Brambles Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

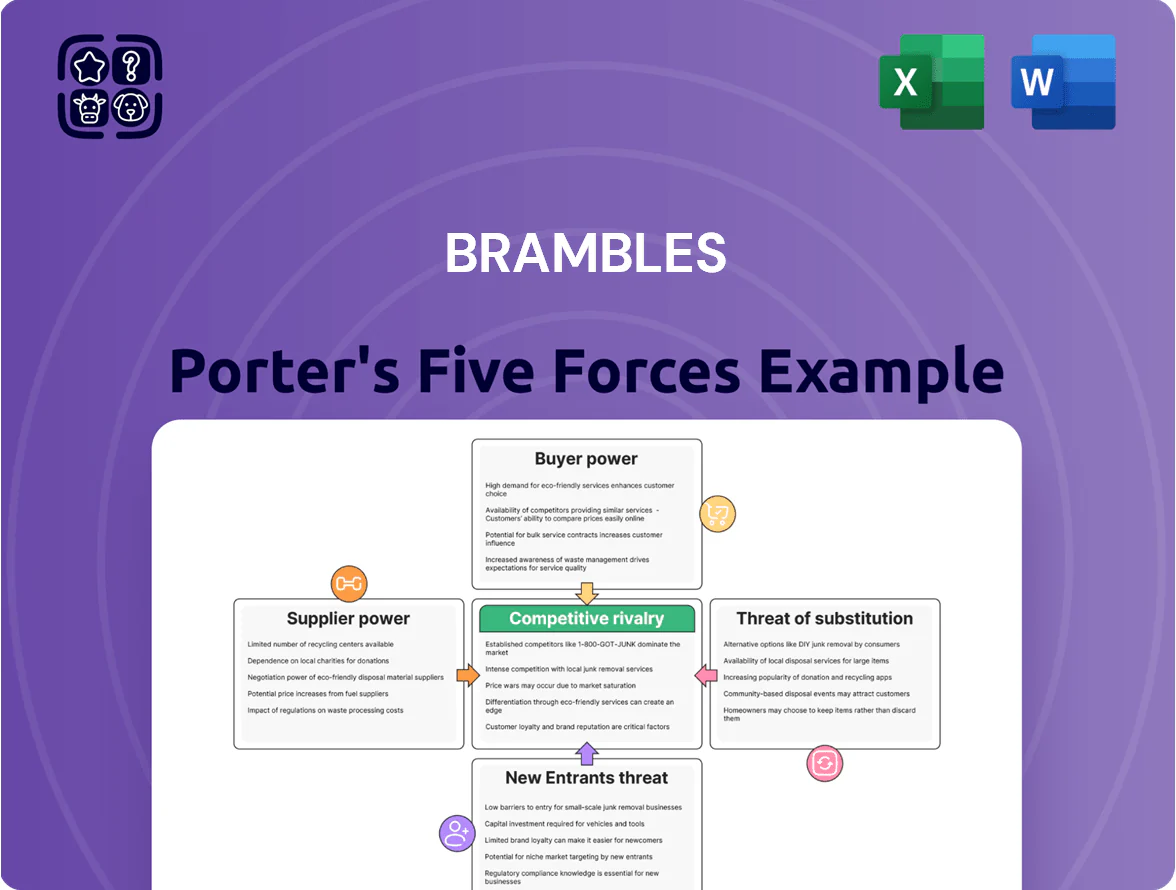

Brambles faces moderate supplier power but benefits from scale in pallet pooling while buyer concentration and cost sensitivity create pricing pressure; threats from new entrants are low but substitutes and tech-driven logistics shifts raise strategic risk. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Brambles’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Raw Material Price Volatility

Brambles relies on global lumber and plastic resins for CHEP pallets; timber price swings raised global softwood lumber prices ~35% in 2021–2023, lifting pallet capex and repair costs and increasing FY2024 pallet replacement spending by an estimated mid-single-digit percentage.

Reliance on Specialized Sawmills

Brambles needs high-quality, sustainably sourced timber that meets strict durability for pooling; that narrows viable suppliers to specialized sawmills able to deliver volume plus FSC or PEFC certification.

