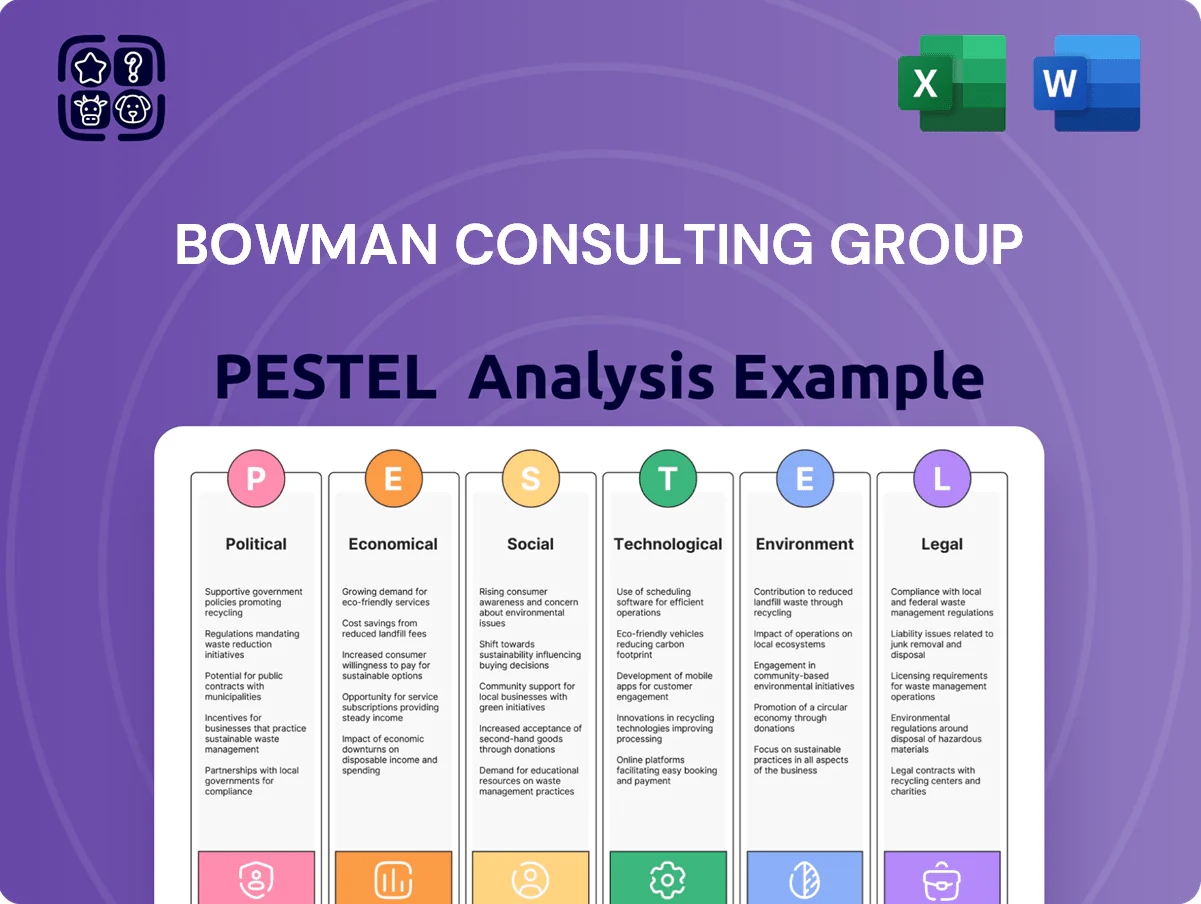

Bowman Consulting Group PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Our PESTLE snapshot reveals how regulatory shifts, infrastructure spending, and technological adoption shape Bowman Consulting Group’s strategic outlook—essential for investors and planners seeking actionable intelligence. Purchase the full PESTLE to access detailed risks, opportunity maps, and ready-to-use recommendations for modeling scenarios and strengthening competitive positioning.

Political factors

Federal Infrastructure Funding Initiatives

The continued rollout of IIJA funding, with $550 billion in new federal infrastructure investment and an estimated $110–130B for IIJA programs annually through 2025, drives Bowman Consulting Group’s public-sector pipeline across transportation, water and broadband projects.

These allocations give multi-year visibility for engineering and planning work; Bowman's backlog growth benefits from predictable contract flows tied to state DOT and EPA stimulus disbursements.

