Bank of Hawaii Business Model Canvas

Bank of Hawaii Business Model Canvas: Strategic Blueprint & Ready Templates

Unlock the full strategic blueprint behind Bank of Hawaii's business model—this in-depth Business Model Canvas reveals how the bank creates customer value, monetizes products, and leverages partnerships to sustain competitive advantage; ideal for investors, consultants, and executives seeking actionable insights and ready-to-use Word/Excel templates to benchmark or adapt these proven strategies.

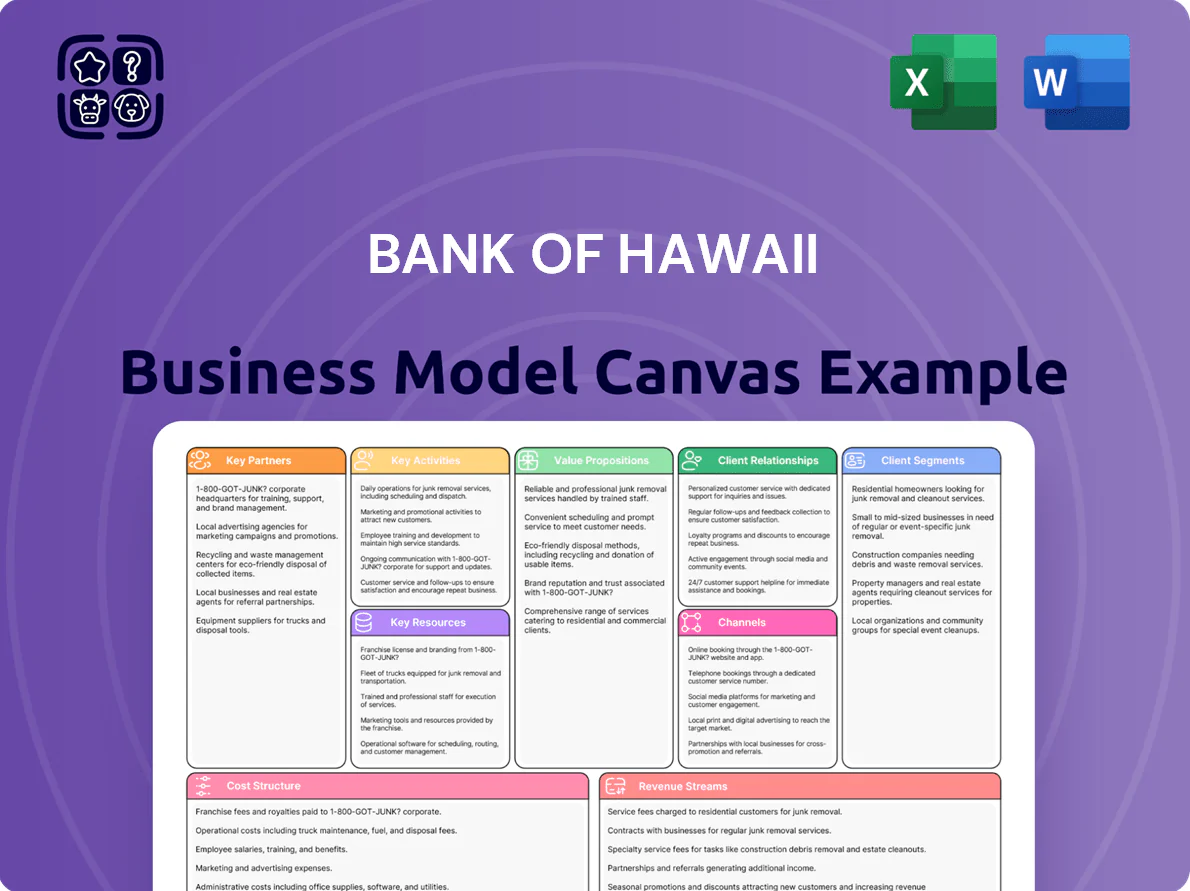

Partnerships

Fintech and Technology Vendors

Fintech and tech vendor partnerships keep Bank of Hawaii’s digital stack competitive with national peers, enabling features like account aggregation and real-time payments; in 2024 the bank cited a 20% rise in mobile users and a 15% cut in digital incident rates after vendor rollouts. By outsourcing specialized cybersecurity and mobile capabilities, the bank stays agile amid 30% annual fintech feature churn.

Global Payment Networks

Long-standing agreements with Visa and Mastercard let Bank of Hawaii issue globally accepted credit and debit cards, supporting ~12,000 merchant locations in Hawai‘i and cross-border use; in 2024 card transactions grew ~8% y/y to $4.2B, giving customers worldwide access to funds.

