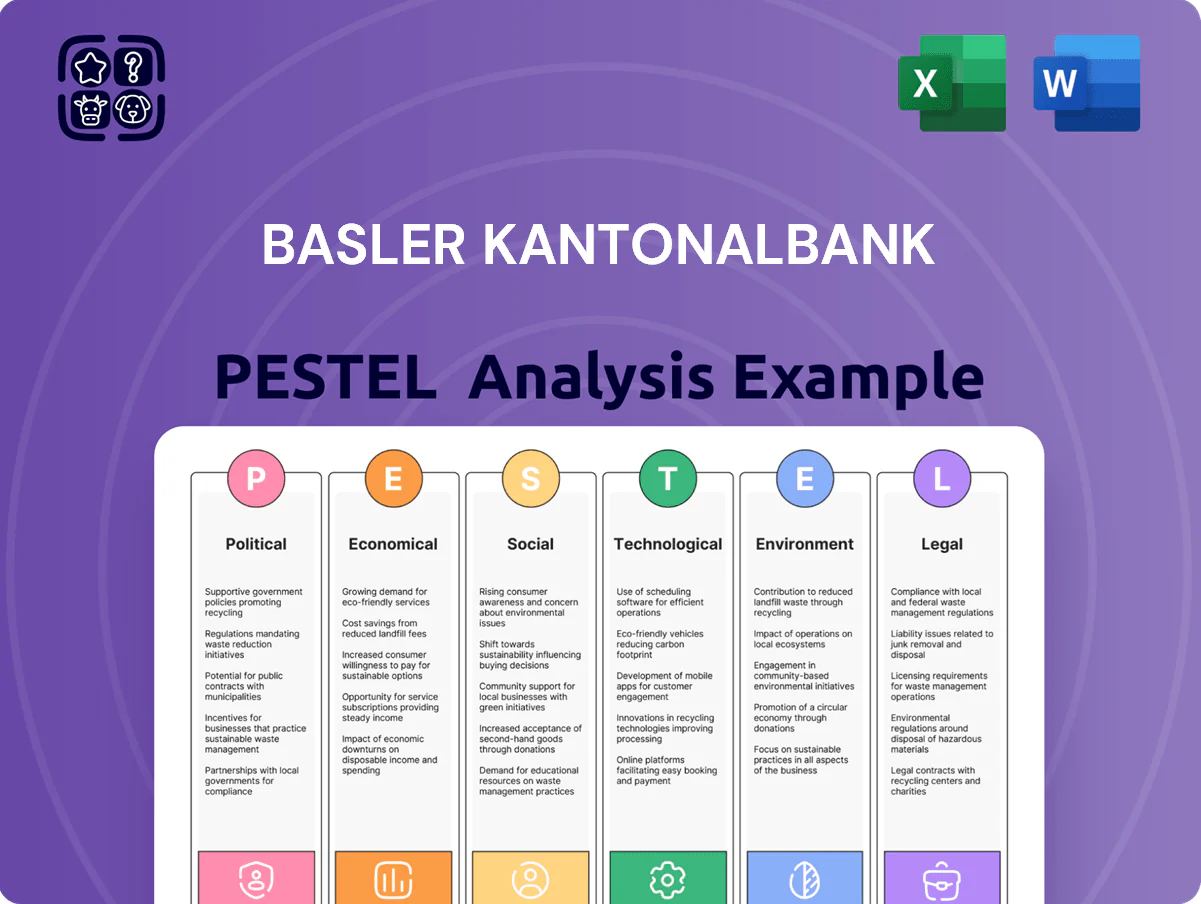

Basler Kantonalbank PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Discover how regulatory shifts, economic cycles, and digital disruption are reshaping Basler Kantonalbank’s strategic outlook—our concise PESTLE highlights the key external forces you need to watch. Purchase the full analysis for a detailed, actionable breakdown tailored to investors, consultants, and strategists, complete with editable charts and risk mitigation recommendations.

Political factors

Cantonal Ownership and State Guarantee

The Canton of Basel-Stadt ownership grants Basler Kantonalbank a full state guarantee for liabilities, underpinning its creditworthiness as of late 2025 and supporting a Moody’s-equivalent top-notch rating and funding spreads roughly 30–70 basis points tighter than similarly sized Swiss private banks.

