Bread Financial Holdings Business Model Canvas

Bread Financial: Business Model Canvas Decoded — How Credit & Loyalty Scale Revenue

Unlock the full strategic blueprint behind Bread Financial Holdings’s business model—this concise Business Model Canvas maps customer segments, value propositions, key partners, and revenue mechanics to reveal how the company scales and monetizes credit and loyalty solutions.

Partnerships

Retail and Brand Partners

Bread Financial partners with major retailers in apparel, home goods, and specialty sectors to embed point-of-sale financing; these integrations drove 62% of new account originations and 68% of transaction volume through 2025, per company disclosures. By year-end 2025, retail-brand channels remained the primary engine for customer acquisition and loan receivable growth, supporting a 14% YoY rise in merchant-funded receivables.

Payment Networks

Strategic alliances with Visa, Mastercard, and American Express let Bread Financial’s co-branded cards work at 100+ million merchant locations worldwide, expanding use beyond partner stores and boosting purchase volume; in 2024 Bread reported 12% year-over-year growth in card transaction volume, driven by network reach and cross-border acceptance.

Technology and Fintech Providers

Collaborations with cloud providers (AWS, Azure) and fintech software firms let Bread Financial keep a modern, agile tech stack, cutting deployment times by ~40% and supporting digital-first products that drove 2024 digital originations to roughly 62% of new accounts.

Financial Institutions and Regulators

As a regulated lender, Bread Financial holds ongoing ties with federal and state banking regulators and partner banks for compliance and liquidity; at year-end 2024 Bread reported $4.2 billion in total financing commitments and noted regulatory capital ratios aligned with supervisory expectations.

Those partnerships secure access to diversified funding—including warehouse lines and securitizations that funded ~45% of receivables in 2024—and ensure adherence to evolving consumer-lending rules, a prerequisite for deposit-taking and lending activities.

- 2024 financing commitments: $4.2B

- Securitization funding share: ~45% of receivables

- Regulatory capital: maintained within supervisory ranges (2024)

Marketing and Data Affiliates

Partnerships with data analytics firms and marketing agencies help Bread Financial cut customer acquisition costs and boost retention by enabling targeted credit offers and personalized loyalty programs; in 2024 Bread reported originations of $2.7 billion, where higher-quality targeted origination raised approval rates by ~12% in pilot segments.

Leveraging external data streams improved Bread’s proprietary scoring and risk models, trimming 60-day delinquencies by ~8% in 2024 and supporting a net charge-off rate near 3.5%.

- Targeted offers raised approval efficiency ~12%

- 60-day delinquencies fell ~8% (2024)

- Net charge-off ~3.5% (2024)

- Originations $2.7B (2024)

Bread Financial partnerships fuel 62% new accounts, $2.7B originations, 68% volume

Bread Financial’s key partnerships—retail brands, Visa/Mastercard/AmEx, cloud providers, banks, securitization counterparties, and analytics firms—drove 62% of new accounts, 68% of transaction volume, $2.7B originations (2024), $4.2B financing commitments (2024), ~45% receivables funded via securitizations, net charge-off ~3.5% (2024).

