Bayerische Motoren Werke Porter's Five Forces Analysis

Don't Miss the Bigger Picture

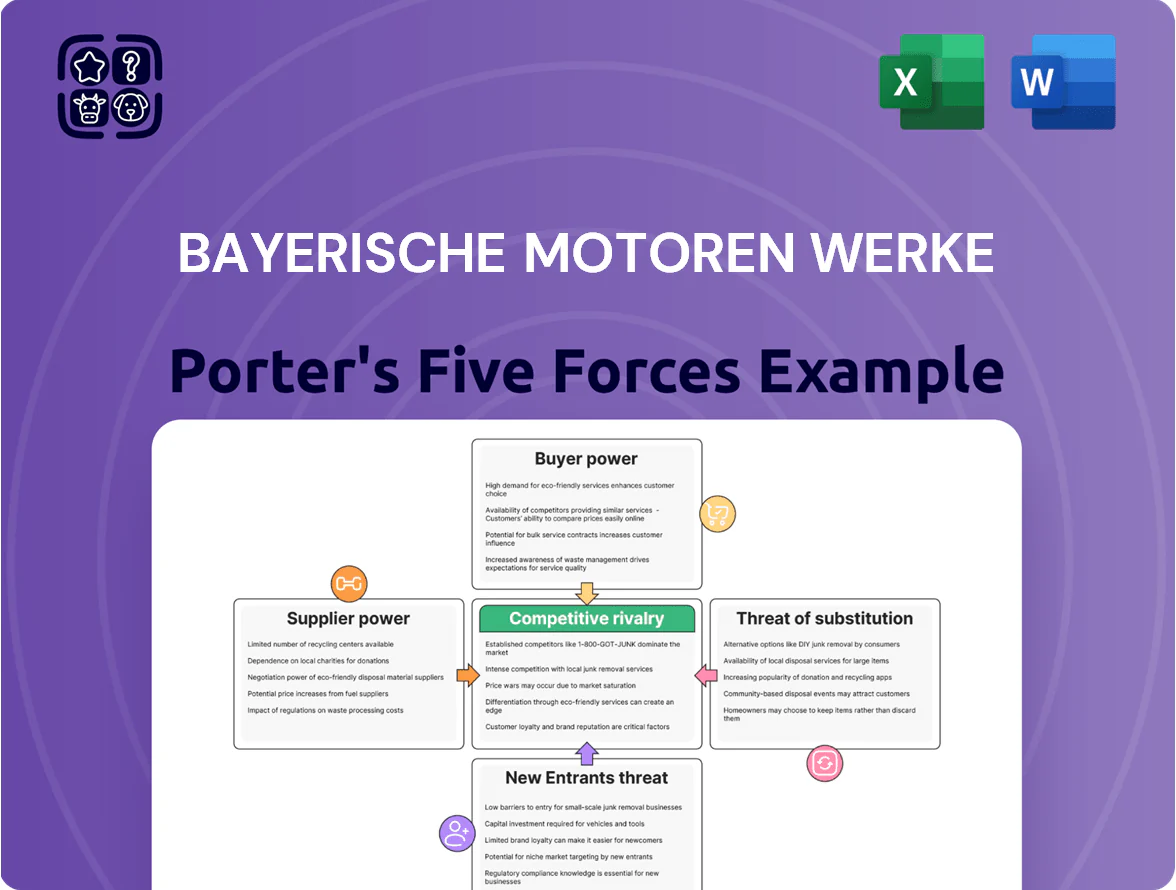

Bayerische Motoren Werke faces intense rivalry from premium rivals, moderate supplier power due to specialized components, rising buyer expectations for EVs and tech, growing substitute threats from mobility services, and high barriers deterring new entrants but enabling incumbents to defend margins.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Bayerische Motoren Werke’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of EV Battery Manufacturers

By end-2025, battery cell market is concentrated: CATL held ~34% global market share and Northvolt scaled to ~6% capacity, giving few firms outsized leverage over BMW’s Neue Klasse sourcing.

Batteries are ~30–40% of EV BOM (bill of materials), so BMW’s production hinges on securing cells; shortages would directly raise costs and delay deliveries.

BMW is diversifying via long-term offtakes and equity stakes (e.g., 2024 €Xbn deals), but high R&D, gigafactory scale, and cell chemistry expertise keep partner pool small.

Semiconductor and Software Integration

As BMW shifts to software-defined vehicles, high-end chipmakers (TSMC, Intel, Infineon) and software suppliers (Nvidia, Continental) hold strong leverage: specialized silicon and middleware are hard to swap without rearchitecting ECUs, raising switching costs. Global advanced logic wafer shortages kept fab utilization >90% in 2024 and led to foundry ASP rises ~15% YoY, so suppliers sustain firm pricing and delivery terms, pressuring BMWs margin and time-to-market.

