Blade Air Mobility PESTLE Analysis

Your Competitive Advantage Starts with This Report

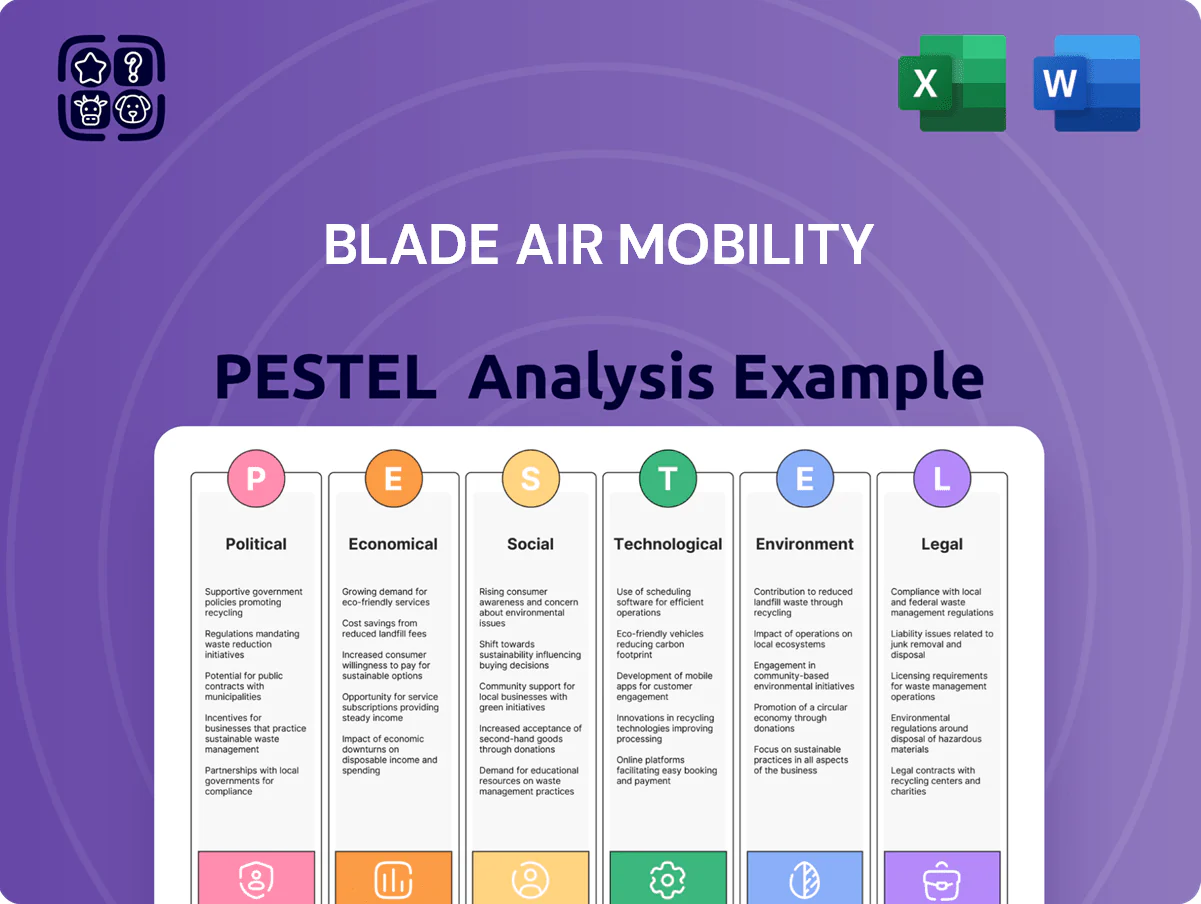

Discover how political, economic, social, technological, legal, and environmental forces are reshaping Blade Air Mobility’s prospects—our concise PESTLE highlights key risks and opportunities to inform smarter decisions. Buy the full analysis for a complete, actionable report—ready for strategy sessions, investor decks, and competitive planning.

Political factors

Municipal Support for Vertiport Development

Local government cooperation is essential for securing landing rights and infrastructure; NYC projects reported 18% faster permitting when city agencies were engaged early, and Blade cites municipal partnerships across 12 US markets as strategic assets.

Political shifts in key markets like New York and Southern France can alter zoning—France passed 2024 draft urban mobility rules enabling rooftop vertiports in select zones, potentially reducing development costs by up to 22% in pilot cities.