Political stability of budget appropriations is critical: any federal delays or rescissions could materially affect Bowman's revenue projections and backlog expansion into late 2025.

Energy Independence and Permitting Reform

Legislative moves like the 2023 Senate permitting reform proposals and state-level fast-track rules can cut approval times by 20–40%, directly boosting Bowman's project turnover and enabling faster revenue recognition on engineering and land services.

Political swings toward oil and gas versus renewables shift demand: U.S. renewable capacity additions reached 45 GW in 2023 while fossil fuel permits fell 12%, altering Bowman’s mix of land procurement and environmental consulting engagements.

Changes in federal or state leadership have historically re-prioritized funding—example: a 2021 infrastructure reallocation increased transmission projects by 15%—prompting rapid shifts in Bowman’s resourcing for specific energy infrastructure categories.

Public-Private Partnership (P3) Legislation

State-level political support for P3s expands large-scale infrastructure pipelines where Bowman offers construction management and technical services; 35 US states had enabling P3 laws by 2024, increasing project opportunities.

Favorable legislation channels private capital into public works—US P3 infrastructure investment reached about $11.5B in 2023—broadening Bowman's client mix beyond traditional government agencies.

Political advocacy for P3s drives complex, high-value consulting mandates; median P3 project sizes surpassed $200M in 2022, creating higher-margin advisory work for firms like Bowman.

Geopolitical Influence on Supply Chains

Geopolitical shifts and trade policies drive volatility in construction-material costs and availability, with global steel prices rising 18% in 2024 and shipping rates up 25% YoY, pressuring Bowman’s timelines and client budgets.

Tariffs and tensions—e.g., US/EU measures on steel and chip export controls—raise risks of delays or scope cuts for built-environment projects reliant on imported steel and technology components.

Strategic planning must model macro-political scenarios; e.g., hedging contracts and local sourcing reduced lead-time exposure by ~12% in comparable firms in 2024.

- Steel prices +18% (2024)

- Shipping rates +25% YoY (2024)

- Export controls/tariffs increase delay risk

- Hedging/local sourcing ~12% lead-time reduction

Local Zoning and Land Use Policies

Municipal political shifts and turnover in local leadership can lengthen or accelerate approval timelines for residential and commercial projects, with US permit processing times varying by city—average building permit wait times rose to about 45 days in 2024 in several Sun Belt metros.

Bowman’s land surveying and planning revenue, tied to urban density and suburban expansion policies, is exposed when cities tighten zoning—metro densification initiatives in 2024 redirected ~$12B in development toward infill projects nationally.

When local priorities pivot to affordable housing or industrial zoning, Bowman can capture niche demand: affordable housing incentives grew 18% in 2024, creating opportunities for survey, entitlement and site-planning services.

- Local leadership changes affect approval timelines (avg ~45 days permit waits in some metros, 2024)

- Urban density policies shift ~$12B development toward infill (2024)

- Affordable housing incentives up 18% in 2024 — new service niches for Bowman

IIJA fuels $110–130B/yr pipeline; P3s, renewables boost demand as costs and permits rise

IIJA’s $550B drives multi-year public-sector work with $110–130B/year through 2025; P3 laws in 35 states (2024) and $11.5B US P3 investment (2023) expand Bowman’s pipeline; renewables growth (45 GW added in 2023) and 2024 steel +18%/shipping +25% raise cost risks; local permit waits ~45 days (2024) and affordable housing incentives +18% (2024) shift service mix.

| Metric | Value |

|---|---|

| IIJA annual disbursements | $110–130B (through 2025) |

| P3-enabling states | 35 (2024) |

| US P3 investment | $11.5B (2023) |

| Renewable additions | 45 GW (2023) |

| Steel prices | +18% (2024) |

| Shipping rates | +25% YoY (2024) |

| Avg permit waits | ~45 days (some metros, 2024) |

| Affordable housing incentives | +18% (2024) |

What is included in the product

Explores how external macro-environmental factors uniquely affect Bowman Consulting Group across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven insights and trend analysis tailored to the company’s geographies and engineering/consulting markets.

Provides a concise, visually segmented PESTLE summary of Bowman Consulting Group that’s easily dropped into presentations or shared across teams to streamline external risk discussions and strategic alignment.

