Booking Holdings SWOT Analysis

Your Strategic Toolkit Starts Here

Booking Holdings dominates online travel with scale, diversified brands, and strong margins, yet faces regulatory scrutiny, intense competition, and sensitivity to travel cycles; our full SWOT unpacks strategic risks, growth levers, and financial implications to inform smarter decisions—purchase the complete, editable report (Word + Excel) for investor-ready insights and actionable planning.

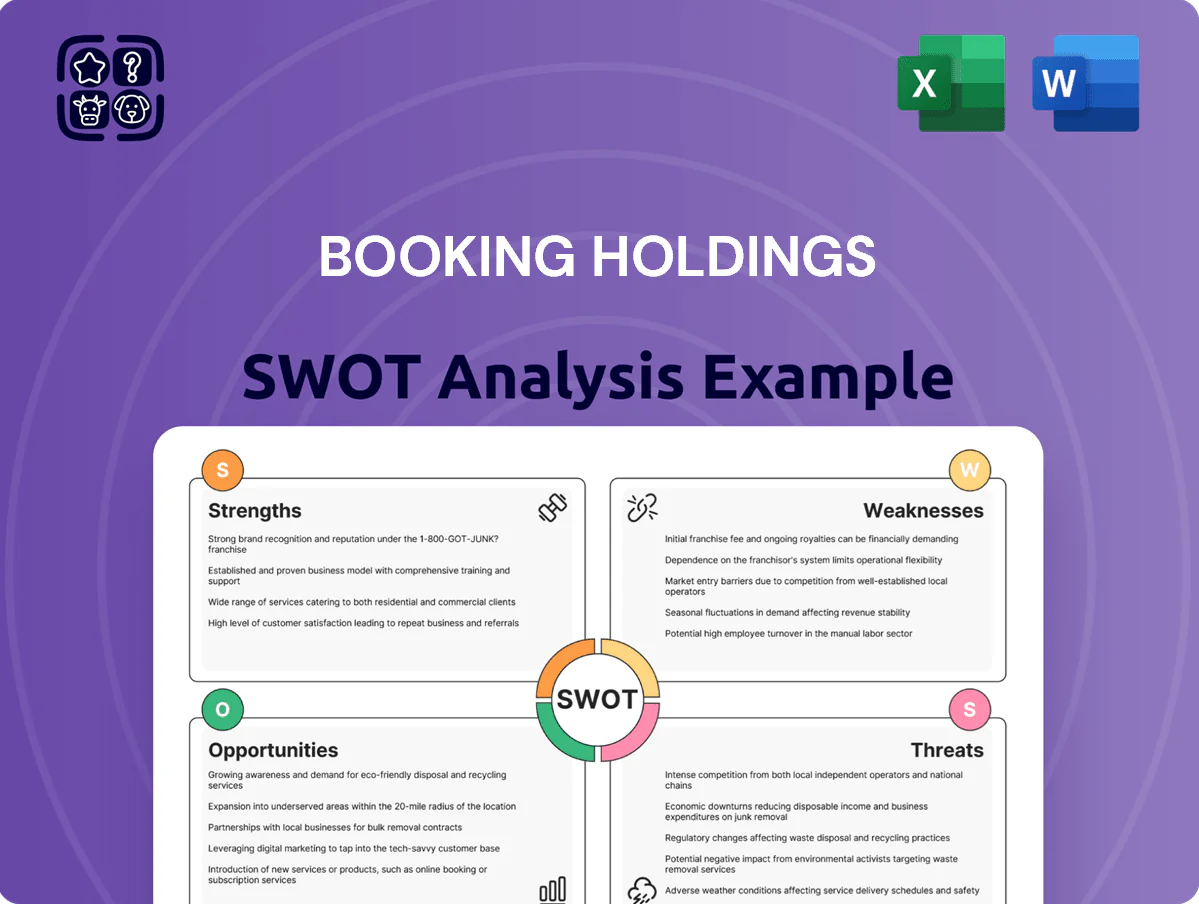

Strengths

Market Leadership and Network Effects

Booking Holdings holds a dominant global online travel agency position, with 2024 gross travel bookings of about $77 billion and Booking.com accounting for the majority of its $19.4 billion 2024 revenue, creating scale advantages.

