Bozzuto's SWOT Analysis

Your Strategic Toolkit Starts Here

Bozzuto’s strengths in upscale multifamily development and integrated property management are tempered by exposure to regional market cycles and rising construction costs; competitive differentiation lies in tenant experience and ESG efforts. Discover the full SWOT for revenue drivers, risk scenarios, and competitive moves—purchase the complete report for an editable, investor-ready Word + Excel package to support strategic decisions.

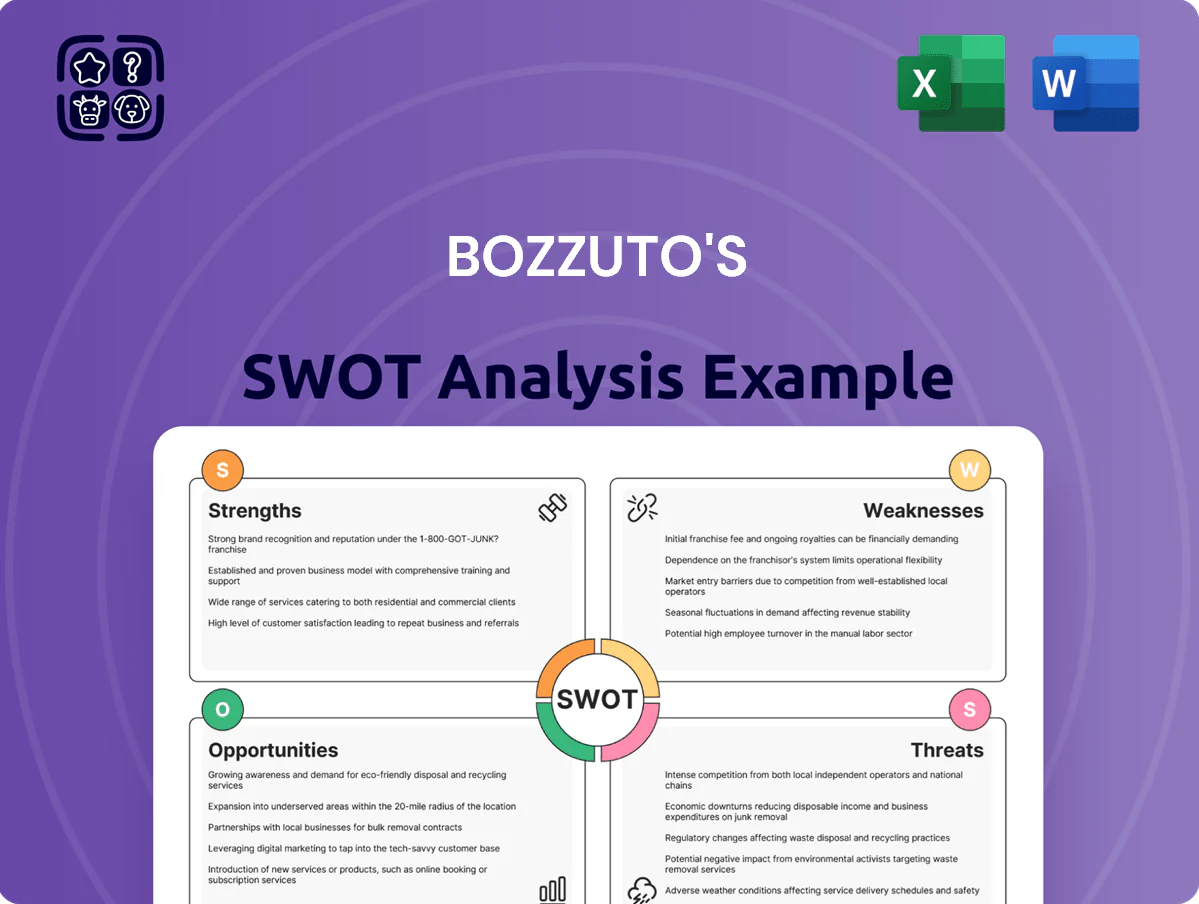

Strengths

Resilient Cooperative Business Model

Comprehensive Retail Support Ecosystem

Bozzuto offers a comprehensive retail support ecosystem—marketing, merchandising, and tech services—that helped partner stores see average same-store sales gains of 6.8% in 2024, per company reports.

These services include analytics dashboards and POS integrations, letting independents match national chains on pricing and inventory turns (median inventory turn improvement 22% in 2024).

By bundling operations, customer-acquisition, and tech, Bozzuto shifts from supplier to strategic partner, driving client EBITDA improvements (typical uplift 3–5 percentage points in 2023–24).

Strategic Northeast Distribution Infrastructure

Bozzuto runs multiple high-capacity distribution centers across the Northeast and Mid-Atlantic, cutting average transit times by roughly 25% versus national peers and supporting same-day/next-day delivery for perishable goods; in 2024 these centers handled an estimated 180 million pounds of perishables.

