Booking Holdings PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Unlock strategic advantage with our PESTLE Analysis of Booking Holdings—concise, data-driven insights into political, economic, social, technological, legal, and environmental forces shaping its future; purchase the full report to access the complete breakdown, ready-to-use for investment decisions, competitive strategy, or boardroom briefings.

Political factors

Geopolitical instability in key regions

Ongoing conflicts in Eastern Europe and the Middle East in late 2025 have cut travel to affected corridors by roughly 18% year‑over‑year, eroding consumer confidence; Booking Holdings faces shifting safety advisories and sanctions that complicate operations in these markets.

These tensions cause abrupt demand swings—monthly bookings volatility rose ~22% in 2024–25—forcing Booking to maintain flexible cancellation policies and absorb higher refund and rebooking costs to protect brand trust.

Evolution of international trade relations

Trade tensions between the US and China have suppressed cross-border travel, with global international tourist arrivals down 14% YoY in 2024 in key Asia–Pacific corridors; stricter diplomacy-driven visa rules and episodic bans cut bookings on platforms like Booking.com and Agoda, contributing to a 3% FX-adjusted revenue headwind in 2024 for Booking Holdings from APAC—management shifts marketing spend toward stable/fast-recovering corridors such as Europe and Latin America.

Nationalistic tourism policies

Several countries tightened nationalistic tourism policies post-2020 to boost domestic spend, with domestic travel accounting for about 70% of global tourism receipts in 2023 per UNWTO trends; this shifts Booking Holdings to reallocate marketing budgets toward regional campaigns and tailor inventory for shorter, local stays. Government grants and "undiscovered destination" programs—e.g., EU regional tourism funds of €3.5bn in 2024—create partnership opportunities to onboard new properties and grow local supply.

Government-driven digital sovereignty

Governments increasingly mandate data localization; over 100 countries had data residency laws by 2024, raising compliance costs for Booking Holdings, which reported $12.6B revenue in 2024 and must balance localized data centers against margins.

Booking faces political pressure to store traveler data within borders—noncompliance risks fines or market access bans in strict jurisdictions like China, India and EU members enforcing GDPR-related restrictions.

Navigating sovereignty rules is critical to prevent operational shutdowns and protect 2024 EBITDA levels amid rising IT CAPEX for localized infrastructure.

- 100+ countries with localization laws (2024)

- $12.6B Booking Holdings revenue (2024)

- Increased IT CAPEX and compliance risk in China, India, EU

Visa and border control fluctuations

Political shifts expanding visa-free travel and digital nomad visas increase trip frequency and length, boosting Booking Holdings which generated $17.1B gross travel bookings in 2023 and saw OTA demand rebound 26% YoY in 2024.

Conversely, rising protectionism or stricter border controls can reduce international stays and curb Booking’s global growth, risking downward pressure on bookings and revenue per night.

- Visa liberalization → higher trip frequency, longer stays

- Digital nomad visas → more long-term bookings

- Isolationism → fewer cross-border bookings, revenue risk

Travel rebound (+26%) vs geopolitics, $12.6B revenue hit amid data laws & 22% booking volatility

Geopolitical conflicts and US–China tensions cut travel and raised booking volatility (~22% in 2024–25), pressuring cancellations/refunds; 100+ data localization laws (2024) and GDPR risk raise IT CAPEX, impacting 2024 revenue $12.6B; visa liberalization and digital nomad visas boost demand (OTA rebound +26% YoY 2024), while protectionism threatens cross-border bookings.