Economic factors

Interest Rate Environment and Capital Costs

By end-2025, interest rate trajectory is crucial for Bowman’s private-sector clients, especially real estate developers facing average US 30-year fixed mortgage rates near 6.7% (Feb 2025) and corporate borrowing costs elevated after Fed policy tightening; higher rates suppress new construction demand and delay projects. A stabilizing or falling rate regime—markets pricing ~25 bps easing through 2025—would likely revive capital investment in infrastructure and lift Bowman’s project pipeline. The firm’s valuation is sensitive to construction-sector rate elasticity, with project IRRs compressed as cap rates rise and discount rates increase, materially affecting backlog and revenue recognition.

Labor Market Dynamics and Technical Talent

The limited supply of skilled engineers, surveyors and technical consultants remains a key constraint for Bowman, with US engineering job openings at 4.5% in 2024 and sector wage growth around 5.8% YoY; competitive wage inflation and retention costs compress operating margins and raise labour as a percentage of revenue, forcing Bowman to target utilization >75% and efficient delivery to justify premium compensation and sustain scalable growth.

Inflationary Pressures on Project Inputs

Persistent inflation in raw materials and energy—U.S. construction material costs rose about 12% year-over-year in 2024—erodes margins and raises project budgets, challenging feasibility on Bowman-managed infrastructure projects.

As a service provider, Bowman's revenue depends on client capital spending; 2024 corporate capex cuts of 7–10% in some sectors reduced demand for engineering services.

Significant price volatility has driven contract renegotiations and delays, with industry reports showing 18% of large public works programs paused or re-scoped in 2024.

Urbanization and Migration Economic Trends

Urbanization toward Sun Belt and secondary markets shapes Bowman’s expansion, with Sun Belt states adding over 3 million net residents in 2023–2024 and metros like Austin, Phoenix, and Charlotte posting 4–6% annual job growth in 2024.

Bowman targets regions with rising infrastructure spend—state capital expenditures rose ~7% YoY in 2024—aligning office openings with local demand for utilities and civil engineering.

Monitoring regional GDP growth and corporate relocations (e.g., 2024 corporate moves adding ~$50–70B in regional investment) guides resource allocation to high-growth offices.

- Sun Belt population +3M (2023–24)

- Key metros job growth 4–6% (2024)

- State capex +7% YoY (2024)

- Corporate relocation investment ~$50–70B (2024)

Governmental Fiscal Health and Tax Policy

The fiscal capacity of state and local governments—total state and local tax revenue reached about $2.1 trillion in FY2023—directly affects funding for infrastructure upkeep and tech projects that drive demand for Bowman’s services.

Shifts in corporate tax rates or new tax credits for green building (over 10-year, IRA-style incentives seen since 2022) can redirect private and public investment toward sustainable projects relevant to Bowman.

A stable tax base underpins recurring public-sector contracts; U.S. capital spending on infrastructure was $1.2 trillion in 2024, indicating sustained market opportunity.

- State/local tax revenue ~$2.1T (FY2023)

- U.S. infrastructure capex ~$1.2T (2024)

- Expanded green tax incentives since 2022 influence project mix

Higher rates, rising costs and labor shortages squeeze construction margins and shift capex

Higher interest rates (30y mortgage ~6.7% Feb 2025) and elevated corporate borrowing compress project IRRs and delay real-estate driven demand; skilled-labor shortages (engineering openings 4.5% in 2024) and wage inflation (~5.8% YoY) raise costs; construction material inflation (~12% YoY 2024) and regional capex shifts (state capex +7% 2024; US infra capex ~$1.2T 2024) shape Bowman’s backlog and geographic focus.

| Metric | Value |

|---|---|

| 30y mortgage | 6.7% (Feb 2025) |

| Eng job openings | 4.5% (2024) |

| Wage growth | 5.8% YoY (2024) |

| Material inflation | 12% YoY (2024) |

| State capex | +7% YoY (2024) |

| US infra capex | $1.2T (2024) |

Full Version Awaits

Bowman Consulting Group PESTLE Analysis

The preview shown here is the exact Bowman Consulting Group PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning and decision-making.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Plan Smarter. Present Sharper. Compete Stronger.

Our PESTLE snapshot reveals how regulatory shifts, infrastructure spending, and technological adoption shape Bowman Consulting Group’s strategic outlook—essential for investors and planners seeking actionable intelligence. Purchase the full PESTLE to access detailed risks, opportunity maps, and ready-to-use recommendations for modeling scenarios and strengthening competitive positioning.

