Bank of Montreal Business Model Canvas

Bank of Montreal Business Model Canvas: Ready-to-Use Blueprint for Investors & Strategists

Unlock the full strategic blueprint behind Bank of Montreal’s business model—our in-depth Business Model Canvas maps customer segments, value propositions, channels, revenue streams, and cost drivers in a clear, actionable format; perfect for investors, advisors, and strategists seeking a ready-to-use Word/Excel template to benchmark, plan, and implement winning financial strategies.

Partnerships

Strategic FinTech Alliances

BMO partners with fintechs to speed digital transformation and add AI-driven insights and seamless mobile payments, lowering development costs; by 2024 BMO reported a 25% increase in digital active users to 2.3 million, reflecting these integrations.

Global Payment Networks

BMO integrates tightly with Visa and Mastercard, enabling acceptance at over 52 million merchant locations worldwide and supporting card volumes that drove C$45.8 billion in payments revenue across Canadian and U.S. retail operations in FY2024; these networks sustain card liquidity, cross-border settlement, and real-time authorization for BMO’s consumer and commercial cards.

Loyalty Program Providers

BMO partners with major loyalty platforms like AIR MILES to offer rewards that boost credit‑card spend and retention; in 2024 BMO cards generated roughly CAD 4.2B in purchase volume tied to rewards, lifting active card spend by ~7% vs non‑reward cards.

Third Party Mortgage Brokers

The bank uses a network of independent mortgage brokers across Canada and the US to widen reach and grew residential mortgage balances by about 4% year-over-year to CAD 190 billion in 2024, with brokers supplying a large share of new originations.

Strong broker relationships keep a steady pipeline of quality applications, lowering acquisition costs and supporting market-share gains in key provinces and US states.

- ~CAD 190B residential mortgages (2024)

- Brokers drive significant new originations—single-digit % growth YoY

- Lower acquisition cost, higher loan quality

Government and Regulatory Bodies

BMO works with the Bank of Canada, Federal Reserve, Office of the Superintendent of Financial Institutions (OSFI) and US regulators to follow evolving rules and support systemic stability, filing quarterly Basel III CET1 ratios (11.8% at 2025-Q3) and large-value payment controls.

These ties include policy input, anti-money-laundering reporting and transaction monitoring; sustaining regulatory approval preserves BMO’s licence and reputation after paying C$350m in compliance penalties in 2023.

- Quarterly CET1 11.8% (2025-Q3)

- C$350m compliance penalty (2023)

- Active OSFI/Bank of Canada/Fed engagement

- AML/reporting and systemic-stability focus

BMO partners fuel digital surge, C$45.8B payments & CAD190B mortgages

BMO’s key partners—fintechs, Visa/Mastercard, loyalty programs, mortgage brokers, and regulators—drive digital growth (2.3M digital users, +25% in 2024), card payments (C$45.8B payments revenue FY2024), mortgage scale (~CAD190B residential balances 2024), and compliance (CET1 11.8% 2025‑Q3; C$350m penalty 2023).