| Metric | Value |

|---|---|

| Revenue (2024) | $12.6B |

| Gross bookings (2023) | $17.1B |

| Booking volatility | ~22% |

| OTA rebound (2024) | +26% YoY |

| Countries with localization laws (2024) | 100+ |

What is included in the product

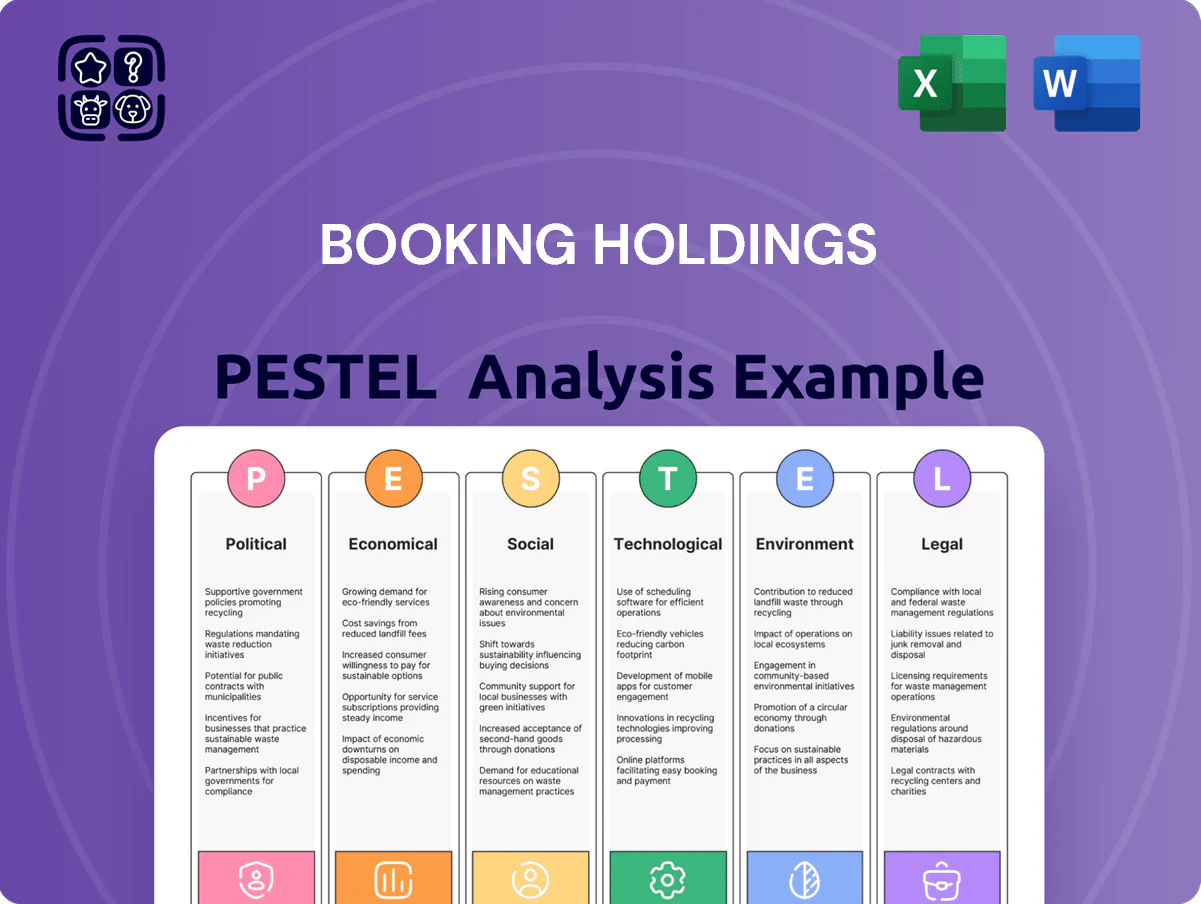

Explores how external macro-environmental factors uniquely affect Booking Holdings across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify threats and opportunities for executives, consultants, and entrepreneurs.

A concise, visually segmented PESTLE snapshot tailored for Booking Holdings that clearly highlights regulatory, economic, and technological risks and opportunities, making it easy to drop into presentations, share across teams, and annotate with region-specific notes during strategic planning.

Economic factors

Global inflationary pressures

Persistent global inflation in services—U.S. CPI shelter and airfare components up ~4–6% year over year in 2024–25—has pushed average hotel and airfare prices higher, risking reduced demand for luxury travel segments. Booking Holdings offsets this via its portfolio, using Priceline and value offerings to capture price-sensitive travelers; Priceline saw room-night growth of low-cost bookings rise ~8% in 2024. The company faces margin pressure as operating expenses climb, needing to balance cost recovery with competitive pricing to defend share versus budget-focused rivals.

