Bank of Montreal Porter's Five Forces Analysis

From Overview to Strategy Blueprint

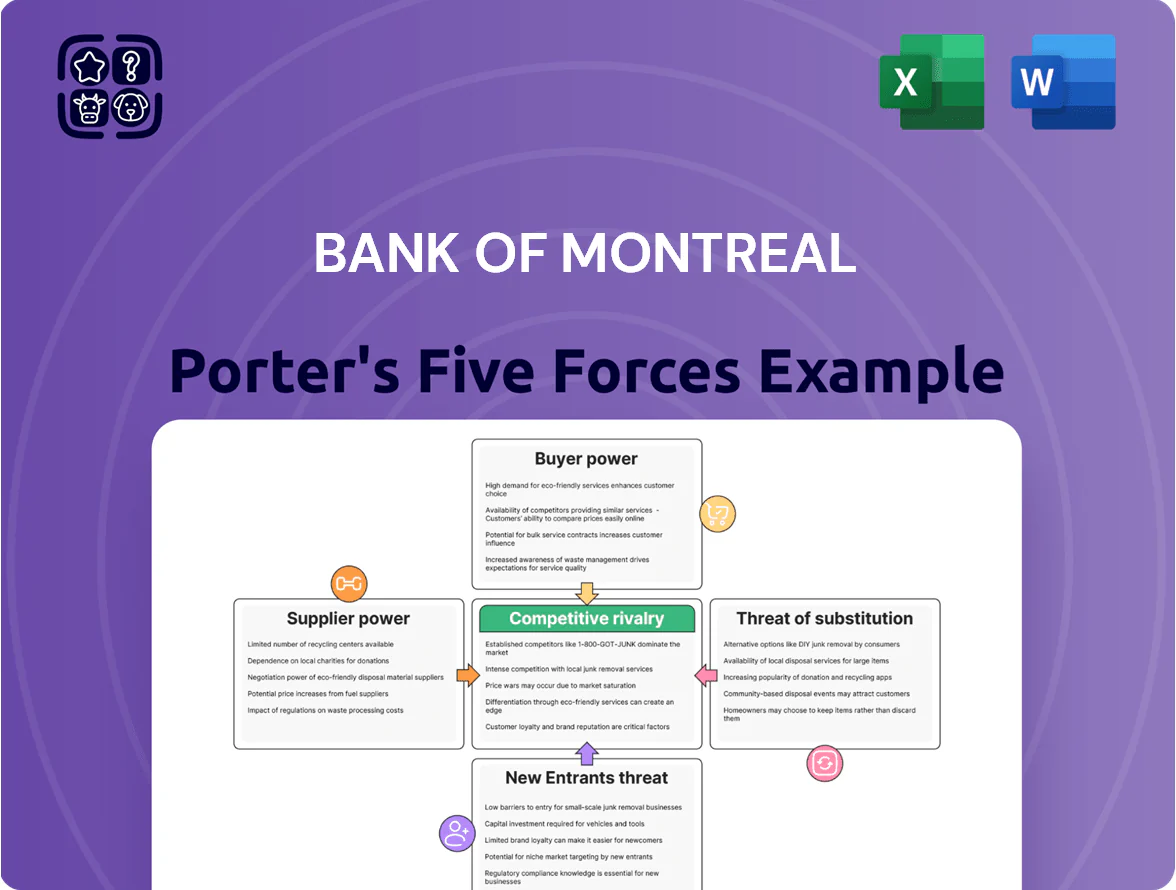

Bank of Montreal faces moderate buyer power, intense rivalry among Canadian banks, tempered supplier influence, manageable threat of new entrants due to high regulatory barriers, and rising substitute threats from fintechs and digital wallets.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Bank of Montreal’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Access to Capital and Liquidity Markets

BMO draws funding from retail deposits (CAD 482 billion in total deposits as of Q3 2025) and wholesale debt markets to fund lending, so individual depositors hold little direct power but collective shifts toward higher-yield options force the bank to raise retail rates. In the late-2025 high-rate environment Canada’s 90-day treasury at ~4.75% pushed BMO’s cost of funds up, squeezing net interest margins, which fell to 1.55% in Q3 2025. Large institutional investors and bondholders exert moderate bargaining power, able to demand higher spreads tied to BMO’s A2/A credit ratings and the bank’s market stability.