Maintaining strong relationships with city planners and transportation departments remains a top priority for operational continuity; Blade’s 2025 target includes formal MOUs with at least five major municipalities to lock in access and receive priority airspace coordination.

Federal Subsidies for Green Aviation

Federal grants and tax credits—including the FAA’s 2024 $100m AAM funding and IRS clean energy tax incentives—can accelerate Blade’s shift to electric vertical aircraft by lowering capex and certification costs.

Decarbonization programs like the Inflation Reduction Act have funneled billions into sustainable transport, offering Blade access to subsidies that reduce operating and R&D burn.

Shifts in federal priorities risk funding volatility: EPA and DOT budget changes between 2024–2025 showed year-over-year variances up to 15%, affecting infrastructure and R&D support.

International Expansion and Geopolitical Stability

As Blade Air Mobility expands into India and Europe it must navigate varied political and regulatory regimes: India’s civil aviation market grew 11% in 2024 while the EU is harmonizing UAM rules, affecting route approvals and safety certifications.

Geopolitical stability influences investor confidence and project viability; for example, FDI into India reached $46.6B in FY2023–24, underpinning infrastructure but exposing projects to policy shifts.

Trade policies and foreign investment rules shape partnerships—local ownership caps and data-localization laws can constrain Blade’s ability to source tech and form joint ventures rapidly.

Healthcare Policy and Organ Logistics

Blade MediMobility is exposed to federal healthcare regulations and Organ Procurement Organization rules; updates to the National Organ Transplant Act or CMS policies can change demand for specialized transport—CMS reported organ transplant payments totaling $5.6B in 2023, which influences service volumes.

Shifts in Medicare reimbursement rates or removal of payment barriers could raise profitability for organ flights; a 10% reimbursement change can materially affect margins given high fixed aircraft costs.

Political advocacy for streamlined organ logistics, including bipartisan bills in 2024 promoting faster transport corridors, could expand Blade’s dedicated medical wing and increase addressable market share.

- Dependent on NOTA and CMS rules; $5.6B transplant payments (2023)

- Medicare reimbursement shifts (±10%) materially affect margins

- 2024 bipartisan advocacy may expand organ transport demand

Urban Air Traffic Management Policies

The integration of low-altitude aircraft into national airspace needs coordinated political and regulatory efforts; FAA’s UAS rulemaking and NASA/FAA AAM roadmap target 2024–2026 standards to manage up to 2,000 daily urban eVTOL flights in major metros by 2030.

Governments must create frameworks balancing increased urban air traffic density with safety and security; projected UAM market value of $1.5–2.1 trillion by 2040 hinges on robust air traffic management systems.

Blade must engage in policy discussions and ICAO/FAA working groups to ensure future UATM architectures support scalable operations and their business model, reducing compliance-driven delays and potential market-entry costs.

- FAA/NASA AAM roadmap (2024–2026) guides UATM standards

- Estimate: up to 2,000 daily eVTOL flights in major metros by 2030

- UAM market potential: $1.5–2.1 trillion by 2040

- Blade engagement in policy reduces regulatory risk and scaling costs

Policy tailwinds boost eVTOL growth: faster NYC permitting, $100M FAA grants, IRA cuts

Political factors: municipal partnerships accelerate permitting (18% faster in NYC); FAA/NASA AAM roadmap (2024–26) targets UATM for ~2,000 daily eVTOL flights by 2030; FAA AAM $100m grant (2024) and IRA/IRS incentives cut EV eVTOL capex up to ~22%; organ-transplant reimbursements ($5.6B payments 2023) tie Medicare policy ±10% to margins; India FDI $46.6B (FY23–24) supports expansion.

| Metric | Value |

|---|---|

| NYC permitting speed | +18% |

| FAA AAM grant (2024) | $100m |

| eVTOL daily flights (2030 est.) | ~2,000 |

| Organ transplant payments (2023) | $5.6B |

| India FDI (FY23–24) | $46.6B |

What is included in the product

Explores how macro-environmental factors uniquely affect Blade Air Mobility across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven insights and forward-looking implications tailored for executives, investors, and strategists to identify risks, opportunities, and actionable scenarios.

A concise, visually segmented PESTLE summary of Blade Air Mobility that highlights regulatory, economic, social, technological, legal, and environmental factors—ideal for quick insertion into presentations or strategy sessions.

Economic factors

Consumer Discretionary Spending Trends

Demand for Blade’s passenger services tracks HNWI disposable income; US household wealth rebounded to a record 2024 Q4 level of about $140 trillion, supporting luxury travel and airport-transfer volumes as time-saving services gain priority.

