Bank Negara Indonesia PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Navigate Bank Negara Indonesia’s future with our concise PESTLE snapshot—highlighting regulatory risks, economic drivers, technological shifts, and social trends shaping performance; ideal for investors and strategists seeking competitive clarity. Buy the full PESTLE report to access detailed, actionable insights and ready-to-use slides and Excel models for immediate decision-making.

Political factors

State-Owned Enterprise Mandates

As a Himbara member, BNI aligns strategy with government development goals, channeling priority credit—IDR 120–150 trillion annually across state banks in 2024—into infrastructure, downstreaming of resources and food security programs.

BNI routed IDR 45 trillion to infrastructure projects and IDR 18 trillion to agriculture/food supply chains in 2024, reflecting mandated sectoral focus.

Government influence over dividend policy and board appointments persists; state guidance limited 2024 dividends to support capital buffers after a 2023 CET1 ratio of 15.2%.

Government Policy Continuity

The Prabowo-Gibran administration (from Oct 2024) emphasizes continuity on major infrastructure and Nusantara relocation, sustaining BNI’s role financing projects—BNI reported Rp 1.2 trillion in syndication loans to infrastructure in 2024, supporting a steady corporate lending pipeline.

Multi-year projects offer predictable asset growth but concentration risk: infrastructure lending comprised about 18% of BNI’s FY2024 corporate loan book.

Policy shifts in fiscal priorities or a reshuffle at the Ministry of SOEs could reallocate capital, forcing BNI to reprice risk or reduce exposure if state-backed project funding falls.

Geopolitical Stability and International Footprint

BNI's international footprint includes branches in London, New York and Tokyo supporting cross-border deals; overseas operations contributed to 14% of international transaction volumes in 2024. Geopolitical tensions in the Middle East or South China Sea can disrupt trade lanes and raised BNI's cost of USD funding by about 45–60 bps during 2022–2024 stress episodes. Management must hedge political and FX risks while aligning with government targets to boost Indonesia's global trade share, which grew 6.2% in 2024.

National Food and Energy Security Programs

The government aims for food and energy self-sufficiency by 2025, directing IDR 150+ trillion in state-led subsidies and investments, increasing demand for state bank financing to agritech and renewables.

BNI is expected to roll out tailored lending for precision agriculture and solar/wind projects; its 2024 renewable exposure stood near IDR 12 trillion, signaling growth but higher tech and yield risks.

New market opportunities come with volatility from crop cycles and unproven green tech, raising credit and operational risk that could affect NPLs and capital ratios.

- Government target: self-sufficiency by 2025; IDR 150+ trillion mobilized

- BNI renewable exposure ~IDR 12 trillion (2024)

- Opportunities: agritech, solar/wind financing

- Risks: agricultural cycles, tech performance, credit and capital pressure

Regulatory Pressure on Financial Inclusion

Political pressure to boost financial inclusion remains a top priority; Indonesia aims to raise the adult financial inclusion rate from 76% in 2019 to over 90% by 2024–25, pushing BNI to expand both digital services and 5,000+ agent/banking outlets in underserved areas.

Meeting this mandate forces BNI to invest heavily in rural infrastructure and last-mile connectivity, increasing CAPEX and raising cost-to-income ratios temporarily; serving remote customers can cost up to 3–5x more per transaction versus urban centers.

BNI pivots state credit to infra, agri, renewables amid FX, funding and governance risks

BNI aligns with state development priorities, channeling mandated credit into infrastructure, agriculture and renewables (infrastructure ~IDR 45T, agriculture ~IDR 18T, renewables ~IDR 12T in 2024), while government influence on dividends/board and SOE policy reshuffles affect capital allocation; international exposure (14% of transaction volumes) and geopolitical funding shocks (USD funding +45–60bps 2022–24) raise FX and credit risks.