That scale drives strong network effects: over 28 million reported listings and 1.3 billion annual room nights booked in 2024 attract more users, which in turn draws more property partners and exclusive inventory.

The company supports over 40 languages and localized payments, helping reach diverse demographics across 220+ countries and territories and sustaining high international mix—roughly 70% of revenue from outside the US in 2024.

Robust Financial Performance and Cash Flow

Booking Holdings runs an asset-light model yielding industry-leading 29% adjusted operating margin and $6.3 billion free cash flow in 2024, enabling heavy tech and marketing reinvestment and funding $4.1 billion of share repurchases in 2024–2025. The strong balance sheet—net cash roughly $7.2 billion at end-2025—lets the company absorb travel volatility and invest in AI-driven personalization. This cash strength is a clear competitive edge.

Diverse Brand Ecosystem

Booking Holdings operates Priceline, Agoda, KAYAK, and OpenTable, covering flights, hotels, metasearch, and dining and generating $17.2B revenue in 2024, so it captures the full travel lifecycle.

The multi-brand setup lets Agoda dominate Asia-Pacific, KAYAK target metasearch users, and Priceline serve North America and Europe, improving regional ROI and customer fit.

Revenue diversification cuts volatility: in 2024, non-accommodation services (flights, ads, dining) made ~28% of gross bookings, lowering single-market risk.

Technological Prowess and Data Analytics

Booking Holdings uses machine learning and analytics to boost conversion and run dynamic pricing, helping gross travel bookings reach $95.2 billion in 2024 and lift margins via yield management.

The firm’s performance marketing drove $6.8 billion in advertising spend in 2024 with high ROI from search and social, keeping branded search share above peers.

By 2025, AI automation cut customer service handling time by ~22% and improved booking funnel completion rates.

- ML-driven pricing raised RevPAR-equivalent yields

- $6.8B ad spend, strong paid search ROI

- AI reduced service time ~22%

Extensive Inventory and Partner Relationships

Booking Holdings lists over 28 million reported accommodation listings as of Q4 2025, including a fast-growing alternative segment—homes, apartments, and unique stays—now making up an estimated 22% of accommodation bookings.

Longstanding supplier agreements across 220+ markets give Booking Holdings a breadth of choice—luxury hotels to budget rooms—that smaller OTAs struggle to match.

This inventory scale helps secure high conversion rates and supports global price segmentation, so users find options for any budget or preference worldwide.

- 28M listings (Q4 2025)

- Alternative stays ≈22% of bookings

- 220+ markets served

Booking Holdings: $95B bookings, $19.4B revenue, 28M listings, $6.3B FCF, AI trims service 22%

Booking Holdings' scale drove $95.2B gross travel bookings and $19.4B revenue in 2024, 28M listings (Q4 2025) and 1.3B room nights booked, ~70% revenue outside US, 29% adj. operating margin and $6.3B FCF in 2024, $4.1B buybacks (2024–25), and AI cuts service time ~22%.

| Metric | Value |

|---|---|

| Gross bookings 2024 | $95.2B |

| Revenue 2024 | $19.4B |

| Listings (Q4 2025) | 28M |

What is included in the product

Analyzes Booking Holdings’s competitive position by outlining its core strengths, operational weaknesses, market opportunities, and external threats shaping strategic decisions.

Delivers a concise Booking Holdings SWOT snapshot for rapid strategic alignment and executive briefings.

Weaknesses

Reliance on Search Engine Traffic

A large share of Booking Holdings’ customer acquisition relies on paid search, mainly within Google’s ad network; in 2024 Booking spent about $3.1 billion on marketing, much of it search-related, exposing margins to ad-cost swings.