Only an estimated 18–22% of global softwood suppliers held FSC/PEFC chain-of-custody in 2024, so certified sawmills exert moderate leverage over Brambles’ procurement.

Rising regulation and corporate sourcing targets (EU Deforestation Regulation effective 2021, many buyers targeting 2025–30) increase supplier bargaining power and pricing pressure.

Logistics and Transportation Providers

The circular model depends on thousands of third-party carriers to return empties; in 2024 Brambles moved ~2.5bn pallet journeys globally, so transport is critical.

Rising diesel prices (up ~18% year‑on‑year in 2023–24) and US/EU trucker shortages (shortfall ~80,000 drivers in 2024) boost carriers’ fee power.

Brambles uses long‑term contracts and its Trax/Dynamics route optimization; these cut empty-km by ~12% in pilot regions, but regional capacity limits still raise spot rates.

Energy Costs for Manufacturing

Energy use for plastic container production and automated service centers is material: Brambles reported energy and fuel costs of US$282m in FY2024, up 6% year-on-year, exposing it to electricity and gas price swings in Europe and North America.

Suppliers wield bargaining power via regulated tariffs and market spikes—European wholesale gas prices rose ~40% in 2023 vs 2022—pressuring margins for energy-intensive ops.

Brambles mitigates risk by spending on efficiency and renewables: as of Dec 2024 it sourced ~35% of electricity from renewables and targets 100% by 2030 to stabilize long-term costs.

- FY2024 energy & fuel expense: US$282m

- European gas spot +~40% in 2023 vs 2022

- Renewable electricity: ~35% (Dec 2024)

- Net-zero/100% renewables target by 2030

Technology and Automation Vendors

As Brambles shifts to Smart Assets, reliance on specialized IoT and analytics vendors rises; key suppliers hold technical IP that's hard to replace, creating vendor lock-in.

Switching platform costs—estimated in similar logistics firms at $5–20m for large-scale integrations in 2024—raise supplier strategic importance and can slow innovation adoption.

Supply chain squeeze: timber, fuel, drivers and IoT lock-in drive costs up

Suppliers exert moderate-to-high power: certified timber scarcity (18–22% FSC/PEFC in 2024) and 35% higher softwood costs 2021–23 raised pallet spend; carriers face diesel +18% (2023–24) and 80,000 US driver shortfall (2024); energy costs US$282m FY2024 with EU gas +40% (2023); IoT/vendor lock-in (switch costs $5–20m) adds strategic leverage.

| Metric | Value |

|---|---|

| FSC/PEFC supply | 18–22% (2024) |

| Softwood price rise | ~35% (2021–23) |

| Energy & fuel | US$282m FY2024 |

| EU gas spike | +40% (2023) |

| Diesel | +18% (2023–24) |

| Driver shortfall | ~80,000 US (2024) |

| Platform switch cost | $5–20m (2024) |

What is included in the product

Concise Porter's Five Forces analysis tailored to Brambles that uncovers competitive intensity, buyer and supplier power, entry barriers, and substitution risks, highlighting strategic levers to sustain market position.

Concise Porter's Five Forces summary for Brambles—quickly pinpoint supply chain and competitive pressures to guide strategic moves.

Customers Bargaining Power

Concentration of Retail Giants

Low Switching Costs for Large Scale Users

Large clients can swap to white-wood pallets or rival poolers, keeping bargaining power high despite Brambles’ integrated CHEP model; transitioning logistics are costly but doable for big retailers handling millions of units.

In 2024 Brambles reported 2024 revenue of US$6.0bn and 172m pooled units in circulation, so customers use threat of exit as leverage at renewals.

Brambles counters by selling value-added logistics data and analytics—Chep data services claim to cut inventory days and shrinkage by mid-single digits—making the service harder to treat as a simple commodity.

Price Sensitivity in Low-Margin Sectors

Demand for Sustainability Reporting

Modern corporate customers demand granular carbon footprint and circularity metrics; 72% of global supply-chain buyers cited ESG data as critical in a 2024 McKinsey survey.

If Brambles cannot match competitors’ ESG reporting, large clients—responsible for ~40% of pallet spend in FMCG—may switch to providers aligned with their 2030 net-zero plans.

This makes sustainability a non-negotiable service feature, increasing customer bargaining power and pressuring margins and capex for upgraded reporting systems.