| Metric | 2024 |

|---|---|

| Infra lending | IDR 45T |

| Agriculture | IDR 18T |

| Renewables | IDR 12T |

| Intl txn vol | 14% |

| USD funding stress | +45–60bps |

What is included in the product

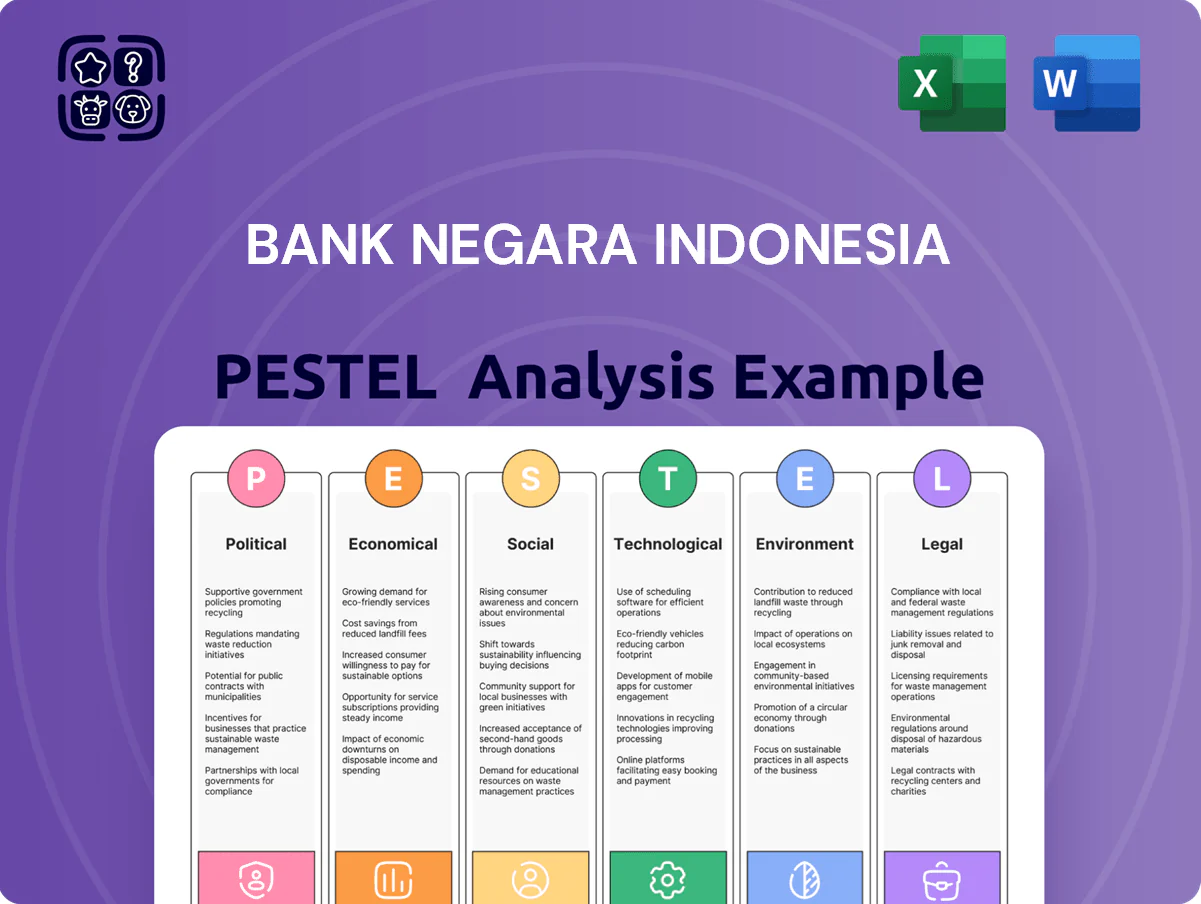

Explores how external macro-environmental factors uniquely affect Bank Negara Indonesia across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and region-specific examples to identify risks and opportunities for executives, consultants, and entrepreneurs.

A concise PESTLE summary of Bank Negara Indonesia that’s easy to drop into presentations or share across teams, helping stakeholders quickly grasp external risks and regulatory shifts impacting strategy.