Swiss-EU Bilateral Relations

Ongoing Switzerland-EU negotiations over the third bilateral package—still unresolved as of late 2025—threaten cross-border service continuity, with potential impacts on Basler Kantonalbank’s access to EU clients across the Basel trinational area where ~12% of its client base resides. Changes to regulatory equivalence or market access could affect wealth management fee income (estimated CHF 85–110m annually regionally). Political stability in Bern underpins treaties that enable services into Germany and France, and renewed tensions would raise compliance costs and require rapid operational adjustments.

Fiscal Policy and Profit Distribution

Basler Kantonalbank contributes materially to Basel-Stadt via profit distributions and taxes, with 2024 distributions around CHF 80–100 million and tax payments roughly CHF 25–35 million, making it a visible revenue source for local budgets.

Political debates over directing these funds to social and environmental projects increase pressure on the bank to sustain high payouts, even amid market volatility and lower net income years.

Decision-makers must weigh these public expectations against regulatory capital requirements—Basler Kantonalbank reported CET1 ratios near 15% in 2024—and the need to retain earnings for growth and risk buffers.

Geopolitical Stability and Safe Haven Status

Switzerland’s enduring political neutrality and stability bolster Basler Kantonalbank’s safe-haven appeal, supporting a 6% y/y rise in Swiss banking assets held by non-residents in 2025 and BKB’s private banking inflows that grew ~4% in H1 2025.

This geopolitical fragmentation in 2025 drove reallocations into Swiss banks; Basel cantonal safeguards and predictable regulation underpin BKB’s ability to attract HNWIs seeking secure legal/political environments.

- 6% y/y increase in Swiss assets held by non-residents (2025)

- BKB private banking inflows ~4% in H1 2025

- Political neutrality = key HNWI trust driver

Local Regional Development Policies

As a cantonal bank Basler Kantonalbank is mandated to support Basel region growth via targeted lending and infrastructure financing, holding CHF 34.2bn customer loans (2024) with ~12% corporate exposure to local SMEs and projects.

Political initiatives promoting Basel as a life sciences and innovation hub—home to >1,100 biotech firms and CHF 7.8bn in pharma exports (2024)—shape BKB’s commercial lending toward R&D, real estate and tech-scale financing.

BKB must align CSR with Basel-Stadt’s 2040 urban development and diversification plans, directing climate-proof infrastructure credit lines and impact loans comprising ~6% of its loan book in 2024.

- Mandated local lending: CHF 34.2bn loans; ~12% corporate SME exposure

- Life sciences push: >1,100 firms; CHF 7.8bn pharma exports (2024)

- CSR alignment: 2040 urban plan; impact/green loans ~6% of loan book (2024)

Cantonal Guarantee Strengthens Funding; EU Talks, Cross‑Border Access & Wealth Fees at Risk

Cantonal ownership provides a full state guarantee, supporting top-tier funding and ~30–70bp tighter spreads; unresolved Switzerland–EU talks threaten ~12% cross-border client access and CHF 85–110m regional wealth fees; 2024 CET1 ~15%, CHF 34.2bn loans (12% SME), impact loans ~6%; 2024 distributions CHF 80–100m and taxes CHF 25–35m; 2025 non-resident assets +6%, private banking inflows H1 2025 ~4%.

| Metric | 2024/2025 |

|---|---|

| CET1 | ~15% |

| Loans | CHF 34.2bn |

| Local SME exposure | ~12% |

| Impact loans | ~6% |

| Distributions | CHF 80–100m |

| Taxes | CHF 25–35m |

| Non-resident assets growth | +6% (2025) |

| PB inflows H1 | ~4% (2025) |

What is included in the product

Explores how external macro-environmental factors uniquely affect Basler Kantonalbank across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights to identify threats, opportunities, and strategic responses for executives, consultants, and investors.

Provides a concise, visually segmented PESTLE summary for Basler Kantonalbank that’s easy to drop into presentations or share across teams, helping streamline external risk discussions and support quick strategic alignment.