| Metric | 2024/2025 |

|---|---|

| New account share (retail) | 62% |

| Txn volume via partners | 68% |

| Originations | $2.7B |

| Financing commitments | $4.2B |

| Securitization share | ~45% |

| Net charge-off | ~3.5% |

What is included in the product

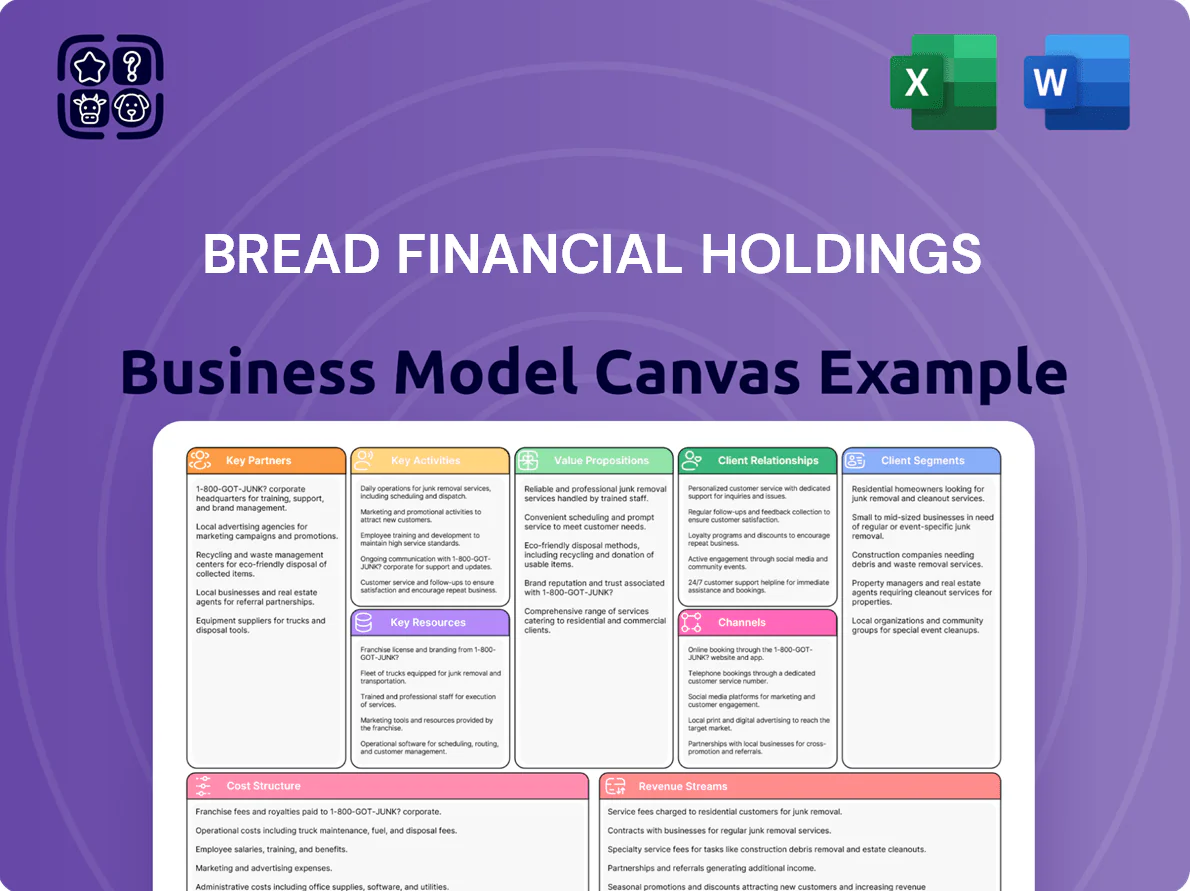

A concise, pre-written Business Model Canvas for Bread Financial Holdings outlining customer segments, channels, value propositions, revenue streams, cost structure, key activities, resources, partners, and customer relationships.

Condenses Bread Financial Holdings’ payments and credit ecosystem into a one-page, editable Business Model Canvas—ideal for quickly identifying revenue drivers, partner networks, and customer pain relievers for boardrooms or team workshops.

Activities

Credit Underwriting and Risk Management

Bread Financial underwrites credit using machine learning and alternative data (transaction, purchase, and bureau signals) to score applicants, aiming to grow receivables while keeping net charge-offs near recent levels (3.4% in 2024 annualized); models and thresholds shift with real‑time macro inputs—unemployment, CPI, and delinquency trends—updated weekly to trim risk and preserve portfolio ROE.

Product Development and Innovation

Bread Financial builds private-label and co-brand credit cards plus BNPL plans, launching 20+ merchant programs in 2024 and growing receivables to $4.1B as of Q4 2024; R&D prioritizes seamless digital UX and embedded finance APIs to boost merchant conversion and repeat spend.

Marketing and Merchant Integration

Bread Financial onboards retailers by integrating APIs and custom point-of-sale lending, tailoring BNPL and installment terms to merchant branding and sales targets; in 2024 Bread reported ~2,000 active merchant partners and originated $1.1B in receivables tied to merchant programs.

Customer Service and Collections

Customer service and collections at Bread Financial manage billing inquiries, disputes, and payments across the lifecycle, using CRM and payment platforms that handled roughly $7.4 billion in receivables as of FY 2024.

Collections teams pursue past-due balances with compliant workflows; Bread reported a 90+ day net charge-off rate near 6% in 2024, so high-quality service supports retention and lowers loss rates.

