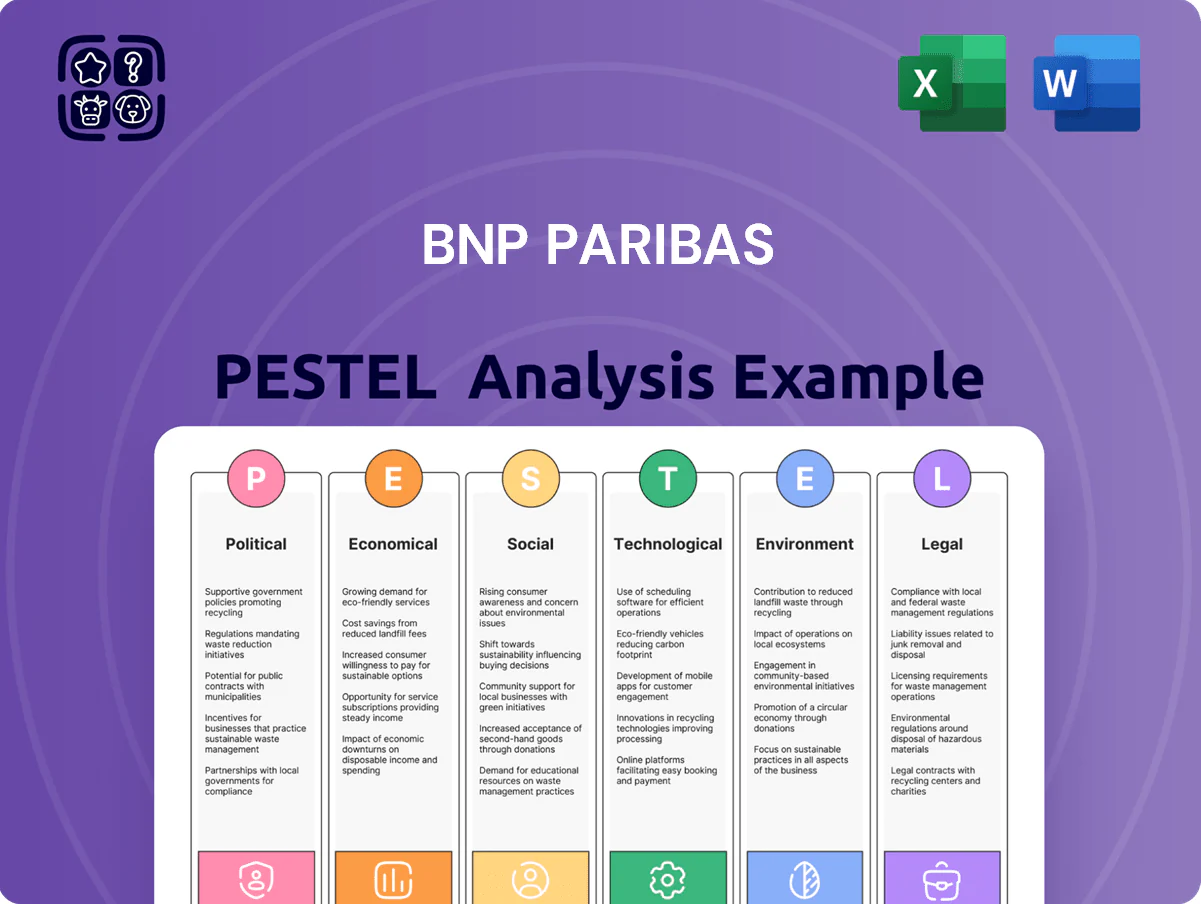

BNP Paribas PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Explore how political shifts, regulatory pressure, and digital transformation are reshaping BNP Paribas’s strategic outlook in our concise PESTLE snapshot—perfect for investors and strategists needing quick, actionable context. Purchase the full PESTLE analysis to access detailed risk assessments, market implications, and ready-to-use recommendations that will sharpen your decisions and planning.