These partnerships power secure processing, integrated fraud protection (tokenization, AI detection) and digital wallet support (Apple Pay, Google Pay), cutting fraud rates—industry average card fraud ~0.07%—and enabling instant, mobile-first payments.

Regulatory and Government Bodies

Ongoing engagement with the Federal Reserve and Hawaii Division of Financial Institutions keeps Bank of Hawaii compliant with evolving laws and standards, preserving its federal and state charters across Hawaii, Guam, and Saipan; as of 2025 the bank reports a CET1 ratio of 12.1% and regulatory liquidity coverage that aligns with Fed stress tests. These ties also grant access to Fed liquidity facilities and support system stability during market stress.

Secondary Mortgage Market Entities

Partnering with Fannie Mae and Freddie Mac lets Bank of Hawaii sell originated mortgages, freeing capital—$1.2B in agency securities held at end-2024—and sustain new lending to local buyers while reducing long-term interest-rate exposure.

This liquidity channel supports Hawaii homeownership by enabling continued originations despite tight local supply; in 2024 Bank of Hawaii closed roughly 3,800 purchase mortgages backed by agencies.

- Agency sales free capital: $1.2B agency securities (2024)

- Supports ~3,800 purchase loans (2024)

- Mitigates duration risk via guaranteed pipelines

Local Community and Business Organizations

Alliances with non-profits and local chambers boost Bank of Hawaii’s brand and community ties, funding financial literacy programs that reached 12,000+ residents in 2024 and supporting $210M in affordable housing loans across the Pacific in 2024.

These partnerships drive economic development—small-business lending in Hawaii rose 8% YoY in 2024—showing a commitment to island economies that mainland banks rarely match.

- 12,000+ people reached by financial literacy in 2024

- $210M affordable housing loans in 2024

- 8% YoY increase in small-business lending (2024)

BOH partners drive digital growth: +20% mobile, $4.2B card spend, $210M housing

Key partners (fintechs, Visa/Mastercard, Fed, Fannie/Freddie, local NGOs) power BOH’s digital ops, card reach, liquidity, mortgage sales and community lending—2024 highlights: mobile users +20%, card spend $4.2B (+8%), $1.2B agency securities, ~3,800 purchase loans, $210M affordable housing, 12k financial-literacy participants.

| Metric | 2024 |

|---|---|

| Mobile users | +20% |

| Card spend | $4.2B (+8%) |

| Agency securities | $1.2B |

| Purchase loans | ~3,800 |

| Affordable housing | $210M |

| Financial-literacy | 12,000+ |

What is included in the product

A concise, pre-written Business Model Canvas for Bank of Hawaii detailing customer segments, channels, value propositions, key activities, resources, partners, cost structure, and revenue streams with competitive analysis and SWOT-linked insights for presentations, investor discussions, and strategic planning.

Condenses Bank of Hawaii’s lending, treasury, and customer-segmentation strategy into a digestible one-page Business Model Canvas, saving hours of structuring while enabling quick comparison, team collaboration, and board-ready presentations.

Activities

Credit Underwriting and Loan Origination

Bank of Hawaii rigorously assesses borrower creditworthiness to issue mortgages, commercial loans, and lines of credit, using risk models and island-specific market data; loans were 62% of earning assets as of 2025 Q3 and net interest income totaled $432M for 12 months through 2025 Q3. Proper underwriting sustains portfolio quality—BOH reported a 0.28% net charge-off rate in 2024, keeping default risk low.

Deposit and Liquidity Management

Managing intake and maintenance of checking, savings, and time deposits funds Bank of Hawaii’s operations; as of 2024 the bank held about $11.2 billion in deposits, so pricing must balance competitive rates with keeping a low-cost funding mix to protect NIM (net interest margin).

Treasury runs liquidity and cash‑flow models to meet daily transactions and regulatory LCR (liquidity coverage ratio) targets, ensuring available high‑quality liquid assets to cover 30+ days of outflows.

Digital Platform Development and Maintenance

Bank of Hawaii must keep investing in mobile and online platforms to match a tech-savvy base; in 2024, 68% of US consumers used mobile banking, so updates to UX, biometric logins, and added payment rails (e.g., real-time ACH, tokenized cards) cut branch load—BOH reported digital transactions rose ~22% YoY in 2023, lowering routine in-branch traffic and operating costs.

Risk Management and Regulatory Compliance

The bank enforces anti-money laundering (AML) and know-your-customer (KYC) rules—complying with Bank Secrecy Act and FinCEN standards—to block illicit flows and shield the institution; in 2024 US banks reported a 14% rise in SARs (suspicious activity reports), increasing compliance workloads.

Internal audits and risk assessments run quarterly, targeting credit, operational, and compliance gaps; effective programs cut regulatory fines—US banking fines hit $2.1B in 2023—so this activity preserves legal standing and customer trust.

