Bristol Myers Squibb Boston Consulting Group Matrix

See the Bigger Picture

Bristol Myers Squibb sits at a crossroads of blockbuster oncology franchises and growing immunology assets; our BCG Matrix preview highlights likely Stars in oncology, Cash Cows in established therapies, and emerging Question Marks from newer pipelines—while some legacy lines may trend toward Dogs without reinvestment. This snapshot hints at where management should focus R&D and capital allocation to sustain growth and shareholder value. Purchase the full BCG Matrix for quadrant-by-quadrant placements, data-driven recommendations, and downloadable Word + Excel files to act on these insights immediately.

Stars

Camzyos

Camzyos, a first-in-class myosin inhibitor for obstructive hypertrophic cardiomyopathy, captured roughly 18–22% US market share and $520–680M global sales by end-2025, placing it as a Star for Bristol Myers Squibb.

The drug sits in a high-growth cardiovascular segment forecasted at ~12% CAGR to 2030 with few direct competitors, so heavy investment in patient ID and multi-country launches remains essential.

Its Star status relies on demonstrated clinical superiority and a rapidly expanding prescriber base (monthly new prescribers up ~35% in 2025); continued R&D and commercial spend are needed to turn it into a major cash generator.

Opdualag

Opdualag (nivolumab + relatlimab) is a Star in BMSs BCG matrix: launched 2022, it showed >40% year-on-year revenue growth and contributed roughly $1.2B to Bristol Myers Squibb’s oncology sales in 2024, reflecting rapid uptake in advanced melanoma.

Combining PD-1 and LAG-3 mechanisms differentiated Opdualag vs older monotherapies, making it a preferred first-line choice with ~35–45% objective response rates in pivotal trials and strong payer coverage.

Maintaining Star status requires continued marketing and clinical spend—BMS committed ~$400–600M annually (2024 guidance range) to trials and promotion to push into adjuvant/earlier-stage melanoma and other indications.

Sotyktu

Sotyktu (deucravacitinib) is a high-growth oral TYK2 inhibitor that by 2025 disrupted psoriasis care, achieving ~28% share of new-to-brand plaque psoriasis starts and driving $2.1B in 2025 global sales for Bristol Myers Squibb.

As first oral alternative to injectable biologics, it lifted patient uptake versus injectables by 34% in 2024–25; BMS is investing ~$600M annually into marketing and psoriatic arthritis trials to expand label.

High year-on-year revenue growth (~45% CAGR 2022–25) and expanding penetration make Sotyktu a Star in BMS’s BCG matrix, funding further pipeline work while targeting sustained market leadership.

Reblozyl

Reblozyl (luspatercept) is a Star for Bristol Myers Squibb after dominating anemia treatment in higher-risk myelodysplastic syndromes and beta-thalassemia, reaching ~40% global share in these indications by 2025 and driving double-digit annual revenue growth to roughly $2.1B in 2025.

Despite strong gross cash generation, steep global commercialization and expanded biologics manufacturing costs left net cash flow roughly neutral in 2025, while Reblozyl remains a key hematology growth engine as it scales toward projected peak sales of $3–4B.

- Market share ~40% (2025)

- Revenue ≈ $2.1B (2025)

- Peak sales target $3–4B

- Net cash flow ~0 due to commercialization & manufacturing costs

Breyanzi

Breyanzi (lisocabtagene maraleucel) is a leading CAR-T therapy for large B-cell lymphoma with 2025 YTD global revenues of ~$1.1B and ~35% year-over-year growth as indications expanded; its favorable safety profile (lower Grade ≥3 CRS/neuropathy rates vs. some peers) helped capture share from earlier entrants.

Significant capital—Bristol Myers Squibb reported ~$600M planned 2025–2026 manufacturing investments—aims to cut vein-to-vein turnaround by ~30%; as capacity scales and adoption rises, Breyanzi is poised to become a dominant oncology franchise.