| Partner | Role | Key 2024/2025 Metric |

|---|---|---|

| Fintechs | Digital+AI | 2.3M digital users (+25% 2024) |

| Visa/Mastercard | Card rails | C$45.8B payments revenue FY2024 |

| Loyalty | Rewards | ~C$4.2B reward-linked spend 2024 |

| Brokers | Mortgage originations | ~CAD190B mortgages 2024 |

| Regulators | Compliance | CET1 11.8% (2025‑Q3); C$350m penalty 2023 |

What is included in the product

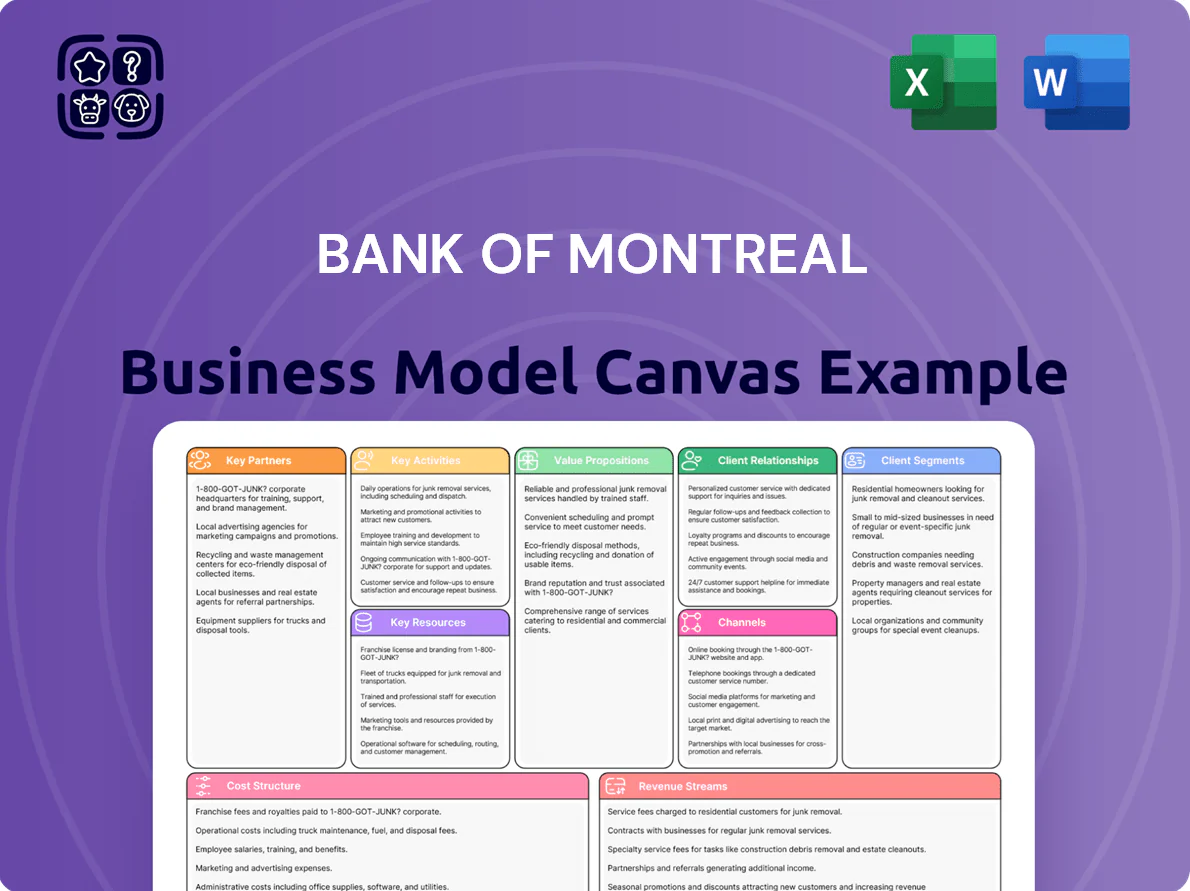

A concise, investor-ready Business Model Canvas for Bank of Montreal covering nine BMC blocks—customer segments, value propositions, channels, customer relationships, revenue streams, key resources, key activities, key partners, and cost structure—aligned with real-world operations and strategic priorities to support presentations, funding discussions, and strategic analysis.

High-level, editable Business Model Canvas for Bank of Montreal that condenses strategy into a one-page snapshot—ideal for quick executive reviews, team collaboration, and saving hours of formatting when comparing banks or preparing board-ready deliverables.

Activities

Financial Product Development

BMO continuously designs and refines products from savings accounts to complex derivatives for corporates, using market research, actuarial analysis, and competitive benchmarking; in 2024 BMO reported $52.5B in deposits and business lending growth of 6% YoY, showing product innovation drives deposit inflows and loan book expansion.

Risk Management and Credit Assessment

BMO rigorously evaluates borrower creditworthiness—retail and corporate—aiming to keep net impaired loan ratio low (0.27% at Q4 2025) and reduce defaults; credit committees and stress tests guide decisions. The bank uses machine learning and advanced analytics for market, liquidity and operational risk modelling, supporting CET1 ratio management (12.8% at FY2024) to protect shareholder capital and depositor funds.

Digital Infrastructure Maintenance

BMO spends about CAD 1.2 billion annually on technology and digital platforms (2024 disclosure), upgrading mobile apps, web portals and backend systems to sustain 24/7 uptime and process millions of transactions daily; secure infrastructure cut branch-related costs and supports customer satisfaction metrics—digital NPS rose to 34 in 2024.

Customer Relationship Management

BMO drives long-term loyalty via proactive outreach, personalized financial planning, and dedicated account teams for HNW clients, plus multi-channel responsive support; in 2024 BMO reported 10% YoY growth in wealth AUM to C$330 billion, boosting cross-sell rates and client lifetime value.

- Personalized planning for retail and commercial clients

- Dedicated HNW account management

- Multi-channel responsive support

- Wealth AUM C$330B (2024), +10% YoY

- Higher cross-sell improves lifetime value

Regulatory Compliance and Auditing

BMO commits substantial resources to regulatory compliance across its global operations, running regular internal audits and submitting reports to regulators to combat money laundering and enforce fair lending; in 2024 BMO’s compliance and conduct costs were CA$1.1bn, reflecting intensified monitoring and remediation efforts.

