BioNTech PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Navigate BioNTech’s external landscape with our concise PESTLE snapshot—highlighting regulatory risks, market drivers, and tech innovations shaping vaccine and oncology prospects; purchase the full PESTLE to unlock detailed, actionable insights for investment, strategy, or due diligence.

Political factors

Post-pandemic healthcare policy shifts

Governments shifted from emergency COVID spending to long-term preparedness, with OECD countries pledging over $50bn for national biotech resilience in 2024–25; BioNTech must adapt as states favor sovereign vaccine manufacturing and local suppliers, complicating multinational procurement and risking pricing pressure on its respiratory vaccine portfolio; this political nationalism affects BioNTech’s ability to secure multi-year contracts and fund rollout of future oncology mRNA programs.

Geopolitical tensions and supply chain security

Ongoing trade frictions between major economies have increased export controls on biological materials and lab equipment, raising compliance costs for BioNTech, which reported €19.2bn revenue in 2023 and depends on cross-border supply chains for mRNA production.

Reliance on global suppliers forces BioNTech to deploy political risk management—diversifying vendors and holding buffer inventories after 2021–22 shortages that impacted vial and lipid nanoparticle inputs.

Political stability in expansion regions like parts of Africa and Asia is critical for continuity; country-risk indicators and rising geopolitical incidents could delay clinical trials or local manufacturing partnerships.

Government funding and R&D subsidies

BioNTech benefits from EU and German initiatives, including Germany's 2024 Biotechnology Strategy and EU Horizon Europe funding; EU R&D grants to life sciences reached about €95bn for 2021–2027 while Germany doubled biotech funding to roughly €1.5bn in 2023–24, boosting mRNA programs.

Shifts in political leadership or fiscal priorities could reduce grants or tax incentives for high-risk mRNA research, risking delays in preclinical work and early trials that often need €10s–100sM in public support.

Maintaining strong ties with policymakers is essential: BioNTech reported over €1.2bn in government-backed contracts and subsidies related to COVID-19 vaccine work through 2024, underpinning public-private partnerships that accelerate early-stage clinical trials.

Global vaccine equity and intellectual property pressure

Political pressure from developing nations and WHO-led coalitions for IP waivers on vaccines remained intense through 2024–25; over 100 low- and middle-income countries backed TRIPS flexibilities, challenging BioNTech’s IP-linked revenue—COVID-19 vaccine sales generated about €17.3bn for Pfizer/BioNTech in 2021–23, spotlighting stakes in waiver debates.

BioNTech must balance commercial interests with calls for technology transfer; failure risks reputational and market-access costs while transfers could dilute margins but open new markets and partnerships across Africa and Asia.

BioNTainer—modular mRNA manufacturing units—serves as a political and strategic response, targeting decentralized production to meet local demand; pilot deployments aim to reduce lead times and support regional autonomy.

- Over 100 LMICs backing IP flexibilities

- Pfizer/BioNTech COVID vaccine revenue ~€17.3bn (2021–23)

- BioNTainer enables localized mRNA production and tech-transfer

Drug pricing regulation and healthcare reform

Political moves in the US and EU to cap drug prices and negotiate directly with pharma introduce revenue uncertainty for BioNTech, with proposals targeting single-digit percentage cuts and price ceilings for specialty drugs.

The US Inflation Reduction Act enables Medicare negotiation for some drugs from 2026, pressuring pricing for new oncology entrants and potentially reducing peak sales estimates by up to 20–30% in modeled scenarios.

BioNTech must shift commercialization toward value-based contracts and outcomes-linked pricing to comply with stricter government mandates and preserve market access.

- Medicare negotiation from 2026 under IRA

- Modeled peak-sales risk: 20–30% downside

- Trend: EU price caps and HTA value frameworks

- Required: outcomes-based contracts, real-world evidence

BioNTech faces export controls, IP pressure and IRA risk—EU support cushions R&D

Political nationalism, export controls and IP waiver pressure through 2024–25 raise procurement, compliance and pricing risks for BioNTech; EU/Germany R&D support (EU Horizon €95bn 2021–27; Germany biotech ≈€1.5bn 2023–24) and €1.2bn+ govt contracts cushion R&D while IRA Medicare negotiation from 2026 threatens 20–30% peak-sales downside, pushing BioNTech toward outcomes-based pricing.

