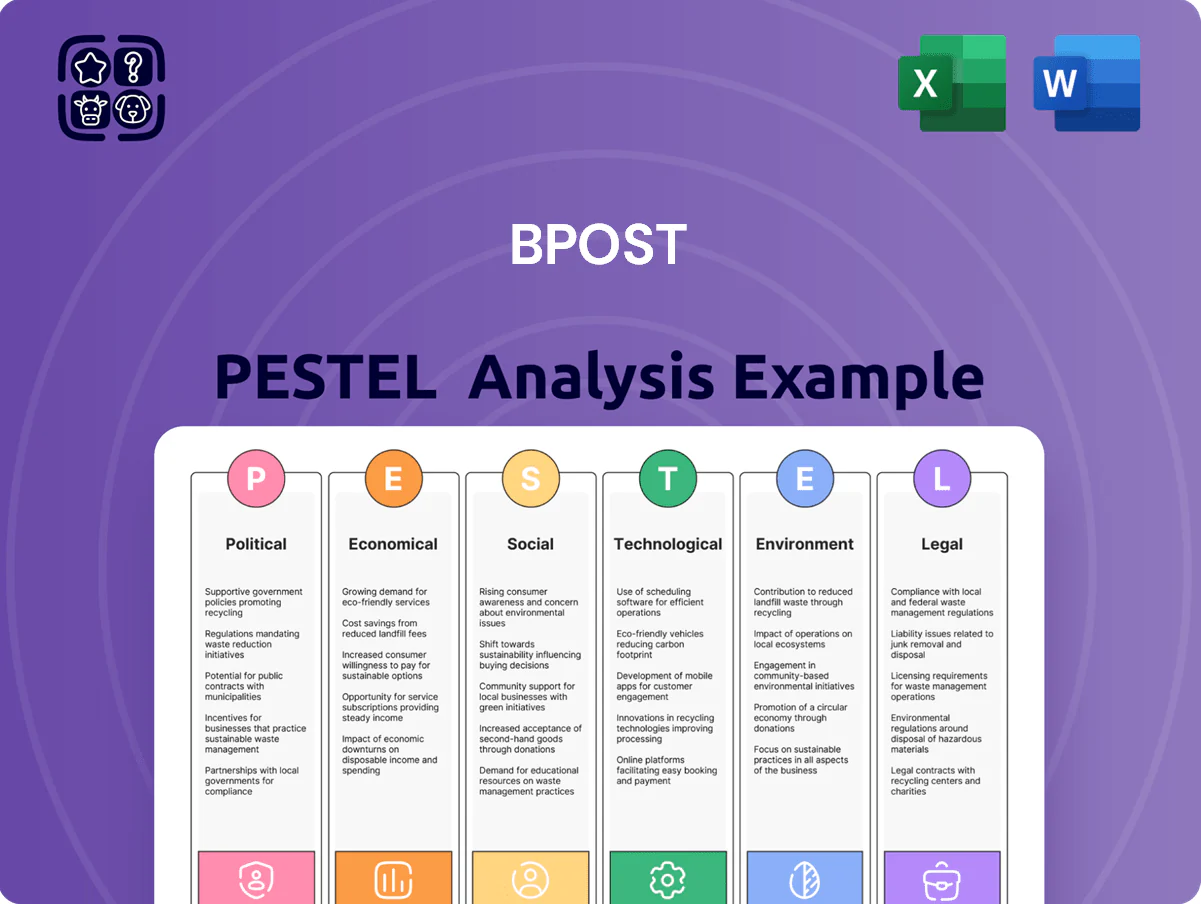

bpost PESTLE Analysis

Skip the Research. Get the Strategy.

Gain a competitive edge with our focused PESTLE Analysis of bpost—uncover how political shifts, economic pressures, and tech disruption shape its strategy and risk profile; ideal for investors and strategists seeking concise, actionable intelligence. Purchase the full report to access the complete, editable breakdown and leverage insights for smarter decisions—download instantly.

