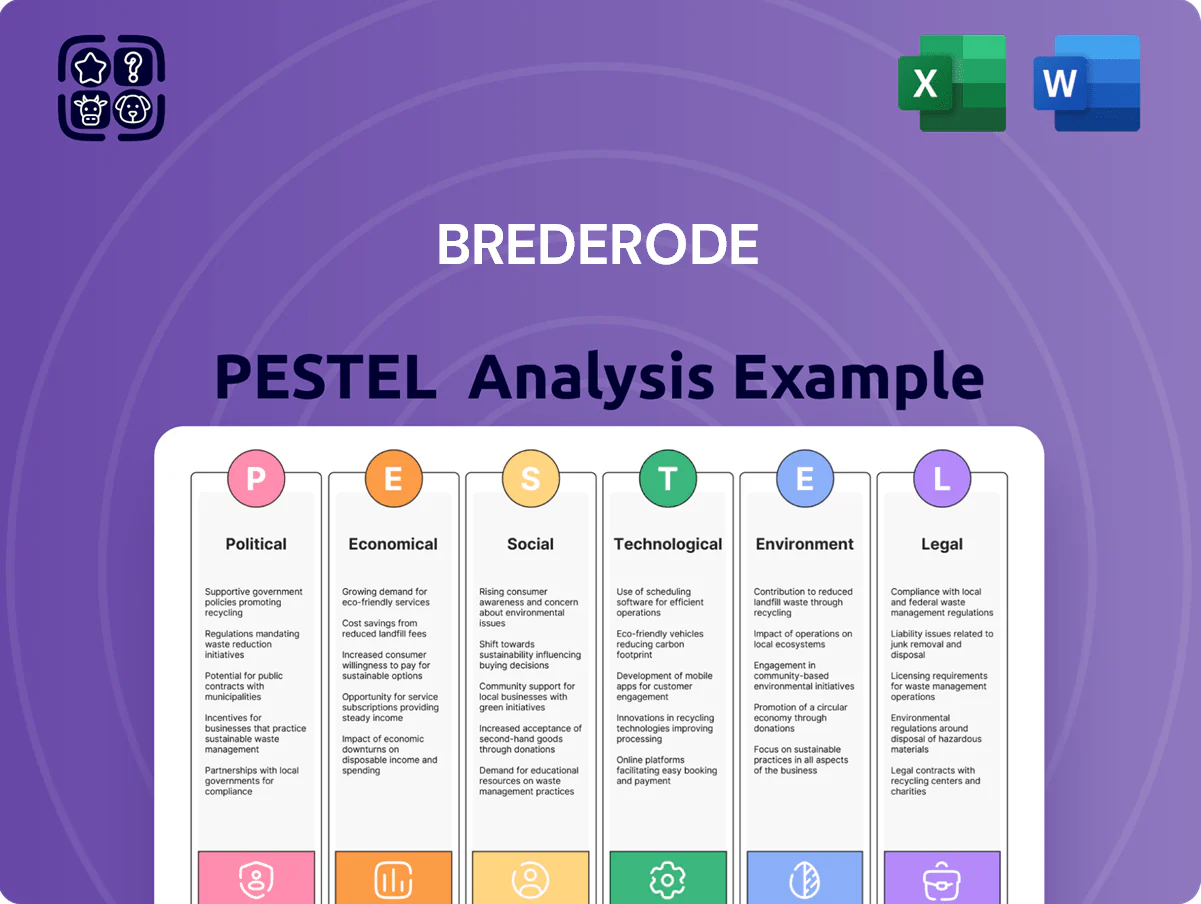

Brederode PESTLE Analysis

Skip the Research. Get the Strategy.

Discover how political shifts, economic cycles, and emerging technologies are reshaping Brederode’s strategic outlook in our concise PESTLE summary—ideal for investors and strategists seeking quick, actionable context. Purchase the full PESTLE analysis to access a detailed, editable report with risk assessments, trend forecasts, and strategic recommendations you can apply immediately.

Political factors

Geopolitical stability in Europe and North America

Brederode’s capital allocation into established EU and US markets makes its portfolio sensitive to geopolitical stability; in 2025 EU GDP growth slowed to 0.8% and US growth to 1.5%, raising downside risk for core holdings.