Economic factors

Interest Rate and Net Interest Margin Volatility

Bank Indonesia’s policy rate moves, tracking Fed-driven global rate shifts, directly alter BNI’s funding costs and loan pricing; BI maintained a 7-day reverse repo at 5.75% in Dec 2025 consensus, pressuring deposit rates and lending spreads. By end-2025 BNI must protect NIM—reported 4.1% in 9M2025—against volatile domestic inflation (estimated 3.6%–4.5%) and IDR swings. Higher rates can boost interest income but may lift NPLs from 2.6% in 2024 if borrower stress rises, tightening credit provisioning and capital ratios.

Domestic Consumption and GDP Growth

Indonesia targets ~5% GDP growth (2024-25 outlook), fueled by domestic consumption that accounted for ~55% of GDP in 2023; rising middle-class households (projected >110 million by 2025) lifts demand for mortgages, auto loans and unsecured credit. BNI’s retail and consumer banking are well positioned to capture this, but performance hinges on consumer purchasing power and retail sales growth (retail sales rose ~6% YoY in 2024).

Rupiah Exchange Rate Stability

BNI is highly exposed to Rupiah/USD volatility given sizable foreign-currency lending; the IDR slid about 5.2% vs USD in 2023 and ranged 0.8–3.5% monthly in 2024, raising FX-driven repayment stress for corporates and risking asset-quality deterioration.

Sharp depreciations amplify nonperforming loan risk for FX borrowers—IFRS 9 provisions rose 12% YoY at Indonesian banks in 2024 amid FX pressure.

BNI mitigates via dynamic hedging—forwards, swaps and options—and held net FX liquidity and reserves covering short-term FX gap equivalent to roughly 1.1 months of import cover at end-2024, reducing immediate currency risk.

Expansion of the SME Segment

Indonesian government targets SMEs as economic backbone; SMEs contribute about 61% of GDP and 97% of employment (BPS 2023), prompting policy support and incentives.

BNI shifted strategy to increase SME exposure, growing SME loan book ~12% YoY to IDR 120 trillion in 2024 and expanding digital channels to cut acquisition/monitoring costs.

Stable SME performance supports BNI’s diversified loan mix, reducing NPL volatility—SME NPLs remained near 2.5% in 2024—helping long-term earnings stability.

- SMEs: ~61% GDP, 97% employment (BPS 2023)

- BNI SME loans: ~IDR 120T, +12% YoY (2024)

- SME NPL ~2.5% (2024)

Capital Market Performance and Wealth Management

The Jakarta Composite Index rose about 18% from end-2023 to end-2025, driving higher retail and institutional flows into wealth products and boosting BNI Asset Management and custodial volumes.

BNI shifted strategy toward fee-based income, targeting a 15–20% share of non-interest income by late 2025 to reduce reliance on net interest margin.

Volatility or liquidity shocks cut AUM and fees; a 10% drop in market cap in 2024 trimmed projected investment product profits by roughly 8%.

- JCI +18% (2023–2025)

- BNI target fee-income 15–20% by late 2025

- 10% market cap fall → ~8% profit hit on investment products

BI 5.75% lifts BNI costs; GDP ~5%, retail & SMEs drive growth amid IDR swings

BI rate at 5.75% (Dec 2025 consensus) lifts BNI funding costs; 9M2025 NIM 4.1% vs 2024 NPL 2.6%. GDP ~5% (2024–25), consumption ~55% of GDP, middle class >110m (2025) supports retail growth; retail sales +6% YoY (2024). IDR volatility: −5.2% vs USD (2023); 2024 monthly swings 0.8–3.5%. SME loans IDR120T (+12% YoY, 2024); SME share ~61% GDP.

| Metric | Value |

|---|---|

| BI rate | 5.75% |

| NIM (9M2025) | 4.1% |

| NPL (2024) | 2.6% |

| GDP growth | ~5% |

| SME loans (2024) | IDR120T |

Preview the Actual Deliverable

Bank Negara Indonesia PESTLE Analysis

The preview shown here is the exact Bank Negara Indonesia PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Plan Smarter. Present Sharper. Compete Stronger.

Navigate Bank Negara Indonesia’s future with our concise PESTLE snapshot—highlighting regulatory risks, economic drivers, technological shifts, and social trends shaping performance; ideal for investors and strategists seeking competitive clarity. Buy the full PESTLE report to access detailed, actionable insights and ready-to-use slides and Excel models for immediate decision-making.