| Metric | Value |

|---|---|

| EU Horizon funding (2021–27) | ≈€95bn |

| Germany biotech funding (2023–24) | ≈€1.5bn |

| Govt contracts/subsidies (through 2024) | €1.2bn+ |

| Pfizer/BioNTech vaccine revenue (2021–23) | ≈€17.3bn |

| Modeled peak-sales downside (IRA) | 20–30% |

What is included in the product

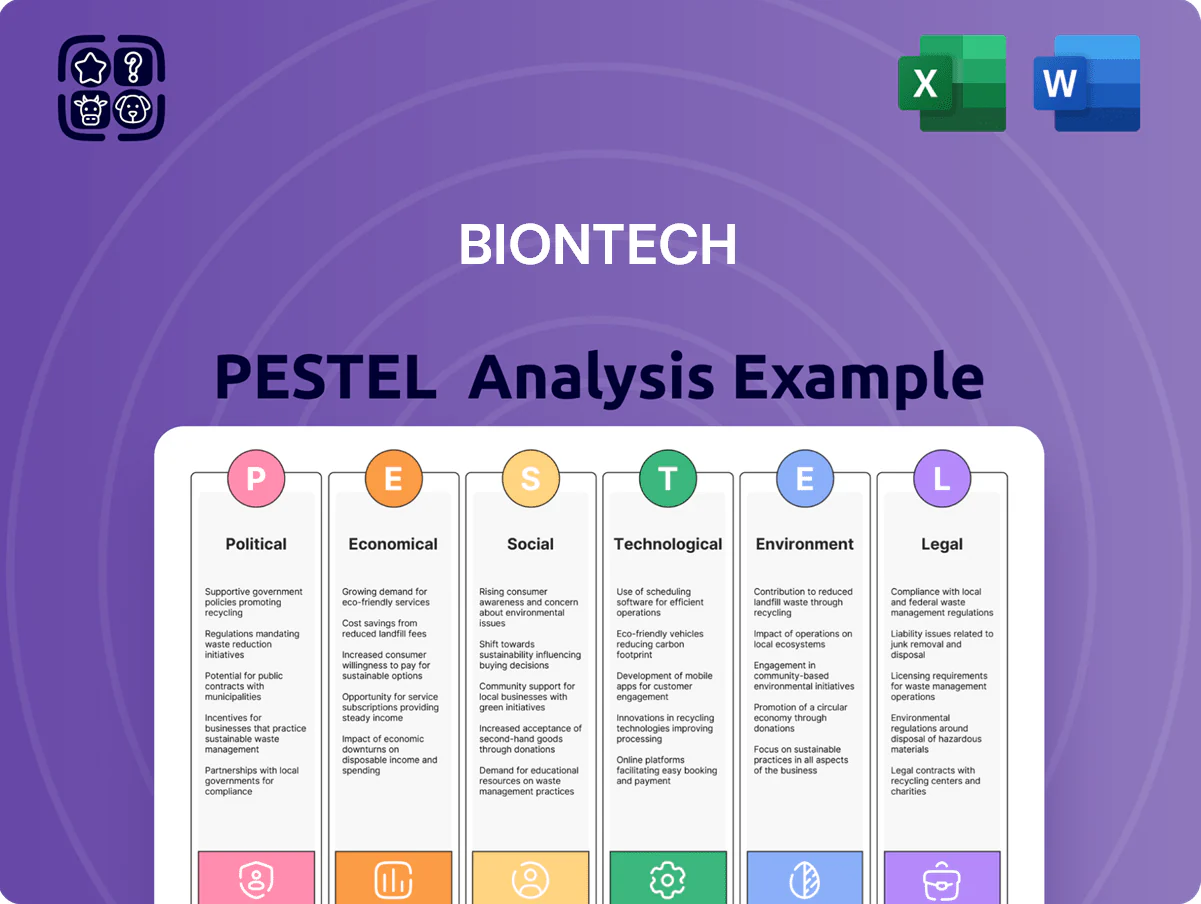

Explores how external macro-environmental factors uniquely affect BioNTech across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven insights and forward-looking implications to identify risks and opportunities for executives, investors, and strategists.

A concise, PESTLE-segmented snapshot of BioNTech that highlights key political, economic, social, technological, legal, and environmental factors for quick reference in meetings or presentations.

Economic factors

R&D intensive capital allocation

As of late 2025 BioNTech has shifted from roughly €18bn COVID-era cash inflows toward heavy reinvestment in oncology, with R&D spend rising to about €2.2bn in 2024 and projected near €2.5–3.0bn in 2025–26 to fund late-stage trials.