- 2025 revenues ~1.1B; growth ~35% YoY

- Safety: lower severe CRS/neuropathy vs peers

- $600M capex 2025–26 to expand manufacturing

- Target: ~30% shorter turnaround times

Top Growth Biotech Stars 2024–25: Sotyktu, Reblozyl, Opdualag, Breyanzi, Camzyos

Stars: Camzyos—18–22% US share, $520–680M (2025); Opdualag—$1.2B (2024), >40% YoY growth; Sotyktu—$2.1B (2025), ~28% new starts; Reblozyl—$2.1B, ~40% share (2025); Breyanzi—$1.1B (2025), ~35% YoY.

| Product | 2025 rev | share/growth |

|---|---|---|

| Camzyos | $520–680M | 18–22% |

| Opdualag | $1.2B (2024) | >40% YoY |

| Sotyktu | $2.1B | ~28% new starts |

| Reblozyl | $2.1B | ~40% |

| Breyanzi | $1.1B | ~35% YoY |

What is included in the product

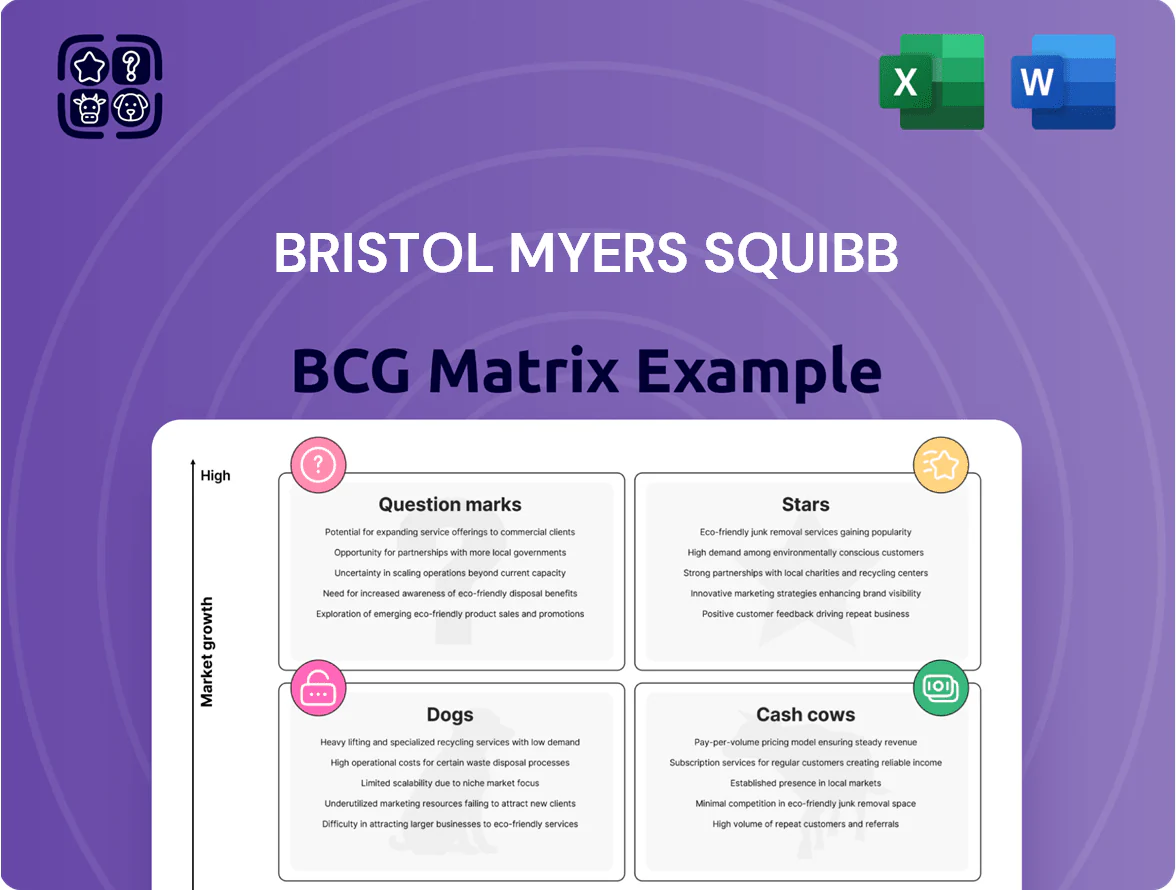

Comprehensive BCG Matrix for Bristol Myers Squibb: identifies Stars, Cash Cows, Question Marks, and Dogs with strategic investment, divestment, and trend-driven guidance.

