Beijing Energy International Porter's Five Forces Analysis

From Overview to Strategy Blueprint

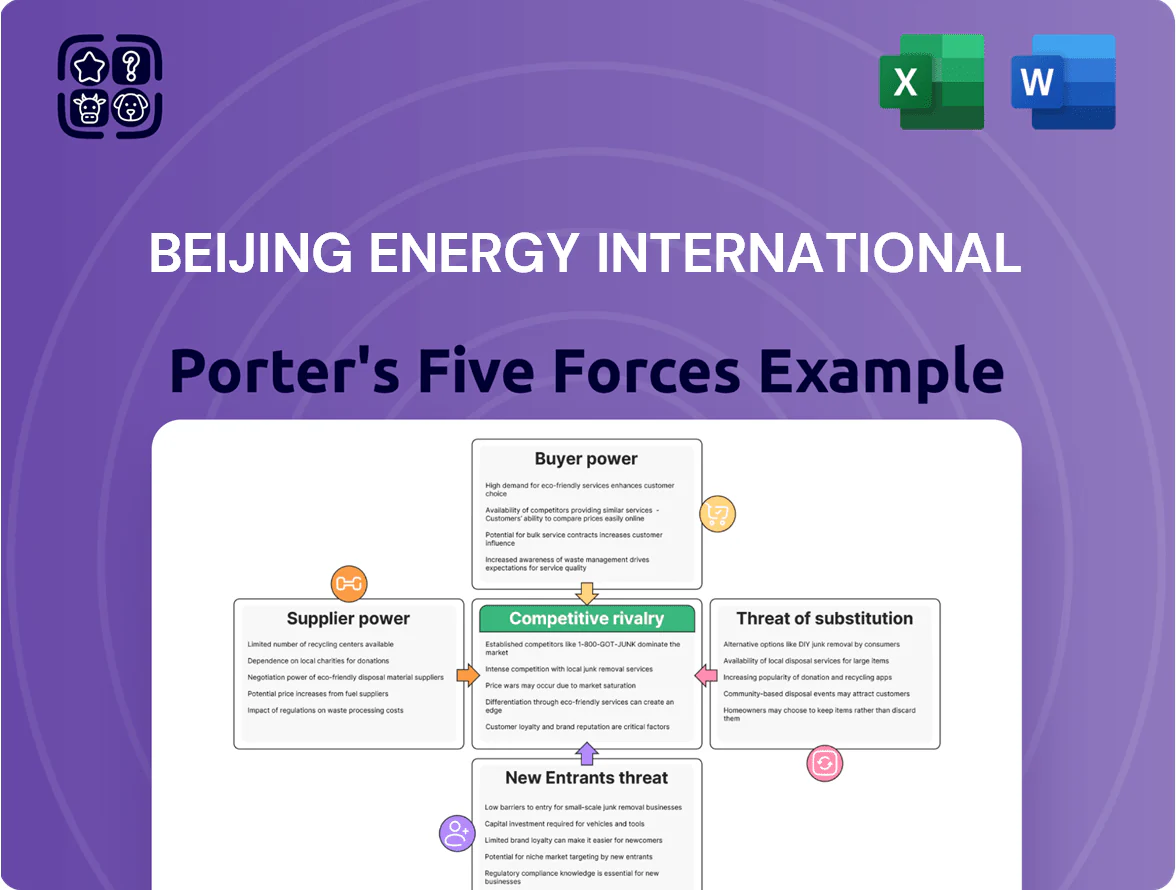

Beijing Energy International faces moderate supplier power, shifting buyer demands, and regulatory pressures that shape its competitive landscape—this snapshot highlights key tensions and opportunities for growth.

Suppliers Bargaining Power

Concentration of Tier One Equipment Manufacturers

Procurement of solar modules and wind turbines for Beijing Energy International depends on a few high-capacity Chinese manufacturers—such as LONGi, Goldwind, and Mingyang—who held roughly 40–55% market share in 2024 for panels and turbines, giving suppliers concentrated market power.

Domestic proximity cuts logistics costs by ~10–15% versus imports, but suppliers keep leverage via proprietary tech and multi-quarter production schedules that can delay delivery for large 500+ MW projects.

To secure components for its 2025–2027 pipeline, Beijing Energy International commonly signs multi-year strategic supply agreements and capacity reservations, often with price escalation clauses tied to polysilicon and rare-earth prices.

Volatility in Raw Material Pricing

Suppliers of polysilicon, steel and rare earths drive project costs for Beijing Energy International; polysilicon rose ~42% in 2024 and steel import prices spiked 18% Y/Y to Q3 2025, heightening supplier leverage.