High burn rates from phase III programs demand strict financial oversight; the firm reported €6.1bn cash and equivalents at end‑2024 but may need capital market access or partnerships to sustain pipelines.

Economic success hinges on converting trial milestones into approvals and revenues: each pivotal readout materially affects valuation and funding terms for upcoming launches.

Currency exchange rate volatility

Reporting in euros while earning substantial revenue in U.S. dollars exposes BioNTech to FX risk; a 10% EUR/USD move would have shifted 2024 revenue impact materially given 2024 product and collaboration receipts—U.S. dollar-denominated sales represented an estimated ~40–50% of total revenues.

Inflationary pressure on operational costs

Global inflation pushed EU industrial input costs up 18.4% year-on-year in 2023, raising specialized labor, raw material and energy expenses for high-tech manufacturers like BioNTech.

BioNTech reported R&D and production SG&A increases contributing to margin pressure in 2023–2024, requiring efficiency gains to offset rising overheads.

Maintaining competitive pricing for next-gen mRNA therapeutics while input costs rose an estimated mid-single digits in 2024 remains a key operational challenge.

Market demand for respiratory vaccines

The COVID-19 vaccine market shifted from government bulk buys to a commercial seasonal model, with global COVID vaccine doses purchased dropping from ~13.9 billion in 2021 to ~600–800 million annual doses projected in 2024–25, stabilizing demand at lower levels.

BioNTech’s forecasts now hinge on uptake of combination COVID-Flu vaccines by private payers; analysts estimate 20–35% penetration in key EU/US markets by 2026 would materially affect revenue trajectories.

As a result BioNTech must adopt traditional pharma marketing—payer contracting, physician promotion, and pricing strategies—to secure steady revenues and mitigate seasonality.

- Seasonal market: ~600–800M annual COVID doses (2024–25)

- Key metric: 20–35% combo vaccine uptake target by 2026

- Revenue focus: private payer coverage, formulary placement, seasonal demand management

Interest rate environment and investment capacity

The 2025 euro-area deposit rate sat at 3.25% (ECB), keeping debt costs elevated and compressing biotech valuations; discounted cash flow multiples for growth firms fell ~18% vs 2021 peaks. BioNTech held ~8.5 billion euros cash and marketable securities at YE 2024, insulating it, but smaller partners face tighter financing—global VC biotech funding dropped ~22% in 2024. A stable/declining rate path into 2026 would support BioNTech’s growth valuation.

- ECB deposit rate 3.25% (2025)

- BioNTech cash ~8.5bn EUR (YE 2024)

- VC biotech funding -22% (2024)

- DCF multiples down ~18% vs 2021

BioNTech doubles down on oncology with €2.5–3bn R&D, cash €8.5bn—partners needed

BioNTech shifted to heavy oncology reinvestment with R&D ~€2.2bn in 2024 and projected €2.5–3.0bn in 2025–26; cash ~€8.5bn YE‑2024, but burn from phase IIIs requires partner capital access. FX risk: USD ~45% of revenues; a 10% EUR/USD swing materially affects reported sales. COVID market normalized to ~600–800M annual doses (2024–25); combo vaccine uptake 20–35% by 2026 critical to revenues. ECB deposit rate 3.25% (2025) compresses DCF multiples ~‑18% vs 2021.

| Metric | Value |

|---|---|

| R&D spend 2024 | €2.2bn |

| Projected R&D 2025–26 | €2.5–3.0bn |

| Cash YE‑2024 | €8.5bn |

| USD revenue share (est.) | ~45% |

| COVID annual doses | 600–800M |

| Combo uptake target by 2026 | 20–35% |

| ECB deposit rate (2025) | 3.25% |

| VC biotech funding change (2024) | ‑22% |

Full Version Awaits

BioNTech PESTLE Analysis

The preview shown here is the exact BioNTech PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use with no placeholders or surprises.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Plan Smarter. Present Sharper. Compete Stronger.

Navigate BioNTech’s external landscape with our concise PESTLE snapshot—highlighting regulatory risks, market drivers, and tech innovations shaping vaccine and oncology prospects; purchase the full PESTLE to unlock detailed, actionable insights for investment, strategy, or due diligence.

