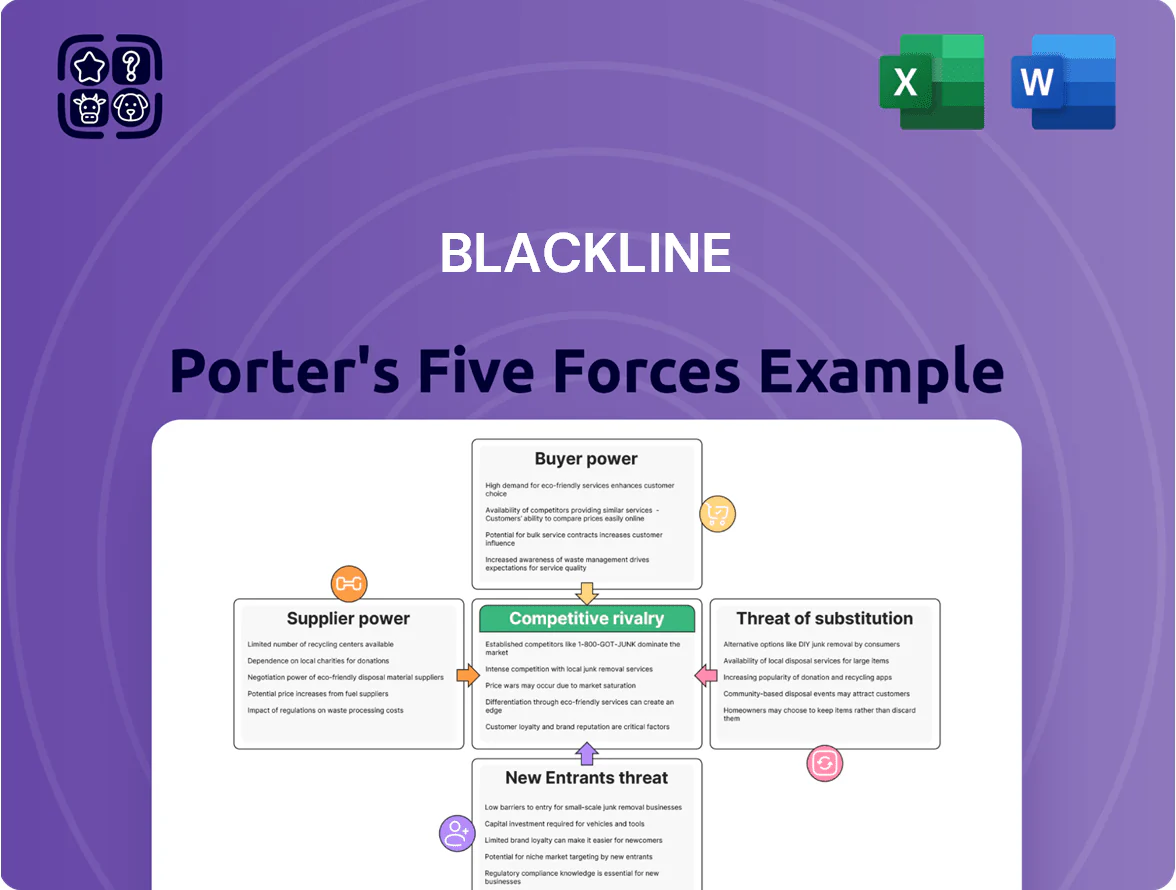

BlackLine Porter's Five Forces Analysis

From Overview to Strategy Blueprint

BlackLine faces moderate supplier concentration, rising buyer expectations, and intensifying rivalry from automation and cloud-native competitors, while barriers to entry and substitutes exert variable pressure depending on integration depth.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore BlackLine’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Cloud Infrastructure Providers

BlackLine depends on hyperscale clouds like Google Cloud Platform and AWS to run its SaaS; by late 2025 GCP + AWS + Azure held ~66% of global cloud IaaS/PaaS revenue, giving suppliers strong leverage. Migrating multi-tenant financial ledgers is costly—estimates show enterprise data migrations can exceed $5–20M and 12–24 months—so BlackLine faces limited bargaining power on price and SLAs.