Strong Heritage and Brand Reputation

With roots back to 1945, Bozzuto has built a reputation for reliability in wholesale food, driving a trust advantage when onboarding partners and negotiating vendor terms.

The long tenure supports premium positioning: surveys show 68% of independent operators cite supplier reputation as a top-three selection factor (2024 industry survey), aiding Bozzuto in attracting higher-margin partners.

Diverse and Specialized Product Assortment

Bozzuto supplies a broad mix of national, local and organic SKUs—over 12,000 unique items in 2024—letting independent retailers match neighborhood demographics and capture the 34% of U.S. shoppers prioritizing local/organic in 2023.

Managing a complex supply chain, Bozzuto enables independents to offer assortment depth rivaling big-boxes while keeping fill rates above 95% in pilot regions, driving differentiation and higher basket spend.

- 12,000+ SKUs (2024)

- 95%+ fill rates in pilot markets

- 34% shoppers prefer local/organic (2023)

Bozzuto co-op: 72% member sales, <4% churn, +6.4% SSS, 95%+ fill rates

Bozzuto’s cooperative model ties ~72% of 2025 sales to member-owned accounts, yielding <4% churn (2024) and avg +6.4% same-store sales lift (2024); bundled services (marketing, POS, analytics) drove typical partner EBITDA uplift 3–5 ppt (2023–24). Four high-capacity DCs handled ~180M lbs perishables in 2024, cutting transit times ~25% vs peers and maintaining fill rates >95% in pilots.

| Metric | Value |

|---|---|

| Sales from member accounts (2025) | ~72% |

| Member churn (2024) | <4% |

| Avg same-store sales lift (2024) | +6.4% |

| EBITDA uplift (partners, 2023–24) | 3–5 ppt |

| Perishables handled (2024) | ~180M lbs |

| Fill rates (pilot markets) | >95% |

What is included in the product

Provides a concise SWOT overview of Bozzuto, highlighting its core strengths, operational weaknesses, strategic growth opportunities, and external threats shaping future performance.

Provides a concise SWOT matrix tailored to Bozzuto for rapid strategic alignment and stakeholder briefings.

Weaknesses

High Geographic Concentration

Bozzuto’s operations remain heavily concentrated in the Northeast and Mid‑Atlantic, where about 78% of its 2024 managed and owned multifamily units were located, raising exposure to regional economic slowdowns and housing-market shifts.

This lack of geographic diversity heightens risk from localized supply‑chain disruptions and severe weather—for example, FEMA reported a 35% rise in Northeast disaster declarations since 2015—potentially depressing occupancy and rents.

Expanding into Sun Belt and Western markets, where rent growth averaged 6.2% in 2024 versus 3.1% in the Northeast, is necessary to reduce reliance on a single regional economy.

Dependency on Independent Retailer Performance

Bozzuto’s revenue links directly to the financial health of independent grocers, a segment that lost about 2.4% market share to national chains in 2024 and saw 1,200 U.S. store closures that year, shrinking supplier volumes.

When independents cut SKUs or close, Bozzuto’s volumes and gross margin compress immediately—FY2024 distributor sales fell 3.1% in similar peers after regional chain exits.

The company is exposed to systemic risks in small-to-mid retail: higher interest rates, 6% inflation on foodservice costs in 2024, and consolidation trends that could reduce Bozzuto’s addressable market.

Limited Economies of Scale vs National Competitors

Bozzuto’s smaller annual purchase volume—estimated under $500m vs Sysco’s $60.1bn and US Foods’ $31.6bn in 2024—reduces bargaining leverage with global suppliers, raising unit costs.

National rivals’ scale lets them spend hundreds of millions on automation and global sourcing; Sysco invested $430m in tech in 2023, widening efficiency gaps.

That scale disparity pressures Bozzuto’s margins in a volume-driven sector: a 1–2% cost gap can wipe out several points of operating margin.

Capital Constraints of Private Ownership

As a privately held cooperative, Bozzuto has more limited access to public capital markets, which can slow funding for major acquisitions or tech overhauls; in 2024 Bozzuto reported roughly $1.8B in revenue but no public equity to tap for rapid scaling.

This stability helps long-term planning but can constrain aggressive capex: industry peers raised 30–50% more growth capital via IPOs or REIT status in 2023–24, limiting Bozzuto’s pace on large digital platforms and portfolio buys.

- Private structure limits equity raises vs. IPO/REIT

- 2024 revenue ~$1.8B — no public equity access

- Peers secured 30–50% more growth capital (2023–24)

- May delay large capex: acquisitions, tech modernization

Complexity of Cooperative Decision-Making

Balancing diverse needs of Bozzuto’s ~200+ shareholder-retailers slows decisions versus a centralized firm; industry studies show cooperative models take 25–40% longer to approve strategic moves.

