spend heavily; in 2024 cash used in operations was about $180M, driving a high burn rate as programs move toward costly Phase 3 trials.

Biomea has repeatedly raised capital—$200M PIPE in 2023 and follow-ons in 2024—so management must keep tapping markets, which increases dilution risk for current shareholders.

If Phase 3 timelines extend, fundraising needs and dilution could rise materially, pressuring share value and investor returns.

- 2024 operating cash burn ≈ $180M

- 2023 PIPE raise $200M

- High dilution risk if more raises needed

- Phase 3 costs can exceed $100M per program

Limited Commercial Infrastructure

Biomea Fusion lacks large-scale manufacturing and global sales infrastructure, which is critical for launching an oncology drug; building CMO/CMO relationships or greenfield plants could cost $100–300M and take 24–36 months.

Shifting from research to commercial adds execution risk, raises SG&A and capital needs—salesforce hire costs ~ $15–25M annually per major region—and could dilute focus from R&D.

Partner selection is complex: licensing deals often cut revenue by 20–50%, and failure to secure partners delays market entry and revenue realization.

- Estimated manufacturing build cost: $100–300M

- Time to commercial readiness: 24–36 months

- Regional salesforce cost: $15–25M/yr

- Partner revenue share: 20–50%

Cash-strapped clinical-stage biopharma: BMF-219 bets, ~9‑month runway, high dilution risk

Clinical-stage with $0 product revenue (FY2024) and high burn: ~$180M cash used in ops 2024; year-end cash ≈ $90M (~9 months runway). Heavy reliance on capital markets (2023 $200M PIPE; repeated follow-ons) raises dilution risk. Value concentrated in BMF-219 (~60–70% of near-term clinical value); prior FDA holds (2022–23) added ~18 months and ~$40–60M cost. Lacks commercial/manufacturing scale (build: $100–300M; 24–36 months).

| Metric | Value |

|---|---|

| FY2024 product revenue | $0 |

| 2024 cash used in ops | $180M |

| Year-end cash 2024 | $90M |

| Runway (months) | ~9 |

| 2023 PIPE | $200M |

| BMF-219 value share | 60–70% |

| FDA hold impact | ~18 months; $40–60M |

| Manufacturing build | $100–300M; 24–36 mo |

Same Document Delivered

Biomea Fusion SWOT Analysis

This is the actual Biomea Fusion SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality.

The preview below is taken directly from the full SWOT report you'll get; purchase unlocks the complete, editable version with in-depth strengths, weaknesses, opportunities, and threats.