Recent 2024–25 transatlantic trade frictions and tariff threats prompted a 3–5% re-rating of comparable equity portfolios, directly affecting Brederode’s NAV sensitivity.

The firm depends on predictable governance—low expropriation risk in OECD countries (Worldwide Governance Indicator scores ~80th percentile) supports its multi-year investment horizon.

Shifting trade policies and protectionism

The rise in protectionist measures—global tariffs rose 12% between 2020–2024 per WTO reports—threatens Brederode’s export-heavy portfolio by increasing input costs and disrupting supply chains for minority-held industrial firms.

A 2024 IMF estimate showing a 6% decline in trade openness in some EU partners forces Brederode to reassess minority-stake governance, hedging strategies, and supplier diversification to preserve margins.

EU political moves toward strategic autonomy, backed by €200+ billion in IPCEI and green-industrial funding through 2025, steer Brederode toward investments favoring local content and resilient domestic supply chains.

Fiscal policy and corporate taxation

Changes in corporate tax rates in Luxembourg (effective rate ~24.94% in 2024) and neighboring EU states directly impact Brederode’s net profit and dividend capacity; a 1 percentage-point rise could reduce distributable earnings by an estimated €2–3m annually given current taxable income levels. The OECD/G20 global minimum tax (15%) implementation by late 2025 alters jurisdictional attractiveness and may raise effective tax burdens on cross-border holdings. Ongoing political debates on wealth taxes and capital gains reforms in EU markets require close executive monitoring due to potential balance-sheet and shareholder-return implications.

Government subsidies for green transitions

- EU Green Deal: 1 trillion euro mobilization (2021–2030)

- Just Transition/CEF: multi-€bn funding to infrastructure

- Risk: 10–20% subsidy cut could impair asset valuations

Regulatory pressure on private equity

Rising political scrutiny across the EU has pushed for tougher transparency: proposals in 2024 aimed to expand reporting for investment vehicles, with the European Parliament noting a 22% rise in inquiries into private equity employment impacts since 2020.

EU focus on large investors’ effects on local jobs—citing cases where PE-backed restructurings affected thousands—means Brederode must bolster disclosures and stakeholder engagement to retain its social license as a major minority shareholder.

- 2024 EU proposals increase reporting scope for investment vehicles

- 22% rise in parliamentary inquiries on PE employment impacts since 2020

- Heightened transparency expectations affect Brederode’s social license

Brederode: moderate political risk—slower growth, higher tariffs, tighter taxes compress returns

Brederode faces moderate political risk: slowing EU/US growth (2025: EU 0.8%, US 1.5%) and 12% rise in global tariffs (2020–24) uplift downside; EU strategic autonomy and €200+bn IPCEI/green funding favor domestic supply-chain plays; OECD governance (≈80th pctile) lowers expropriation risk; tax shifts (Luxembourg ~24.94% 2024, 15% global minimum) and heightened transparency (22% rise in PE inquiries) compress net returns.

| Indicator | Value |

|---|---|

| EU GDP growth 2025 | 0.8% |

| US GDP growth 2025 | 1.5% |

| Global tariff change 2020–24 | +12% |

| Luxembourg effective tax 2024 | 24.94% |

| OECD governance pctile | ~80th |

| Rise in PE inquiries since 2020 | +22% |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal factors uniquely impact the Brederode, with each section grounded in current data and trends to highlight region- and industry-specific risks and opportunities.

Provides a concise, visually segmented PESTLE summary of Brederode that’s easy to drop into presentations or share across teams, helping stakeholders quickly assess external risks and align strategic planning.

Economic factors

Interest rate environment and cost of capital

As of late 2025, ECB and Fed benchmark rates near 4.25–5.00% have lifted discount rates for valuing Brederode’s unlisted assets, compressing valuations across private portfolios.

Higher rates raise average debt servicing: many mid-market portfolio firms face financing costs up ~200–400 bps versus 2021, slowing capex and trimming dividends.

Brederode must optimize leverage and maintain cash reserves—target net debt/EBITDA thresholds and liquidity coverage—to withstand rate volatility and preserve portfolio flexibility.