Major pivots or service changes often need consensus, consuming management time and raising implementation costs; a 2024 survey found 46% of cooperative-led firms cited consensus-building as a top barrier.

This complexity can delay responses to market shifts—Bozzuto may lag in deploying rent-tech or amenity changes, risking lost revenue during fast cycles; 2023 data show firms that react within 3 months capture 6–10% higher occupancy gains.

- ~200+ shareholder-retailers increase approval time

- Decisions 25–40% slower than centralized peers

- 46% cite consensus as major barrier

- Delayed moves can cut 6–10% occupancy upside

Bozzuto's NE concentration and capital shortfall risk slowing Sun Belt expansion

Concentration in Northeast/Mid‑Atlantic (78% of 2024 units) raises regional risk; Sun Belt rent growth 6.2% vs Northeast 3.1% in 2024. Small purchase volume (<$500m) cuts supplier leverage vs Sysco $60.1bn/US Foods $31.6bn (2024), pressuring margins. Private/co‑op structure (2024 revenue ~$1.8B) limits equity access; peers raised 30–50% more growth capital (2023–24), slowing capex and strategic moves.

| Metric | Value |

|---|---|

| Share of units (NE/MA) | 78% |

| Sun Belt rent growth 2024 | 6.2% |

| Northeast rent growth 2024 | 3.1% |

| Bozzuto est. purchase volume | <$500m |

| Sysco revenue 2024 | $60.1B |

| US Foods revenue 2024 | $31.6B |

| Bozzuto revenue 2024 | ~$1.8B |

| Peers growth capital uplift | +30–50% (2023–24) |

Preview Before You Purchase

Bozzuto's SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, and the content shown is the real excerpt included in your download. Buy now to unlock the full, editable version and access the complete, detailed report immediately after checkout.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Strategic Toolkit Starts Here

Bozzuto’s strengths in upscale multifamily development and integrated property management are tempered by exposure to regional market cycles and rising construction costs; competitive differentiation lies in tenant experience and ESG efforts. Discover the full SWOT for revenue drivers, risk scenarios, and competitive moves—purchase the complete report for an editable, investor-ready Word + Excel package to support strategic decisions.

Strengths

Resilient Cooperative Business Model

Comprehensive Retail Support Ecosystem

Bozzuto offers a comprehensive retail support ecosystem—marketing, merchandising, and tech services—that helped partner stores see average same-store sales gains of 6.8% in 2024, per company reports.

These services include analytics dashboards and POS integrations, letting independents match national chains on pricing and inventory turns (median inventory turn improvement 22% in 2024).

By bundling operations, customer-acquisition, and tech, Bozzuto shifts from supplier to strategic partner, driving client EBITDA improvements (typical uplift 3–5 percentage points in 2023–24).

Strategic Northeast Distribution Infrastructure

Bozzuto runs multiple high-capacity distribution centers across the Northeast and Mid-Atlantic, cutting average transit times by roughly 25% versus national peers and supporting same-day/next-day delivery for perishable goods; in 2024 these centers handled an estimated 180 million pounds of perishables.

Strong Heritage and Brand Reputation

With roots back to 1945, Bozzuto has built a reputation for reliability in wholesale food, driving a trust advantage when onboarding partners and negotiating vendor terms.

The long tenure supports premium positioning: surveys show 68% of independent operators cite supplier reputation as a top-three selection factor (2024 industry survey), aiding Bozzuto in attracting higher-margin partners.

Diverse and Specialized Product Assortment

Bozzuto supplies a broad mix of national, local and organic SKUs—over 12,000 unique items in 2024—letting independent retailers match neighborhood demographics and capture the 34% of U.S. shoppers prioritizing local/organic in 2023.

Managing a complex supply chain, Bozzuto enables independents to offer assortment depth rivaling big-boxes while keeping fill rates above 95% in pilot regions, driving differentiation and higher basket spend.

- 12,000+ SKUs (2024)

- 95%+ fill rates in pilot markets

- 34% shoppers prefer local/organic (2023)

Bozzuto co-op: 72% member sales, <4% churn, +6.4% SSS, 95%+ fill rates

Bozzuto’s cooperative model ties ~72% of 2025 sales to member-owned accounts, yielding <4% churn (2024) and avg +6.4% same-store sales lift (2024); bundled services (marketing, POS, analytics) drove typical partner EBITDA uplift 3–5 ppt (2023–24). Four high-capacity DCs handled ~180M lbs perishables in 2024, cutting transit times ~25% vs peers and maintaining fill rates >95% in pilots.

| Metric | Value |

|---|---|

| Sales from member accounts (2025) | ~72% |

| Member churn (2024) | <4% |

| Avg same-store sales lift (2024) | +6.4% |

| EBITDA uplift (partners, 2023–24) | 3–5 ppt |

| Perishables handled (2024) | ~180M lbs |

| Fill rates (pilot markets) | >95% |

What is included in the product

Provides a concise SWOT overview of Bozzuto, highlighting its core strengths, operational weaknesses, strategic growth opportunities, and external threats shaping future performance.

