Bravura Solutions SWOT Analysis

Dive Deeper Into the Company’s Strategic Blueprint

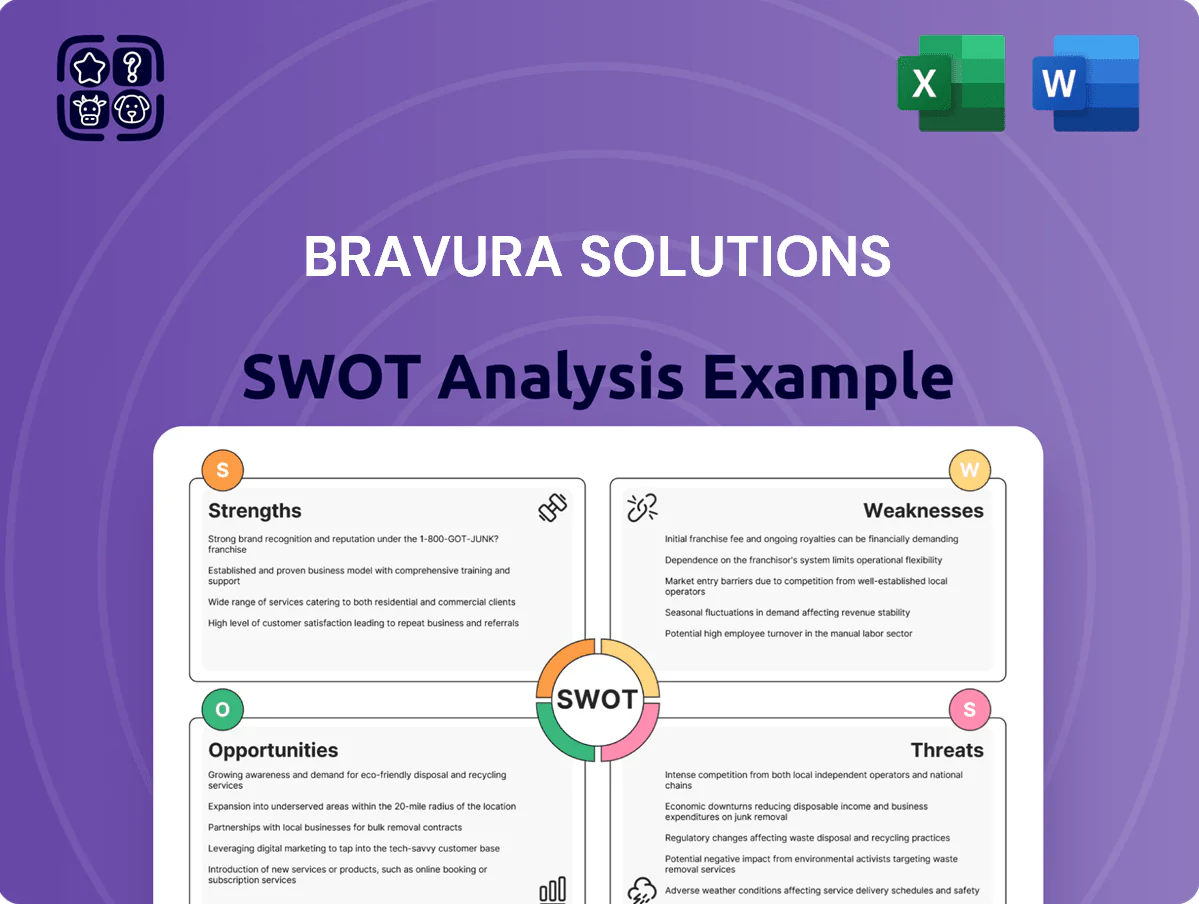

Bravura Solutions shows strong global footholds in wealth and fund administration software, but faces integration and competitive pressures amid tech shifts; our full SWOT unpacks these dynamics with financial context and strategic options. Purchase the complete analysis to receive a professionally written, editable Word report plus an Excel matrix—ready for investor pitches, strategy planning, or due diligence.

Strengths

Leading Market Position in Wealth Tech

Bravura Solutions holds a dominant footprint in Australian and UK wealth management, serving roughly 60% of Australian superannuation funds and 35% of UK pension administrators as of Dec 2025, providing mission-critical admin platforms to major banks and fund managers.

By end-2025 it was the primary provider for complex superannuation and pension administration, supporting over A$1.2 trillion in assets under administration (AUA).

That scale and integration generate high switching costs—platform migrations often exceed 12–24 months and millions in transition spend—creating effective barriers to entry for new competitors.

High Proportion of Recurring Revenue

Bravura Solutions derives roughly 70% of FY2024 revenue from recurring subscription and maintenance fees, giving valuation stability and predictable cash flow—FY2024 recurring revenue NZD 190m of total NZD 270m.