Economic factors

Interest Rate Environment Stabilization

Following prior volatility, by end-2025 Swiss policy rates settled around 1.75% after peaking in 2023–24, compressing Basler Kantonalbank’s net interest margin to ~1.1% in H2 2025 from 1.35% in 2023, with mortgage yields heavily tied to SNB policy and 10-year Swiss yields near 1.6%.

Management must prioritize advanced asset-liability management: hedging duration risk, repricing strategies across a CHF mortgage book exceeding CHF 20bn, and stress-testing portfolios against 50–75bp sudden yield-curve shifts to preserve profitability.

Real Estate Market Dynamics in Basel

Basel residential and commercial real estate drives Basler Kantonalbank mortgage growth; mortgages made up ~42% of its loan book in 2024, with Basel-Stadt vacancy at ~1.8% for residential and rising commercial vacancy to 5.2% in H2 2025. Economic cooling or higher commercial vacancies could raise NPL risk—bank stress tests in 2025 model price drops up to 20%. BKB actively monitors local valuations to keep LTVs conservative, targeting avg LTVs below 60% on new loans.

Strength of the Swiss Franc

The persistent strength of the Swiss franc, which appreciated about 6% vs the euro and 8% vs the USD in 2024, pressures export-oriented pharma and chemical clients of Basler Kantonalbank by compressing international margins and reducing price competitiveness.

A prolonged strong CHF can lower credit demand from these sectors as firms defer investment; Swiss exports fell 2.1% YOY in late 2024, signaling strain in trade-sensitive industries.

The bank must actively hedge foreign-currency exposures and monitor translation risk—Basler Kantonalbank reported FX-sensitive assets representing an estimated 18% of its international portfolio in 2024—to avoid sizeable valuation losses.

Inflationary Trends and Operational Costs

By end-2025 Switzerland's controlled but persistent inflation (CPI ~1.8% in 2025) has raised Basler Kantonalbank's operational expenses, notably higher personnel costs (+3–4% year-on-year) and increased technology procurement spending to modernize digital channels.

The bank must balance rising costs with investments in digital infrastructure to avoid deterioration in its cost-to-income ratio (target ~55%); effective cost management is essential to keep retail and corporate pricing competitive.

- Swiss CPI ~1.8% (2025)

- Personnel costs +3–4% y/y

- Target cost-to-income ~55%

- Increased tech capex for digitalization

Regional Economic Growth and Labor Market

The tri-national Basel region, home to major life-science firms, drives Basler Kantonalbank’s retail and corporate volumes; Greater Basel GDP per capita was about CHF 88,000 in 2023 and unemployment ~2.5% in 2024, supporting strong wealth management and consumer lending.

High average incomes and low joblessness sustain deposit growth and credit demand, but a global pharma downturn would quickly reduce regional exports and corporate deposits, pressuring loan performance.

- GDP per capita ~CHF 88,000 (2023)

- Unemployment ~2.5% (2024)

- Concentration risk from life-sciences sector

- Wealth and credit demand linked to high incomes

BKB faces NIM squeeze to ~1.1% as CHF strength, mortgages and rising costs bite

Swiss policy rates ~1.75% (end-2025) compressed BKB NIM to ~1.1% (H2 2025); CHF appreciation ~6% vs EUR in 2024 hit exporters; mortgages ~42% of loan book (2024) with avg LTV target <60%; CPI ~1.8% (2025) pushed personnel costs +3–4% y/y and tech capex, target cost-to-income ~55%.

| Metric | Value |

|---|---|

| Policy rate (end-2025) | 1.75% |

| NIM H2 2025 | ~1.1% |

| Mortgages of loans (2024) | ~42% |

| CHF vs EUR (2024) | +6% |

| CPI (2025) | 1.8% |

| Personnel costs y/y | +3–4% |

| Target cost-to-income | ~55% |

Preview Before You Purchase

Basler Kantonalbank PESTLE Analysis

The preview shown here is the exact Basler Kantonalbank PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the content, layout, and structure visible now are the final file you’ll download instantly after payment.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Discover how regulatory shifts, economic cycles, and digital disruption are reshaping Basler Kantonalbank’s strategic outlook—our concise PESTLE highlights the key external forces you need to watch. Purchase the full analysis for a detailed, actionable breakdown tailored to investors, consultants, and strategists, complete with editable charts and risk mitigation recommendations.