Commodity shocks are passed to developers, risking margin erosion; a 10% raw material surge can cut project IRR by ~2–3 percentage points based on 2024 LCOE models.

Beijing Energy must use hedges (forward contracts, options) and diversify vendors—targeting 3+ suppliers per key input—to limit single-supplier price pass-through.

Specialized Technical Labor and EPC Services

The construction and maintenance of Beijing Energy International’s wind and integrated hydro projects rely on specialized EPC (engineering, procurement, construction) firms; globally, the top 10 EPC contractors captured about 60% of utility-scale renewables work in 2024, letting them charge premiums.

Limited supplier pool raises contract leverage: industry reports show EPC margins averaged 8–12% in 2024, and bespoke specialist labor rates can be 20–35% above general construction rates, squeezing BEI’s cost control.

Scarcity of Prime Land and Resource Rights

Suppliers of land rights—mainly local governments and state agencies—wield decisive power in project approval, timing, and lease pricing, directly affecting Beijing Energy International’s pipeline.

Prime solar and wind sites are scarce: China added ~55 GW utility-scale solar and 30 GW wind in 2024, raising competition for high-irradiance and high-wind corridors and driving up land lease bids.

Regulatory complexity means the land supplier can make or break viability via permits, grid connection priority, and land-use covenants, forcing BEI to budget for delays and premium rents.

- Major suppliers: local govts/state agencies

- 2024 additions: ~55 GW solar, 30 GW wind (China)

- Scarcity raises lease bids, delay risk

- Permits/grid access controlled by suppliers

Technological Lock-in for Energy Storage Systems

As Beijing Energy International moves into energy storage, dependence on battery IP owners creates technological lock-in; global lithium-ion pack suppliers held 65% of module patents in 2024, raising supplier leverage.

Integrated software-hardware switching costs run into millions per site and multi-month migrations, letting suppliers sustain price premia (battery pack ASPs rose 8% in 2024) and control upgrade cadence.

- High IP concentration: 65% module patents (2024)

- ASP rise: battery packs +8% (2024)

- Switch cost: multi-month, $0.5–3m per MW site

- Supplier controls upgrades, maintenance timing

Supplier power rising: input costs surge, IP concentrated—BEI hedges via vendors & contracts

Suppliers hold moderate-to-high power: concentrated module/turbine makers (40–55% share), EPCs with 8–12% margins, polysilicon +42% in 2024, steel +18% Y/Y to Q3 2025, battery-pack ASP +8% (2024), IP concentration 65% patents—BEI mitigates via 3+ vendors, multi-year contracts, and hedges.

| Metric | 2024–25 |

|---|---|

| Module/turbine share | 40–55% |

| Polysilicon | +42% |

| Steel | +18% Y/Y |

| Battery ASP | +8% |

| IP concentration | 65% |

What is included in the product

Tailored Porter's Five Forces for Beijing Energy International, revealing competitive intensity, supplier/buyer power, entry barriers, substitute threats, and strategic levers to protect margins and market share.

Compact Porter's Five Forces snapshot tailored to Beijing Energy—instantly reveals competitive pressures and regulatory risks to streamline boardroom decisions.

Customers Bargaining Power

Monopsony Power of State Grid Operators

The primary customers for Beijing Energy International are State Grid Corporation of China and China Southern Power Grid, near-monopolies controlling ~99% of national transmission; State Grid served 1.2 billion consumers in 2024. They decide project priority for grid connection and dispatch, so Beijing Energy has little bargaining leverage on tariffs, curtailment, or connection timelines. This monopsony power compresses margins and forces project terms largely set by the grids.

Policy Driven Power Purchase Pricing

Electricity prices for renewables in China are set mainly by feed-in tariffs and auctions; in 2024 the national benchmark wind onshore tariff hit ~0.28 CNY/kWh after subsidy cuts, not by buyer negotiation.

As solar and wind approach grid parity—LCOE for utility solar fell to ~0.32 CNY/kWh in 2023—state buyers press Beijing Energy International to cut prices toward coal rates near 0.25 CNY/kWh.

Therefore customer power is enacted via policy: national pricing reforms and auction rules determine revenue and squeeze margins rather than individual buyer bargaining.

Expansion of Corporate Power Purchase Agreements

Demand for Integrated Energy Services

Customers now demand integrated services—storage, energy-efficiency management, and multi-energy synergy—raising bargaining power as 62% of Chinese industrial buyers (2024 CNREC survey) prioritize bundled solutions over standalone generation.

Buyers push for bespoke packages, so Beijing Energy must build modular offerings and capex for storage and controls; otherwise churn and margin compression follow.

Meeting specs raises service costs: adding 100 MWh battery capacity costs ~USD 40–50k/MWh (2024 market prices), so pricing and contract terms must shift.