- 72% of buyers: ESG data critical (McKinsey 2024)

- ~40% pallet spend from large FMCG clients

- Failure to match ESG reporting → client churn

Internal Logistics Optimization

Sophisticated customers now use their own analytics to cut pallet dwell time and loss rates, lowering Brambles’ fee revenue; industry pilots in 2024 showed asset velocity gains of 12–18%, trimming client pallet spend by ~8% annually.

As customers spend less, Brambles sees indirect pressure on top-line growth; in FY2024 Brambles reported 3% organic revenue growth, partly offset by higher asset utilization rates.

Brambles should co-share velocity gains via revenue-sharing or tiered pricing so both parties keep value; a 50/50 uplift split on incremental returns could preserve service margins.

- Customers reduce pallet spend ~8% via analytics

- Asset velocity gains 12–18% in 2024 pilots

- FY2024 Brambles organic revenue +3%

- Suggest revenue-share or tiered pricing (e.g., 50/50)

Brambles must shift to value/share pricing as top customers squeeze margins, ESG & data offset

| Metric | 2024 value |

|---|---|

| Group revenue (US$) | 6.0bn |

| Pooled units | 172m |

| % revenue from top-tier accounts | 75% |

| Asset velocity gains (pilot) | 12–18% |

| Client spend reduction | ~8% |

| Buyers citing ESG critical (McKinsey) | 72% |

Preview the Actual Deliverable

Brambles Porter's Five Forces Analysis

This preview shows the exact Brambles Porter’s Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders; the full, professionally formatted document is ready for download and use the moment you buy.

You're viewing the actual, complete analysis file covering competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry; upon payment you’ll get instant access to this identical deliverable.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

Brambles faces moderate supplier power but benefits from scale in pallet pooling while buyer concentration and cost sensitivity create pricing pressure; threats from new entrants are low but substitutes and tech-driven logistics shifts raise strategic risk. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Brambles’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Raw Material Price Volatility

Brambles relies on global lumber and plastic resins for CHEP pallets; timber price swings raised global softwood lumber prices ~35% in 2021–2023, lifting pallet capex and repair costs and increasing FY2024 pallet replacement spending by an estimated mid-single-digit percentage.

Reliance on Specialized Sawmills

Brambles needs high-quality, sustainably sourced timber that meets strict durability for pooling; that narrows viable suppliers to specialized sawmills able to deliver volume plus FSC or PEFC certification.

Only an estimated 18–22% of global softwood suppliers held FSC/PEFC chain-of-custody in 2024, so certified sawmills exert moderate leverage over Brambles’ procurement.

Rising regulation and corporate sourcing targets (EU Deforestation Regulation effective 2021, many buyers targeting 2025–30) increase supplier bargaining power and pricing pressure.

Logistics and Transportation Providers

The circular model depends on thousands of third-party carriers to return empties; in 2024 Brambles moved ~2.5bn pallet journeys globally, so transport is critical.

Rising diesel prices (up ~18% year‑on‑year in 2023–24) and US/EU trucker shortages (shortfall ~80,000 drivers in 2024) boost carriers’ fee power.

Brambles uses long‑term contracts and its Trax/Dynamics route optimization; these cut empty-km by ~12% in pilot regions, but regional capacity limits still raise spot rates.

Energy Costs for Manufacturing

Energy use for plastic container production and automated service centers is material: Brambles reported energy and fuel costs of US$282m in FY2024, up 6% year-on-year, exposing it to electricity and gas price swings in Europe and North America.

Suppliers wield bargaining power via regulated tariffs and market spikes—European wholesale gas prices rose ~40% in 2023 vs 2022—pressuring margins for energy-intensive ops.

Brambles mitigates risk by spending on efficiency and renewables: as of Dec 2024 it sourced ~35% of electricity from renewables and targets 100% by 2030 to stabilize long-term costs.

- FY2024 energy & fuel expense: US$282m

- European gas spot +~40% in 2023 vs 2022

- Renewable electricity: ~35% (Dec 2024)

- Net-zero/100% renewables target by 2030

Technology and Automation Vendors

As Brambles shifts to Smart Assets, reliance on specialized IoT and analytics vendors rises; key suppliers hold technical IP that's hard to replace, creating vendor lock-in.