Political factors

Post-pandemic healthcare policy shifts

Governments shifted from emergency COVID spending to long-term preparedness, with OECD countries pledging over $50bn for national biotech resilience in 2024–25; BioNTech must adapt as states favor sovereign vaccine manufacturing and local suppliers, complicating multinational procurement and risking pricing pressure on its respiratory vaccine portfolio; this political nationalism affects BioNTech’s ability to secure multi-year contracts and fund rollout of future oncology mRNA programs.

Geopolitical tensions and supply chain security

Ongoing trade frictions between major economies have increased export controls on biological materials and lab equipment, raising compliance costs for BioNTech, which reported €19.2bn revenue in 2023 and depends on cross-border supply chains for mRNA production.

Reliance on global suppliers forces BioNTech to deploy political risk management—diversifying vendors and holding buffer inventories after 2021–22 shortages that impacted vial and lipid nanoparticle inputs.

Political stability in expansion regions like parts of Africa and Asia is critical for continuity; country-risk indicators and rising geopolitical incidents could delay clinical trials or local manufacturing partnerships.

Government funding and R&D subsidies

BioNTech benefits from EU and German initiatives, including Germany's 2024 Biotechnology Strategy and EU Horizon Europe funding; EU R&D grants to life sciences reached about €95bn for 2021–2027 while Germany doubled biotech funding to roughly €1.5bn in 2023–24, boosting mRNA programs.

Shifts in political leadership or fiscal priorities could reduce grants or tax incentives for high-risk mRNA research, risking delays in preclinical work and early trials that often need €10s–100sM in public support.

Maintaining strong ties with policymakers is essential: BioNTech reported over €1.2bn in government-backed contracts and subsidies related to COVID-19 vaccine work through 2024, underpinning public-private partnerships that accelerate early-stage clinical trials.

Global vaccine equity and intellectual property pressure

Political pressure from developing nations and WHO-led coalitions for IP waivers on vaccines remained intense through 2024–25; over 100 low- and middle-income countries backed TRIPS flexibilities, challenging BioNTech’s IP-linked revenue—COVID-19 vaccine sales generated about €17.3bn for Pfizer/BioNTech in 2021–23, spotlighting stakes in waiver debates.

BioNTech must balance commercial interests with calls for technology transfer; failure risks reputational and market-access costs while transfers could dilute margins but open new markets and partnerships across Africa and Asia.

BioNTainer—modular mRNA manufacturing units—serves as a political and strategic response, targeting decentralized production to meet local demand; pilot deployments aim to reduce lead times and support regional autonomy.

- Over 100 LMICs backing IP flexibilities

- Pfizer/BioNTech COVID vaccine revenue ~€17.3bn (2021–23)

- BioNTainer enables localized mRNA production and tech-transfer

Drug pricing regulation and healthcare reform

Political moves in the US and EU to cap drug prices and negotiate directly with pharma introduce revenue uncertainty for BioNTech, with proposals targeting single-digit percentage cuts and price ceilings for specialty drugs.

The US Inflation Reduction Act enables Medicare negotiation for some drugs from 2026, pressuring pricing for new oncology entrants and potentially reducing peak sales estimates by up to 20–30% in modeled scenarios.

BioNTech must shift commercialization toward value-based contracts and outcomes-linked pricing to comply with stricter government mandates and preserve market access.

- Medicare negotiation from 2026 under IRA

- Modeled peak-sales risk: 20–30% downside

- Trend: EU price caps and HTA value frameworks

- Required: outcomes-based contracts, real-world evidence

BioNTech faces export controls, IP pressure and IRA risk—EU support cushions R&D

Political nationalism, export controls and IP waiver pressure through 2024–25 raise procurement, compliance and pricing risks for BioNTech; EU/Germany R&D support (EU Horizon €95bn 2021–27; Germany biotech ≈€1.5bn 2023–24) and €1.2bn+ govt contracts cushion R&D while IRA Medicare negotiation from 2026 threatens 20–30% peak-sales downside, pushing BioNTech toward outcomes-based pricing.

| Metric | Value |

|---|---|

| EU Horizon funding (2021–27) | ≈€95bn |

| Germany biotech funding (2023–24) | ≈€1.5bn |

| Govt contracts/subsidies (through 2024) | €1.2bn+ |

| Pfizer/BioNTech vaccine revenue (2021–23) | ≈€17.3bn |

| Modeled peak-sales downside (IRA) | 20–30% |

What is included in the product

Explores how external macro-environmental factors uniquely affect BioNTech across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven insights and forward-looking implications to identify risks and opportunities for executives, investors, and strategists.