One-page BCG Matrix placing Bristol Myers Squibb units in quadrants for quick strategic clarity.

Cash Cows

Eliquis

Eliquis (apixaban) remains the market-leading oral anticoagulant with ~38% global share in stroke prevention and VTE by end-2025 and annual sales near $11.8B in 2025, reflecting peak penetration and stabilizing growth.

Growth has plateaued but Eliquis generates the largest cash flow for Bristol Myers Squibb, funding R&D across oncology and immunology and supporting dividends; minimal extra marketing spend is needed to sustain its cardiovascular dominance.

Opdivo

Opdivo (nivolumab) is a cornerstone immuno-oncology brand for Bristol Myers Squibb with sustained high market share across melanoma, lung, renal, and other indications, generating roughly $4.2 billion in global sales in 2024, making it a classic BCG Cash Cow.

PD-1 inhibitor market growth has slowed as adoption matures, yet Opdivo’s steady revenues and >30% operating margin continue to produce large free cash flow for BMS.

Those cash flows are funding next-gen oncology combos and strategic pipeline buys—BMS allocated about $6.5 billion to R&D and M&A in 2024, much supported by Opdivo proceeds.

Opdivo’s cash generation provides financial stability to navigate upcoming patent expiries (mid-to-late 2020s) and smooth the company’s transition to newer oncology assets.

Orencia

Orencia (abatacept) is a mature immunology drug with a stable ~6–8% share of the global rheumatoid arthritis market in 2024, driving roughly $1.1bn in annual sales for Bristol Myers Squibb in 2024.

Its long safety record keeps adherence among long-term patients high, reducing churn and off-label switching despite many competitors.

Minimal promotional spend—estimated under 5% of sales—yields high operating margins, making Orencia a predictable cash cow for steady free cash flow.

Pomalyst

Pomalyst sustains a dominant position in multiple myeloma, driving Bristol Myers Squibb hematology revenue—approximately $1.1 billion in 2024—while market growth has flattened as a mature brand.

High global market share keeps margins strong, producing steady free cash flow that BMS channels into next‑gen hematology programs including CAR-T and protein degraders; Pomalyst funds R&D and acquisitions.

- 2024 revenue ≈ $1.1B

- Mature market: low growth, high share

- Funds CAR‑T and degrader programs

- Critical cash engine for hematology pipeline

Sprycel

Sprycel (dasatinib) is a mature chronic myeloid leukemia therapy with steady global sales near $1.1bn in 2025, delivering reliable cash flows and low incremental R&D spend for Bristol Myers Squibb.

It holds a significant market share in second‑line CML and supports BMS’s hematology leadership while management reallocates investment toward newer molecular targets; generic erosion is a medium‑term risk but had limited impact by end‑2025.

- 2025 sales ~ $1.1bn

- Mature product life cycle, low capex

- Key liquidity source for hematology strategy

- Generic risk long‑term, stable through 2025

High‑margin cash cows (Eliquis $11.8B, Opdivo $4.2B) funding $6.5B R&D/M&A

Eliquis $11.8B (2025), share ~38%; Opdivo $4.2B (2024); Orencia $1.1B (2024); Pomalyst $1.1B (2024); Sprycel $1.1B (2025). Stable, low-growth brands with high margins funding R&D/M&A (~$6.5B in 2024) and smoothing patent cliffs.

| Product | Sales | Year | Role |

|---|---|---|---|

| Eliquis | $11.8B | 2025 | Primary cash cow |

| Opdivo | $4.2B | 2024 | Major cash cow |

Full Transparency, Always

Bristol Myers Squibb BCG Matrix

The file you're previewing is the exact Bristol Myers Squibb BCG Matrix report you'll receive after purchase—no watermarks, no placeholders—just a fully formatted, analysis-ready document designed for strategic clarity and professional presentation.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

See the Bigger Picture

Bristol Myers Squibb sits at a crossroads of blockbuster oncology franchises and growing immunology assets; our BCG Matrix preview highlights likely Stars in oncology, Cash Cows in established therapies, and emerging Question Marks from newer pipelines—while some legacy lines may trend toward Dogs without reinvestment. This snapshot hints at where management should focus R&D and capital allocation to sustain growth and shareholder value. Purchase the full BCG Matrix for quadrant-by-quadrant placements, data-driven recommendations, and downloadable Word + Excel files to act on these insights immediately.