Raw Material Scarcity and Sustainability

Suppliers of lithium, cobalt and rare earths gained leverage as EV demand rose; lithium prices jumped ~120% in 2021–2023 and cobalt averaged $38,000/ton in 2024, raising BMW’s input costs.

BMW needs multi-year contracts and equity stakes in mines; in 2024 BMW committed to securing sources for cells, targeting 50 GWh of battery capacity by 2030 to lock supply.

Compliance with ESG (environmental, social, governance) audits adds cost and limits supplier pool, giving a few mining firms pricing power and creating a production bottleneck.

Specialized Premium Components

BMW relies on specialized suppliers for leather, Alcantara, carbon fiber and precision driveline parts; in 2024 BMW Group spent €55.4 billion on materials and third-party services, much of which supports premium components.

These suppliers co-develop parts with BMW, creating mutual dependence but giving suppliers pricing and delivery leverage due to unique craftsmanship and certifications; switching suppliers risks 6–18 months of validation and potential warranty/quality costs.

- €55.4bn materials/third-party spend (2024)

- 6–18 months supplier requalification time

- High supplier leverage from certified craftsmanship

High Switching Costs for Tooling

High switching costs for tooling give suppliers strong leverage over Bayerische Motoren Werke (BMW); dedicated presses, dies, and stamping tools often cost €1–5 million per part and require months of revalidation. Suppliers can demand higher margins during a model lifecycle because mid-cycle replacement triggers new homologation, testing, and line reconfiguration that can exceed 10% of program cost. In 2024, automotive OEMs reported average supplier changeover lead times of 6–12 months, raising practical lock-in. This technical lock-in raises supplier bargaining power through price and delivery terms.

- Tool cost per part: €1–5M

- Changeover lead time: 6–12 months (2024)

- Revalidation/line costs: often >10% of program

Supplier Power Dominates EV Value Chain: Batteries, Chips, and Long-Term Offtakes

Suppliers hold high bargaining power: cell makers (CATL ~34% share end-2025) and chip fabs (TSMC >90% utilization in 2024) command pricing and delivery; batteries are 30–40% of EV BOM, lithium rose ~120% (2021–23) and cobalt ~€38k/ton (2024). BMW’s €55.4bn materials spend (2024), 6–18 month requalification, and €1–5M tooling per part lock-in, so long-term offtakes and equity stakes are needed to mitigate risk.

| Metric | Value |

|---|---|

| CATL global share (end-2025) | ~34% |

| Battery share of EV BOM | 30–40% |

| Lithium price change (2021–23) | +120% |

| Cobalt price (2024) | ~€38,000/ton |

| BMW materials spend (2024) | €55.4bn |

| Supplier requalification | 6–18 months |

| Tooling cost per part | €1–5M |

What is included in the product

Tailored exclusively for Bayerische Motoren Werke, this Porter's Five Forces analysis uncovers competitive drivers, customer and supplier influence, entry barriers, substitutes, and emerging threats shaping BMW's pricing power and profitability.

Compact Porter's Five Forces snapshot for BMW—quickly highlights supplier/buyer leverage, competitive rivalry, entrant threats, and substitution risk to streamline strategic decisions.

Customers Bargaining Power

High Information Transparency

By end-2025, digital platforms let premium buyers compare prices, specs, and real-world performance across brands in minutes; 78% of luxury-vehicle shoppers used online configurators or third-party reviews when buying in 2024, per McKinsey. This info transparency lets customers pressure dealers for discounts, so BMW must keep competitive pricing, clearer total-cost-of-ownership messaging, and frequent online incentives to retain sophisticated buyers.

Low Switching Costs in Premium Segment

Low switching costs in the premium segment weaken buyer power for BMW: wealthy customers often shift among Mercedes-Benz, Audi, and Tesla with little friction, and global premium lease penetration reached about 28% of new luxury registrations in 2024, up from 22% in 2019. Lease terms (typically 24–36 months) let buyers adopt new tech or better financing frequently, so BMW must outcompete on features, software updates, and lease incentives.

Expansion of Alternative Ownership Models

The rise of car-subscription services and high-end car-sharing platforms (e.g., Share Now, Porsche Drive) gave consumers access to BMW models without purchase; in 2024 global car subscriptions grew ~25% to ~1.2 million users, shifting demand toward access over ownership.

This access preference reduces BMW’s bargaining leverage, forcing competition on mobility offerings; BMW Group reported 2024 Mobility Services revenue of €2.9bn, so flexibility and seamless finance/mobility packages now matter as much as vehicle specs.

Demand for Technological Innovation

Modern premium buyers now value software, ADAS (advanced driver-assist systems), and low-emission powertrains more than mechanical prestige, and BMW faces rapid churn risk if its digital UX lags—Tesla held 16% of global BEV luxury share in 2024 and Chinese luxury EV entrants grew 42% y/y in 2024, showing fast substitutability.