A concise, PESTLE-segmented snapshot of BioNTech that highlights key political, economic, social, technological, legal, and environmental factors for quick reference in meetings or presentations.

Economic factors

R&D intensive capital allocation

As of late 2025 BioNTech has shifted from roughly €18bn COVID-era cash inflows toward heavy reinvestment in oncology, with R&D spend rising to about €2.2bn in 2024 and projected near €2.5–3.0bn in 2025–26 to fund late-stage trials.

High burn rates from phase III programs demand strict financial oversight; the firm reported €6.1bn cash and equivalents at end‑2024 but may need capital market access or partnerships to sustain pipelines.

Economic success hinges on converting trial milestones into approvals and revenues: each pivotal readout materially affects valuation and funding terms for upcoming launches.

Currency exchange rate volatility

Reporting in euros while earning substantial revenue in U.S. dollars exposes BioNTech to FX risk; a 10% EUR/USD move would have shifted 2024 revenue impact materially given 2024 product and collaboration receipts—U.S. dollar-denominated sales represented an estimated ~40–50% of total revenues.

Inflationary pressure on operational costs

Global inflation pushed EU industrial input costs up 18.4% year-on-year in 2023, raising specialized labor, raw material and energy expenses for high-tech manufacturers like BioNTech.

BioNTech reported R&D and production SG&A increases contributing to margin pressure in 2023–2024, requiring efficiency gains to offset rising overheads.

Maintaining competitive pricing for next-gen mRNA therapeutics while input costs rose an estimated mid-single digits in 2024 remains a key operational challenge.

Market demand for respiratory vaccines

The COVID-19 vaccine market shifted from government bulk buys to a commercial seasonal model, with global COVID vaccine doses purchased dropping from ~13.9 billion in 2021 to ~600–800 million annual doses projected in 2024–25, stabilizing demand at lower levels.

BioNTech’s forecasts now hinge on uptake of combination COVID-Flu vaccines by private payers; analysts estimate 20–35% penetration in key EU/US markets by 2026 would materially affect revenue trajectories.

As a result BioNTech must adopt traditional pharma marketing—payer contracting, physician promotion, and pricing strategies—to secure steady revenues and mitigate seasonality.

- Seasonal market: ~600–800M annual COVID doses (2024–25)

- Key metric: 20–35% combo vaccine uptake target by 2026

- Revenue focus: private payer coverage, formulary placement, seasonal demand management

Interest rate environment and investment capacity

The 2025 euro-area deposit rate sat at 3.25% (ECB), keeping debt costs elevated and compressing biotech valuations; discounted cash flow multiples for growth firms fell ~18% vs 2021 peaks. BioNTech held ~8.5 billion euros cash and marketable securities at YE 2024, insulating it, but smaller partners face tighter financing—global VC biotech funding dropped ~22% in 2024. A stable/declining rate path into 2026 would support BioNTech’s growth valuation.

- ECB deposit rate 3.25% (2025)

- BioNTech cash ~8.5bn EUR (YE 2024)

- VC biotech funding -22% (2024)

- DCF multiples down ~18% vs 2021

BioNTech doubles down on oncology with €2.5–3bn R&D, cash €8.5bn—partners needed

BioNTech shifted to heavy oncology reinvestment with R&D ~€2.2bn in 2024 and projected €2.5–3.0bn in 2025–26; cash ~€8.5bn YE‑2024, but burn from phase IIIs requires partner capital access. FX risk: USD ~45% of revenues; a 10% EUR/USD swing materially affects reported sales. COVID market normalized to ~600–800M annual doses (2024–25); combo vaccine uptake 20–35% by 2026 critical to revenues. ECB deposit rate 3.25% (2025) compresses DCF multiples ~‑18% vs 2021.

| Metric | Value |

|---|---|

| R&D spend 2024 | €2.2bn |

| Projected R&D 2025–26 | €2.5–3.0bn |

| Cash YE‑2024 | €8.5bn |

| USD revenue share (est.) | ~45% |

| COVID annual doses | 600–800M |

| Combo uptake target by 2026 | 20–35% |

| ECB deposit rate (2025) | 3.25% |

| VC biotech funding change (2024) | ‑22% |

Full Version Awaits

BioNTech PESTLE Analysis

The preview shown here is the exact BioNTech PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use with no placeholders or surprises.