Technology and Cloud Infrastructure Providers

BMO’s aggressive digital push raises dependence on a few dominant tech suppliers—Microsoft, Amazon Web Services, and niche fintechs—giving them strong bargaining power due to high technical complexity and switching costs; legacy core migration can exceed CAD 100–300m and multi-year cloud contracts lock capacity and pricing. As AI becomes standard, these vendors gain pricing power—AWS and Microsoft reported combined 2024 cloud revenue ~USD 240bn—so cost increases or outages pose material strategic and operational risk to BMO.

Specialized Human Capital and Labor

The demand for cybersec, data science and AI experts gives suppliers strong leverage; banks pay premium salaries—BMO raised tech hiring compensation ~12–18% in 2024–25—and offers remote/flexible roles to compete with Big Tech and fintechs. A 2025 Canadian tech talent shortage pushed fintech salaries up ~15% year-over-year, increasing BMO’s tech OPEX and capital spend on retention. These roles are strategic for BMO’s multi-year digital roadmap, amplifying supplier power.

Regulatory and Government Oversight

Regulatory bodies like the Office of the Superintendent of Financial Institutions (OSFI) act as non-market suppliers of licenses and rules essential for BMO’s operations, giving them high bargaining power.

OSFI and international regulators set capital reserve requirements (OSFI’s 2024 Basel III Liquidity Buffer guidance raised CET1-like targets by ~50–100 bps for major banks) and operational standards that BMO cannot negotiate, making compliance a mandatory, non-discretionary cost.

Changes in capital adequacy ratios or consumer protection laws—such as a 25–100 bps hike in required capital or tighter conduct rules—directly reduce BMO’s ROE and force strategic shifts (asset mix, dividend policy, lending growth).

- OSFI = absolute rule-maker; licenses required

- 2024 guidance: ~50–100 bps higher capital targets for big banks

- Compliance = non-negotiable, recurring cost

- Capital or consumer-law changes cut ROE, shift strategy

Data and Information Service Providers

BMO relies on credit rating agencies, Bloomberg, Reuters and credit bureaus for pricing, risk models and trade execution; these data suppliers are concentrated—Bloomberg had ~20% market share of terminal subscriptions in 2024—letting them charge high fees for real-time feeds and analytics. Without live access, BMO’s trade execution and risk-pricing accuracy would drop materially, raising funding and counterparty risk. The small pool of alternatives keeps supplier bargaining power elevated.

- Bloomberg ~20% terminal share (2024)

- High fees for real-time feeds raise operating cost

- Limited alternatives increase supplier leverage

- Loss of real-time data hurts pricing, execution, risk

Rising supplier power lifts BMO costs: deposits, cloud, talent, ratings, and OSFI

Suppliers exert moderate-to-high power: depositors drive retail funding costs (CAD 482b deposits, rising retail rates in 2025), wholesale bondholders pressure spreads via credit ratings (BMO A2/A), big cloud vendors (Microsoft, AWS) and data providers (Bloomberg ~20% terminal share) charge premium fees and create switching costs, cyber/AI talent shortages raised tech pay ~12–18% in 2024–25, and OSFI’s 2024 guidance lifted capital targets ~50–100 bps, all raising BMO’s operating and compliance costs.

| Supplier | Key metric | 2024–25 |

|---|---|---|

| Retail deposits | Total | CAD 482b |

| Net interest margin | Q3 2025 | 1.55% |

| Cloud vendors | Combined 2024 rev (AWS+MS) | ~USD 240bn |

| Tech pay pressure | Comp rise | 12–18% |

| OSFI capital guidance | Raised targets | ~50–100 bps |

| Bloomberg | Terminal share | ~20% |

What is included in the product

Tailored Porter's Five Forces analysis for Bank of Montreal that uncovers competitive drivers, buyer/supplier power, entry barriers, substitutes, and emerging threats to its market position, with strategic commentary for investors and managers.

Clear one-sheet Porter's Five Forces for Bank of Montreal—ideal for quick strategic decisions and boardroom briefings.

Customers Bargaining Power

Retail Banking Consumer Choice

Individual consumers in North America face over 5,000 banking alternatives including fintechs and credit unions, boosting their bargaining power over fees and service quality.