Political factors

State-Owned Enterprise Mandates

As a Himbara member, BNI aligns strategy with government development goals, channeling priority credit—IDR 120–150 trillion annually across state banks in 2024—into infrastructure, downstreaming of resources and food security programs.

BNI routed IDR 45 trillion to infrastructure projects and IDR 18 trillion to agriculture/food supply chains in 2024, reflecting mandated sectoral focus.

Government influence over dividend policy and board appointments persists; state guidance limited 2024 dividends to support capital buffers after a 2023 CET1 ratio of 15.2%.

Government Policy Continuity

The Prabowo-Gibran administration (from Oct 2024) emphasizes continuity on major infrastructure and Nusantara relocation, sustaining BNI’s role financing projects—BNI reported Rp 1.2 trillion in syndication loans to infrastructure in 2024, supporting a steady corporate lending pipeline.

Multi-year projects offer predictable asset growth but concentration risk: infrastructure lending comprised about 18% of BNI’s FY2024 corporate loan book.

Policy shifts in fiscal priorities or a reshuffle at the Ministry of SOEs could reallocate capital, forcing BNI to reprice risk or reduce exposure if state-backed project funding falls.

Geopolitical Stability and International Footprint

BNI's international footprint includes branches in London, New York and Tokyo supporting cross-border deals; overseas operations contributed to 14% of international transaction volumes in 2024. Geopolitical tensions in the Middle East or South China Sea can disrupt trade lanes and raised BNI's cost of USD funding by about 45–60 bps during 2022–2024 stress episodes. Management must hedge political and FX risks while aligning with government targets to boost Indonesia's global trade share, which grew 6.2% in 2024.

National Food and Energy Security Programs

The government aims for food and energy self-sufficiency by 2025, directing IDR 150+ trillion in state-led subsidies and investments, increasing demand for state bank financing to agritech and renewables.

BNI is expected to roll out tailored lending for precision agriculture and solar/wind projects; its 2024 renewable exposure stood near IDR 12 trillion, signaling growth but higher tech and yield risks.

New market opportunities come with volatility from crop cycles and unproven green tech, raising credit and operational risk that could affect NPLs and capital ratios.

- Government target: self-sufficiency by 2025; IDR 150+ trillion mobilized

- BNI renewable exposure ~IDR 12 trillion (2024)

- Opportunities: agritech, solar/wind financing

- Risks: agricultural cycles, tech performance, credit and capital pressure

Regulatory Pressure on Financial Inclusion

Political pressure to boost financial inclusion remains a top priority; Indonesia aims to raise the adult financial inclusion rate from 76% in 2019 to over 90% by 2024–25, pushing BNI to expand both digital services and 5,000+ agent/banking outlets in underserved areas.

Meeting this mandate forces BNI to invest heavily in rural infrastructure and last-mile connectivity, increasing CAPEX and raising cost-to-income ratios temporarily; serving remote customers can cost up to 3–5x more per transaction versus urban centers.

BNI pivots state credit to infra, agri, renewables amid FX, funding and governance risks

BNI aligns with state development priorities, channeling mandated credit into infrastructure, agriculture and renewables (infrastructure ~IDR 45T, agriculture ~IDR 18T, renewables ~IDR 12T in 2024), while government influence on dividends/board and SOE policy reshuffles affect capital allocation; international exposure (14% of transaction volumes) and geopolitical funding shocks (USD funding +45–60bps 2022–24) raise FX and credit risks.

| Metric | 2024 |

|---|---|

| Infra lending | IDR 45T |

| Agriculture | IDR 18T |

| Renewables | IDR 12T |

| Intl txn vol | 14% |

| USD funding stress | +45–60bps |

What is included in the product

Explores how external macro-environmental factors uniquely affect Bank Negara Indonesia across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and region-specific examples to identify risks and opportunities for executives, consultants, and entrepreneurs.

A concise PESTLE summary of Bank Negara Indonesia that’s easy to drop into presentations or share across teams, helping stakeholders quickly grasp external risks and regulatory shifts impacting strategy.