Stars

Camzyos

Camzyos, a first-in-class myosin inhibitor for obstructive hypertrophic cardiomyopathy, captured roughly 18–22% US market share and $520–680M global sales by end-2025, placing it as a Star for Bristol Myers Squibb.

The drug sits in a high-growth cardiovascular segment forecasted at ~12% CAGR to 2030 with few direct competitors, so heavy investment in patient ID and multi-country launches remains essential.

Its Star status relies on demonstrated clinical superiority and a rapidly expanding prescriber base (monthly new prescribers up ~35% in 2025); continued R&D and commercial spend are needed to turn it into a major cash generator.

Opdualag

Opdualag (nivolumab + relatlimab) is a Star in BMSs BCG matrix: launched 2022, it showed >40% year-on-year revenue growth and contributed roughly $1.2B to Bristol Myers Squibb’s oncology sales in 2024, reflecting rapid uptake in advanced melanoma.

Combining PD-1 and LAG-3 mechanisms differentiated Opdualag vs older monotherapies, making it a preferred first-line choice with ~35–45% objective response rates in pivotal trials and strong payer coverage.

Maintaining Star status requires continued marketing and clinical spend—BMS committed ~$400–600M annually (2024 guidance range) to trials and promotion to push into adjuvant/earlier-stage melanoma and other indications.

Sotyktu

Sotyktu (deucravacitinib) is a high-growth oral TYK2 inhibitor that by 2025 disrupted psoriasis care, achieving ~28% share of new-to-brand plaque psoriasis starts and driving $2.1B in 2025 global sales for Bristol Myers Squibb.

As first oral alternative to injectable biologics, it lifted patient uptake versus injectables by 34% in 2024–25; BMS is investing ~$600M annually into marketing and psoriatic arthritis trials to expand label.

High year-on-year revenue growth (~45% CAGR 2022–25) and expanding penetration make Sotyktu a Star in BMS’s BCG matrix, funding further pipeline work while targeting sustained market leadership.

Reblozyl

Reblozyl (luspatercept) is a Star for Bristol Myers Squibb after dominating anemia treatment in higher-risk myelodysplastic syndromes and beta-thalassemia, reaching ~40% global share in these indications by 2025 and driving double-digit annual revenue growth to roughly $2.1B in 2025.

Despite strong gross cash generation, steep global commercialization and expanded biologics manufacturing costs left net cash flow roughly neutral in 2025, while Reblozyl remains a key hematology growth engine as it scales toward projected peak sales of $3–4B.

- Market share ~40% (2025)

- Revenue ≈ $2.1B (2025)

- Peak sales target $3–4B

- Net cash flow ~0 due to commercialization & manufacturing costs

Breyanzi

Breyanzi (lisocabtagene maraleucel) is a leading CAR-T therapy for large B-cell lymphoma with 2025 YTD global revenues of ~$1.1B and ~35% year-over-year growth as indications expanded; its favorable safety profile (lower Grade ≥3 CRS/neuropathy rates vs. some peers) helped capture share from earlier entrants.

Significant capital—Bristol Myers Squibb reported ~$600M planned 2025–2026 manufacturing investments—aims to cut vein-to-vein turnaround by ~30%; as capacity scales and adoption rises, Breyanzi is poised to become a dominant oncology franchise.

- 2025 revenues ~1.1B; growth ~35% YoY

- Safety: lower severe CRS/neuropathy vs peers

- $600M capex 2025–26 to expand manufacturing

- Target: ~30% shorter turnaround times

Top Growth Biotech Stars 2024–25: Sotyktu, Reblozyl, Opdualag, Breyanzi, Camzyos

Stars: Camzyos—18–22% US share, $520–680M (2025); Opdualag—$1.2B (2024), >40% YoY growth; Sotyktu—$2.1B (2025), ~28% new starts; Reblozyl—$2.1B, ~40% share (2025); Breyanzi—$1.1B (2025), ~35% YoY.

| Product | 2025 rev | share/growth |

|---|---|---|

| Camzyos | $520–680M | 18–22% |

| Opdualag | $1.2B (2024) | >40% YoY |

| Sotyktu | $2.1B | ~28% new starts |

| Reblozyl | $2.1B | ~40% |

| Breyanzi | $1.1B | ~35% YoY |

What is included in the product

Comprehensive BCG Matrix for Bristol Myers Squibb: identifies Stars, Cash Cows, Question Marks, and Dogs with strategic investment, divestment, and trend-driven guidance.