Breach avoidance is core: non-compliance risks costly fines and reputational loss, so BMO’s compliance teams and external auditors perform continuous reviews and controls testing to maintain license and market trust.

- CA$1.1bn compliance costs (2024)

- Ongoing AML (anti-money laundering) audits

- Regular external regulator reporting

- Focus on fair lending controls and remediation

BMO boosts AUM to C$330bn, invests CA$2.3bn in tech & compliance with strong CET1

BMO designs retail to corporate products, manages credit and liquidity (CET1 12.8% FY2024), spends CA$1.2bn on tech (2024) and CA$1.1bn on compliance (2024), grows wealth AUM to C$330bn (+10% YoY) and keeps impaired loans low (net impaired 0.27% Q4 2025), using ML risk models and multi-channel client servicing to boost cross-sell and retention.

| Metric | Value |

|---|---|

| Deposits | CA$52.5bn (2024) |

| Wealth AUM | CA$330bn (+10% YoY) |

| Tech spend | CA$1.2bn (2024) |

| Compliance cost | CA$1.1bn (2024) |

| CET1 | 12.8% (FY2024) |

| Net impaired | 0.27% (Q4 2025) |

What You See Is What You Get

Business Model Canvas

The document you're previewing is the actual Bank of Montreal Business Model Canvas you’ll receive—no mockup or sample. When you purchase, you’ll get this exact file in full, ready-to-edit formats with all sections and content intact. What you see is what you’ll own: complete, professionally structured, and immediately downloadable for presentation or analysis.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Bank of Montreal Business Model Canvas: Ready-to-Use Blueprint for Investors & Strategists

Unlock the full strategic blueprint behind Bank of Montreal’s business model—our in-depth Business Model Canvas maps customer segments, value propositions, channels, revenue streams, and cost drivers in a clear, actionable format; perfect for investors, advisors, and strategists seeking a ready-to-use Word/Excel template to benchmark, plan, and implement winning financial strategies.

Partnerships

Strategic FinTech Alliances

BMO partners with fintechs to speed digital transformation and add AI-driven insights and seamless mobile payments, lowering development costs; by 2024 BMO reported a 25% increase in digital active users to 2.3 million, reflecting these integrations.

Global Payment Networks

BMO integrates tightly with Visa and Mastercard, enabling acceptance at over 52 million merchant locations worldwide and supporting card volumes that drove C$45.8 billion in payments revenue across Canadian and U.S. retail operations in FY2024; these networks sustain card liquidity, cross-border settlement, and real-time authorization for BMO’s consumer and commercial cards.

Loyalty Program Providers

BMO partners with major loyalty platforms like AIR MILES to offer rewards that boost credit‑card spend and retention; in 2024 BMO cards generated roughly CAD 4.2B in purchase volume tied to rewards, lifting active card spend by ~7% vs non‑reward cards.

Third Party Mortgage Brokers

The bank uses a network of independent mortgage brokers across Canada and the US to widen reach and grew residential mortgage balances by about 4% year-over-year to CAD 190 billion in 2024, with brokers supplying a large share of new originations.

Strong broker relationships keep a steady pipeline of quality applications, lowering acquisition costs and supporting market-share gains in key provinces and US states.

- ~CAD 190B residential mortgages (2024)

- Brokers drive significant new originations—single-digit % growth YoY

- Lower acquisition cost, higher loan quality

Government and Regulatory Bodies

BMO works with the Bank of Canada, Federal Reserve, Office of the Superintendent of Financial Institutions (OSFI) and US regulators to follow evolving rules and support systemic stability, filing quarterly Basel III CET1 ratios (11.8% at 2025-Q3) and large-value payment controls.

These ties include policy input, anti-money-laundering reporting and transaction monitoring; sustaining regulatory approval preserves BMO’s licence and reputation after paying C$350m in compliance penalties in 2023.