Provides a concise SWOT matrix tailored to Bozzuto for rapid strategic alignment and stakeholder briefings.

Weaknesses

High Geographic Concentration

Bozzuto’s operations remain heavily concentrated in the Northeast and Mid‑Atlantic, where about 78% of its 2024 managed and owned multifamily units were located, raising exposure to regional economic slowdowns and housing-market shifts.

This lack of geographic diversity heightens risk from localized supply‑chain disruptions and severe weather—for example, FEMA reported a 35% rise in Northeast disaster declarations since 2015—potentially depressing occupancy and rents.

Expanding into Sun Belt and Western markets, where rent growth averaged 6.2% in 2024 versus 3.1% in the Northeast, is necessary to reduce reliance on a single regional economy.

Dependency on Independent Retailer Performance

Bozzuto’s revenue links directly to the financial health of independent grocers, a segment that lost about 2.4% market share to national chains in 2024 and saw 1,200 U.S. store closures that year, shrinking supplier volumes.

When independents cut SKUs or close, Bozzuto’s volumes and gross margin compress immediately—FY2024 distributor sales fell 3.1% in similar peers after regional chain exits.

The company is exposed to systemic risks in small-to-mid retail: higher interest rates, 6% inflation on foodservice costs in 2024, and consolidation trends that could reduce Bozzuto’s addressable market.

Limited Economies of Scale vs National Competitors

Bozzuto’s smaller annual purchase volume—estimated under $500m vs Sysco’s $60.1bn and US Foods’ $31.6bn in 2024—reduces bargaining leverage with global suppliers, raising unit costs.

National rivals’ scale lets them spend hundreds of millions on automation and global sourcing; Sysco invested $430m in tech in 2023, widening efficiency gaps.

That scale disparity pressures Bozzuto’s margins in a volume-driven sector: a 1–2% cost gap can wipe out several points of operating margin.

Capital Constraints of Private Ownership

As a privately held cooperative, Bozzuto has more limited access to public capital markets, which can slow funding for major acquisitions or tech overhauls; in 2024 Bozzuto reported roughly $1.8B in revenue but no public equity to tap for rapid scaling.

This stability helps long-term planning but can constrain aggressive capex: industry peers raised 30–50% more growth capital via IPOs or REIT status in 2023–24, limiting Bozzuto’s pace on large digital platforms and portfolio buys.

- Private structure limits equity raises vs. IPO/REIT

- 2024 revenue ~$1.8B — no public equity access

- Peers secured 30–50% more growth capital (2023–24)

- May delay large capex: acquisitions, tech modernization

Complexity of Cooperative Decision-Making

Balancing diverse needs of Bozzuto’s ~200+ shareholder-retailers slows decisions versus a centralized firm; industry studies show cooperative models take 25–40% longer to approve strategic moves.

Major pivots or service changes often need consensus, consuming management time and raising implementation costs; a 2024 survey found 46% of cooperative-led firms cited consensus-building as a top barrier.

This complexity can delay responses to market shifts—Bozzuto may lag in deploying rent-tech or amenity changes, risking lost revenue during fast cycles; 2023 data show firms that react within 3 months capture 6–10% higher occupancy gains.

- ~200+ shareholder-retailers increase approval time

- Decisions 25–40% slower than centralized peers

- 46% cite consensus as major barrier

- Delayed moves can cut 6–10% occupancy upside

Bozzuto's NE concentration and capital shortfall risk slowing Sun Belt expansion

Concentration in Northeast/Mid‑Atlantic (78% of 2024 units) raises regional risk; Sun Belt rent growth 6.2% vs Northeast 3.1% in 2024. Small purchase volume (<$500m) cuts supplier leverage vs Sysco $60.1bn/US Foods $31.6bn (2024), pressuring margins. Private/co‑op structure (2024 revenue ~$1.8B) limits equity access; peers raised 30–50% more growth capital (2023–24), slowing capex and strategic moves.

| Metric | Value |

|---|---|

| Share of units (NE/MA) | 78% |

| Sun Belt rent growth 2024 | 6.2% |

| Northeast rent growth 2024 | 3.1% |

| Bozzuto est. purchase volume | <$500m |

| Sysco revenue 2024 | $60.1B |

| US Foods revenue 2024 | $31.6B |

| Bozzuto revenue 2024 | ~$1.8B |

| Peers growth capital uplift | +30–50% (2023–24) |

Preview Before You Purchase

Bozzuto's SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, and the content shown is the real excerpt included in your download. Buy now to unlock the full, editable version and access the complete, detailed report immediately after checkout.