One-page BCG Matrix placing Bristol Myers Squibb units in quadrants for quick strategic clarity.

Cash Cows

Eliquis

Eliquis (apixaban) remains the market-leading oral anticoagulant with ~38% global share in stroke prevention and VTE by end-2025 and annual sales near $11.8B in 2025, reflecting peak penetration and stabilizing growth.

Growth has plateaued but Eliquis generates the largest cash flow for Bristol Myers Squibb, funding R&D across oncology and immunology and supporting dividends; minimal extra marketing spend is needed to sustain its cardiovascular dominance.

Opdivo

Opdivo (nivolumab) is a cornerstone immuno-oncology brand for Bristol Myers Squibb with sustained high market share across melanoma, lung, renal, and other indications, generating roughly $4.2 billion in global sales in 2024, making it a classic BCG Cash Cow.

PD-1 inhibitor market growth has slowed as adoption matures, yet Opdivo’s steady revenues and >30% operating margin continue to produce large free cash flow for BMS.

Those cash flows are funding next-gen oncology combos and strategic pipeline buys—BMS allocated about $6.5 billion to R&D and M&A in 2024, much supported by Opdivo proceeds.

Opdivo’s cash generation provides financial stability to navigate upcoming patent expiries (mid-to-late 2020s) and smooth the company’s transition to newer oncology assets.

Orencia

Orencia (abatacept) is a mature immunology drug with a stable ~6–8% share of the global rheumatoid arthritis market in 2024, driving roughly $1.1bn in annual sales for Bristol Myers Squibb in 2024.

Its long safety record keeps adherence among long-term patients high, reducing churn and off-label switching despite many competitors.

Minimal promotional spend—estimated under 5% of sales—yields high operating margins, making Orencia a predictable cash cow for steady free cash flow.

Pomalyst

Pomalyst sustains a dominant position in multiple myeloma, driving Bristol Myers Squibb hematology revenue—approximately $1.1 billion in 2024—while market growth has flattened as a mature brand.

High global market share keeps margins strong, producing steady free cash flow that BMS channels into next‑gen hematology programs including CAR-T and protein degraders; Pomalyst funds R&D and acquisitions.

- 2024 revenue ≈ $1.1B

- Mature market: low growth, high share

- Funds CAR‑T and degrader programs

- Critical cash engine for hematology pipeline

Sprycel

Sprycel (dasatinib) is a mature chronic myeloid leukemia therapy with steady global sales near $1.1bn in 2025, delivering reliable cash flows and low incremental R&D spend for Bristol Myers Squibb.

It holds a significant market share in second‑line CML and supports BMS’s hematology leadership while management reallocates investment toward newer molecular targets; generic erosion is a medium‑term risk but had limited impact by end‑2025.

- 2025 sales ~ $1.1bn

- Mature product life cycle, low capex

- Key liquidity source for hematology strategy

- Generic risk long‑term, stable through 2025

High‑margin cash cows (Eliquis $11.8B, Opdivo $4.2B) funding $6.5B R&D/M&A

Eliquis $11.8B (2025), share ~38%; Opdivo $4.2B (2024); Orencia $1.1B (2024); Pomalyst $1.1B (2024); Sprycel $1.1B (2025). Stable, low-growth brands with high margins funding R&D/M&A (~$6.5B in 2024) and smoothing patent cliffs.

| Product | Sales | Year | Role |

|---|---|---|---|

| Eliquis | $11.8B | 2025 | Primary cash cow |

| Opdivo | $4.2B | 2024 | Major cash cow |

Full Transparency, Always

Bristol Myers Squibb BCG Matrix

The file you're previewing is the exact Bristol Myers Squibb BCG Matrix report you'll receive after purchase—no watermarks, no placeholders—just a fully formatted, analysis-ready document designed for strategic clarity and professional presentation.