Digital-only banks and comparison tools let customers quickly find higher deposit rates (often 0.5–1.5 percentage points higher) or lower fees, increasing switching likelihood.

BMO must keep innovating mobile features and loyalty perks—retail deposit churn rose toward 8% in 2024—to avoid losing customers.

By 2025 product transparency is at an all-time high, making retention the primary strategic challenge.

Corporate and Institutional Client Leverage

Large corporate clients drive a big slice of BMO’s fee income—BMO Capital Markets earned C$2.7bn in 2024 revenue, and top 10 institutional mandates can represent several percentage points of that, so clients can demand tailored deals and lower spreads.

These firms invite bids from global banks, which boosts bargaining power; BMO must show superior execution, tech, and relationship teams to win mandates and avoid quarter-to-quarter revenue swings if a major client leaves.

Wealth Management Client Sophistication

Wealthy clients demand personalized, low-cost strategies and clear fees; in 2025, 68% of HNW clients say fee transparency affects loyalty (Capgemini, 2025), so they can shift $millions to boutiques or robo-advisors if BMO underdelivers on alpha or service.

Self-directed and digital platforms raised price sensitivity: global digital-advice AUM reached $1.2 trillion in 2025, increasing client churn risk for incumbents.

BMO counters with hybrid advisory models—human planners plus AI-driven portfolio tools—aiming to retain HNW flows by demonstrating net-of-fee outperformance and tailored service.

Low Switching Costs in Digital Services

The 2025 rollout of open banking APIs has cut friction in moving accounts; third-party aggregators now link 70% of Canadian digital users, lowering BMO’s exit barriers as customers shift balances with a few clicks.

That means BMO must compete on UX and integrated financial-wellness tools—apps, analytics, and rewards—to retain clients; low switching costs raise customer leverage to demand better fees and features.

- Open banking adoption ~70% digital users (2025)

- Lowered exit barrier → higher churn risk

- Must compete on UX, tools, fees

SME Sensitivity to Credit Terms

SMEs are crucial to BMO’s commercial book but highly sensitive to credit availability and rate swings; a Bank of Canada rate hike cycle in 2022–2024 pushed SME loan delinquencies up modestly, and 2024 SME lending grew only 2.1% year-over-year, showing price elasticity.

When bank terms tighten, SMEs often shift to private credit or government-backed programs—Canada’s Business Credit Availability Program disbursed billions in 2020–2021 and private credit AUM in Canada rose ~35% 2019–2023—so BMO must balance risk controls with competitive pricing.

The SME segment’s collective bargaining power shapes BMO product design and pricing: keeping market share requires targeted term flexibility, quicker decisioning, and segmented risk-based pricing to avoid migration to nonbank lenders.

- SME lending growth: +2.1% YoY (2024)

- Private credit AUM Canada: +35% (2019–2023)

- BMO focus: faster decisions, segmented pricing

Customers Drive Down Fees and Switch Rates Rise as Open Banking and Robo-AUM Surge

Customers hold high bargaining power: retail churn ~8% (2024), open-banking link rates ~70% (2025), digital-advice AUM $1.2T (2025), and deposit rate gaps 0.5–1.5pp versus challengers; corporates (BMO Capital Markets rev C$2.7bn, 2024) and HNW clients (68% cite fee transparency, Capgemini 2025) push for lower fees and tailored deals.

| Metric | Value |

|---|---|

| Retail churn (2024) | ~8% |

| Open-banking links (2025) | ~70% |

| Digital-advice AUM (2025) | $1.2T |

| BMO Capital Markets rev (2024) | C$2.7bn |

| HNW fee transparency (2025) | 68% |

Preview Before You Purchase

Bank of Montreal Porter's Five Forces Analysis

This preview shows the exact Bank of Montreal Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders and no edits needed.

The file displayed is the fully formatted, final deliverable; once you buy, you’ll get instant access to this identical document for download and use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

Bank of Montreal faces moderate buyer power, intense rivalry among Canadian banks, tempered supplier influence, manageable threat of new entrants due to high regulatory barriers, and rising substitute threats from fintechs and digital wallets.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Bank of Montreal’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Access to Capital and Liquidity Markets

BMO draws funding from retail deposits (CAD 482 billion in total deposits as of Q3 2025) and wholesale debt markets to fund lending, so individual depositors hold little direct power but collective shifts toward higher-yield options force the bank to raise retail rates. In the late-2025 high-rate environment Canada’s 90-day treasury at ~4.75% pushed BMO’s cost of funds up, squeezing net interest margins, which fell to 1.55% in Q3 2025. Large institutional investors and bondholders exert moderate bargaining power, able to demand higher spreads tied to BMO’s A2/A credit ratings and the bank’s market stability.