Specialized Software and API Partners

Suppliers of specialized ERP connectors and API partners wield moderate bargaining power over BlackLine because the platform must integrate with SAP, Oracle, NetSuite and niche tools to automate finance; in 2025 Oracle and SAP together still power ~60% of global ERP installations, so changes to API terms or fees could raise BlackLine’s costs or slow rollouts. Maintaining certified partnerships and multi-API strategies keeps compatibility for enterprise clients and limits supplier leverage.

Highly Skilled Technical Talent

The supply of specialized software engineers and financial domain experts constrains BlackLine’s development velocity; U.S. job openings for software developers rose 12% year-over-year in 2024, tightening the market. Competition from tech giants and banks pushed median total compensation for senior cloud engineers to about $250k in 2024, increasing workforce bargaining power. BlackLine spent $143m on R&D in fiscal 2024, and must boost recruitment and retention spend to sustain innovation in financial close automation.

Data Security and Compliance Vendors

To meet global financial rules, BlackLine relies on a few certified data security and audit vendors (SOC 2, ISO 27001, GDPR) to protect sensitive customer data and pass audits; Gartner estimated in 2024 that 62% of enterprises prioritize vendor certifications when buying cloud finance software.

These providers are critical to enterprise trust and uptime, so with roughly 5–10 global vendors able to deliver full coverage, suppliers hold moderate pricing and SLA leverage, affecting BlackLine’s cost of compliance and margins.

- Dependence: few certified global vendors (≈5–10)

- Customer priority: 62% of enterprises cite certifications (Gartner 2024)

- Impact: moderate supplier leverage on price and SLAs

- Financial effect: raises compliance costs, pressures margins

Financial Data Feed Aggregators

BlackLine relies on third-party financial data feed aggregators to pull transaction feeds from global banks for reconciliation; in 2025 about 60% of enterprise reconciliations use such feeds, so feed quality is critical.

Few providers offer the required global coverage and accuracy, so price hikes or outages shift costs and risk service-level breaches—BlackLine reported integration-dependent downtime impacting ARR in past vendor incidents.

- High dependence on feed accuracy and breadth

- Concentrated supplier set raises bargaining power

- Price rises translate to higher operating costs

- Service disruptions risk SLA breaches and revenue impact

Concentrated supplier power (cloud, ERP, security) squeezes margins and raises ops risk

Suppliers exert moderate-to-high bargaining power: hyperscale clouds (GCP/AWS/Azure ~66% IaaS/PaaS revenue by late-2025) and ERP leaders (SAP+Oracle ~60% ERP installs in 2025) limit price/SLA flexibility; certified security vendors (~5–10 global) and bank feed aggregators (covering ~60% enterprise reconciliations in 2025) further raise compliance and uptime costs, pressuring margins (R&D $143M FY2024).

| Supplier | 2024–25 Stat | Impact |

|---|---|---|

| Hyperscale cloud | GCP+AWS+Azure ≈66% IaaS/PaaS revenue (late-2025) | High leverage on price/SLA |

| ERP vendors | SAP+Oracle ≈60% ERP installs (2025) | Integrations cost/time risk |

| Security vendors | ≈5–10 global cert providers | Moderate pricing on compliance |

| Bank feed aggregators | Cover ≈60% enterprise reconciliations (2025) | Concentrated outage/price risk |

What is included in the product

Tailored Porter's Five Forces analysis for BlackLine that uncovers competitive drivers, buyer and supplier leverage, entry barriers, substitute threats, and strategic implications for pricing and profitability.

A concise Porter's Five Forces snapshot tailored to BlackLine—helps you pinpoint competitive pressures and prioritize strategic moves in seconds.