Political factors

Government Shareholding and State Control

The Belgian State holds 50.01% of bpost’s shares as of 2025, shaping board appointments and strategic priorities; this secures public service obligations like universal mail delivery but can prompt political influence over commercial moves. State ownership has coincided with slower rollouts of parcel automation despite parcel revenue rising 12% in 2024 to EUR 1.2bn. Investors should track policy shifts that may conflict with bpost’s profitability and modernization plans.

Management of Universal Service Obligations

The Belgian government mandates that bpost deliver universal postal services nationwide at affordable rates, a requirement that in 2024 covered roughly 3.8 million items weekly and contributed to 2023 reported public service costs of about EUR 120 million. Negotiations over compensation for these public service missions remain politically sensitive and directly influence bpost’s EBITDA, which was EUR 540 million in 2023. Any change in scope or funding can disrupt operational stability and complicate financial planning, given the company’s 2024 capex guidance of around EUR 300 million.

Geopolitical Stability in International Markets

Through subsidiaries like Radial, bpost faces political exposure in North America and Asia where 2024 US-China trade frictions and 2023-24 tariff adjustments impacted cross-border parcels—global e-commerce shipments fell 1.8% in 2023 in some routes—while changes to the Universal Postal Union rates could alter terminal dues revenue; bpost’s diversified footprint (Belgium 2024 revenue €2.9bn, Radial contributing ~€500m) helps mitigate regional protectionist shocks.

Labor Union Relations and Political Pressure

The Belgian postal sector's strong unionization makes labor relations a frequent national political issue; bpost recorded 12 strike days in 2023 affecting 4% of deliveries and prompting government-led talks in 2024.

Strikes and disputes have caused measurable service disruptions, denting reliability metrics—on-time delivery fell 2.8 percentage points in peak 2023—and often require mediation.

Political pressure to protect employment conflicts with efficiency-driven restructuring: bpost's 2022–24 plan aimed to cut 1,100 jobs but faced political resistance tied to social employment goals.

- 12 strike days in 2023; 4% delivery impact

- On-time delivery down 2.8 pp in peak 2023

- 1,100 job-reduction target (2022–24) met political pushback

EU Postal Services Liberalization

EU directives continue to liberalize postal markets, increasing competition; by 2024 over 80% of EU member states have full market opening, pressuring incumbents like bpost which reported 2024 parcel revenue of €1.2bn and mail revenue decline of 7% YoY.

Compliance with EU state aid and competition rules is mandatory to avoid fines—recent EC rulings have imposed fines up to €100m in sector cases—and bpost must align operations to avoid restructuring orders.

bpost must navigate supra-national frameworks while defending market share against private entrants: private operators captured about 15–20% of Belgian parcel volumes in 2024, eroding legacy margins.

- 80%+ EU full market opening (2024)

- bpost 2024 parcel revenue €1.2bn; mail -7% YoY

- Private operators 15–20% Belgian parcel share (2024)

- EC fines in sector cases reached ~€100m

State 50.01% stake shapes postal finances: €1.2bn parcels, €120m universal cost

State 50.01% (2025) drives public service and board influence; universal service cost ~€120m (2023) affects EBITDA (€540m 2023). Parcel revenue €1.2bn (2024); mail -7% YoY. 12 strike days (2023) cut deliveries 4%; on-time -2.8 pp. EU market open >80% (2024); private parcel share 15–20% (2024).

| Metric | Value |

|---|---|

| State stake | 50.01% (2025) |

| Parcel rev | €1.2bn (2024) |

| Universal cost | €120m (2023) |

| EBITDA | €540m (2023) |

| Strikes | 12 days (2023) |

| Private parcel share | 15–20% (2024) |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal factors uniquely impact bpost, with data-driven subpoints and forward-looking insights tailored to its regional postal/logistics market to support strategy, risk management and investor communication.

A concise, visually segmented PESTLE summary tailored to bpost that clarifies regulatory, economic, and technological impacts for quick use in presentations or cross-team planning sessions.

Economic factors

E-commerce Growth and Parcel Volume

Continued expansion of online shopping drives bpost parcel revenue—Belgian e-commerce sales rose 9.3% in 2024 to €18.6bn, pushing bpost parcel volumes up ~7% y/y in FY2024 and contributing over 60% of parcel revenue.