- Quarterly audits and continuous monitoring

- AML/KYC compliance per FinCEN and BSA

- 14% rise in SARs reported in 2024

- US bank fines totaled $2.1B in 2023

Wealth Management and Fiduciary Advisory

Wealth management and fiduciary advisory at Bank of Hawaii diversifies revenue beyond lending—trusted advisory and trust fees made up about 14% of noninterest income in 2024, supporting fee stability amid rate cycles.

Advisors build customized, multi-generational portfolios aligned to clients’ goals and risk tolerances, requiring deep market expertise and long-term relationship management.

- 14% of 2024 noninterest income from advisory/trust fees

- Custom portfolios matched to risk profiles

- Focus on multi-generational client retention

BOH: Loan-Driven NII $432M, $11.2B Deposits, 22% Digital Growth, 14% Wealth Fees

BOH issues and services loans (62% of earning assets; net interest income $432M TTM through 2025 Q3), manages $11.2B deposits (2024), runs treasury for LCR coverage, expands digital banking (digital txns +22% YoY 2023), enforces AML/KYC (SARs +14% 2024), and provides wealth/advisory (14% of 2024 noninterest income).

| Metric | Value |

|---|---|

| Loans % earning assets | 62% |

| NII (TTM) | $432M |

| Deposits (2024) | $11.2B |

| Digital txn growth | +22% YoY 2023 |

| Wealth fees | 14% noninterest |

What You See Is What You Get

Business Model Canvas

The document you're previewing is the actual Bank of Hawaii Business Model Canvas—not a mockup or sample—and it matches the file you'll receive after purchase; upon payment you'll instantly download this same, fully formatted and editable document ready for presentation or further customization.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Bank of Hawaii Business Model Canvas: Strategic Blueprint & Ready Templates

Unlock the full strategic blueprint behind Bank of Hawaii's business model—this in-depth Business Model Canvas reveals how the bank creates customer value, monetizes products, and leverages partnerships to sustain competitive advantage; ideal for investors, consultants, and executives seeking actionable insights and ready-to-use Word/Excel templates to benchmark or adapt these proven strategies.

Partnerships

Fintech and Technology Vendors

Fintech and tech vendor partnerships keep Bank of Hawaii’s digital stack competitive with national peers, enabling features like account aggregation and real-time payments; in 2024 the bank cited a 20% rise in mobile users and a 15% cut in digital incident rates after vendor rollouts. By outsourcing specialized cybersecurity and mobile capabilities, the bank stays agile amid 30% annual fintech feature churn.

Global Payment Networks

Long-standing agreements with Visa and Mastercard let Bank of Hawaii issue globally accepted credit and debit cards, supporting ~12,000 merchant locations in Hawai‘i and cross-border use; in 2024 card transactions grew ~8% y/y to $4.2B, giving customers worldwide access to funds.

These partnerships power secure processing, integrated fraud protection (tokenization, AI detection) and digital wallet support (Apple Pay, Google Pay), cutting fraud rates—industry average card fraud ~0.07%—and enabling instant, mobile-first payments.

Regulatory and Government Bodies

Ongoing engagement with the Federal Reserve and Hawaii Division of Financial Institutions keeps Bank of Hawaii compliant with evolving laws and standards, preserving its federal and state charters across Hawaii, Guam, and Saipan; as of 2025 the bank reports a CET1 ratio of 12.1% and regulatory liquidity coverage that aligns with Fed stress tests. These ties also grant access to Fed liquidity facilities and support system stability during market stress.

Secondary Mortgage Market Entities

Partnering with Fannie Mae and Freddie Mac lets Bank of Hawaii sell originated mortgages, freeing capital—$1.2B in agency securities held at end-2024—and sustain new lending to local buyers while reducing long-term interest-rate exposure.

This liquidity channel supports Hawaii homeownership by enabling continued originations despite tight local supply; in 2024 Bank of Hawaii closed roughly 3,800 purchase mortgages backed by agencies.

- Agency sales free capital: $1.2B agency securities (2024)

- Supports ~3,800 purchase loans (2024)

- Mitigates duration risk via guaranteed pipelines

Local Community and Business Organizations

Alliances with non-profits and local chambers boost Bank of Hawaii’s brand and community ties, funding financial literacy programs that reached 12,000+ residents in 2024 and supporting $210M in affordable housing loans across the Pacific in 2024.

These partnerships drive economic development—small-business lending in Hawaii rose 8% YoY in 2024—showing a commitment to island economies that mainland banks rarely match.