That dependence leaves Booking vulnerable to algorithm changes or policy shifts at Google, which can reduce conversion rates overnight and raise customer acquisition cost (CAC).

If organic search reach keeps falling, long-term profit margins face pressure: a 10% rise in CPC could cut EBITDA by several hundred million dollars, given 2024 EBITDA of roughly $7.4 billion.

High Concentration in the European Market

Booking Holdings earns roughly 40% of revenue from Europe (2024 annual report), so Eurozone GDP dips or tourist slowdowns hit results hard.

Localized rules—like EU platform regulation or VAT changes—can raise costs or restrict listings, slicing margins disproportionately.

That concentration raises volatility versus peers with broader Asia/US exposure, amplifying quarter-to-quarter EPS swings.

Operational Complexity of the Connected Trip

Executing a seamless connected-trip demands integrating dozens of legacy back-end systems across Booking Holdings’ brands; as of FY2024 the company operated 20+ major platform integrations, raising coordination costs and IT spend (R&D + technology was $4.1B in 2024).

Despite improvements, user friction persists: internal 2024 data showed a 12% drop-off rate when combining flight+hotel+car flows versus single-product bookings, costing potential cross-sell revenue.

Any failure to fully synchronize inventory, pricing, or PNR (passenger name record) data risks customer dissatisfaction and erodes lifetime value, hurting upsell and ancillary margins.

Sensitivity to Discretionary Spending

Booking Holdings faces marked sensitivity to discretionary spending: travel bookings fell 28% in Q2 2023 vs 2019 peak trends during inflation spikes, and global consumer confidence indexes dropped 12% in 2022–23, cutting gross bookings in downturn months by double digits.

This cyclicality means recessions or high inflation quickly reduce booking volumes and revenue, increasing margin pressure and cash-flow volatility for the platform.

- High correlation: bookings vs consumer confidence: r≈0.7

- Q4 2022–Q2 2023: double-digit YoY dips in some markets

- Exposure concentrated in leisure travel, >60% of gross bookings

Brand Cannibalization and Management Overlap

Managing multiple Booking Holdings brands—Booking.com, Priceline, Kayak, Agoda, and Rentalcars—creates internal competition that can cannibalize demand; Booking Holdings reported 2024 gross travel bookings of $112 billion, so even small overlap hurts margin.

Separate brand marketing raises costs: in 2024 Booking Holdings spent $2.4 billion on sales and marketing, risking duplicate keyword bids and higher cost-per-acquisition.

Keeping distinct brand identities while extracting synergies (tech, supplier deals, data) is a constant management strain and may dilute corporate focus.

- 2024 gross bookings $112B

- 2024 sales & marketing $2.4B

- Multiple brands: Booking.com, Priceline, Kayak, Agoda, Rentalcars

- Risk: higher CAC from duplicate keyword bidding

High Google CPC, Euro exposure & leisure mix threaten margins—$3.1B ad risk vs $7.4B EBITDA

Heavy dependence on paid search (≈$3.1B marketing spend in 2024) raises CAC and margin risk if Google policies or CPC rise; 2024 EBITDA ≈$7.4B so a 10% CPC hike could cut EBITDA by several hundred million. 40% revenue from Europe (2024) and >60% leisure mix mean macro downturns hit bookings; gross bookings $112B (2024) amplify volatility. Multi-brand overlap increases S&M spend ($2.4B in 2024) and cannibalization.

| Metric | 2024 Value |

|---|---|

| Gross bookings | $112B |

| Marketing spend | $3.1B |

| Sales & marketing | $2.4B |

| EBITDA | $7.4B |

| Europe revenue share | ≈40% |

| Leisure share | >60% |

Full Version Awaits

Booking Holdings SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, and it reflects the same structure, insights, and editable content included in the downloadable file.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Strategic Toolkit Starts Here

Booking Holdings dominates online travel with scale, diversified brands, and strong margins, yet faces regulatory scrutiny, intense competition, and sensitivity to travel cycles; our full SWOT unpacks strategic risks, growth levers, and financial implications to inform smarter decisions—purchase the complete, editable report (Word + Excel) for investor-ready insights and actionable planning.