Long-term contracts with Tier 1 banks and asset managers—multi-year deals covering ~60% of recurring bookings—sustain income through market volatility, as seen during 2022–24 downturns.

This steady cash allows planning and reinvestment: R&D spend rose to NZD 34m in FY2024 (up 18% year-over-year), funding product roadmaps and client-specific enhancements.

Successful Operational Transformation Completion

Following multi-year restructuring, Bravura Solutions entered 2026 with a leaner operating model after cutting ~18% of global headcount and consolidating offshore centres, lifting FY2025 adjusted EBIT margin to 12.8% (from 7.1% in FY2022).

Optimised delivery and lower SG&A reduced opex by ~23% versus FY2022, restoring investor confidence: share price rose ~34% in 2025 and net debt fell to AU$45m at Dec 31, 2025, supporting profitable growth.

Deep Regulatory and Domain Expertise

Bravura holds deep regulatory and domain expertise across jurisdictions, notably the UK and Australia, embedding pension and financial-regulation rules into its platforms so clients stay compliant as laws change; in 2024 Bravura serviced over 1,200 clients globally, many in pensions and wealth, reducing client compliance incidents by reported 18% year‑on‑year.

That domain-specific IP—decades of rules, templates, and audit trails—is costly and time-consuming for generic providers to replicate, giving Bravura defensible product differentiation and higher switching costs for customers.

- Coverage: UK, Australia core markets

- Clients: 1,200+ global (2024)

- Compliance incidents down 18% YoY (2024)

- High switching costs due to embedded IP

Robust Sonata Platform Adoption

The Sonata platform remains Bravura Solutions’ flagship, unifying wealth management and life insurance administration and serving 230+ clients globally as of Dec 2025.

By late 2025 Sonata supports pensions, investments, annuities and retail banking products, driving 18% year‑over‑year SaaS revenue growth and broadening its client mix.

Its consolidation of legacy stacks into one modern interface reduces client IT spend by ~30% in pilot cases, a key selling point for large enterprises.

- 230+ clients (Dec 2025)

- Supports pensions, investments, annuities, retail banking

- 18% YoY SaaS revenue growth (2025)

- ~30% estimated legacy IT cost reduction

Bravura: Dominant AU/UK pension platform—A$1.2T AUA, NZD190m recurring, 12.8% EBIT

Bravura dominates UK/Australia wealth with ~60% AU super funds and 35% UK pension admins (Dec 2025), AUA ~A$1.2T, recurring FY2024 revenue NZD 190m of NZD 270m, 70% recurring, Sonata: 230+ clients, 18% SaaS YoY growth, lower opex (−23% vs FY2022) and FY2025 adj. EBIT margin 12.8%; high switching costs from deep regulatory IP.

| Metric | Value |

|---|---|

| AUA | A$1.2T (Dec 2025) |

| Recurring Rev FY2024 | NZD 190m |

| Sonata clients | 230+ |

| Adj EBIT margin FY2025 | 12.8% |

What is included in the product

Provides a concise SWOT overview of Bravura Solutions, highlighting its core strengths and weaknesses while mapping external opportunities and threats shaping the company’s strategic outlook.

Delivers a focused SWOT snapshot tailored to Bravura Solutions, enabling rapid strategic alignment and clear communication across teams for quicker, data-driven decisions.

Weaknesses

Geographic Revenue Concentration

About 58% of Bravura Solutions’ FY2024 revenue came from the UK (34%) and Australia (24%), leaving it exposed to country-specific shocks and regulatory shifts such as the UK Financial Conduct Authority changes in 2023 and APRA guidance in 2022.

Legacy Infrastructure Maintenance Costs

Bravura Solutions still supports multiple legacy platforms for long-term clients, consuming ~18–22% of FY2024 R&D spend and requiring specialized engineers at higher salary bands. This maintenance burden diverts capital from cloud-native product development and contributed to a 1.4ppt slower annual feature-release cadence versus cloud-first peers in 2024. That technical debt risks slower product evolution and competitive pressure on pricing.

Lengthy Sales and Implementation Cycles

The enterprise scope of Bravura Solutions' software drives sales and implementation cycles that can stretch 12–36 months, delaying revenue recognition and front-loading costs; in FY2024 the firm reported implementation-related deferred revenue representing ~18% of total contract value. These long lead times raise risk of project overruns and shifting client priorities during onboarding, increasing chance of milestone slippage. Resulting delays contribute to quarterly earnings volatility and can strain client relationships when deliverables miss agreed dates.

Historical Profitability Volatility

Despite EBITDA recovery in FY2024 (A$38.2m) and a positive FY2025 guidance, Bravura Solutions recorded large impairment charges—A$62.4m in FY2022—that drove negative equity trends and uneven net income across 2019–2023.