- 12,000+ people reached by financial literacy in 2024

- $210M affordable housing loans in 2024

- 8% YoY increase in small-business lending (2024)

BOH partners drive digital growth: +20% mobile, $4.2B card spend, $210M housing

Key partners (fintechs, Visa/Mastercard, Fed, Fannie/Freddie, local NGOs) power BOH’s digital ops, card reach, liquidity, mortgage sales and community lending—2024 highlights: mobile users +20%, card spend $4.2B (+8%), $1.2B agency securities, ~3,800 purchase loans, $210M affordable housing, 12k financial-literacy participants.

| Metric | 2024 |

|---|---|

| Mobile users | +20% |

| Card spend | $4.2B (+8%) |

| Agency securities | $1.2B |

| Purchase loans | ~3,800 |

| Affordable housing | $210M |

| Financial-literacy | 12,000+ |

What is included in the product

A concise, pre-written Business Model Canvas for Bank of Hawaii detailing customer segments, channels, value propositions, key activities, resources, partners, cost structure, and revenue streams with competitive analysis and SWOT-linked insights for presentations, investor discussions, and strategic planning.

Condenses Bank of Hawaii’s lending, treasury, and customer-segmentation strategy into a digestible one-page Business Model Canvas, saving hours of structuring while enabling quick comparison, team collaboration, and board-ready presentations.

Activities

Credit Underwriting and Loan Origination

Bank of Hawaii rigorously assesses borrower creditworthiness to issue mortgages, commercial loans, and lines of credit, using risk models and island-specific market data; loans were 62% of earning assets as of 2025 Q3 and net interest income totaled $432M for 12 months through 2025 Q3. Proper underwriting sustains portfolio quality—BOH reported a 0.28% net charge-off rate in 2024, keeping default risk low.

Deposit and Liquidity Management

Managing intake and maintenance of checking, savings, and time deposits funds Bank of Hawaii’s operations; as of 2024 the bank held about $11.2 billion in deposits, so pricing must balance competitive rates with keeping a low-cost funding mix to protect NIM (net interest margin).

Treasury runs liquidity and cash‑flow models to meet daily transactions and regulatory LCR (liquidity coverage ratio) targets, ensuring available high‑quality liquid assets to cover 30+ days of outflows.

Digital Platform Development and Maintenance

Bank of Hawaii must keep investing in mobile and online platforms to match a tech-savvy base; in 2024, 68% of US consumers used mobile banking, so updates to UX, biometric logins, and added payment rails (e.g., real-time ACH, tokenized cards) cut branch load—BOH reported digital transactions rose ~22% YoY in 2023, lowering routine in-branch traffic and operating costs.

Risk Management and Regulatory Compliance

The bank enforces anti-money laundering (AML) and know-your-customer (KYC) rules—complying with Bank Secrecy Act and FinCEN standards—to block illicit flows and shield the institution; in 2024 US banks reported a 14% rise in SARs (suspicious activity reports), increasing compliance workloads.

Internal audits and risk assessments run quarterly, targeting credit, operational, and compliance gaps; effective programs cut regulatory fines—US banking fines hit $2.1B in 2023—so this activity preserves legal standing and customer trust.

- Quarterly audits and continuous monitoring

- AML/KYC compliance per FinCEN and BSA

- 14% rise in SARs reported in 2024

- US bank fines totaled $2.1B in 2023

Wealth Management and Fiduciary Advisory

Wealth management and fiduciary advisory at Bank of Hawaii diversifies revenue beyond lending—trusted advisory and trust fees made up about 14% of noninterest income in 2024, supporting fee stability amid rate cycles.

Advisors build customized, multi-generational portfolios aligned to clients’ goals and risk tolerances, requiring deep market expertise and long-term relationship management.

- 14% of 2024 noninterest income from advisory/trust fees

- Custom portfolios matched to risk profiles

- Focus on multi-generational client retention

BOH: Loan-Driven NII $432M, $11.2B Deposits, 22% Digital Growth, 14% Wealth Fees

BOH issues and services loans (62% of earning assets; net interest income $432M TTM through 2025 Q3), manages $11.2B deposits (2024), runs treasury for LCR coverage, expands digital banking (digital txns +22% YoY 2023), enforces AML/KYC (SARs +14% 2024), and provides wealth/advisory (14% of 2024 noninterest income).

| Metric | Value |

|---|---|

| Loans % earning assets | 62% |

| NII (TTM) | $432M |

| Deposits (2024) | $11.2B |

| Digital txn growth | +22% YoY 2023 |

| Wealth fees | 14% noninterest |

What You See Is What You Get

Business Model Canvas

The document you're previewing is the actual Bank of Hawaii Business Model Canvas—not a mockup or sample—and it matches the file you'll receive after purchase; upon payment you'll instantly download this same, fully formatted and editable document ready for presentation or further customization.