Political factors

European Banking Union integration

BNP Paribas is shaped by Eurozone banking union integration and ECB oversight, with the bank classified as globally systemic (G-SIB) and subject to ECB supervision covering 19 euro area countries; the ECB’s SSM enforces harmonized capital and liquidity rules, influencing BNP Paribas’s CET1 target (12.3% pro forma at end‑2025 guidance) and cross‑border capital flows across its €1.7tn+ assets. Political stability in France and the Eurozone affects its EU champion strategy and market access.

Geopolitical instability and trade tensions

BNP Paribas faces heightened exposure as geopolitical conflicts and US-China-Russia trade barriers increase; cross-border revenue represented ~44% of group net banking income in 2024, amplifying sensitivity to disruptions.

Sanctions and alliance shifts force enhanced compliance—BNP Paribas reported €1.1bn in non-credit risk provisions in 2024 and maintains advanced screening across its Corporate & Institutional Banking unit.

Political shifts in emerging markets reduce lending appetite: EMEA and Asia credit growth slowed to 2.3% and 3.1% respectively in 2024, prompting tighter risk limits on international loans.

French domestic policy and fiscal measures

As a French-headquartered bank, BNP Paribas is exposed to changes in domestic taxation and labor laws; for example, France's 2024 corporate tax rate remained at 25%, while proposals for sector-specific levies could raise effective rates for banks and dent 2025 net income estimates (2024 net income €17.5bn). Political shifts in public spending and industrial sovereignty programs, with €20bn in 2023-24 strategic funding, steer the bank toward financing national strategic sectors, affecting capital allocation and risk appetite.

Regulatory pressure on sovereign debt exposure

Political decisions on national debt and fiscal discipline across Europe directly affect valuation of BNP Paribas’s sovereign bond portfolio, which totalled roughly EUR 150bn on the balance sheet in 2024, exposing the bank to yield-driven mark-to-market moves.

Shifts in political climate can spike bond yields—European 10-year yields rose ~120bp during 2022–24 stress—pressuring CET1, liquidity coverage ratio and funding costs.

Policymakers’ positions on debt restructuring and EU stability tools (EFSF/ESM reforms) are key inputs for BNP Paribas’s multi-year capital planning and stress tests.

- EUR 150bn sovereign holdings (2024)

- 10y Euro area yields +~120bp (2022–24)

- Impact channels: MTM losses, LCR, CET1

Government-led ESG mandates

Political agendas prioritizing a low-carbon transition increase pressure on banks like BNP Paribas to decarbonize portfolios; EU Fit for 55 and France’s 2030/2050 targets push alignment with national climate goals.

Governments are tightening disclosure—EU CSRD expands reporting to ~50,000 firms—and channeling subsidies and guarantees into green financing, boosting public-private green lending pools.

BNP Paribas must revise lending policies to retain public-sector mandates and access to green facilities; the bank disclosed €240bn in sustainable finance commitments by 2025 targets.

- EU CSRD: ~50,000 firms in scope

- BNP Paribas sustainable finance target: €240bn by 2025

- National net-zero laws raise compliance risk and affect public mandates

BNP Paribas: €1.7tn G‑SIB, €17.5bn profit, 12.3% CET1 target, €240bn sustainable finance

BNP Paribas faces ECB SSM oversight as a G-SIB, €1.7tn+ assets; 2024 CET1 guidance 12.3% pro forma to 2025, sovereign holdings ~€150bn; 2024 net income €17.5bn; cross-border revenue ~44% of NBI; non-credit provisions €1.1bn (2024); EMEA/Asia credit growth 2.3%/3.1% (2024); sustainable finance target €240bn by 2025.

| Metric | 2024/Target |

|---|---|

| Assets | €1.7tn+ |

| CET1 (target) | 12.3% pro forma |

| Net income | €17.5bn |

| Sovereigns | €150bn |

| Cross-border NBI | ~44% |

| Sustainable finance | €240bn (2025) |

What is included in the product

Explores how external macro-environmental factors uniquely affect BNP Paribas across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven trends and forward-looking insights to inform risk mitigation and strategic opportunity identification for executives and investors.

Provides a succinct, PESTLE-segmented summary of BNP Paribas’s external environment that can be dropped into presentations or shared across teams for quick alignment and risk discussion.