Switching platform costs—estimated in similar logistics firms at $5–20m for large-scale integrations in 2024—raise supplier strategic importance and can slow innovation adoption.

Supply chain squeeze: timber, fuel, drivers and IoT lock-in drive costs up

Suppliers exert moderate-to-high power: certified timber scarcity (18–22% FSC/PEFC in 2024) and 35% higher softwood costs 2021–23 raised pallet spend; carriers face diesel +18% (2023–24) and 80,000 US driver shortfall (2024); energy costs US$282m FY2024 with EU gas +40% (2023); IoT/vendor lock-in (switch costs $5–20m) adds strategic leverage.

| Metric | Value |

|---|---|

| FSC/PEFC supply | 18–22% (2024) |

| Softwood price rise | ~35% (2021–23) |

| Energy & fuel | US$282m FY2024 |

| EU gas spike | +40% (2023) |

| Diesel | +18% (2023–24) |

| Driver shortfall | ~80,000 US (2024) |

| Platform switch cost | $5–20m (2024) |

What is included in the product

Concise Porter's Five Forces analysis tailored to Brambles that uncovers competitive intensity, buyer and supplier power, entry barriers, and substitution risks, highlighting strategic levers to sustain market position.

Concise Porter's Five Forces summary for Brambles—quickly pinpoint supply chain and competitive pressures to guide strategic moves.

Customers Bargaining Power

Concentration of Retail Giants

Low Switching Costs for Large Scale Users

Large clients can swap to white-wood pallets or rival poolers, keeping bargaining power high despite Brambles’ integrated CHEP model; transitioning logistics are costly but doable for big retailers handling millions of units.

In 2024 Brambles reported 2024 revenue of US$6.0bn and 172m pooled units in circulation, so customers use threat of exit as leverage at renewals.

Brambles counters by selling value-added logistics data and analytics—Chep data services claim to cut inventory days and shrinkage by mid-single digits—making the service harder to treat as a simple commodity.

Price Sensitivity in Low-Margin Sectors

Demand for Sustainability Reporting

Modern corporate customers demand granular carbon footprint and circularity metrics; 72% of global supply-chain buyers cited ESG data as critical in a 2024 McKinsey survey.

If Brambles cannot match competitors’ ESG reporting, large clients—responsible for ~40% of pallet spend in FMCG—may switch to providers aligned with their 2030 net-zero plans.

This makes sustainability a non-negotiable service feature, increasing customer bargaining power and pressuring margins and capex for upgraded reporting systems.

- 72% of buyers: ESG data critical (McKinsey 2024)

- ~40% pallet spend from large FMCG clients

- Failure to match ESG reporting → client churn

Internal Logistics Optimization

Sophisticated customers now use their own analytics to cut pallet dwell time and loss rates, lowering Brambles’ fee revenue; industry pilots in 2024 showed asset velocity gains of 12–18%, trimming client pallet spend by ~8% annually.

As customers spend less, Brambles sees indirect pressure on top-line growth; in FY2024 Brambles reported 3% organic revenue growth, partly offset by higher asset utilization rates.

Brambles should co-share velocity gains via revenue-sharing or tiered pricing so both parties keep value; a 50/50 uplift split on incremental returns could preserve service margins.

- Customers reduce pallet spend ~8% via analytics

- Asset velocity gains 12–18% in 2024 pilots

- FY2024 Brambles organic revenue +3%

- Suggest revenue-share or tiered pricing (e.g., 50/50)

Brambles must shift to value/share pricing as top customers squeeze margins, ESG & data offset

| Metric | 2024 value |

|---|---|

| Group revenue (US$) | 6.0bn |

| Pooled units | 172m |

| % revenue from top-tier accounts | 75% |

| Asset velocity gains (pilot) | 12–18% |

| Client spend reduction | ~8% |

| Buyers citing ESG critical (McKinsey) | 72% |

Preview the Actual Deliverable

Brambles Porter's Five Forces Analysis

This preview shows the exact Brambles Porter’s Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders; the full, professionally formatted document is ready for download and use the moment you buy.

You're viewing the actual, complete analysis file covering competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry; upon payment you’ll get instant access to this identical deliverable.