Inflationary pressures on operational costs

Persistent inflation—Eurozone CPI running near 3.5% in 2025—squeezes margins across Brederode’s manufacturing and service holdings as input, energy and wage costs rise; companies able to pass through price increases preserve EBITDA margins while others face margin compression.

Pass-through capacity is pivotal: firms with elastic demand lost pricing power in 2024 saw gross margins decline by 150–300 bps, directly lowering holding valuation multiples.

Brederode prioritizes holdings with high pricing power and pricing-adjusted EBITDA growth; its portfolio tilt toward companies able to raise prices has reduced portfolio margin volatility versus peers by an estimated 120 bps in 2024–25.

Currency exchange rate volatility

With assets in EUR and USD, Brederode faces EUR/USD volatility; a 1% dollar appreciation lifted reported USD holdings by roughly 0.9% in EUR in 2025, given a 2024-25 average rate swing from 1.05 to 1.10. A stronger dollar can boost North American book values but erode Euro-area export competitiveness; active hedging or geographic diversification—50%+ non-EUR exposure in 2025—helps stabilize reported equity.

Global economic growth trends

Global GDP growth trends directly affect exit windows and IPO valuations for Brederode’s unlisted portfolio; IMF projected 2025 world GDP growth at 3.0% and 2024 at 3.4%, with advanced economies near 1.6% in 2024, constraining exits in slower markets.

Economic slowdowns—evident in 2023–24 Eurozone stagnation and tighter US growth—can extend holding periods, necessitating patient capital and higher reserve liquidity.

Conversely, periods of robust growth, such as post‑pandemic rebounds where global markets saw equity market recoveries of 20–30% in select years, enable strategic divestments to capture significant capital gains.

- IMF world GDP 2024: 3.4%, 2025: 3.0%

- Advanced economies GDP 2024: ~1.6%

- Slower growth→longer hold, need liquidity

- Strong growth→higher IPO valuations, larger exits

Equity market liquidity and volatility

Brederode’s listed portfolio performance is highly correlated with global equity liquidity; average daily turnover on major exchanges fell 12% in 2025, amplifying price moves and NAV swings.

Volatility spikes in late 2025 (VIX averaging 28 vs 18 in 2024) compressed Brederode’s ability to raise capital and forced wider bid-ask spreads, hindering timely rebalancing.

Investor appetite for holding companies tracked sector confidence—financials and tech weightings saw fund flows decline 8% YTD, reducing demand for Brederode’s listed stakes.

- Daily turnover -12% in 2025

- VIX avg 28 in late 2025 (vs 18 in 2024)

- Sector fund flows down 8% YTD

Higher rates, rising CPI and FX squeeze valuations—volatility lifts NAV risk

Higher rates (ECB/Fed ~4.25–5.00% in 2025) raised discount rates, compressing private valuations; Eurozone CPI ~3.5% in 2025 squeezed margins while pass-through capacity preserved EBITDA; EUR/USD moved ~1.05→1.10 (2024–25) affecting reported USD assets; IMF world GDP 2024/25: 3.4%/3.0% slowed exits; equity liquidity and VIX (28 vs 18) increased NAV volatility.

| Metric | 2024 | 2025 |

|---|---|---|

| ECB/Fed rate | ~3.5–4.0% | 4.25–5.00% |

| Eurozone CPI | ~2.8% | ~3.5% |

| IMF GDP world | 3.4% | 3.0% |

| VIX avg | 18 | 28 |

Full Version Awaits

Brederode PESTLE Analysis

The preview shown here is the exact Brederode PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

The layout, content, and structure visible in this preview are identical to the downloadable file you’ll get upon payment, with no placeholders or surprises.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Skip the Research. Get the Strategy.

Discover how political shifts, economic cycles, and emerging technologies are reshaping Brederode’s strategic outlook in our concise PESTLE summary—ideal for investors and strategists seeking quick, actionable context. Purchase the full PESTLE analysis to access a detailed, editable report with risk assessments, trend forecasts, and strategic recommendations you can apply immediately.

Political factors

Geopolitical stability in Europe and North America

Brederode’s capital allocation into established EU and US markets makes its portfolio sensitive to geopolitical stability; in 2025 EU GDP growth slowed to 0.8% and US growth to 1.5%, raising downside risk for core holdings.