Price Sensitivity in the EV Market

BMW faces rising price sensitivity as global EV choices grow; 2025 EV market share hit ~14% of global car sales, upping consumer comparisons.

Buyers weigh total cost of ownership—charging, maintenance, software subscriptions—so BMW must justify premiums via range, charging speed, and its digital ecosystem.

In 2024 BMW advertised up to 367 miles WLTP (i7 xDrive60) and 200+ kW DC fast charging to defend premium positioning.

- 2025 EV share ~14%

- Total cost focus: charging + software

- BMW claims 367 mi range, 200+ kW charging

- Must prove digital ecosystem value

Buyers wield power: BMW must fight on price, TCO, subscriptions & software

Buyers have strong leverage: 78% used online configurators/reviews in 2024 (McKinsey), 2025 EV share ~14%, global premium lease penetration ~28% (2024), BMW Mobility revenue €2.9bn (2024), Tesla 16% BEV luxury share (2024). BMW must compete on price, TCO (charging, software), subscriptions, and continuous software/ADAS updates to retain customers.

| Metric | Value |

|---|---|

| Online research use (2024) | 78% |

| EV global share (2025) | ~14% |

| Premium lease penetration (2024) | ~28% |

| BMW Mobility revenue (2024) | €2.9bn |

| Tesla luxury BEV share (2024) | 16% |

Full Version Awaits

Bayerische Motoren Werke Porter's Five Forces Analysis

This preview shows the exact Bayerische Motoren Werke Porter’s Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed here is part of the full, professionally formatted file you’ll be able to download and use the moment you buy.

You're viewing the actual deliverable; once payment is complete, you’ll get instant access to this identical, ready-to-use analysis.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

Bayerische Motoren Werke faces intense rivalry from premium rivals, moderate supplier power due to specialized components, rising buyer expectations for EVs and tech, growing substitute threats from mobility services, and high barriers deterring new entrants but enabling incumbents to defend margins.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Bayerische Motoren Werke’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of EV Battery Manufacturers

By end-2025, battery cell market is concentrated: CATL held ~34% global market share and Northvolt scaled to ~6% capacity, giving few firms outsized leverage over BMW’s Neue Klasse sourcing.

Batteries are ~30–40% of EV BOM (bill of materials), so BMW’s production hinges on securing cells; shortages would directly raise costs and delay deliveries.

BMW is diversifying via long-term offtakes and equity stakes (e.g., 2024 €Xbn deals), but high R&D, gigafactory scale, and cell chemistry expertise keep partner pool small.

Semiconductor and Software Integration

As BMW shifts to software-defined vehicles, high-end chipmakers (TSMC, Intel, Infineon) and software suppliers (Nvidia, Continental) hold strong leverage: specialized silicon and middleware are hard to swap without rearchitecting ECUs, raising switching costs. Global advanced logic wafer shortages kept fab utilization >90% in 2024 and led to foundry ASP rises ~15% YoY, so suppliers sustain firm pricing and delivery terms, pressuring BMWs margin and time-to-market.

Raw Material Scarcity and Sustainability

Suppliers of lithium, cobalt and rare earths gained leverage as EV demand rose; lithium prices jumped ~120% in 2021–2023 and cobalt averaged $38,000/ton in 2024, raising BMW’s input costs.

BMW needs multi-year contracts and equity stakes in mines; in 2024 BMW committed to securing sources for cells, targeting 50 GWh of battery capacity by 2030 to lock supply.

Compliance with ESG (environmental, social, governance) audits adds cost and limits supplier pool, giving a few mining firms pricing power and creating a production bottleneck.

Specialized Premium Components

BMW relies on specialized suppliers for leather, Alcantara, carbon fiber and precision driveline parts; in 2024 BMW Group spent €55.4 billion on materials and third-party services, much of which supports premium components.

These suppliers co-develop parts with BMW, creating mutual dependence but giving suppliers pricing and delivery leverage due to unique craftsmanship and certifications; switching suppliers risks 6–18 months of validation and potential warranty/quality costs.

- €55.4bn materials/third-party spend (2024)

- 6–18 months supplier requalification time

- High supplier leverage from certified craftsmanship

High Switching Costs for Tooling

High switching costs for tooling give suppliers strong leverage over Bayerische Motoren Werke (BMW); dedicated presses, dies, and stamping tools often cost €1–5 million per part and require months of revalidation. Suppliers can demand higher margins during a model lifecycle because mid-cycle replacement triggers new homologation, testing, and line reconfiguration that can exceed 10% of program cost. In 2024, automotive OEMs reported average supplier changeover lead times of 6–12 months, raising practical lock-in. This technical lock-in raises supplier bargaining power through price and delivery terms.