Technology and Cloud Infrastructure Providers

BMO’s aggressive digital push raises dependence on a few dominant tech suppliers—Microsoft, Amazon Web Services, and niche fintechs—giving them strong bargaining power due to high technical complexity and switching costs; legacy core migration can exceed CAD 100–300m and multi-year cloud contracts lock capacity and pricing. As AI becomes standard, these vendors gain pricing power—AWS and Microsoft reported combined 2024 cloud revenue ~USD 240bn—so cost increases or outages pose material strategic and operational risk to BMO.

Specialized Human Capital and Labor

The demand for cybersec, data science and AI experts gives suppliers strong leverage; banks pay premium salaries—BMO raised tech hiring compensation ~12–18% in 2024–25—and offers remote/flexible roles to compete with Big Tech and fintechs. A 2025 Canadian tech talent shortage pushed fintech salaries up ~15% year-over-year, increasing BMO’s tech OPEX and capital spend on retention. These roles are strategic for BMO’s multi-year digital roadmap, amplifying supplier power.

Regulatory and Government Oversight

Regulatory bodies like the Office of the Superintendent of Financial Institutions (OSFI) act as non-market suppliers of licenses and rules essential for BMO’s operations, giving them high bargaining power.

OSFI and international regulators set capital reserve requirements (OSFI’s 2024 Basel III Liquidity Buffer guidance raised CET1-like targets by ~50–100 bps for major banks) and operational standards that BMO cannot negotiate, making compliance a mandatory, non-discretionary cost.

Changes in capital adequacy ratios or consumer protection laws—such as a 25–100 bps hike in required capital or tighter conduct rules—directly reduce BMO’s ROE and force strategic shifts (asset mix, dividend policy, lending growth).

- OSFI = absolute rule-maker; licenses required

- 2024 guidance: ~50–100 bps higher capital targets for big banks

- Compliance = non-negotiable, recurring cost

- Capital or consumer-law changes cut ROE, shift strategy

Data and Information Service Providers

BMO relies on credit rating agencies, Bloomberg, Reuters and credit bureaus for pricing, risk models and trade execution; these data suppliers are concentrated—Bloomberg had ~20% market share of terminal subscriptions in 2024—letting them charge high fees for real-time feeds and analytics. Without live access, BMO’s trade execution and risk-pricing accuracy would drop materially, raising funding and counterparty risk. The small pool of alternatives keeps supplier bargaining power elevated.

- Bloomberg ~20% terminal share (2024)

- High fees for real-time feeds raise operating cost

- Limited alternatives increase supplier leverage

- Loss of real-time data hurts pricing, execution, risk

Rising supplier power lifts BMO costs: deposits, cloud, talent, ratings, and OSFI

Suppliers exert moderate-to-high power: depositors drive retail funding costs (CAD 482b deposits, rising retail rates in 2025), wholesale bondholders pressure spreads via credit ratings (BMO A2/A), big cloud vendors (Microsoft, AWS) and data providers (Bloomberg ~20% terminal share) charge premium fees and create switching costs, cyber/AI talent shortages raised tech pay ~12–18% in 2024–25, and OSFI’s 2024 guidance lifted capital targets ~50–100 bps, all raising BMO’s operating and compliance costs.

| Supplier | Key metric | 2024–25 |

|---|---|---|

| Retail deposits | Total | CAD 482b |

| Net interest margin | Q3 2025 | 1.55% |

| Cloud vendors | Combined 2024 rev (AWS+MS) | ~USD 240bn |

| Tech pay pressure | Comp rise | 12–18% |

| OSFI capital guidance | Raised targets | ~50–100 bps |

| Bloomberg | Terminal share | ~20% |

What is included in the product

Tailored Porter's Five Forces analysis for Bank of Montreal that uncovers competitive drivers, buyer/supplier power, entry barriers, substitutes, and emerging threats to its market position, with strategic commentary for investors and managers.