Economic factors

Interest rate environment and monetary policy

The transition from a high-rate environment (ECB deposit rate peaking at 4.0% in 2023) toward stabilization and gradual easing by late 2025 pressures BNP Paribas net interest margin, which expanded to c.1.25% in 2023 but faces compression as lending yields realign.

Higher rates boosted retail lending income—group net interest income rose c.9% YoY in 2023—but the bank must pivot to fee-based services and wealth management to sustain revenue growth as margins normalize.

The European Central Bank remains the primary driver of BNP Paribas cost of funding and lending profitability; shifts in ECB policy directly affect funding spreads and credit pricing across its euro-area portfolio.

Inflationary trends and operating costs

Persisting inflation—Eurozone CPI at 3.4% in Dec 2025—raises BNP Paribas operating expenses via higher personnel costs (wage inflation ~4% in 2024‑25) and increased IT/cloud spending, squeezing margins.

Reduced consumer purchasing power and weaker corporate capex cut loan demand; European new lending volumes slowed ~2% YoY in 2024, pressuring net interest income.

Elevated service costs and wage growth complicate managing the cost-to-income ratio, which stood around 67% for BNP Paribas in FY 2024, highlighting margin pressure.

Global economic growth and recessionary risks

BNP Paribas’ results closely track GDP in core markets—Eurozone GDP grew 0.5% q/q in Q4 2024 but IMF warned global growth slows to 3.0% in 2025, raising recession risk; downturns push non-performing loans up and forced provisions (bank CET1 ratio pressure).

Currency exchange rate volatility

As a global bank, BNP Paribas is exposed to EUR volatility versus USD, GBP and EM currencies; a 10% EUR appreciation in 2024 would have reduced translated revenues from non-euro operations materially (group reported 2024 net banking income €52.0bn, with ~40% generated outside the euro area).

Exchange swings affect translated earnings, capital ratios and pricing of trade finance; BNP reported FX hedges of €120bn notional at end-2024 to limit P&L volatility.

- 10% EUR move can significantly alter translated revenues (~€20bn non-euro income exposure)

- €120bn hedging notional at end-2024 to mitigate FX impact

- FX volatility affects capital ratios, earnings and trade finance competitiveness

Capital market performance and asset valuations

Capital market health directly affects BNP Paribas; global equity markets rose ~18% in 2023 and remained up ~6% YTD through 2024, boosting AUM and performance fees in Wealth and Asset Management, while 2022–23 bond volatility cut trading volumes and advisory income.

Proprietary portfolios are exposed to valuation swings—BNP reported Group net income sensitivity to market shocks, with trading revenues varying ±20% across high-volatility quarters in 2022–24.

- Higher equities → increased AUM/performance fees

- Bond/volatility spikes → lower trading/advisory income

- Proprietary portfolios sensitive; trading revenues swung ~±20%

ECB peak 4.0% → easing; NII up, margins squeezed, FX & hedges drive revenue volatility

ECB rate peak 4.0% (2023) then easing to 3.0% by late‑2025 compresses NIM (1.25% in 2023); NII rose ~9% in 2023 but lending volumes fell ~2% in 2024; Eurozone CPI 3.4% (Dec 2025) and wage inflation ~4% push costs (cost/income ~67% in 2024); EUR FX moves (10% swing) and €120bn hedges (end‑2024) materially affect translated revenues (2024 NBI €52.0bn, ~40% non‑EUR).

| Metric | Value |

|---|---|

| ECB rate peak | 4.0% (2023) |

| NIM | ~1.25% (2023) |

| Group NBI | €52.0bn (2024) |

| Non‑EUR share | ~40% |

| Hedges notional | €120bn (end‑2024) |

| Cost/Income | ~67% (2024) |

Preview the Actual Deliverable

BNP Paribas PESTLE Analysis

The preview shown here is the exact BNP Paribas PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic or investment work.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Explore how political shifts, regulatory pressure, and digital transformation are reshaping BNP Paribas’s strategic outlook in our concise PESTLE snapshot—perfect for investors and strategists needing quick, actionable context. Purchase the full PESTLE analysis to access detailed risk assessments, market implications, and ready-to-use recommendations that will sharpen your decisions and planning.