Permanent shift to digital storefronts forces bpost to invest in sorting capacity and last-mile delivery; capex for parcel network increased to €180m in 2024.

Economic downturns can cut discretionary e-commerce spend—Belgian retail confidence fell in 2024 and bpost saw monthly parcel volumes volatile, dipping ~4% in recession-sensitive categories.

Inflationary Pressures and Operational Costs

Rising energy, fuel and labor costs erode logistics margins; diesel prices rose ~14% in 2024 while Belgian industrial electricity costs averaged €0.22/kWh, pressuring bpost’s 2024 adjusted EBIT margin of 4.6%. Passing costs risks churn to lean competitors like DPD and PostNL; Belgium’s automatic wage indexation (inflation ~4.1% in 2024) forces forecasted personnel cost increases of ~3–5%, necessitating tight cost-control and pricing strategy.

Decline in Traditional Mail Volumes

The structural shift to digital communication has cut Belgian addressed mail volumes by about 40% since 2010, with bpost reporting letter volumes falling roughly 6% year-on-year in 2024, eroding high-margin mail revenue and raising unit costs as legacy infrastructure underutilization grows; bpost’s 2024 annual report shows parcels and parcels-related services now account for over 60% of operating income, underscoring urgent pivots into logistics and financial services to offset permanent mail contraction.

Interest Rate Volatility and Financing

Fluctuations in interest rates directly alter bpost’s cost of debt—Belgium’s 10‑yr government yield rose from 1.0% in 2021 to ~3.5% in 2024, raising corporate borrowing costs and tightening margins on planned infrastructure upgrades and the 2023–25 capex program.

Higher rates discount future cash flows, lowering valuation and reducing appeal to dividend-seeking investors given bpost’s 2024 dividend yield ~5%; capital allocation must stay flexible to optimize debt maturities and preserve liquidity.

- Rising yields (Belgian 10‑yr ~3.5% in 2024) increase funding costs

- Discounted cash flows can reduce stock attractiveness to yield investors (dividend yield ~5% in 2024)

- Flexible capital allocation and active debt management required

Global Supply Chain Dynamics

Global supply chain disruptions directly impact bpost’s timing and costs for international shipments; 2024 data shows global container freight rates remained 20-30% above 2019 levels during parts of the year, increasing per-shipment costs for carriers.

Economic instability in manufacturing hubs like China and Vietnam can cause inventory shortages for e-commerce clients, lowering bpost’s fulfillment volumes—EU cross-border parcel demand fell 5% YoY in Q3 2024 in some corridors.

Building resilient logistics networks—diversifying routes, nearshoring, and increasing buffer capacity—is vital to maintain service levels during shocks; bpost’s capex focus on hub automation and partnerships aims to mitigate such risks.

- Higher freight rates raise per-parcel costs 20–30%

- Supply shortages can cut fulfillment volumes ≈5% YoY in affected corridors

- Resilience investments (automation, route diversification) are key mitigation

Belgian e‑commerce lifts parcels; rising costs squeeze margins and raise funding needs

Belgian e‑commerce +9.3% (2024) lifts parcels (~+7% FY2024) but mail volumes −6% YoY (2024); capex for parcel network €180m (2024). Energy/fuel +14% (diesel 2024) and wages (indexation, inflation ~4.1%) squeeze EBIT margin 4.6% (2024); Belgian 10‑yr ~3.5% raises funding costs; global freight 20–30% above 2019 raising per‑parcel costs.

| Metric | 2024 |

|---|---|

| E‑commerce sales (BE) | €18.6bn (+9.3%) |

| Parcel vol. bpost | +7% YoY |

| Capex parcels | €180m |

| EBIT adj. margin | 4.6% |

| Diesel | +14% |

| 10‑yr BE yield | ~3.5% |

Same Document Delivered

bpost PESTLE Analysis

The preview shown here is the exact bpost PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic or investment decisions.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Skip the Research. Get the Strategy.

Gain a competitive edge with our focused PESTLE Analysis of bpost—uncover how political shifts, economic pressures, and tech disruption shape its strategy and risk profile; ideal for investors and strategists seeking concise, actionable intelligence. Purchase the full report to access the complete, editable breakdown and leverage insights for smarter decisions—download instantly.