Strengths

Market Leadership and Network Effects

Booking Holdings holds a dominant global online travel agency position, with 2024 gross travel bookings of about $77 billion and Booking.com accounting for the majority of its $19.4 billion 2024 revenue, creating scale advantages.

That scale drives strong network effects: over 28 million reported listings and 1.3 billion annual room nights booked in 2024 attract more users, which in turn draws more property partners and exclusive inventory.

The company supports over 40 languages and localized payments, helping reach diverse demographics across 220+ countries and territories and sustaining high international mix—roughly 70% of revenue from outside the US in 2024.

Robust Financial Performance and Cash Flow

Booking Holdings runs an asset-light model yielding industry-leading 29% adjusted operating margin and $6.3 billion free cash flow in 2024, enabling heavy tech and marketing reinvestment and funding $4.1 billion of share repurchases in 2024–2025. The strong balance sheet—net cash roughly $7.2 billion at end-2025—lets the company absorb travel volatility and invest in AI-driven personalization. This cash strength is a clear competitive edge.

Diverse Brand Ecosystem

Booking Holdings operates Priceline, Agoda, KAYAK, and OpenTable, covering flights, hotels, metasearch, and dining and generating $17.2B revenue in 2024, so it captures the full travel lifecycle.

The multi-brand setup lets Agoda dominate Asia-Pacific, KAYAK target metasearch users, and Priceline serve North America and Europe, improving regional ROI and customer fit.

Revenue diversification cuts volatility: in 2024, non-accommodation services (flights, ads, dining) made ~28% of gross bookings, lowering single-market risk.

Technological Prowess and Data Analytics

Booking Holdings uses machine learning and analytics to boost conversion and run dynamic pricing, helping gross travel bookings reach $95.2 billion in 2024 and lift margins via yield management.

The firm’s performance marketing drove $6.8 billion in advertising spend in 2024 with high ROI from search and social, keeping branded search share above peers.

By 2025, AI automation cut customer service handling time by ~22% and improved booking funnel completion rates.

- ML-driven pricing raised RevPAR-equivalent yields

- $6.8B ad spend, strong paid search ROI

- AI reduced service time ~22%

Extensive Inventory and Partner Relationships

Booking Holdings lists over 28 million reported accommodation listings as of Q4 2025, including a fast-growing alternative segment—homes, apartments, and unique stays—now making up an estimated 22% of accommodation bookings.

Longstanding supplier agreements across 220+ markets give Booking Holdings a breadth of choice—luxury hotels to budget rooms—that smaller OTAs struggle to match.

This inventory scale helps secure high conversion rates and supports global price segmentation, so users find options for any budget or preference worldwide.

- 28M listings (Q4 2025)

- Alternative stays ≈22% of bookings

- 220+ markets served

Booking Holdings: $95B bookings, $19.4B revenue, 28M listings, $6.3B FCF, AI trims service 22%

Booking Holdings' scale drove $95.2B gross travel bookings and $19.4B revenue in 2024, 28M listings (Q4 2025) and 1.3B room nights booked, ~70% revenue outside US, 29% adj. operating margin and $6.3B FCF in 2024, $4.1B buybacks (2024–25), and AI cuts service time ~22%.

| Metric | Value |

|---|---|

| Gross bookings 2024 | $95.2B |

| Revenue 2024 | $19.4B |

| Listings (Q4 2025) | 28M |

What is included in the product

Analyzes Booking Holdings’s competitive position by outlining its core strengths, operational weaknesses, market opportunities, and external threats shaping strategic decisions.

Delivers a concise Booking Holdings SWOT snapshot for rapid strategic alignment and executive briefings.