- Tool cost per part: €1–5M

- Changeover lead time: 6–12 months (2024)

- Revalidation/line costs: often >10% of program

Supplier Power Dominates EV Value Chain: Batteries, Chips, and Long-Term Offtakes

Suppliers hold high bargaining power: cell makers (CATL ~34% share end-2025) and chip fabs (TSMC >90% utilization in 2024) command pricing and delivery; batteries are 30–40% of EV BOM, lithium rose ~120% (2021–23) and cobalt ~€38k/ton (2024). BMW’s €55.4bn materials spend (2024), 6–18 month requalification, and €1–5M tooling per part lock-in, so long-term offtakes and equity stakes are needed to mitigate risk.

| Metric | Value |

|---|---|

| CATL global share (end-2025) | ~34% |

| Battery share of EV BOM | 30–40% |

| Lithium price change (2021–23) | +120% |

| Cobalt price (2024) | ~€38,000/ton |

| BMW materials spend (2024) | €55.4bn |

| Supplier requalification | 6–18 months |

| Tooling cost per part | €1–5M |

What is included in the product

Tailored exclusively for Bayerische Motoren Werke, this Porter's Five Forces analysis uncovers competitive drivers, customer and supplier influence, entry barriers, substitutes, and emerging threats shaping BMW's pricing power and profitability.

Compact Porter's Five Forces snapshot for BMW—quickly highlights supplier/buyer leverage, competitive rivalry, entrant threats, and substitution risk to streamline strategic decisions.

Customers Bargaining Power

High Information Transparency

By end-2025, digital platforms let premium buyers compare prices, specs, and real-world performance across brands in minutes; 78% of luxury-vehicle shoppers used online configurators or third-party reviews when buying in 2024, per McKinsey. This info transparency lets customers pressure dealers for discounts, so BMW must keep competitive pricing, clearer total-cost-of-ownership messaging, and frequent online incentives to retain sophisticated buyers.

Low Switching Costs in Premium Segment

Low switching costs in the premium segment weaken buyer power for BMW: wealthy customers often shift among Mercedes-Benz, Audi, and Tesla with little friction, and global premium lease penetration reached about 28% of new luxury registrations in 2024, up from 22% in 2019. Lease terms (typically 24–36 months) let buyers adopt new tech or better financing frequently, so BMW must outcompete on features, software updates, and lease incentives.

Expansion of Alternative Ownership Models

The rise of car-subscription services and high-end car-sharing platforms (e.g., Share Now, Porsche Drive) gave consumers access to BMW models without purchase; in 2024 global car subscriptions grew ~25% to ~1.2 million users, shifting demand toward access over ownership.

This access preference reduces BMW’s bargaining leverage, forcing competition on mobility offerings; BMW Group reported 2024 Mobility Services revenue of €2.9bn, so flexibility and seamless finance/mobility packages now matter as much as vehicle specs.

Demand for Technological Innovation

Modern premium buyers now value software, ADAS (advanced driver-assist systems), and low-emission powertrains more than mechanical prestige, and BMW faces rapid churn risk if its digital UX lags—Tesla held 16% of global BEV luxury share in 2024 and Chinese luxury EV entrants grew 42% y/y in 2024, showing fast substitutability.

Price Sensitivity in the EV Market

BMW faces rising price sensitivity as global EV choices grow; 2025 EV market share hit ~14% of global car sales, upping consumer comparisons.

Buyers weigh total cost of ownership—charging, maintenance, software subscriptions—so BMW must justify premiums via range, charging speed, and its digital ecosystem.

In 2024 BMW advertised up to 367 miles WLTP (i7 xDrive60) and 200+ kW DC fast charging to defend premium positioning.

- 2025 EV share ~14%

- Total cost focus: charging + software

- BMW claims 367 mi range, 200+ kW charging

- Must prove digital ecosystem value

Buyers wield power: BMW must fight on price, TCO, subscriptions & software

Buyers have strong leverage: 78% used online configurators/reviews in 2024 (McKinsey), 2025 EV share ~14%, global premium lease penetration ~28% (2024), BMW Mobility revenue €2.9bn (2024), Tesla 16% BEV luxury share (2024). BMW must compete on price, TCO (charging, software), subscriptions, and continuous software/ADAS updates to retain customers.

| Metric | Value |

|---|---|

| Online research use (2024) | 78% |

| EV global share (2025) | ~14% |

| Premium lease penetration (2024) | ~28% |

| BMW Mobility revenue (2024) | €2.9bn |

| Tesla luxury BEV share (2024) | 16% |

Full Version Awaits

Bayerische Motoren Werke Porter's Five Forces Analysis

This preview shows the exact Bayerische Motoren Werke Porter’s Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed here is part of the full, professionally formatted file you’ll be able to download and use the moment you buy.

You're viewing the actual deliverable; once payment is complete, you’ll get instant access to this identical, ready-to-use analysis.