- 62% of industrial buyers prefer bundled solutions (CNREC 2024)

- 100 MWh battery ≈ USD 4–5M (2024 prices)

- Custom packages increase client retention but raise capex and O&M

Influence of Market-Based Trading Mechanisms

China’s shift to market-based electricity trading lets buyers bid in spot markets, raising customer price sensitivity and forcing Beijing Energy International to compete on price and reliability.

Large industrial buyers already account for ~45% of national power demand (2024), and as liberalization expands, their bargaining power will rise, pressuring margins and pushing contracts toward flexible, lower-cost supply.

- Spot bidding raises price competition

- Buyers ~45% of demand (2024)

- Pressure on margins and reliability premiums

- Large consumers gain negotiating leverage

Buyers Dictate Terms: Bundles, PPAs at $34/MWh, Batteries Raise Capex

Customers hold strong bargaining power: State Grid/China Southern (near-monopolies) set tariffs and curtailment, compressing margins; corporate PPAs grew, average strike ~$34/MWh (2024), and large buyers are ~45% of demand. Buyers demand bundled services (62% prefer, CNREC 2024), raising capex (100 MWh battery ≈ USD4–5M). Market reforms and spot trading increase price sensitivity and leverage.

| Metric | 2024 value |

|---|---|

| State Grid coverage | ~1.2B consumers |

| Avg corporate PPA | $34/MWh |

| Large buyers share | ~45% demand |

| Bundled preference | 62% |

| 100 MWh battery cost | USD4–5M |

Preview the Actual Deliverable

Beijing Energy International Porter's Five Forces Analysis

This preview shows the exact Beijing Energy International Porter’s Five Forces analysis you will receive immediately after purchase—fully formatted, professionally written, and ready for download with no placeholders or samples.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

Beijing Energy International faces moderate supplier power, shifting buyer demands, and regulatory pressures that shape its competitive landscape—this snapshot highlights key tensions and opportunities for growth.

Suppliers Bargaining Power

Concentration of Tier One Equipment Manufacturers

Procurement of solar modules and wind turbines for Beijing Energy International depends on a few high-capacity Chinese manufacturers—such as LONGi, Goldwind, and Mingyang—who held roughly 40–55% market share in 2024 for panels and turbines, giving suppliers concentrated market power.

Domestic proximity cuts logistics costs by ~10–15% versus imports, but suppliers keep leverage via proprietary tech and multi-quarter production schedules that can delay delivery for large 500+ MW projects.

To secure components for its 2025–2027 pipeline, Beijing Energy International commonly signs multi-year strategic supply agreements and capacity reservations, often with price escalation clauses tied to polysilicon and rare-earth prices.

Volatility in Raw Material Pricing

Suppliers of polysilicon, steel and rare earths drive project costs for Beijing Energy International; polysilicon rose ~42% in 2024 and steel import prices spiked 18% Y/Y to Q3 2025, heightening supplier leverage.

Commodity shocks are passed to developers, risking margin erosion; a 10% raw material surge can cut project IRR by ~2–3 percentage points based on 2024 LCOE models.

Beijing Energy must use hedges (forward contracts, options) and diversify vendors—targeting 3+ suppliers per key input—to limit single-supplier price pass-through.

Specialized Technical Labor and EPC Services

The construction and maintenance of Beijing Energy International’s wind and integrated hydro projects rely on specialized EPC (engineering, procurement, construction) firms; globally, the top 10 EPC contractors captured about 60% of utility-scale renewables work in 2024, letting them charge premiums.

Limited supplier pool raises contract leverage: industry reports show EPC margins averaged 8–12% in 2024, and bespoke specialist labor rates can be 20–35% above general construction rates, squeezing BEI’s cost control.

Scarcity of Prime Land and Resource Rights

Suppliers of land rights—mainly local governments and state agencies—wield decisive power in project approval, timing, and lease pricing, directly affecting Beijing Energy International’s pipeline.

Prime solar and wind sites are scarce: China added ~55 GW utility-scale solar and 30 GW wind in 2024, raising competition for high-irradiance and high-wind corridors and driving up land lease bids.

Regulatory complexity means the land supplier can make or break viability via permits, grid connection priority, and land-use covenants, forcing BEI to budget for delays and premium rents.

- Major suppliers: local govts/state agencies

- 2024 additions: ~55 GW solar, 30 GW wind (China)

- Scarcity raises lease bids, delay risk

- Permits/grid access controlled by suppliers

Technological Lock-in for Energy Storage Systems

As Beijing Energy International moves into energy storage, dependence on battery IP owners creates technological lock-in; global lithium-ion pack suppliers held 65% of module patents in 2024, raising supplier leverage.