Political factors

Federal Infrastructure Funding Initiatives

The continued rollout of IIJA funding, with $550 billion in new federal infrastructure investment and an estimated $110–130B for IIJA programs annually through 2025, drives Bowman Consulting Group’s public-sector pipeline across transportation, water and broadband projects.

These allocations give multi-year visibility for engineering and planning work; Bowman's backlog growth benefits from predictable contract flows tied to state DOT and EPA stimulus disbursements.

Political stability of budget appropriations is critical: any federal delays or rescissions could materially affect Bowman's revenue projections and backlog expansion into late 2025.

Energy Independence and Permitting Reform

Legislative moves like the 2023 Senate permitting reform proposals and state-level fast-track rules can cut approval times by 20–40%, directly boosting Bowman's project turnover and enabling faster revenue recognition on engineering and land services.

Political swings toward oil and gas versus renewables shift demand: U.S. renewable capacity additions reached 45 GW in 2023 while fossil fuel permits fell 12%, altering Bowman’s mix of land procurement and environmental consulting engagements.

Changes in federal or state leadership have historically re-prioritized funding—example: a 2021 infrastructure reallocation increased transmission projects by 15%—prompting rapid shifts in Bowman’s resourcing for specific energy infrastructure categories.

Public-Private Partnership (P3) Legislation

State-level political support for P3s expands large-scale infrastructure pipelines where Bowman offers construction management and technical services; 35 US states had enabling P3 laws by 2024, increasing project opportunities.

Favorable legislation channels private capital into public works—US P3 infrastructure investment reached about $11.5B in 2023—broadening Bowman's client mix beyond traditional government agencies.

Political advocacy for P3s drives complex, high-value consulting mandates; median P3 project sizes surpassed $200M in 2022, creating higher-margin advisory work for firms like Bowman.

Geopolitical Influence on Supply Chains

Geopolitical shifts and trade policies drive volatility in construction-material costs and availability, with global steel prices rising 18% in 2024 and shipping rates up 25% YoY, pressuring Bowman’s timelines and client budgets.

Tariffs and tensions—e.g., US/EU measures on steel and chip export controls—raise risks of delays or scope cuts for built-environment projects reliant on imported steel and technology components.

Strategic planning must model macro-political scenarios; e.g., hedging contracts and local sourcing reduced lead-time exposure by ~12% in comparable firms in 2024.

- Steel prices +18% (2024)

- Shipping rates +25% YoY (2024)

- Export controls/tariffs increase delay risk

- Hedging/local sourcing ~12% lead-time reduction

Local Zoning and Land Use Policies

Municipal political shifts and turnover in local leadership can lengthen or accelerate approval timelines for residential and commercial projects, with US permit processing times varying by city—average building permit wait times rose to about 45 days in 2024 in several Sun Belt metros.

Bowman’s land surveying and planning revenue, tied to urban density and suburban expansion policies, is exposed when cities tighten zoning—metro densification initiatives in 2024 redirected ~$12B in development toward infill projects nationally.

When local priorities pivot to affordable housing or industrial zoning, Bowman can capture niche demand: affordable housing incentives grew 18% in 2024, creating opportunities for survey, entitlement and site-planning services.

- Local leadership changes affect approval timelines (avg ~45 days permit waits in some metros, 2024)

- Urban density policies shift ~$12B development toward infill (2024)

- Affordable housing incentives up 18% in 2024 — new service niches for Bowman

IIJA fuels $110–130B/yr pipeline; P3s, renewables boost demand as costs and permits rise

IIJA’s $550B drives multi-year public-sector work with $110–130B/year through 2025; P3 laws in 35 states (2024) and $11.5B US P3 investment (2023) expand Bowman’s pipeline; renewables growth (45 GW added in 2023) and 2024 steel +18%/shipping +25% raise cost risks; local permit waits ~45 days (2024) and affordable housing incentives +18% (2024) shift service mix.

| Metric | Value |

|---|---|

| IIJA annual disbursements | $110–130B (through 2025) |

| P3-enabling states | 35 (2024) |

| US P3 investment | $11.5B (2023) |

| Renewable additions | 45 GW (2023) |

| Steel prices | +18% (2024) |

| Shipping rates | +25% YoY (2024) |

| Avg permit waits | ~45 days (some metros, 2024) |

| Affordable housing incentives | +18% (2024) |

What is included in the product

Explores how external macro-environmental factors uniquely affect Bowman Consulting Group across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven insights and trend analysis tailored to the company’s geographies and engineering/consulting markets.