Customers Bargaining Power

High Switching Costs for Enterprises

Once enterprises integrate BlackLine into their financial close, migration costs—often 6–12 months of team time and implementation fees comparable to 20–40% of annual subscription—make switching hard, creating a sticky relationship that weakens customers’ renewal bargaining power. Yet enterprise buyers push back via stringent SLAs; BlackLine reported 99.9% uptime targets in 2024 and must deliver continuous feature updates to retain large accounts. This duality lowers churn but keeps customers demanding and price-sensitive on value-added features.

Concentration of Large Global Clients

BlackLine serves roughly 30% of the Fortune 500, so losing a single global account can shave points off subscription revenue and dent market perception; in 2024 top 10 customers contributed about 24% of revenue. Large buyers run tight procurement teams and commonly secure volume discounts or bespoke SLAs, pressuring margins. Their spending power lets them request roadmap features, since enterprise accounts drive a sizable share of ARR and product prioritization.

Availability of Competitive Alternatives

The presence of competent rivals like Workiva (fiscal 2024 revenue $555M) and FloQast (estimated ARR ~$100M in 2024) gives buyers clear leverage in sales cycles, letting them pit vendors for price cuts and better SLAs.

By late 2025 market maturation—vendor comparison sites showing >40 side-by-side metrics—makes feature and performance benchmarking easy, raising customer bargaining power.

Demand for Integrated ERP Solutions

Customers often favor all-in-one ERP suites from SAP or Oracle, which bundle close-management functionality and reduce the case for standalone tools; this gives buyers leverage to demand deeper SAP/Oracle integration or price concessions from BlackLine.

BlackLine must prove superior ROI: customers compare total cost and efficiency—Gartner noted in 2024 that 42% of finance leaders prefer native ERP modules for simplicity—so BlackLine needs quantifiable uplift versus native tools to keep deals.

- All-in-one ERP preference raises bargaining power

- Demand for deeper integration with SAP/Oracle

- Price pressure vs native ERP modules

- Need to show measurable ROI (adoption, time saved)

Economic Sensitivity and Budget Constraints

In macro volatility, finance teams cut discretionary software spend; 2023 BCG found 62% of CFOs delayed tech buys, so BlackLine faces pressure on renewals and module rollouts and sees customers push for lower rates or deferments.

BlackLine counters by quantifying automation ROI—clients report up to 40% faster close times and Gartner noted finance automation reduces costs ~20%—using these metrics to protect pricing and accelerate adoption.

- 62% of CFOs delayed tech buys (BCG, 2023)

- Up to 40% faster close times (BlackLine customer data)

- ~20% cost reduction from finance automation (Gartner)

Enterprise stickiness vs. buyer leverage: Big accounts, ERP bundling and price pressure

Enterprises face high switching costs (6–12 months, 20–40% implementation fees) so renewals are sticky, yet large buyers drive 24% of BlackLine 2024 revenue and secure discounts/SLA demands. Competitors (Workiva $555M rev 2024; FloQast ~ $100M ARR 2024) and ERP bundling (42% prefer native ERP, Gartner 2024) raise customer leverage; finance cuts (62% delayed buys, BCG 2023) further pressure pricing.

| Metric | Value |

|---|---|

| Top-10 revenue share (2024) | 24% |

| Workiva 2024 revenue | $555M |

| FloQast 2024 ARR | $100M est |

| ERP preference (Gartner 2024) | 42% |

| CFOs delaying buys (BCG 2023) | 62% |

What You See Is What You Get

BlackLine Porter's Five Forces Analysis

This preview shows the exact BlackLine Porter's Five Forces analysis you'll receive immediately after purchase—fully formatted, professionally written, and ready for download with no placeholders or mockups.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

BlackLine faces moderate supplier concentration, rising buyer expectations, and intensifying rivalry from automation and cloud-native competitors, while barriers to entry and substitutes exert variable pressure depending on integration depth.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore BlackLine’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Cloud Infrastructure Providers

BlackLine depends on hyperscale clouds like Google Cloud Platform and AWS to run its SaaS; by late 2025 GCP + AWS + Azure held ~66% of global cloud IaaS/PaaS revenue, giving suppliers strong leverage. Migrating multi-tenant financial ledgers is costly—estimates show enterprise data migrations can exceed $5–20M and 12–24 months—so BlackLine faces limited bargaining power on price and SLAs.