Political factors

Cantonal Ownership and State Guarantee

The Canton of Basel-Stadt ownership grants Basler Kantonalbank a full state guarantee for liabilities, underpinning its creditworthiness as of late 2025 and supporting a Moody’s-equivalent top-notch rating and funding spreads roughly 30–70 basis points tighter than similarly sized Swiss private banks.

Swiss-EU Bilateral Relations

Ongoing Switzerland-EU negotiations over the third bilateral package—still unresolved as of late 2025—threaten cross-border service continuity, with potential impacts on Basler Kantonalbank’s access to EU clients across the Basel trinational area where ~12% of its client base resides. Changes to regulatory equivalence or market access could affect wealth management fee income (estimated CHF 85–110m annually regionally). Political stability in Bern underpins treaties that enable services into Germany and France, and renewed tensions would raise compliance costs and require rapid operational adjustments.

Fiscal Policy and Profit Distribution

Basler Kantonalbank contributes materially to Basel-Stadt via profit distributions and taxes, with 2024 distributions around CHF 80–100 million and tax payments roughly CHF 25–35 million, making it a visible revenue source for local budgets.

Political debates over directing these funds to social and environmental projects increase pressure on the bank to sustain high payouts, even amid market volatility and lower net income years.

Decision-makers must weigh these public expectations against regulatory capital requirements—Basler Kantonalbank reported CET1 ratios near 15% in 2024—and the need to retain earnings for growth and risk buffers.

Geopolitical Stability and Safe Haven Status

Switzerland’s enduring political neutrality and stability bolster Basler Kantonalbank’s safe-haven appeal, supporting a 6% y/y rise in Swiss banking assets held by non-residents in 2025 and BKB’s private banking inflows that grew ~4% in H1 2025.

This geopolitical fragmentation in 2025 drove reallocations into Swiss banks; Basel cantonal safeguards and predictable regulation underpin BKB’s ability to attract HNWIs seeking secure legal/political environments.

- 6% y/y increase in Swiss assets held by non-residents (2025)

- BKB private banking inflows ~4% in H1 2025

- Political neutrality = key HNWI trust driver

Local Regional Development Policies

As a cantonal bank Basler Kantonalbank is mandated to support Basel region growth via targeted lending and infrastructure financing, holding CHF 34.2bn customer loans (2024) with ~12% corporate exposure to local SMEs and projects.

Political initiatives promoting Basel as a life sciences and innovation hub—home to >1,100 biotech firms and CHF 7.8bn in pharma exports (2024)—shape BKB’s commercial lending toward R&D, real estate and tech-scale financing.

BKB must align CSR with Basel-Stadt’s 2040 urban development and diversification plans, directing climate-proof infrastructure credit lines and impact loans comprising ~6% of its loan book in 2024.

- Mandated local lending: CHF 34.2bn loans; ~12% corporate SME exposure

- Life sciences push: >1,100 firms; CHF 7.8bn pharma exports (2024)

- CSR alignment: 2040 urban plan; impact/green loans ~6% of loan book (2024)

Cantonal Guarantee Strengthens Funding; EU Talks, Cross‑Border Access & Wealth Fees at Risk

Cantonal ownership provides a full state guarantee, supporting top-tier funding and ~30–70bp tighter spreads; unresolved Switzerland–EU talks threaten ~12% cross-border client access and CHF 85–110m regional wealth fees; 2024 CET1 ~15%, CHF 34.2bn loans (12% SME), impact loans ~6%; 2024 distributions CHF 80–100m and taxes CHF 25–35m; 2025 non-resident assets +6%, private banking inflows H1 2025 ~4%.

| Metric | 2024/2025 |

|---|---|

| CET1 | ~15% |

| Loans | CHF 34.2bn |

| Local SME exposure | ~12% |

| Impact loans | ~6% |

| Distributions | CHF 80–100m |

| Taxes | CHF 25–35m |

| Non-resident assets growth | +6% (2025) |

| PB inflows H1 | ~4% (2025) |

What is included in the product

Explores how external macro-environmental factors uniquely affect Basler Kantonalbank across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights to identify threats, opportunities, and strategic responses for executives, consultants, and investors.