- Quarterly CET1 11.8% (2025-Q3)

- C$350m compliance penalty (2023)

- Active OSFI/Bank of Canada/Fed engagement

- AML/reporting and systemic-stability focus

BMO partners fuel digital surge, C$45.8B payments & CAD190B mortgages

BMO’s key partners—fintechs, Visa/Mastercard, loyalty programs, mortgage brokers, and regulators—drive digital growth (2.3M digital users, +25% in 2024), card payments (C$45.8B payments revenue FY2024), mortgage scale (~CAD190B residential balances 2024), and compliance (CET1 11.8% 2025‑Q3; C$350m penalty 2023).

| Partner | Role | Key 2024/2025 Metric |

|---|---|---|

| Fintechs | Digital+AI | 2.3M digital users (+25% 2024) |

| Visa/Mastercard | Card rails | C$45.8B payments revenue FY2024 |

| Loyalty | Rewards | ~C$4.2B reward-linked spend 2024 |

| Brokers | Mortgage originations | ~CAD190B mortgages 2024 |

| Regulators | Compliance | CET1 11.8% (2025‑Q3); C$350m penalty 2023 |

What is included in the product

A concise, investor-ready Business Model Canvas for Bank of Montreal covering nine BMC blocks—customer segments, value propositions, channels, customer relationships, revenue streams, key resources, key activities, key partners, and cost structure—aligned with real-world operations and strategic priorities to support presentations, funding discussions, and strategic analysis.

High-level, editable Business Model Canvas for Bank of Montreal that condenses strategy into a one-page snapshot—ideal for quick executive reviews, team collaboration, and saving hours of formatting when comparing banks or preparing board-ready deliverables.

Activities

Financial Product Development

BMO continuously designs and refines products from savings accounts to complex derivatives for corporates, using market research, actuarial analysis, and competitive benchmarking; in 2024 BMO reported $52.5B in deposits and business lending growth of 6% YoY, showing product innovation drives deposit inflows and loan book expansion.

Risk Management and Credit Assessment

BMO rigorously evaluates borrower creditworthiness—retail and corporate—aiming to keep net impaired loan ratio low (0.27% at Q4 2025) and reduce defaults; credit committees and stress tests guide decisions. The bank uses machine learning and advanced analytics for market, liquidity and operational risk modelling, supporting CET1 ratio management (12.8% at FY2024) to protect shareholder capital and depositor funds.

Digital Infrastructure Maintenance

BMO spends about CAD 1.2 billion annually on technology and digital platforms (2024 disclosure), upgrading mobile apps, web portals and backend systems to sustain 24/7 uptime and process millions of transactions daily; secure infrastructure cut branch-related costs and supports customer satisfaction metrics—digital NPS rose to 34 in 2024.

Customer Relationship Management

BMO drives long-term loyalty via proactive outreach, personalized financial planning, and dedicated account teams for HNW clients, plus multi-channel responsive support; in 2024 BMO reported 10% YoY growth in wealth AUM to C$330 billion, boosting cross-sell rates and client lifetime value.

- Personalized planning for retail and commercial clients

- Dedicated HNW account management

- Multi-channel responsive support

- Wealth AUM C$330B (2024), +10% YoY

- Higher cross-sell improves lifetime value

Regulatory Compliance and Auditing

BMO commits substantial resources to regulatory compliance across its global operations, running regular internal audits and submitting reports to regulators to combat money laundering and enforce fair lending; in 2024 BMO’s compliance and conduct costs were CA$1.1bn, reflecting intensified monitoring and remediation efforts.

Breach avoidance is core: non-compliance risks costly fines and reputational loss, so BMO’s compliance teams and external auditors perform continuous reviews and controls testing to maintain license and market trust.

- CA$1.1bn compliance costs (2024)

- Ongoing AML (anti-money laundering) audits

- Regular external regulator reporting

- Focus on fair lending controls and remediation

BMO boosts AUM to C$330bn, invests CA$2.3bn in tech & compliance with strong CET1

BMO designs retail to corporate products, manages credit and liquidity (CET1 12.8% FY2024), spends CA$1.2bn on tech (2024) and CA$1.1bn on compliance (2024), grows wealth AUM to C$330bn (+10% YoY) and keeps impaired loans low (net impaired 0.27% Q4 2025), using ML risk models and multi-channel client servicing to boost cross-sell and retention.

| Metric | Value |

|---|---|

| Deposits | CA$52.5bn (2024) |

| Wealth AUM | CA$330bn (+10% YoY) |

| Tech spend | CA$1.2bn (2024) |

| Compliance cost | CA$1.1bn (2024) |

| CET1 | 12.8% (FY2024) |

| Net impaired | 0.27% (Q4 2025) |

What You See Is What You Get

Business Model Canvas

The document you're previewing is the actual Bank of Montreal Business Model Canvas you’ll receive—no mockup or sample. When you purchase, you’ll get this exact file in full, ready-to-edit formats with all sections and content intact. What you see is what you’ll own: complete, professionally structured, and immediately downloadable for presentation or analysis.