Clear one-sheet Porter's Five Forces for Bank of Montreal—ideal for quick strategic decisions and boardroom briefings.

Customers Bargaining Power

Retail Banking Consumer Choice

Individual consumers in North America face over 5,000 banking alternatives including fintechs and credit unions, boosting their bargaining power over fees and service quality.

Digital-only banks and comparison tools let customers quickly find higher deposit rates (often 0.5–1.5 percentage points higher) or lower fees, increasing switching likelihood.

BMO must keep innovating mobile features and loyalty perks—retail deposit churn rose toward 8% in 2024—to avoid losing customers.

By 2025 product transparency is at an all-time high, making retention the primary strategic challenge.

Corporate and Institutional Client Leverage

Large corporate clients drive a big slice of BMO’s fee income—BMO Capital Markets earned C$2.7bn in 2024 revenue, and top 10 institutional mandates can represent several percentage points of that, so clients can demand tailored deals and lower spreads.

These firms invite bids from global banks, which boosts bargaining power; BMO must show superior execution, tech, and relationship teams to win mandates and avoid quarter-to-quarter revenue swings if a major client leaves.

Wealth Management Client Sophistication

Wealthy clients demand personalized, low-cost strategies and clear fees; in 2025, 68% of HNW clients say fee transparency affects loyalty (Capgemini, 2025), so they can shift $millions to boutiques or robo-advisors if BMO underdelivers on alpha or service.

Self-directed and digital platforms raised price sensitivity: global digital-advice AUM reached $1.2 trillion in 2025, increasing client churn risk for incumbents.

BMO counters with hybrid advisory models—human planners plus AI-driven portfolio tools—aiming to retain HNW flows by demonstrating net-of-fee outperformance and tailored service.

Low Switching Costs in Digital Services

The 2025 rollout of open banking APIs has cut friction in moving accounts; third-party aggregators now link 70% of Canadian digital users, lowering BMO’s exit barriers as customers shift balances with a few clicks.

That means BMO must compete on UX and integrated financial-wellness tools—apps, analytics, and rewards—to retain clients; low switching costs raise customer leverage to demand better fees and features.

- Open banking adoption ~70% digital users (2025)

- Lowered exit barrier → higher churn risk

- Must compete on UX, tools, fees

SME Sensitivity to Credit Terms

SMEs are crucial to BMO’s commercial book but highly sensitive to credit availability and rate swings; a Bank of Canada rate hike cycle in 2022–2024 pushed SME loan delinquencies up modestly, and 2024 SME lending grew only 2.1% year-over-year, showing price elasticity.

When bank terms tighten, SMEs often shift to private credit or government-backed programs—Canada’s Business Credit Availability Program disbursed billions in 2020–2021 and private credit AUM in Canada rose ~35% 2019–2023—so BMO must balance risk controls with competitive pricing.

The SME segment’s collective bargaining power shapes BMO product design and pricing: keeping market share requires targeted term flexibility, quicker decisioning, and segmented risk-based pricing to avoid migration to nonbank lenders.

- SME lending growth: +2.1% YoY (2024)

- Private credit AUM Canada: +35% (2019–2023)

- BMO focus: faster decisions, segmented pricing

Customers Drive Down Fees and Switch Rates Rise as Open Banking and Robo-AUM Surge

Customers hold high bargaining power: retail churn ~8% (2024), open-banking link rates ~70% (2025), digital-advice AUM $1.2T (2025), and deposit rate gaps 0.5–1.5pp versus challengers; corporates (BMO Capital Markets rev C$2.7bn, 2024) and HNW clients (68% cite fee transparency, Capgemini 2025) push for lower fees and tailored deals.

| Metric | Value |

|---|---|

| Retail churn (2024) | ~8% |

| Open-banking links (2025) | ~70% |

| Digital-advice AUM (2025) | $1.2T |

| BMO Capital Markets rev (2024) | C$2.7bn |

| HNW fee transparency (2025) | 68% |

Preview Before You Purchase

Bank of Montreal Porter's Five Forces Analysis

This preview shows the exact Bank of Montreal Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders and no edits needed.

The file displayed is the fully formatted, final deliverable; once you buy, you’ll get instant access to this identical document for download and use.