Specialized Software and API Partners

Suppliers of specialized ERP connectors and API partners wield moderate bargaining power over BlackLine because the platform must integrate with SAP, Oracle, NetSuite and niche tools to automate finance; in 2025 Oracle and SAP together still power ~60% of global ERP installations, so changes to API terms or fees could raise BlackLine’s costs or slow rollouts. Maintaining certified partnerships and multi-API strategies keeps compatibility for enterprise clients and limits supplier leverage.

Highly Skilled Technical Talent

The supply of specialized software engineers and financial domain experts constrains BlackLine’s development velocity; U.S. job openings for software developers rose 12% year-over-year in 2024, tightening the market. Competition from tech giants and banks pushed median total compensation for senior cloud engineers to about $250k in 2024, increasing workforce bargaining power. BlackLine spent $143m on R&D in fiscal 2024, and must boost recruitment and retention spend to sustain innovation in financial close automation.

Data Security and Compliance Vendors

To meet global financial rules, BlackLine relies on a few certified data security and audit vendors (SOC 2, ISO 27001, GDPR) to protect sensitive customer data and pass audits; Gartner estimated in 2024 that 62% of enterprises prioritize vendor certifications when buying cloud finance software.

These providers are critical to enterprise trust and uptime, so with roughly 5–10 global vendors able to deliver full coverage, suppliers hold moderate pricing and SLA leverage, affecting BlackLine’s cost of compliance and margins.

- Dependence: few certified global vendors (≈5–10)

- Customer priority: 62% of enterprises cite certifications (Gartner 2024)

- Impact: moderate supplier leverage on price and SLAs

- Financial effect: raises compliance costs, pressures margins

Financial Data Feed Aggregators

BlackLine relies on third-party financial data feed aggregators to pull transaction feeds from global banks for reconciliation; in 2025 about 60% of enterprise reconciliations use such feeds, so feed quality is critical.

Few providers offer the required global coverage and accuracy, so price hikes or outages shift costs and risk service-level breaches—BlackLine reported integration-dependent downtime impacting ARR in past vendor incidents.

- High dependence on feed accuracy and breadth

- Concentrated supplier set raises bargaining power

- Price rises translate to higher operating costs

- Service disruptions risk SLA breaches and revenue impact

Concentrated supplier power (cloud, ERP, security) squeezes margins and raises ops risk

Suppliers exert moderate-to-high bargaining power: hyperscale clouds (GCP/AWS/Azure ~66% IaaS/PaaS revenue by late-2025) and ERP leaders (SAP+Oracle ~60% ERP installs in 2025) limit price/SLA flexibility; certified security vendors (~5–10 global) and bank feed aggregators (covering ~60% enterprise reconciliations in 2025) further raise compliance and uptime costs, pressuring margins (R&D $143M FY2024).

| Supplier | 2024–25 Stat | Impact |

|---|---|---|

| Hyperscale cloud | GCP+AWS+Azure ≈66% IaaS/PaaS revenue (late-2025) | High leverage on price/SLA |

| ERP vendors | SAP+Oracle ≈60% ERP installs (2025) | Integrations cost/time risk |

| Security vendors | ≈5–10 global cert providers | Moderate pricing on compliance |

| Bank feed aggregators | Cover ≈60% enterprise reconciliations (2025) | Concentrated outage/price risk |

What is included in the product

Tailored Porter's Five Forces analysis for BlackLine that uncovers competitive drivers, buyer and supplier leverage, entry barriers, substitute threats, and strategic implications for pricing and profitability.