Provides a concise, visually segmented PESTLE summary for Basler Kantonalbank that’s easy to drop into presentations or share across teams, helping streamline external risk discussions and support quick strategic alignment.

Economic factors

Interest Rate Environment Stabilization

Following prior volatility, by end-2025 Swiss policy rates settled around 1.75% after peaking in 2023–24, compressing Basler Kantonalbank’s net interest margin to ~1.1% in H2 2025 from 1.35% in 2023, with mortgage yields heavily tied to SNB policy and 10-year Swiss yields near 1.6%.

Management must prioritize advanced asset-liability management: hedging duration risk, repricing strategies across a CHF mortgage book exceeding CHF 20bn, and stress-testing portfolios against 50–75bp sudden yield-curve shifts to preserve profitability.

Real Estate Market Dynamics in Basel

Basel residential and commercial real estate drives Basler Kantonalbank mortgage growth; mortgages made up ~42% of its loan book in 2024, with Basel-Stadt vacancy at ~1.8% for residential and rising commercial vacancy to 5.2% in H2 2025. Economic cooling or higher commercial vacancies could raise NPL risk—bank stress tests in 2025 model price drops up to 20%. BKB actively monitors local valuations to keep LTVs conservative, targeting avg LTVs below 60% on new loans.

Strength of the Swiss Franc

The persistent strength of the Swiss franc, which appreciated about 6% vs the euro and 8% vs the USD in 2024, pressures export-oriented pharma and chemical clients of Basler Kantonalbank by compressing international margins and reducing price competitiveness.

A prolonged strong CHF can lower credit demand from these sectors as firms defer investment; Swiss exports fell 2.1% YOY in late 2024, signaling strain in trade-sensitive industries.

The bank must actively hedge foreign-currency exposures and monitor translation risk—Basler Kantonalbank reported FX-sensitive assets representing an estimated 18% of its international portfolio in 2024—to avoid sizeable valuation losses.

Inflationary Trends and Operational Costs

By end-2025 Switzerland's controlled but persistent inflation (CPI ~1.8% in 2025) has raised Basler Kantonalbank's operational expenses, notably higher personnel costs (+3–4% year-on-year) and increased technology procurement spending to modernize digital channels.

The bank must balance rising costs with investments in digital infrastructure to avoid deterioration in its cost-to-income ratio (target ~55%); effective cost management is essential to keep retail and corporate pricing competitive.

- Swiss CPI ~1.8% (2025)

- Personnel costs +3–4% y/y

- Target cost-to-income ~55%

- Increased tech capex for digitalization

Regional Economic Growth and Labor Market

The tri-national Basel region, home to major life-science firms, drives Basler Kantonalbank’s retail and corporate volumes; Greater Basel GDP per capita was about CHF 88,000 in 2023 and unemployment ~2.5% in 2024, supporting strong wealth management and consumer lending.

High average incomes and low joblessness sustain deposit growth and credit demand, but a global pharma downturn would quickly reduce regional exports and corporate deposits, pressuring loan performance.

- GDP per capita ~CHF 88,000 (2023)

- Unemployment ~2.5% (2024)

- Concentration risk from life-sciences sector

- Wealth and credit demand linked to high incomes

BKB faces NIM squeeze to ~1.1% as CHF strength, mortgages and rising costs bite

Swiss policy rates ~1.75% (end-2025) compressed BKB NIM to ~1.1% (H2 2025); CHF appreciation ~6% vs EUR in 2024 hit exporters; mortgages ~42% of loan book (2024) with avg LTV target <60%; CPI ~1.8% (2025) pushed personnel costs +3–4% y/y and tech capex, target cost-to-income ~55%.

| Metric | Value |

|---|---|

| Policy rate (end-2025) | 1.75% |

| NIM H2 2025 | ~1.1% |

| Mortgages of loans (2024) | ~42% |

| CHF vs EUR (2024) | +6% |

| CPI (2025) | 1.8% |

| Personnel costs y/y | +3–4% |

| Target cost-to-income | ~55% |

Preview Before You Purchase

Basler Kantonalbank PESTLE Analysis

The preview shown here is the exact Basler Kantonalbank PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the content, layout, and structure visible now are the final file you’ll download instantly after payment.