- End-to-end support: billing, disputes, payments

- Receivables: ~$7.4B (FY2024)

- 90+ day net charge-offs: ~6% (2024)

- Compliance-driven collections workflows

- Service quality tied to retention & brand

Regulatory Compliance and Reporting

Bread Financial must follow consumer protection, AML, and capital rules; in 2024 it spent an estimated 8–10% of operating expenses on compliance and reported a CET1-equivalent capital buffer above regulatory minima to regulators.

Internal audits, legal reviews, and monthly financial reporting reduce legal risk and support stability; Bread closed 2024 with a loan loss reserve coverage ratio near 6% and regulatory filings on schedule.

- 8–10% of OpEx on compliance

- CET1-equivalent buffer above minimum

- Loan loss reserve coverage ≈ 6% in 2024

- Monthly filings and regular audits

Bread Financial: $7.4B receivables, $1.1B merchant originations, 3.4% NCO (2024)

Bread Financial underwrites credit via ML and alternative data, keeping net charge-offs ~3.4% (2024 annualized) and receivables $7.4B (FY2024) while launching 20+ merchant programs and $1.1B merchant-originated receivables in 2024.

| Metric | Value |

|---|---|

| Receivables | $7.4B (FY2024) |

| Merchant receivables | $1.1B (2024) |

| Net charge-offs | 3.4% (2024 ann.) |

| 90+ day NCO | ~6% (2024) |

| Merchants | ~2,000 (2024) |

Preview Before You Purchase

Business Model Canvas

The document you're previewing is the authentic Bread Financial Holdings Business Model Canvas—not a mockup or sample—and it matches the exact file you'll receive after purchase.

When you complete your order, you'll get full access to this same professional, ready-to-use document, formatted and structured exactly as shown for immediate editing and presentation.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Bread Financial: Business Model Canvas Decoded — How Credit & Loyalty Scale Revenue

Unlock the full strategic blueprint behind Bread Financial Holdings’s business model—this concise Business Model Canvas maps customer segments, value propositions, key partners, and revenue mechanics to reveal how the company scales and monetizes credit and loyalty solutions.

Partnerships

Retail and Brand Partners

Bread Financial partners with major retailers in apparel, home goods, and specialty sectors to embed point-of-sale financing; these integrations drove 62% of new account originations and 68% of transaction volume through 2025, per company disclosures. By year-end 2025, retail-brand channels remained the primary engine for customer acquisition and loan receivable growth, supporting a 14% YoY rise in merchant-funded receivables.

Payment Networks

Strategic alliances with Visa, Mastercard, and American Express let Bread Financial’s co-branded cards work at 100+ million merchant locations worldwide, expanding use beyond partner stores and boosting purchase volume; in 2024 Bread reported 12% year-over-year growth in card transaction volume, driven by network reach and cross-border acceptance.

Technology and Fintech Providers

Collaborations with cloud providers (AWS, Azure) and fintech software firms let Bread Financial keep a modern, agile tech stack, cutting deployment times by ~40% and supporting digital-first products that drove 2024 digital originations to roughly 62% of new accounts.

Financial Institutions and Regulators

As a regulated lender, Bread Financial holds ongoing ties with federal and state banking regulators and partner banks for compliance and liquidity; at year-end 2024 Bread reported $4.2 billion in total financing commitments and noted regulatory capital ratios aligned with supervisory expectations.

Those partnerships secure access to diversified funding—including warehouse lines and securitizations that funded ~45% of receivables in 2024—and ensure adherence to evolving consumer-lending rules, a prerequisite for deposit-taking and lending activities.

- 2024 financing commitments: $4.2B

- Securitization funding share: ~45% of receivables

- Regulatory capital: maintained within supervisory ranges (2024)

Marketing and Data Affiliates

Partnerships with data analytics firms and marketing agencies help Bread Financial cut customer acquisition costs and boost retention by enabling targeted credit offers and personalized loyalty programs; in 2024 Bread reported originations of $2.7 billion, where higher-quality targeted origination raised approval rates by ~12% in pilot segments.

Leveraging external data streams improved Bread’s proprietary scoring and risk models, trimming 60-day delinquencies by ~8% in 2024 and supporting a net charge-off rate near 3.5%.