Political factors

Government Shareholding and State Control

The Belgian State holds 50.01% of bpost’s shares as of 2025, shaping board appointments and strategic priorities; this secures public service obligations like universal mail delivery but can prompt political influence over commercial moves. State ownership has coincided with slower rollouts of parcel automation despite parcel revenue rising 12% in 2024 to EUR 1.2bn. Investors should track policy shifts that may conflict with bpost’s profitability and modernization plans.

Management of Universal Service Obligations

The Belgian government mandates that bpost deliver universal postal services nationwide at affordable rates, a requirement that in 2024 covered roughly 3.8 million items weekly and contributed to 2023 reported public service costs of about EUR 120 million. Negotiations over compensation for these public service missions remain politically sensitive and directly influence bpost’s EBITDA, which was EUR 540 million in 2023. Any change in scope or funding can disrupt operational stability and complicate financial planning, given the company’s 2024 capex guidance of around EUR 300 million.

Geopolitical Stability in International Markets

Through subsidiaries like Radial, bpost faces political exposure in North America and Asia where 2024 US-China trade frictions and 2023-24 tariff adjustments impacted cross-border parcels—global e-commerce shipments fell 1.8% in 2023 in some routes—while changes to the Universal Postal Union rates could alter terminal dues revenue; bpost’s diversified footprint (Belgium 2024 revenue €2.9bn, Radial contributing ~€500m) helps mitigate regional protectionist shocks.

Labor Union Relations and Political Pressure

The Belgian postal sector's strong unionization makes labor relations a frequent national political issue; bpost recorded 12 strike days in 2023 affecting 4% of deliveries and prompting government-led talks in 2024.

Strikes and disputes have caused measurable service disruptions, denting reliability metrics—on-time delivery fell 2.8 percentage points in peak 2023—and often require mediation.

Political pressure to protect employment conflicts with efficiency-driven restructuring: bpost's 2022–24 plan aimed to cut 1,100 jobs but faced political resistance tied to social employment goals.

- 12 strike days in 2023; 4% delivery impact

- On-time delivery down 2.8 pp in peak 2023

- 1,100 job-reduction target (2022–24) met political pushback

EU Postal Services Liberalization

EU directives continue to liberalize postal markets, increasing competition; by 2024 over 80% of EU member states have full market opening, pressuring incumbents like bpost which reported 2024 parcel revenue of €1.2bn and mail revenue decline of 7% YoY.

Compliance with EU state aid and competition rules is mandatory to avoid fines—recent EC rulings have imposed fines up to €100m in sector cases—and bpost must align operations to avoid restructuring orders.

bpost must navigate supra-national frameworks while defending market share against private entrants: private operators captured about 15–20% of Belgian parcel volumes in 2024, eroding legacy margins.

- 80%+ EU full market opening (2024)

- bpost 2024 parcel revenue €1.2bn; mail -7% YoY

- Private operators 15–20% Belgian parcel share (2024)

- EC fines in sector cases reached ~€100m

State 50.01% stake shapes postal finances: €1.2bn parcels, €120m universal cost

State 50.01% (2025) drives public service and board influence; universal service cost ~€120m (2023) affects EBITDA (€540m 2023). Parcel revenue €1.2bn (2024); mail -7% YoY. 12 strike days (2023) cut deliveries 4%; on-time -2.8 pp. EU market open >80% (2024); private parcel share 15–20% (2024).

| Metric | Value |

|---|---|

| State stake | 50.01% (2025) |

| Parcel rev | €1.2bn (2024) |

| Universal cost | €120m (2023) |

| EBITDA | €540m (2023) |

| Strikes | 12 days (2023) |

| Private parcel share | 15–20% (2024) |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal factors uniquely impact bpost, with data-driven subpoints and forward-looking insights tailored to its regional postal/logistics market to support strategy, risk management and investor communication.

A concise, visually segmented PESTLE summary tailored to bpost that clarifies regulatory, economic, and technological impacts for quick use in presentations or cross-team planning sessions.