Provides a concise, visually segmented PESTLE summary of Bowman Consulting Group that’s easily dropped into presentations or shared across teams to streamline external risk discussions and strategic alignment.

Economic factors

Interest Rate Environment and Capital Costs

By end-2025, interest rate trajectory is crucial for Bowman’s private-sector clients, especially real estate developers facing average US 30-year fixed mortgage rates near 6.7% (Feb 2025) and corporate borrowing costs elevated after Fed policy tightening; higher rates suppress new construction demand and delay projects. A stabilizing or falling rate regime—markets pricing ~25 bps easing through 2025—would likely revive capital investment in infrastructure and lift Bowman’s project pipeline. The firm’s valuation is sensitive to construction-sector rate elasticity, with project IRRs compressed as cap rates rise and discount rates increase, materially affecting backlog and revenue recognition.

Labor Market Dynamics and Technical Talent

The limited supply of skilled engineers, surveyors and technical consultants remains a key constraint for Bowman, with US engineering job openings at 4.5% in 2024 and sector wage growth around 5.8% YoY; competitive wage inflation and retention costs compress operating margins and raise labour as a percentage of revenue, forcing Bowman to target utilization >75% and efficient delivery to justify premium compensation and sustain scalable growth.

Inflationary Pressures on Project Inputs

Persistent inflation in raw materials and energy—U.S. construction material costs rose about 12% year-over-year in 2024—erodes margins and raises project budgets, challenging feasibility on Bowman-managed infrastructure projects.

As a service provider, Bowman's revenue depends on client capital spending; 2024 corporate capex cuts of 7–10% in some sectors reduced demand for engineering services.

Significant price volatility has driven contract renegotiations and delays, with industry reports showing 18% of large public works programs paused or re-scoped in 2024.

Urbanization and Migration Economic Trends

Urbanization toward Sun Belt and secondary markets shapes Bowman’s expansion, with Sun Belt states adding over 3 million net residents in 2023–2024 and metros like Austin, Phoenix, and Charlotte posting 4–6% annual job growth in 2024.

Bowman targets regions with rising infrastructure spend—state capital expenditures rose ~7% YoY in 2024—aligning office openings with local demand for utilities and civil engineering.

Monitoring regional GDP growth and corporate relocations (e.g., 2024 corporate moves adding ~$50–70B in regional investment) guides resource allocation to high-growth offices.

- Sun Belt population +3M (2023–24)

- Key metros job growth 4–6% (2024)

- State capex +7% YoY (2024)

- Corporate relocation investment ~$50–70B (2024)

Governmental Fiscal Health and Tax Policy

The fiscal capacity of state and local governments—total state and local tax revenue reached about $2.1 trillion in FY2023—directly affects funding for infrastructure upkeep and tech projects that drive demand for Bowman’s services.

Shifts in corporate tax rates or new tax credits for green building (over 10-year, IRA-style incentives seen since 2022) can redirect private and public investment toward sustainable projects relevant to Bowman.

A stable tax base underpins recurring public-sector contracts; U.S. capital spending on infrastructure was $1.2 trillion in 2024, indicating sustained market opportunity.

- State/local tax revenue ~$2.1T (FY2023)

- U.S. infrastructure capex ~$1.2T (2024)

- Expanded green tax incentives since 2022 influence project mix

Higher rates, rising costs and labor shortages squeeze construction margins and shift capex

Higher interest rates (30y mortgage ~6.7% Feb 2025) and elevated corporate borrowing compress project IRRs and delay real-estate driven demand; skilled-labor shortages (engineering openings 4.5% in 2024) and wage inflation (~5.8% YoY) raise costs; construction material inflation (~12% YoY 2024) and regional capex shifts (state capex +7% 2024; US infra capex ~$1.2T 2024) shape Bowman’s backlog and geographic focus.

| Metric | Value |

|---|---|

| 30y mortgage | 6.7% (Feb 2025) |

| Eng job openings | 4.5% (2024) |

| Wage growth | 5.8% YoY (2024) |

| Material inflation | 12% YoY (2024) |

| State capex | +7% YoY (2024) |

| US infra capex | $1.2T (2024) |

Full Version Awaits

Bowman Consulting Group PESTLE Analysis

The preview shown here is the exact Bowman Consulting Group PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning and decision-making.