Foreign exchange rate volatility

Reporting in USD while booking volumes are heavily earned in EUR, GBP and other currencies makes Booking Holdings highly exposed to forex volatility; in 2024 roughly 35% of gross bookings were from Europe, amplifying USD/EUR and USD/GBP swings on reported revenue.

Large currency moves alter the local-currency price of travel, affecting demand and cross-border booking patterns and can compress net margins when translated into USD.

Booking uses dynamic pricing and a portfolio of forward contracts and options; in 2023 it reported foreign-currency losses/gains of about $120 million related to transactional and translational effects, illustrating active hedging to stabilize consolidated results.

Interest rate environment impacts

By late 2025, global policy rates remained elevated—US Fed funds near 5.25–5.50%—raising Booking Holdings’ cost of capital, constraining large acquisitions and share buybacks; the company held about $6.5bn net cash (Q3 2025) but investors still watch leverage ratios and free cash flow conversion closely.

Emerging market growth potential

Rapid GDP growth in Southeast Asia (projected 4.7% in 2025) and Latin America (around 2.5% in 2025) fuels a swelling middle class and rising travel spend; UNWTO data show intra-regional travel recovering to ~85% of 2019 levels by 2024.

Booking Holdings is increasing investments and localized offerings—EMEA and APAC platforms grew international room nights ~18% YoY in 2024—aiming to lock brand loyalty among first-time international travelers.

These high-growth regions act as a strategic hedge versus stagnating North American/European markets, where revenue growth slowed to mid-single digits in 2024 for major OTAs.

- SE Asia GDP ~4.7% (2025 proj); LatAm ~2.5% (2025 proj)

- UNWTO: intra-regional travel ~85% of 2019 levels (2024)

- Booking: international room nights in growth markets +18% YoY (2024)

- NA/EU OTA revenue growth mid-single digits (2024)

Consumer discretionary spending shifts

Economic cycles shift consumers between travel and other discretionary buys; during downturns travel can be deferred in favor of essentials, while in expansions spending on experiences rises. By end-2025 the global move toward experience over things persisted, with 2024 US leisure travel spending up 7% YoY and OTA bookings recovering to 2019+ levels. Booking Holdings leverages transaction and search-data analytics to reprice promotions in real time and target segments with 1Q–4Q dynamic campaigns.

- Leisure spend +7% YoY (US, 2024)

- OTA bookings ~2019 levels by 2024–25

- Real-time analytics drive dynamic promotions

Inflation, FX and rates test travel margins as international demand surges

Inflation-driven price rises (US shelter/airfare +4–6% in 2024–25) pressure demand and margins; Priceline low-cost room nights +8% (2024). FX exposure: ~35% gross bookings Europe; 2023 FX P/L ≈ $120m. Elevated rates (Fed 5.25–5.50% 2025) raise cost of capital; net cash ≈ $6.5bn (Q3 2025). EM growth: SE Asia GDP ~4.7% (2025), LatAm ~2.5%; intl room nights +18% YoY (2024).

| Metric | Value |

|---|---|

| US shelter/airfare inflation | +4–6% |

| Priceline low-cost room nights | +8% (2024) |

| Europe share | ~35% gross bookings |

| FX P/L | $120m (2023) |

| Net cash | $6.5bn (Q3 2025) |

| SE Asia GDP | 4.7% (2025) |

| Intl room nights growth | +18% YoY (2024) |

Same Document Delivered

Booking Holdings PESTLE Analysis

The preview shown here is the exact Booking Holdings PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

The content, layout, and insights visible in this sample are identical to the final downloadable file delivered immediately after payment.

No placeholders or teasers—what you see is the finished document, complete with political, economic, social, technological, legal, and environmental analysis.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Unlock strategic advantage with our PESTLE Analysis of Booking Holdings—concise, data-driven insights into political, economic, social, technological, legal, and environmental forces shaping its future; purchase the full report to access the complete breakdown, ready-to-use for investment decisions, competitive strategy, or boardroom briefings.