Economic factors

E-commerce Growth and Parcel Volume

Continued expansion of online shopping drives bpost parcel revenue—Belgian e-commerce sales rose 9.3% in 2024 to €18.6bn, pushing bpost parcel volumes up ~7% y/y in FY2024 and contributing over 60% of parcel revenue.

Permanent shift to digital storefronts forces bpost to invest in sorting capacity and last-mile delivery; capex for parcel network increased to €180m in 2024.

Economic downturns can cut discretionary e-commerce spend—Belgian retail confidence fell in 2024 and bpost saw monthly parcel volumes volatile, dipping ~4% in recession-sensitive categories.

Inflationary Pressures and Operational Costs

Rising energy, fuel and labor costs erode logistics margins; diesel prices rose ~14% in 2024 while Belgian industrial electricity costs averaged €0.22/kWh, pressuring bpost’s 2024 adjusted EBIT margin of 4.6%. Passing costs risks churn to lean competitors like DPD and PostNL; Belgium’s automatic wage indexation (inflation ~4.1% in 2024) forces forecasted personnel cost increases of ~3–5%, necessitating tight cost-control and pricing strategy.

Decline in Traditional Mail Volumes

The structural shift to digital communication has cut Belgian addressed mail volumes by about 40% since 2010, with bpost reporting letter volumes falling roughly 6% year-on-year in 2024, eroding high-margin mail revenue and raising unit costs as legacy infrastructure underutilization grows; bpost’s 2024 annual report shows parcels and parcels-related services now account for over 60% of operating income, underscoring urgent pivots into logistics and financial services to offset permanent mail contraction.

Interest Rate Volatility and Financing

Fluctuations in interest rates directly alter bpost’s cost of debt—Belgium’s 10‑yr government yield rose from 1.0% in 2021 to ~3.5% in 2024, raising corporate borrowing costs and tightening margins on planned infrastructure upgrades and the 2023–25 capex program.

Higher rates discount future cash flows, lowering valuation and reducing appeal to dividend-seeking investors given bpost’s 2024 dividend yield ~5%; capital allocation must stay flexible to optimize debt maturities and preserve liquidity.

- Rising yields (Belgian 10‑yr ~3.5% in 2024) increase funding costs

- Discounted cash flows can reduce stock attractiveness to yield investors (dividend yield ~5% in 2024)

- Flexible capital allocation and active debt management required

Global Supply Chain Dynamics

Global supply chain disruptions directly impact bpost’s timing and costs for international shipments; 2024 data shows global container freight rates remained 20-30% above 2019 levels during parts of the year, increasing per-shipment costs for carriers.

Economic instability in manufacturing hubs like China and Vietnam can cause inventory shortages for e-commerce clients, lowering bpost’s fulfillment volumes—EU cross-border parcel demand fell 5% YoY in Q3 2024 in some corridors.

Building resilient logistics networks—diversifying routes, nearshoring, and increasing buffer capacity—is vital to maintain service levels during shocks; bpost’s capex focus on hub automation and partnerships aims to mitigate such risks.

- Higher freight rates raise per-parcel costs 20–30%

- Supply shortages can cut fulfillment volumes ≈5% YoY in affected corridors

- Resilience investments (automation, route diversification) are key mitigation

Belgian e‑commerce lifts parcels; rising costs squeeze margins and raise funding needs

Belgian e‑commerce +9.3% (2024) lifts parcels (~+7% FY2024) but mail volumes −6% YoY (2024); capex for parcel network €180m (2024). Energy/fuel +14% (diesel 2024) and wages (indexation, inflation ~4.1%) squeeze EBIT margin 4.6% (2024); Belgian 10‑yr ~3.5% raises funding costs; global freight 20–30% above 2019 raising per‑parcel costs.

| Metric | 2024 |

|---|---|

| E‑commerce sales (BE) | €18.6bn (+9.3%) |

| Parcel vol. bpost | +7% YoY |

| Capex parcels | €180m |

| EBIT adj. margin | 4.6% |

| Diesel | +14% |

| 10‑yr BE yield | ~3.5% |

Same Document Delivered

bpost PESTLE Analysis

The preview shown here is the exact bpost PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic or investment decisions.