Capital Intensity of EVA Transition

Transitioning from helicopters to Electric Vertical Aircraft (EVA) demands heavy capital: eVTOL unit costs range $1–5M each and vertiport charging upgrades can add $0.5–2M per site, pressuring Blade’s liquidity without JV or OEM financing.

Blade must secure favorable financing; with US 2025 prime rates near 8% and commercial lending spreads elevated, higher borrowing costs could erode margins and extend payback periods beyond projected 5–8 years.

Strategic partnerships, lease structures, and credit facilities will be critical to finance fleet rollouts and meet projected 2026–2030 capex of tens to hundreds of millions while preserving operational cash flow.

Fuel Price Volatility and Operating Margins

Until full electrification, Blade remains exposed to jet fuel volatility; U.S. jet fuel averages rose 46% year-over-year to about $3.10/gal in 2024, a spike that can compress margins on a business where fuel often represents 20–30% of variable costs.

Sudden price jumps force surcharges that risk deterring price-sensitive riders—Blade reported fare elasticity concerns after fuel-linked surcharges in 2023 reduced repeat bookings by an estimated mid-single-digit percentage.

Hedging fuel and transitioning to electric VTOLs are Blade’s primary defenses: modest hedging programs offset near-term swings, while management targets fleet electrification timelines to cut fuel exposure and lower operating costs by up to 40% per flight in pilot studies.

Economic Resilience of Medical Logistics

Blade Air Mobility’s organ transport division delivers recurring revenue largely insulated from economic cycles; in 2024 Blade reported MediMobility contributed an estimated 12–15% of consolidated revenue and showed high utilization rates tied to hospital scheduling rather than consumer spending.

Because organ transplants are essential, demand remains stable despite inflation—transplant volumes in the U.S. rose ~3% in 2023–24—providing predictable cash flow that cushions the more cyclical passenger helicopter and seaplane segments.

- Stable revenue: MediMobility ≈12–15% of 2024 revenue

- Insulation: transplant demand up ~3% (2023–24)

- Financial stabilizer: supports volatile passenger operations

Interest Rates and Infrastructure Financing

High US interest rates (Fed funds 5.25–5.50% in 2024) raise Blade’s cost of debt for capital-intensive vertiport and charging infrastructure, increasing project financing costs by an estimated 100–300 bps versus pre-2022 lows.

Blade’s asset-light model reduces balance-sheet exposure, but building vertiports still needs significant capex—industry estimates for a single vertiport range $2–10m—making low borrowing costs critical for rapid rollout.

Favorable borrowing conditions (e.g., AAA muni yields falling from ~4.0% to <3.0%) would enable faster scaling and lower unit economics for electric flight networks.

- Fed funds 5.25–5.50% (2024)

- Vertiport capex est. $2–10m each

- Higher rates add ~100–300 bps to financing costs

- Muni yield drop <3.0% aids expansion

HNWI wealth fuels Blade demand; eVTOL capex and rates squeeze liquidity

Blade’s demand tied to HNWI wealth (US household wealth ≈$140T in 2024) supports premium travel, while EV adoption requires $1–5M eVTOL units and $0.5–2M vertiport upgrades, pressuring liquidity amid 2024–25 rates (Fed funds 5.25–5.50%; prime ≈8%). MediMobility (≈12–15% of 2024 revenue) provides stable, ~3% rising transplant demand; hedging and partnerships needed to offset fuel ($3.10/gal 2024) and high financing costs.

| Metric | Value |

|---|---|

| Household wealth (2024 Q4) | $140T |

| eVTOL unit cost | $1–5M |

| Vertiport capex | $0.5–2M/site |

| Fed funds (2024) | 5.25–5.50% |

| Jet fuel (2024 avg) | $3.10/gal |

| MediMobility revenue | 12–15% |

Preview the Actual Deliverable

Blade Air Mobility PESTLE Analysis

The preview shown here is the exact Blade Air Mobility PESTLE analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic or investment decisions.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Competitive Advantage Starts with This Report

Discover how political, economic, social, technological, legal, and environmental forces are reshaping Blade Air Mobility’s prospects—our concise PESTLE highlights key risks and opportunities to inform smarter decisions. Buy the full analysis for a complete, actionable report—ready for strategy sessions, investor decks, and competitive planning.