- Targeted offers raised approval efficiency ~12%

- 60-day delinquencies fell ~8% (2024)

- Net charge-off ~3.5% (2024)

- Originations $2.7B (2024)

Bread Financial partnerships fuel 62% new accounts, $2.7B originations, 68% volume

Bread Financial’s key partnerships—retail brands, Visa/Mastercard/AmEx, cloud providers, banks, securitization counterparties, and analytics firms—drove 62% of new accounts, 68% of transaction volume, $2.7B originations (2024), $4.2B financing commitments (2024), ~45% receivables funded via securitizations, net charge-off ~3.5% (2024).

| Metric | 2024/2025 |

|---|---|

| New account share (retail) | 62% |

| Txn volume via partners | 68% |

| Originations | $2.7B |

| Financing commitments | $4.2B |

| Securitization share | ~45% |

| Net charge-off | ~3.5% |

What is included in the product

A concise, pre-written Business Model Canvas for Bread Financial Holdings outlining customer segments, channels, value propositions, revenue streams, cost structure, key activities, resources, partners, and customer relationships.

Condenses Bread Financial Holdings’ payments and credit ecosystem into a one-page, editable Business Model Canvas—ideal for quickly identifying revenue drivers, partner networks, and customer pain relievers for boardrooms or team workshops.

Activities

Credit Underwriting and Risk Management

Bread Financial underwrites credit using machine learning and alternative data (transaction, purchase, and bureau signals) to score applicants, aiming to grow receivables while keeping net charge-offs near recent levels (3.4% in 2024 annualized); models and thresholds shift with real‑time macro inputs—unemployment, CPI, and delinquency trends—updated weekly to trim risk and preserve portfolio ROE.

Product Development and Innovation

Bread Financial builds private-label and co-brand credit cards plus BNPL plans, launching 20+ merchant programs in 2024 and growing receivables to $4.1B as of Q4 2024; R&D prioritizes seamless digital UX and embedded finance APIs to boost merchant conversion and repeat spend.

Marketing and Merchant Integration

Bread Financial onboards retailers by integrating APIs and custom point-of-sale lending, tailoring BNPL and installment terms to merchant branding and sales targets; in 2024 Bread reported ~2,000 active merchant partners and originated $1.1B in receivables tied to merchant programs.

Customer Service and Collections

Customer service and collections at Bread Financial manage billing inquiries, disputes, and payments across the lifecycle, using CRM and payment platforms that handled roughly $7.4 billion in receivables as of FY 2024.

Collections teams pursue past-due balances with compliant workflows; Bread reported a 90+ day net charge-off rate near 6% in 2024, so high-quality service supports retention and lowers loss rates.

- End-to-end support: billing, disputes, payments

- Receivables: ~$7.4B (FY2024)

- 90+ day net charge-offs: ~6% (2024)

- Compliance-driven collections workflows

- Service quality tied to retention & brand

Regulatory Compliance and Reporting

Bread Financial must follow consumer protection, AML, and capital rules; in 2024 it spent an estimated 8–10% of operating expenses on compliance and reported a CET1-equivalent capital buffer above regulatory minima to regulators.

Internal audits, legal reviews, and monthly financial reporting reduce legal risk and support stability; Bread closed 2024 with a loan loss reserve coverage ratio near 6% and regulatory filings on schedule.

- 8–10% of OpEx on compliance

- CET1-equivalent buffer above minimum

- Loan loss reserve coverage ≈ 6% in 2024

- Monthly filings and regular audits

Bread Financial: $7.4B receivables, $1.1B merchant originations, 3.4% NCO (2024)

Bread Financial underwrites credit via ML and alternative data, keeping net charge-offs ~3.4% (2024 annualized) and receivables $7.4B (FY2024) while launching 20+ merchant programs and $1.1B merchant-originated receivables in 2024.

| Metric | Value |

|---|---|

| Receivables | $7.4B (FY2024) |

| Merchant receivables | $1.1B (2024) |

| Net charge-offs | 3.4% (2024 ann.) |

| 90+ day NCO | ~6% (2024) |

| Merchants | ~2,000 (2024) |

Preview Before You Purchase

Business Model Canvas

The document you're previewing is the authentic Bread Financial Holdings Business Model Canvas—not a mockup or sample—and it matches the exact file you'll receive after purchase.

When you complete your order, you'll get full access to this same professional, ready-to-use document, formatted and structured exactly as shown for immediate editing and presentation.