Political factors

Geopolitical instability in key regions

Ongoing conflicts in Eastern Europe and the Middle East in late 2025 have cut travel to affected corridors by roughly 18% year‑over‑year, eroding consumer confidence; Booking Holdings faces shifting safety advisories and sanctions that complicate operations in these markets.

These tensions cause abrupt demand swings—monthly bookings volatility rose ~22% in 2024–25—forcing Booking to maintain flexible cancellation policies and absorb higher refund and rebooking costs to protect brand trust.

Evolution of international trade relations

Trade tensions between the US and China have suppressed cross-border travel, with global international tourist arrivals down 14% YoY in 2024 in key Asia–Pacific corridors; stricter diplomacy-driven visa rules and episodic bans cut bookings on platforms like Booking.com and Agoda, contributing to a 3% FX-adjusted revenue headwind in 2024 for Booking Holdings from APAC—management shifts marketing spend toward stable/fast-recovering corridors such as Europe and Latin America.

Nationalistic tourism policies

Several countries tightened nationalistic tourism policies post-2020 to boost domestic spend, with domestic travel accounting for about 70% of global tourism receipts in 2023 per UNWTO trends; this shifts Booking Holdings to reallocate marketing budgets toward regional campaigns and tailor inventory for shorter, local stays. Government grants and "undiscovered destination" programs—e.g., EU regional tourism funds of €3.5bn in 2024—create partnership opportunities to onboard new properties and grow local supply.

Government-driven digital sovereignty

Governments increasingly mandate data localization; over 100 countries had data residency laws by 2024, raising compliance costs for Booking Holdings, which reported $12.6B revenue in 2024 and must balance localized data centers against margins.

Booking faces political pressure to store traveler data within borders—noncompliance risks fines or market access bans in strict jurisdictions like China, India and EU members enforcing GDPR-related restrictions.

Navigating sovereignty rules is critical to prevent operational shutdowns and protect 2024 EBITDA levels amid rising IT CAPEX for localized infrastructure.

- 100+ countries with localization laws (2024)

- $12.6B Booking Holdings revenue (2024)

- Increased IT CAPEX and compliance risk in China, India, EU

Visa and border control fluctuations

Political shifts expanding visa-free travel and digital nomad visas increase trip frequency and length, boosting Booking Holdings which generated $17.1B gross travel bookings in 2023 and saw OTA demand rebound 26% YoY in 2024.

Conversely, rising protectionism or stricter border controls can reduce international stays and curb Booking’s global growth, risking downward pressure on bookings and revenue per night.

- Visa liberalization → higher trip frequency, longer stays

- Digital nomad visas → more long-term bookings

- Isolationism → fewer cross-border bookings, revenue risk

Travel rebound (+26%) vs geopolitics, $12.6B revenue hit amid data laws & 22% booking volatility

Geopolitical conflicts and US–China tensions cut travel and raised booking volatility (~22% in 2024–25), pressuring cancellations/refunds; 100+ data localization laws (2024) and GDPR risk raise IT CAPEX, impacting 2024 revenue $12.6B; visa liberalization and digital nomad visas boost demand (OTA rebound +26% YoY 2024), while protectionism threatens cross-border bookings.

| Metric | Value |

|---|---|

| Revenue (2024) | $12.6B |

| Gross bookings (2023) | $17.1B |

| Booking volatility | ~22% |

| OTA rebound (2024) | +26% YoY |

| Countries with localization laws (2024) | 100+ |

What is included in the product

Explores how external macro-environmental factors uniquely affect Booking Holdings across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify threats and opportunities for executives, consultants, and entrepreneurs.

A concise, visually segmented PESTLE snapshot tailored for Booking Holdings that clearly highlights regulatory, economic, and technological risks and opportunities, making it easy to drop into presentations, share across teams, and annotate with region-specific notes during strategic planning.