Political factors

Municipal Support for Vertiport Development

Local government cooperation is essential for securing landing rights and infrastructure; NYC projects reported 18% faster permitting when city agencies were engaged early, and Blade cites municipal partnerships across 12 US markets as strategic assets.

Political shifts in key markets like New York and Southern France can alter zoning—France passed 2024 draft urban mobility rules enabling rooftop vertiports in select zones, potentially reducing development costs by up to 22% in pilot cities.

Maintaining strong relationships with city planners and transportation departments remains a top priority for operational continuity; Blade’s 2025 target includes formal MOUs with at least five major municipalities to lock in access and receive priority airspace coordination.

Federal Subsidies for Green Aviation

Federal grants and tax credits—including the FAA’s 2024 $100m AAM funding and IRS clean energy tax incentives—can accelerate Blade’s shift to electric vertical aircraft by lowering capex and certification costs.

Decarbonization programs like the Inflation Reduction Act have funneled billions into sustainable transport, offering Blade access to subsidies that reduce operating and R&D burn.

Shifts in federal priorities risk funding volatility: EPA and DOT budget changes between 2024–2025 showed year-over-year variances up to 15%, affecting infrastructure and R&D support.

International Expansion and Geopolitical Stability

As Blade Air Mobility expands into India and Europe it must navigate varied political and regulatory regimes: India’s civil aviation market grew 11% in 2024 while the EU is harmonizing UAM rules, affecting route approvals and safety certifications.

Geopolitical stability influences investor confidence and project viability; for example, FDI into India reached $46.6B in FY2023–24, underpinning infrastructure but exposing projects to policy shifts.

Trade policies and foreign investment rules shape partnerships—local ownership caps and data-localization laws can constrain Blade’s ability to source tech and form joint ventures rapidly.

Healthcare Policy and Organ Logistics

Blade MediMobility is exposed to federal healthcare regulations and Organ Procurement Organization rules; updates to the National Organ Transplant Act or CMS policies can change demand for specialized transport—CMS reported organ transplant payments totaling $5.6B in 2023, which influences service volumes.

Shifts in Medicare reimbursement rates or removal of payment barriers could raise profitability for organ flights; a 10% reimbursement change can materially affect margins given high fixed aircraft costs.

Political advocacy for streamlined organ logistics, including bipartisan bills in 2024 promoting faster transport corridors, could expand Blade’s dedicated medical wing and increase addressable market share.

- Dependent on NOTA and CMS rules; $5.6B transplant payments (2023)

- Medicare reimbursement shifts (±10%) materially affect margins

- 2024 bipartisan advocacy may expand organ transport demand

Urban Air Traffic Management Policies

The integration of low-altitude aircraft into national airspace needs coordinated political and regulatory efforts; FAA’s UAS rulemaking and NASA/FAA AAM roadmap target 2024–2026 standards to manage up to 2,000 daily urban eVTOL flights in major metros by 2030.

Governments must create frameworks balancing increased urban air traffic density with safety and security; projected UAM market value of $1.5–2.1 trillion by 2040 hinges on robust air traffic management systems.

Blade must engage in policy discussions and ICAO/FAA working groups to ensure future UATM architectures support scalable operations and their business model, reducing compliance-driven delays and potential market-entry costs.

- FAA/NASA AAM roadmap (2024–2026) guides UATM standards

- Estimate: up to 2,000 daily eVTOL flights in major metros by 2030

- UAM market potential: $1.5–2.1 trillion by 2040

- Blade engagement in policy reduces regulatory risk and scaling costs

Policy tailwinds boost eVTOL growth: faster NYC permitting, $100M FAA grants, IRA cuts

Political factors: municipal partnerships accelerate permitting (18% faster in NYC); FAA/NASA AAM roadmap (2024–26) targets UATM for ~2,000 daily eVTOL flights by 2030; FAA AAM $100m grant (2024) and IRA/IRS incentives cut EV eVTOL capex up to ~22%; organ-transplant reimbursements ($5.6B payments 2023) tie Medicare policy ±10% to margins; India FDI $46.6B (FY23–24) supports expansion.

| Metric | Value |

|---|---|

| NYC permitting speed | +18% |

| FAA AAM grant (2024) | $100m |

| eVTOL daily flights (2030 est.) | ~2,000 |

| Organ transplant payments (2023) | $5.6B |

| India FDI (FY23–24) | $46.6B |

What is included in the product

Explores how macro-environmental factors uniquely affect Blade Air Mobility across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven insights and forward-looking implications tailored for executives, investors, and strategists to identify risks, opportunities, and actionable scenarios.