Political factors

European Banking Union integration

BNP Paribas is shaped by Eurozone banking union integration and ECB oversight, with the bank classified as globally systemic (G-SIB) and subject to ECB supervision covering 19 euro area countries; the ECB’s SSM enforces harmonized capital and liquidity rules, influencing BNP Paribas’s CET1 target (12.3% pro forma at end‑2025 guidance) and cross‑border capital flows across its €1.7tn+ assets. Political stability in France and the Eurozone affects its EU champion strategy and market access.

Geopolitical instability and trade tensions

BNP Paribas faces heightened exposure as geopolitical conflicts and US-China-Russia trade barriers increase; cross-border revenue represented ~44% of group net banking income in 2024, amplifying sensitivity to disruptions.

Sanctions and alliance shifts force enhanced compliance—BNP Paribas reported €1.1bn in non-credit risk provisions in 2024 and maintains advanced screening across its Corporate & Institutional Banking unit.

Political shifts in emerging markets reduce lending appetite: EMEA and Asia credit growth slowed to 2.3% and 3.1% respectively in 2024, prompting tighter risk limits on international loans.

French domestic policy and fiscal measures

As a French-headquartered bank, BNP Paribas is exposed to changes in domestic taxation and labor laws; for example, France's 2024 corporate tax rate remained at 25%, while proposals for sector-specific levies could raise effective rates for banks and dent 2025 net income estimates (2024 net income €17.5bn). Political shifts in public spending and industrial sovereignty programs, with €20bn in 2023-24 strategic funding, steer the bank toward financing national strategic sectors, affecting capital allocation and risk appetite.

Regulatory pressure on sovereign debt exposure

Political decisions on national debt and fiscal discipline across Europe directly affect valuation of BNP Paribas’s sovereign bond portfolio, which totalled roughly EUR 150bn on the balance sheet in 2024, exposing the bank to yield-driven mark-to-market moves.

Shifts in political climate can spike bond yields—European 10-year yields rose ~120bp during 2022–24 stress—pressuring CET1, liquidity coverage ratio and funding costs.

Policymakers’ positions on debt restructuring and EU stability tools (EFSF/ESM reforms) are key inputs for BNP Paribas’s multi-year capital planning and stress tests.

- EUR 150bn sovereign holdings (2024)

- 10y Euro area yields +~120bp (2022–24)

- Impact channels: MTM losses, LCR, CET1

Government-led ESG mandates

Political agendas prioritizing a low-carbon transition increase pressure on banks like BNP Paribas to decarbonize portfolios; EU Fit for 55 and France’s 2030/2050 targets push alignment with national climate goals.

Governments are tightening disclosure—EU CSRD expands reporting to ~50,000 firms—and channeling subsidies and guarantees into green financing, boosting public-private green lending pools.

BNP Paribas must revise lending policies to retain public-sector mandates and access to green facilities; the bank disclosed €240bn in sustainable finance commitments by 2025 targets.

- EU CSRD: ~50,000 firms in scope

- BNP Paribas sustainable finance target: €240bn by 2025

- National net-zero laws raise compliance risk and affect public mandates

BNP Paribas: €1.7tn G‑SIB, €17.5bn profit, 12.3% CET1 target, €240bn sustainable finance

BNP Paribas faces ECB SSM oversight as a G-SIB, €1.7tn+ assets; 2024 CET1 guidance 12.3% pro forma to 2025, sovereign holdings ~€150bn; 2024 net income €17.5bn; cross-border revenue ~44% of NBI; non-credit provisions €1.1bn (2024); EMEA/Asia credit growth 2.3%/3.1% (2024); sustainable finance target €240bn by 2025.

| Metric | 2024/Target |

|---|---|

| Assets | €1.7tn+ |

| CET1 (target) | 12.3% pro forma |

| Net income | €17.5bn |

| Sovereigns | €150bn |

| Cross-border NBI | ~44% |

| Sustainable finance | €240bn (2025) |

What is included in the product

Explores how external macro-environmental factors uniquely affect BNP Paribas across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven trends and forward-looking insights to inform risk mitigation and strategic opportunity identification for executives and investors.