Economic factors

Interest Rate and Net Interest Margin Volatility

Bank Indonesia’s policy rate moves, tracking Fed-driven global rate shifts, directly alter BNI’s funding costs and loan pricing; BI maintained a 7-day reverse repo at 5.75% in Dec 2025 consensus, pressuring deposit rates and lending spreads. By end-2025 BNI must protect NIM—reported 4.1% in 9M2025—against volatile domestic inflation (estimated 3.6%–4.5%) and IDR swings. Higher rates can boost interest income but may lift NPLs from 2.6% in 2024 if borrower stress rises, tightening credit provisioning and capital ratios.

Domestic Consumption and GDP Growth

Indonesia targets ~5% GDP growth (2024-25 outlook), fueled by domestic consumption that accounted for ~55% of GDP in 2023; rising middle-class households (projected >110 million by 2025) lifts demand for mortgages, auto loans and unsecured credit. BNI’s retail and consumer banking are well positioned to capture this, but performance hinges on consumer purchasing power and retail sales growth (retail sales rose ~6% YoY in 2024).

Rupiah Exchange Rate Stability

BNI is highly exposed to Rupiah/USD volatility given sizable foreign-currency lending; the IDR slid about 5.2% vs USD in 2023 and ranged 0.8–3.5% monthly in 2024, raising FX-driven repayment stress for corporates and risking asset-quality deterioration.

Sharp depreciations amplify nonperforming loan risk for FX borrowers—IFRS 9 provisions rose 12% YoY at Indonesian banks in 2024 amid FX pressure.

BNI mitigates via dynamic hedging—forwards, swaps and options—and held net FX liquidity and reserves covering short-term FX gap equivalent to roughly 1.1 months of import cover at end-2024, reducing immediate currency risk.

Expansion of the SME Segment

Indonesian government targets SMEs as economic backbone; SMEs contribute about 61% of GDP and 97% of employment (BPS 2023), prompting policy support and incentives.

BNI shifted strategy to increase SME exposure, growing SME loan book ~12% YoY to IDR 120 trillion in 2024 and expanding digital channels to cut acquisition/monitoring costs.

Stable SME performance supports BNI’s diversified loan mix, reducing NPL volatility—SME NPLs remained near 2.5% in 2024—helping long-term earnings stability.

- SMEs: ~61% GDP, 97% employment (BPS 2023)

- BNI SME loans: ~IDR 120T, +12% YoY (2024)

- SME NPL ~2.5% (2024)

Capital Market Performance and Wealth Management

The Jakarta Composite Index rose about 18% from end-2023 to end-2025, driving higher retail and institutional flows into wealth products and boosting BNI Asset Management and custodial volumes.

BNI shifted strategy toward fee-based income, targeting a 15–20% share of non-interest income by late 2025 to reduce reliance on net interest margin.

Volatility or liquidity shocks cut AUM and fees; a 10% drop in market cap in 2024 trimmed projected investment product profits by roughly 8%.

- JCI +18% (2023–2025)

- BNI target fee-income 15–20% by late 2025

- 10% market cap fall → ~8% profit hit on investment products

BI 5.75% lifts BNI costs; GDP ~5%, retail & SMEs drive growth amid IDR swings

BI rate at 5.75% (Dec 2025 consensus) lifts BNI funding costs; 9M2025 NIM 4.1% vs 2024 NPL 2.6%. GDP ~5% (2024–25), consumption ~55% of GDP, middle class >110m (2025) supports retail growth; retail sales +6% YoY (2024). IDR volatility: −5.2% vs USD (2023); 2024 monthly swings 0.8–3.5%. SME loans IDR120T (+12% YoY, 2024); SME share ~61% GDP.

| Metric | Value |

|---|---|

| BI rate | 5.75% |

| NIM (9M2025) | 4.1% |

| NPL (2024) | 2.6% |

| GDP growth | ~5% |

| SME loans (2024) | IDR120T |

Preview the Actual Deliverable

Bank Negara Indonesia PESTLE Analysis

The preview shown here is the exact Bank Negara Indonesia PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.