Integrated software-hardware switching costs run into millions per site and multi-month migrations, letting suppliers sustain price premia (battery pack ASPs rose 8% in 2024) and control upgrade cadence.

- High IP concentration: 65% module patents (2024)

- ASP rise: battery packs +8% (2024)

- Switch cost: multi-month, $0.5–3m per MW site

- Supplier controls upgrades, maintenance timing

Supplier power rising: input costs surge, IP concentrated—BEI hedges via vendors & contracts

Suppliers hold moderate-to-high power: concentrated module/turbine makers (40–55% share), EPCs with 8–12% margins, polysilicon +42% in 2024, steel +18% Y/Y to Q3 2025, battery-pack ASP +8% (2024), IP concentration 65% patents—BEI mitigates via 3+ vendors, multi-year contracts, and hedges.

| Metric | 2024–25 |

|---|---|

| Module/turbine share | 40–55% |

| Polysilicon | +42% |

| Steel | +18% Y/Y |

| Battery ASP | +8% |

| IP concentration | 65% |

What is included in the product

Tailored Porter's Five Forces for Beijing Energy International, revealing competitive intensity, supplier/buyer power, entry barriers, substitute threats, and strategic levers to protect margins and market share.

Compact Porter's Five Forces snapshot tailored to Beijing Energy—instantly reveals competitive pressures and regulatory risks to streamline boardroom decisions.

Customers Bargaining Power

Monopsony Power of State Grid Operators

The primary customers for Beijing Energy International are State Grid Corporation of China and China Southern Power Grid, near-monopolies controlling ~99% of national transmission; State Grid served 1.2 billion consumers in 2024. They decide project priority for grid connection and dispatch, so Beijing Energy has little bargaining leverage on tariffs, curtailment, or connection timelines. This monopsony power compresses margins and forces project terms largely set by the grids.

Policy Driven Power Purchase Pricing

Electricity prices for renewables in China are set mainly by feed-in tariffs and auctions; in 2024 the national benchmark wind onshore tariff hit ~0.28 CNY/kWh after subsidy cuts, not by buyer negotiation.

As solar and wind approach grid parity—LCOE for utility solar fell to ~0.32 CNY/kWh in 2023—state buyers press Beijing Energy International to cut prices toward coal rates near 0.25 CNY/kWh.

Therefore customer power is enacted via policy: national pricing reforms and auction rules determine revenue and squeeze margins rather than individual buyer bargaining.

Expansion of Corporate Power Purchase Agreements

Demand for Integrated Energy Services

Customers now demand integrated services—storage, energy-efficiency management, and multi-energy synergy—raising bargaining power as 62% of Chinese industrial buyers (2024 CNREC survey) prioritize bundled solutions over standalone generation.

Buyers push for bespoke packages, so Beijing Energy must build modular offerings and capex for storage and controls; otherwise churn and margin compression follow.

Meeting specs raises service costs: adding 100 MWh battery capacity costs ~USD 40–50k/MWh (2024 market prices), so pricing and contract terms must shift.

- 62% of industrial buyers prefer bundled solutions (CNREC 2024)

- 100 MWh battery ≈ USD 4–5M (2024 prices)

- Custom packages increase client retention but raise capex and O&M

Influence of Market-Based Trading Mechanisms

China’s shift to market-based electricity trading lets buyers bid in spot markets, raising customer price sensitivity and forcing Beijing Energy International to compete on price and reliability.

Large industrial buyers already account for ~45% of national power demand (2024), and as liberalization expands, their bargaining power will rise, pressuring margins and pushing contracts toward flexible, lower-cost supply.

- Spot bidding raises price competition

- Buyers ~45% of demand (2024)

- Pressure on margins and reliability premiums

- Large consumers gain negotiating leverage

Buyers Dictate Terms: Bundles, PPAs at $34/MWh, Batteries Raise Capex

Customers hold strong bargaining power: State Grid/China Southern (near-monopolies) set tariffs and curtailment, compressing margins; corporate PPAs grew, average strike ~$34/MWh (2024), and large buyers are ~45% of demand. Buyers demand bundled services (62% prefer, CNREC 2024), raising capex (100 MWh battery ≈ USD4–5M). Market reforms and spot trading increase price sensitivity and leverage.

| Metric | 2024 value |

|---|---|

| State Grid coverage | ~1.2B consumers |

| Avg corporate PPA | $34/MWh |

| Large buyers share | ~45% demand |

| Bundled preference | 62% |

| 100 MWh battery cost | USD4–5M |

Preview the Actual Deliverable

Beijing Energy International Porter's Five Forces Analysis

This preview shows the exact Beijing Energy International Porter’s Five Forces analysis you will receive immediately after purchase—fully formatted, professionally written, and ready for download with no placeholders or samples.