Investors question sustainability of current margins after volatile years; analysts want a 3–5 year streak of rising EPS before rerating the stock.

- FY2022 impairment A$62.4m

- FY2024 EBITDA A$38.2m

- No multi-year EPS growth 2019–2023

- Analyst rerating needs 3–5 years of consistent net profit

Dependency on Key Tier 1 Clients

Bravura Solutions derives an estimated 40–55% of FY2024 revenue from a handful of Tier 1 banks and insurers, so losing one major contract or a client insourcing tech would hit revenue and EBITDA disproportionately.

High client concentration gives those Tier 1 customers leverage at renewals, evidenced by margin pressure in 2023–24 where gross margin fell ~150 basis points versus 2021–22.

- 40–55% revenue from few Tier 1 clients

- Loss of one client risks double-digit revenue decline

- Renewal leverage compressed margins ~150 bps (2023–24)

High client & regional concentration, heavy tech debt; EBITDA steady, rerate years away

Concentration: 58% revenue UK/Australia; 40–55% from few Tier‑1 clients, risking double‑digit hit if one leaves. Tech debt: legacy platforms eat 18–22% of FY2024 R&D, slowing releases by 1.4ppt versus cloud peers. Financials: FY2022 impairment A$62.4m; FY2024 EBITDA A$38.2m; no multi‑year EPS growth 2019–2023; analyst rerate needs 3–5 years.

| Metric | Value |

|---|---|

| UK+AU share FY2024 | 58% |

| Tier‑1 client revenue | 40–55% |

| R&D on legacy | 18–22% |

| Feature cadence gap | 1.4 ppt |

| FY2022 impairment | A$62.4m |

| FY2024 EBITDA | A$38.2m |

What You See Is What You Get

Bravura Solutions SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report you'll get; buying unlocks the complete, editable version with all strengths, weaknesses, opportunities, and threats fully detailed.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Dive Deeper Into the Company’s Strategic Blueprint

Bravura Solutions shows strong global footholds in wealth and fund administration software, but faces integration and competitive pressures amid tech shifts; our full SWOT unpacks these dynamics with financial context and strategic options. Purchase the complete analysis to receive a professionally written, editable Word report plus an Excel matrix—ready for investor pitches, strategy planning, or due diligence.

Strengths

Leading Market Position in Wealth Tech

Bravura Solutions holds a dominant footprint in Australian and UK wealth management, serving roughly 60% of Australian superannuation funds and 35% of UK pension administrators as of Dec 2025, providing mission-critical admin platforms to major banks and fund managers.

By end-2025 it was the primary provider for complex superannuation and pension administration, supporting over A$1.2 trillion in assets under administration (AUA).

That scale and integration generate high switching costs—platform migrations often exceed 12–24 months and millions in transition spend—creating effective barriers to entry for new competitors.

High Proportion of Recurring Revenue

Bravura Solutions derives roughly 70% of FY2024 revenue from recurring subscription and maintenance fees, giving valuation stability and predictable cash flow—FY2024 recurring revenue NZD 190m of total NZD 270m.

Long-term contracts with Tier 1 banks and asset managers—multi-year deals covering ~60% of recurring bookings—sustain income through market volatility, as seen during 2022–24 downturns.

This steady cash allows planning and reinvestment: R&D spend rose to NZD 34m in FY2024 (up 18% year-over-year), funding product roadmaps and client-specific enhancements.

Successful Operational Transformation Completion

Following multi-year restructuring, Bravura Solutions entered 2026 with a leaner operating model after cutting ~18% of global headcount and consolidating offshore centres, lifting FY2025 adjusted EBIT margin to 12.8% (from 7.1% in FY2022).

Optimised delivery and lower SG&A reduced opex by ~23% versus FY2022, restoring investor confidence: share price rose ~34% in 2025 and net debt fell to AU$45m at Dec 31, 2025, supporting profitable growth.

Deep Regulatory and Domain Expertise

Bravura holds deep regulatory and domain expertise across jurisdictions, notably the UK and Australia, embedding pension and financial-regulation rules into its platforms so clients stay compliant as laws change; in 2024 Bravura serviced over 1,200 clients globally, many in pensions and wealth, reducing client compliance incidents by reported 18% year‑on‑year.

That domain-specific IP—decades of rules, templates, and audit trails—is costly and time-consuming for generic providers to replicate, giving Bravura defensible product differentiation and higher switching costs for customers.

- Coverage: UK, Australia core markets

- Clients: 1,200+ global (2024)

- Compliance incidents down 18% YoY (2024)

- High switching costs due to embedded IP

Robust Sonata Platform Adoption

The Sonata platform remains Bravura Solutions’ flagship, unifying wealth management and life insurance administration and serving 230+ clients globally as of Dec 2025.

By late 2025 Sonata supports pensions, investments, annuities and retail banking products, driving 18% year‑over‑year SaaS revenue growth and broadening its client mix.