Economic factors

Global inflationary pressures

Persistent global inflation in services—U.S. CPI shelter and airfare components up ~4–6% year over year in 2024–25—has pushed average hotel and airfare prices higher, risking reduced demand for luxury travel segments. Booking Holdings offsets this via its portfolio, using Priceline and value offerings to capture price-sensitive travelers; Priceline saw room-night growth of low-cost bookings rise ~8% in 2024. The company faces margin pressure as operating expenses climb, needing to balance cost recovery with competitive pricing to defend share versus budget-focused rivals.

Foreign exchange rate volatility

Reporting in USD while booking volumes are heavily earned in EUR, GBP and other currencies makes Booking Holdings highly exposed to forex volatility; in 2024 roughly 35% of gross bookings were from Europe, amplifying USD/EUR and USD/GBP swings on reported revenue.

Large currency moves alter the local-currency price of travel, affecting demand and cross-border booking patterns and can compress net margins when translated into USD.

Booking uses dynamic pricing and a portfolio of forward contracts and options; in 2023 it reported foreign-currency losses/gains of about $120 million related to transactional and translational effects, illustrating active hedging to stabilize consolidated results.

Interest rate environment impacts

By late 2025, global policy rates remained elevated—US Fed funds near 5.25–5.50%—raising Booking Holdings’ cost of capital, constraining large acquisitions and share buybacks; the company held about $6.5bn net cash (Q3 2025) but investors still watch leverage ratios and free cash flow conversion closely.

Emerging market growth potential

Rapid GDP growth in Southeast Asia (projected 4.7% in 2025) and Latin America (around 2.5% in 2025) fuels a swelling middle class and rising travel spend; UNWTO data show intra-regional travel recovering to ~85% of 2019 levels by 2024.

Booking Holdings is increasing investments and localized offerings—EMEA and APAC platforms grew international room nights ~18% YoY in 2024—aiming to lock brand loyalty among first-time international travelers.

These high-growth regions act as a strategic hedge versus stagnating North American/European markets, where revenue growth slowed to mid-single digits in 2024 for major OTAs.

- SE Asia GDP ~4.7% (2025 proj); LatAm ~2.5% (2025 proj)

- UNWTO: intra-regional travel ~85% of 2019 levels (2024)

- Booking: international room nights in growth markets +18% YoY (2024)

- NA/EU OTA revenue growth mid-single digits (2024)

Consumer discretionary spending shifts

Economic cycles shift consumers between travel and other discretionary buys; during downturns travel can be deferred in favor of essentials, while in expansions spending on experiences rises. By end-2025 the global move toward experience over things persisted, with 2024 US leisure travel spending up 7% YoY and OTA bookings recovering to 2019+ levels. Booking Holdings leverages transaction and search-data analytics to reprice promotions in real time and target segments with 1Q–4Q dynamic campaigns.

- Leisure spend +7% YoY (US, 2024)

- OTA bookings ~2019 levels by 2024–25

- Real-time analytics drive dynamic promotions

Inflation, FX and rates test travel margins as international demand surges

Inflation-driven price rises (US shelter/airfare +4–6% in 2024–25) pressure demand and margins; Priceline low-cost room nights +8% (2024). FX exposure: ~35% gross bookings Europe; 2023 FX P/L ≈ $120m. Elevated rates (Fed 5.25–5.50% 2025) raise cost of capital; net cash ≈ $6.5bn (Q3 2025). EM growth: SE Asia GDP ~4.7% (2025), LatAm ~2.5%; intl room nights +18% YoY (2024).

| Metric | Value |

|---|---|

| US shelter/airfare inflation | +4–6% |

| Priceline low-cost room nights | +8% (2024) |

| Europe share | ~35% gross bookings |

| FX P/L | $120m (2023) |

| Net cash | $6.5bn (Q3 2025) |

| SE Asia GDP | 4.7% (2025) |

| Intl room nights growth | +18% YoY (2024) |

Same Document Delivered

Booking Holdings PESTLE Analysis

The preview shown here is the exact Booking Holdings PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

The content, layout, and insights visible in this sample are identical to the final downloadable file delivered immediately after payment.

No placeholders or teasers—what you see is the finished document, complete with political, economic, social, technological, legal, and environmental analysis.