Provides a succinct, PESTLE-segmented summary of BNP Paribas’s external environment that can be dropped into presentations or shared across teams for quick alignment and risk discussion.

Economic factors

Interest rate environment and monetary policy

The transition from a high-rate environment (ECB deposit rate peaking at 4.0% in 2023) toward stabilization and gradual easing by late 2025 pressures BNP Paribas net interest margin, which expanded to c.1.25% in 2023 but faces compression as lending yields realign.

Higher rates boosted retail lending income—group net interest income rose c.9% YoY in 2023—but the bank must pivot to fee-based services and wealth management to sustain revenue growth as margins normalize.

The European Central Bank remains the primary driver of BNP Paribas cost of funding and lending profitability; shifts in ECB policy directly affect funding spreads and credit pricing across its euro-area portfolio.

Inflationary trends and operating costs

Persisting inflation—Eurozone CPI at 3.4% in Dec 2025—raises BNP Paribas operating expenses via higher personnel costs (wage inflation ~4% in 2024‑25) and increased IT/cloud spending, squeezing margins.

Reduced consumer purchasing power and weaker corporate capex cut loan demand; European new lending volumes slowed ~2% YoY in 2024, pressuring net interest income.

Elevated service costs and wage growth complicate managing the cost-to-income ratio, which stood around 67% for BNP Paribas in FY 2024, highlighting margin pressure.

Global economic growth and recessionary risks

BNP Paribas’ results closely track GDP in core markets—Eurozone GDP grew 0.5% q/q in Q4 2024 but IMF warned global growth slows to 3.0% in 2025, raising recession risk; downturns push non-performing loans up and forced provisions (bank CET1 ratio pressure).

Currency exchange rate volatility

As a global bank, BNP Paribas is exposed to EUR volatility versus USD, GBP and EM currencies; a 10% EUR appreciation in 2024 would have reduced translated revenues from non-euro operations materially (group reported 2024 net banking income €52.0bn, with ~40% generated outside the euro area).

Exchange swings affect translated earnings, capital ratios and pricing of trade finance; BNP reported FX hedges of €120bn notional at end-2024 to limit P&L volatility.

- 10% EUR move can significantly alter translated revenues (~€20bn non-euro income exposure)

- €120bn hedging notional at end-2024 to mitigate FX impact

- FX volatility affects capital ratios, earnings and trade finance competitiveness

Capital market performance and asset valuations

Capital market health directly affects BNP Paribas; global equity markets rose ~18% in 2023 and remained up ~6% YTD through 2024, boosting AUM and performance fees in Wealth and Asset Management, while 2022–23 bond volatility cut trading volumes and advisory income.

Proprietary portfolios are exposed to valuation swings—BNP reported Group net income sensitivity to market shocks, with trading revenues varying ±20% across high-volatility quarters in 2022–24.

- Higher equities → increased AUM/performance fees

- Bond/volatility spikes → lower trading/advisory income

- Proprietary portfolios sensitive; trading revenues swung ~±20%

ECB peak 4.0% → easing; NII up, margins squeezed, FX & hedges drive revenue volatility

ECB rate peak 4.0% (2023) then easing to 3.0% by late‑2025 compresses NIM (1.25% in 2023); NII rose ~9% in 2023 but lending volumes fell ~2% in 2024; Eurozone CPI 3.4% (Dec 2025) and wage inflation ~4% push costs (cost/income ~67% in 2024); EUR FX moves (10% swing) and €120bn hedges (end‑2024) materially affect translated revenues (2024 NBI €52.0bn, ~40% non‑EUR).

| Metric | Value |

|---|---|

| ECB rate peak | 4.0% (2023) |

| NIM | ~1.25% (2023) |

| Group NBI | €52.0bn (2024) |

| Non‑EUR share | ~40% |

| Hedges notional | €120bn (end‑2024) |

| Cost/Income | ~67% (2024) |

Preview the Actual Deliverable

BNP Paribas PESTLE Analysis

The preview shown here is the exact BNP Paribas PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic or investment work.