Its consolidation of legacy stacks into one modern interface reduces client IT spend by ~30% in pilot cases, a key selling point for large enterprises.

- 230+ clients (Dec 2025)

- Supports pensions, investments, annuities, retail banking

- 18% YoY SaaS revenue growth (2025)

- ~30% estimated legacy IT cost reduction

Bravura: Dominant AU/UK pension platform—A$1.2T AUA, NZD190m recurring, 12.8% EBIT

Bravura dominates UK/Australia wealth with ~60% AU super funds and 35% UK pension admins (Dec 2025), AUA ~A$1.2T, recurring FY2024 revenue NZD 190m of NZD 270m, 70% recurring, Sonata: 230+ clients, 18% SaaS YoY growth, lower opex (−23% vs FY2022) and FY2025 adj. EBIT margin 12.8%; high switching costs from deep regulatory IP.

| Metric | Value |

|---|---|

| AUA | A$1.2T (Dec 2025) |

| Recurring Rev FY2024 | NZD 190m |

| Sonata clients | 230+ |

| Adj EBIT margin FY2025 | 12.8% |

What is included in the product

Provides a concise SWOT overview of Bravura Solutions, highlighting its core strengths and weaknesses while mapping external opportunities and threats shaping the company’s strategic outlook.

Delivers a focused SWOT snapshot tailored to Bravura Solutions, enabling rapid strategic alignment and clear communication across teams for quicker, data-driven decisions.

Weaknesses

Geographic Revenue Concentration

About 58% of Bravura Solutions’ FY2024 revenue came from the UK (34%) and Australia (24%), leaving it exposed to country-specific shocks and regulatory shifts such as the UK Financial Conduct Authority changes in 2023 and APRA guidance in 2022.

Legacy Infrastructure Maintenance Costs

Bravura Solutions still supports multiple legacy platforms for long-term clients, consuming ~18–22% of FY2024 R&D spend and requiring specialized engineers at higher salary bands. This maintenance burden diverts capital from cloud-native product development and contributed to a 1.4ppt slower annual feature-release cadence versus cloud-first peers in 2024. That technical debt risks slower product evolution and competitive pressure on pricing.

Lengthy Sales and Implementation Cycles

The enterprise scope of Bravura Solutions' software drives sales and implementation cycles that can stretch 12–36 months, delaying revenue recognition and front-loading costs; in FY2024 the firm reported implementation-related deferred revenue representing ~18% of total contract value. These long lead times raise risk of project overruns and shifting client priorities during onboarding, increasing chance of milestone slippage. Resulting delays contribute to quarterly earnings volatility and can strain client relationships when deliverables miss agreed dates.

Historical Profitability Volatility

Despite EBITDA recovery in FY2024 (A$38.2m) and a positive FY2025 guidance, Bravura Solutions recorded large impairment charges—A$62.4m in FY2022—that drove negative equity trends and uneven net income across 2019–2023.

Investors question sustainability of current margins after volatile years; analysts want a 3–5 year streak of rising EPS before rerating the stock.

- FY2022 impairment A$62.4m

- FY2024 EBITDA A$38.2m

- No multi-year EPS growth 2019–2023

- Analyst rerating needs 3–5 years of consistent net profit

Dependency on Key Tier 1 Clients

Bravura Solutions derives an estimated 40–55% of FY2024 revenue from a handful of Tier 1 banks and insurers, so losing one major contract or a client insourcing tech would hit revenue and EBITDA disproportionately.

High client concentration gives those Tier 1 customers leverage at renewals, evidenced by margin pressure in 2023–24 where gross margin fell ~150 basis points versus 2021–22.

- 40–55% revenue from few Tier 1 clients

- Loss of one client risks double-digit revenue decline

- Renewal leverage compressed margins ~150 bps (2023–24)

High client & regional concentration, heavy tech debt; EBITDA steady, rerate years away

Concentration: 58% revenue UK/Australia; 40–55% from few Tier‑1 clients, risking double‑digit hit if one leaves. Tech debt: legacy platforms eat 18–22% of FY2024 R&D, slowing releases by 1.4ppt versus cloud peers. Financials: FY2022 impairment A$62.4m; FY2024 EBITDA A$38.2m; no multi‑year EPS growth 2019–2023; analyst rerate needs 3–5 years.

| Metric | Value |

|---|---|

| UK+AU share FY2024 | 58% |

| Tier‑1 client revenue | 40–55% |

| R&D on legacy | 18–22% |

| Feature cadence gap | 1.4 ppt |

| FY2022 impairment | A$62.4m |

| FY2024 EBITDA | A$38.2m |

What You See Is What You Get

Bravura Solutions SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report you'll get; buying unlocks the complete, editable version with all strengths, weaknesses, opportunities, and threats fully detailed.