A concise, visually segmented PESTLE summary of Blade Air Mobility that highlights regulatory, economic, social, technological, legal, and environmental factors—ideal for quick insertion into presentations or strategy sessions.

Economic factors

Consumer Discretionary Spending Trends

Demand for Blade’s passenger services tracks HNWI disposable income; US household wealth rebounded to a record 2024 Q4 level of about $140 trillion, supporting luxury travel and airport-transfer volumes as time-saving services gain priority.

Capital Intensity of EVA Transition

Transitioning from helicopters to Electric Vertical Aircraft (EVA) demands heavy capital: eVTOL unit costs range $1–5M each and vertiport charging upgrades can add $0.5–2M per site, pressuring Blade’s liquidity without JV or OEM financing.

Blade must secure favorable financing; with US 2025 prime rates near 8% and commercial lending spreads elevated, higher borrowing costs could erode margins and extend payback periods beyond projected 5–8 years.

Strategic partnerships, lease structures, and credit facilities will be critical to finance fleet rollouts and meet projected 2026–2030 capex of tens to hundreds of millions while preserving operational cash flow.

Fuel Price Volatility and Operating Margins

Until full electrification, Blade remains exposed to jet fuel volatility; U.S. jet fuel averages rose 46% year-over-year to about $3.10/gal in 2024, a spike that can compress margins on a business where fuel often represents 20–30% of variable costs.

Sudden price jumps force surcharges that risk deterring price-sensitive riders—Blade reported fare elasticity concerns after fuel-linked surcharges in 2023 reduced repeat bookings by an estimated mid-single-digit percentage.

Hedging fuel and transitioning to electric VTOLs are Blade’s primary defenses: modest hedging programs offset near-term swings, while management targets fleet electrification timelines to cut fuel exposure and lower operating costs by up to 40% per flight in pilot studies.

Economic Resilience of Medical Logistics

Blade Air Mobility’s organ transport division delivers recurring revenue largely insulated from economic cycles; in 2024 Blade reported MediMobility contributed an estimated 12–15% of consolidated revenue and showed high utilization rates tied to hospital scheduling rather than consumer spending.

Because organ transplants are essential, demand remains stable despite inflation—transplant volumes in the U.S. rose ~3% in 2023–24—providing predictable cash flow that cushions the more cyclical passenger helicopter and seaplane segments.

- Stable revenue: MediMobility ≈12–15% of 2024 revenue

- Insulation: transplant demand up ~3% (2023–24)

- Financial stabilizer: supports volatile passenger operations

Interest Rates and Infrastructure Financing

High US interest rates (Fed funds 5.25–5.50% in 2024) raise Blade’s cost of debt for capital-intensive vertiport and charging infrastructure, increasing project financing costs by an estimated 100–300 bps versus pre-2022 lows.

Blade’s asset-light model reduces balance-sheet exposure, but building vertiports still needs significant capex—industry estimates for a single vertiport range $2–10m—making low borrowing costs critical for rapid rollout.

Favorable borrowing conditions (e.g., AAA muni yields falling from ~4.0% to <3.0%) would enable faster scaling and lower unit economics for electric flight networks.

- Fed funds 5.25–5.50% (2024)

- Vertiport capex est. $2–10m each

- Higher rates add ~100–300 bps to financing costs

- Muni yield drop <3.0% aids expansion

HNWI wealth fuels Blade demand; eVTOL capex and rates squeeze liquidity

Blade’s demand tied to HNWI wealth (US household wealth ≈$140T in 2024) supports premium travel, while EV adoption requires $1–5M eVTOL units and $0.5–2M vertiport upgrades, pressuring liquidity amid 2024–25 rates (Fed funds 5.25–5.50%; prime ≈8%). MediMobility (≈12–15% of 2024 revenue) provides stable, ~3% rising transplant demand; hedging and partnerships needed to offset fuel ($3.10/gal 2024) and high financing costs.

| Metric | Value |

|---|---|

| Household wealth (2024 Q4) | $140T |

| eVTOL unit cost | $1–5M |

| Vertiport capex | $0.5–2M/site |

| Fed funds (2024) | 5.25–5.50% |

| Jet fuel (2024 avg) | $3.10/gal |

| MediMobility revenue | 12–15% |

Preview the Actual Deliverable

Blade Air Mobility PESTLE Analysis

The preview shown here is the exact Blade Air Mobility PESTLE analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic or investment decisions.