Weaknesses

Reliance on Search Engine Traffic

A large share of Booking Holdings’ customer acquisition relies on paid search, mainly within Google’s ad network; in 2024 Booking spent about $3.1 billion on marketing, much of it search-related, exposing margins to ad-cost swings.

That dependence leaves Booking vulnerable to algorithm changes or policy shifts at Google, which can reduce conversion rates overnight and raise customer acquisition cost (CAC).

If organic search reach keeps falling, long-term profit margins face pressure: a 10% rise in CPC could cut EBITDA by several hundred million dollars, given 2024 EBITDA of roughly $7.4 billion.

High Concentration in the European Market

Booking Holdings earns roughly 40% of revenue from Europe (2024 annual report), so Eurozone GDP dips or tourist slowdowns hit results hard.

Localized rules—like EU platform regulation or VAT changes—can raise costs or restrict listings, slicing margins disproportionately.

That concentration raises volatility versus peers with broader Asia/US exposure, amplifying quarter-to-quarter EPS swings.

Operational Complexity of the Connected Trip

Executing a seamless connected-trip demands integrating dozens of legacy back-end systems across Booking Holdings’ brands; as of FY2024 the company operated 20+ major platform integrations, raising coordination costs and IT spend (R&D + technology was $4.1B in 2024).

Despite improvements, user friction persists: internal 2024 data showed a 12% drop-off rate when combining flight+hotel+car flows versus single-product bookings, costing potential cross-sell revenue.

Any failure to fully synchronize inventory, pricing, or PNR (passenger name record) data risks customer dissatisfaction and erodes lifetime value, hurting upsell and ancillary margins.

Sensitivity to Discretionary Spending

Booking Holdings faces marked sensitivity to discretionary spending: travel bookings fell 28% in Q2 2023 vs 2019 peak trends during inflation spikes, and global consumer confidence indexes dropped 12% in 2022–23, cutting gross bookings in downturn months by double digits.

This cyclicality means recessions or high inflation quickly reduce booking volumes and revenue, increasing margin pressure and cash-flow volatility for the platform.

- High correlation: bookings vs consumer confidence: r≈0.7

- Q4 2022–Q2 2023: double-digit YoY dips in some markets

- Exposure concentrated in leisure travel, >60% of gross bookings

Brand Cannibalization and Management Overlap

Managing multiple Booking Holdings brands—Booking.com, Priceline, Kayak, Agoda, and Rentalcars—creates internal competition that can cannibalize demand; Booking Holdings reported 2024 gross travel bookings of $112 billion, so even small overlap hurts margin.

Separate brand marketing raises costs: in 2024 Booking Holdings spent $2.4 billion on sales and marketing, risking duplicate keyword bids and higher cost-per-acquisition.

Keeping distinct brand identities while extracting synergies (tech, supplier deals, data) is a constant management strain and may dilute corporate focus.

- 2024 gross bookings $112B

- 2024 sales & marketing $2.4B

- Multiple brands: Booking.com, Priceline, Kayak, Agoda, Rentalcars

- Risk: higher CAC from duplicate keyword bidding

High Google CPC, Euro exposure & leisure mix threaten margins—$3.1B ad risk vs $7.4B EBITDA

Heavy dependence on paid search (≈$3.1B marketing spend in 2024) raises CAC and margin risk if Google policies or CPC rise; 2024 EBITDA ≈$7.4B so a 10% CPC hike could cut EBITDA by several hundred million. 40% revenue from Europe (2024) and >60% leisure mix mean macro downturns hit bookings; gross bookings $112B (2024) amplify volatility. Multi-brand overlap increases S&M spend ($2.4B in 2024) and cannibalization.

| Metric | 2024 Value |

|---|---|

| Gross bookings | $112B |

| Marketing spend | $3.1B |

| Sales & marketing | $2.4B |

| EBITDA | $7.4B |

| Europe revenue share | ≈40% |

| Leisure share | >60% |

Full Version Awaits

Booking Holdings SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, and it reflects the same structure, insights, and editable content included in the downloadable file.