A concise Porter's Five Forces snapshot tailored to BlackLine—helps you pinpoint competitive pressures and prioritize strategic moves in seconds.

Customers Bargaining Power

High Switching Costs for Enterprises

Once enterprises integrate BlackLine into their financial close, migration costs—often 6–12 months of team time and implementation fees comparable to 20–40% of annual subscription—make switching hard, creating a sticky relationship that weakens customers’ renewal bargaining power. Yet enterprise buyers push back via stringent SLAs; BlackLine reported 99.9% uptime targets in 2024 and must deliver continuous feature updates to retain large accounts. This duality lowers churn but keeps customers demanding and price-sensitive on value-added features.

Concentration of Large Global Clients

BlackLine serves roughly 30% of the Fortune 500, so losing a single global account can shave points off subscription revenue and dent market perception; in 2024 top 10 customers contributed about 24% of revenue. Large buyers run tight procurement teams and commonly secure volume discounts or bespoke SLAs, pressuring margins. Their spending power lets them request roadmap features, since enterprise accounts drive a sizable share of ARR and product prioritization.

Availability of Competitive Alternatives

The presence of competent rivals like Workiva (fiscal 2024 revenue $555M) and FloQast (estimated ARR ~$100M in 2024) gives buyers clear leverage in sales cycles, letting them pit vendors for price cuts and better SLAs.

By late 2025 market maturation—vendor comparison sites showing >40 side-by-side metrics—makes feature and performance benchmarking easy, raising customer bargaining power.

Demand for Integrated ERP Solutions

Customers often favor all-in-one ERP suites from SAP or Oracle, which bundle close-management functionality and reduce the case for standalone tools; this gives buyers leverage to demand deeper SAP/Oracle integration or price concessions from BlackLine.

BlackLine must prove superior ROI: customers compare total cost and efficiency—Gartner noted in 2024 that 42% of finance leaders prefer native ERP modules for simplicity—so BlackLine needs quantifiable uplift versus native tools to keep deals.

- All-in-one ERP preference raises bargaining power

- Demand for deeper integration with SAP/Oracle

- Price pressure vs native ERP modules

- Need to show measurable ROI (adoption, time saved)

Economic Sensitivity and Budget Constraints

In macro volatility, finance teams cut discretionary software spend; 2023 BCG found 62% of CFOs delayed tech buys, so BlackLine faces pressure on renewals and module rollouts and sees customers push for lower rates or deferments.

BlackLine counters by quantifying automation ROI—clients report up to 40% faster close times and Gartner noted finance automation reduces costs ~20%—using these metrics to protect pricing and accelerate adoption.

- 62% of CFOs delayed tech buys (BCG, 2023)

- Up to 40% faster close times (BlackLine customer data)

- ~20% cost reduction from finance automation (Gartner)

Enterprise stickiness vs. buyer leverage: Big accounts, ERP bundling and price pressure

Enterprises face high switching costs (6–12 months, 20–40% implementation fees) so renewals are sticky, yet large buyers drive 24% of BlackLine 2024 revenue and secure discounts/SLA demands. Competitors (Workiva $555M rev 2024; FloQast ~ $100M ARR 2024) and ERP bundling (42% prefer native ERP, Gartner 2024) raise customer leverage; finance cuts (62% delayed buys, BCG 2023) further pressure pricing.

| Metric | Value |

|---|---|

| Top-10 revenue share (2024) | 24% |

| Workiva 2024 revenue | $555M |

| FloQast 2024 ARR | $100M est |

| ERP preference (Gartner 2024) | 42% |

| CFOs delaying buys (BCG 2023) | 62% |

What You See Is What You Get

BlackLine Porter's Five Forces Analysis

This preview shows the exact BlackLine Porter's Five Forces analysis you'll receive immediately after purchase—fully formatted, professionally written, and ready for download with no placeholders or mockups.