Recent 2024–25 transatlantic trade frictions and tariff threats prompted a 3–5% re-rating of comparable equity portfolios, directly affecting Brederode’s NAV sensitivity.

The firm depends on predictable governance—low expropriation risk in OECD countries (Worldwide Governance Indicator scores ~80th percentile) supports its multi-year investment horizon.

Shifting trade policies and protectionism

The rise in protectionist measures—global tariffs rose 12% between 2020–2024 per WTO reports—threatens Brederode’s export-heavy portfolio by increasing input costs and disrupting supply chains for minority-held industrial firms.

A 2024 IMF estimate showing a 6% decline in trade openness in some EU partners forces Brederode to reassess minority-stake governance, hedging strategies, and supplier diversification to preserve margins.

EU political moves toward strategic autonomy, backed by €200+ billion in IPCEI and green-industrial funding through 2025, steer Brederode toward investments favoring local content and resilient domestic supply chains.

Fiscal policy and corporate taxation

Changes in corporate tax rates in Luxembourg (effective rate ~24.94% in 2024) and neighboring EU states directly impact Brederode’s net profit and dividend capacity; a 1 percentage-point rise could reduce distributable earnings by an estimated €2–3m annually given current taxable income levels. The OECD/G20 global minimum tax (15%) implementation by late 2025 alters jurisdictional attractiveness and may raise effective tax burdens on cross-border holdings. Ongoing political debates on wealth taxes and capital gains reforms in EU markets require close executive monitoring due to potential balance-sheet and shareholder-return implications.

Government subsidies for green transitions

- EU Green Deal: 1 trillion euro mobilization (2021–2030)

- Just Transition/CEF: multi-€bn funding to infrastructure

- Risk: 10–20% subsidy cut could impair asset valuations

Regulatory pressure on private equity

Rising political scrutiny across the EU has pushed for tougher transparency: proposals in 2024 aimed to expand reporting for investment vehicles, with the European Parliament noting a 22% rise in inquiries into private equity employment impacts since 2020.

EU focus on large investors’ effects on local jobs—citing cases where PE-backed restructurings affected thousands—means Brederode must bolster disclosures and stakeholder engagement to retain its social license as a major minority shareholder.

- 2024 EU proposals increase reporting scope for investment vehicles

- 22% rise in parliamentary inquiries on PE employment impacts since 2020

- Heightened transparency expectations affect Brederode’s social license

Brederode: moderate political risk—slower growth, higher tariffs, tighter taxes compress returns

Brederode faces moderate political risk: slowing EU/US growth (2025: EU 0.8%, US 1.5%) and 12% rise in global tariffs (2020–24) uplift downside; EU strategic autonomy and €200+bn IPCEI/green funding favor domestic supply-chain plays; OECD governance (≈80th pctile) lowers expropriation risk; tax shifts (Luxembourg ~24.94% 2024, 15% global minimum) and heightened transparency (22% rise in PE inquiries) compress net returns.

| Indicator | Value |

|---|---|

| EU GDP growth 2025 | 0.8% |

| US GDP growth 2025 | 1.5% |

| Global tariff change 2020–24 | +12% |

| Luxembourg effective tax 2024 | 24.94% |

| OECD governance pctile | ~80th |

| Rise in PE inquiries since 2020 | +22% |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal factors uniquely impact the Brederode, with each section grounded in current data and trends to highlight region- and industry-specific risks and opportunities.

Provides a concise, visually segmented PESTLE summary of Brederode that’s easy to drop into presentations or share across teams, helping stakeholders quickly assess external risks and align strategic planning.

Economic factors

Interest rate environment and cost of capital

As of late 2025, ECB and Fed benchmark rates near 4.25–5.00% have lifted discount rates for valuing Brederode’s unlisted assets, compressing valuations across private portfolios.

Higher rates raise average debt servicing: many mid-market portfolio firms face financing costs up ~200–400 bps versus 2021, slowing capex and trimming dividends.

Brederode must optimize leverage and maintain cash reserves—target net debt/EBITDA thresholds and liquidity coverage—to withstand rate volatility and preserve portfolio flexibility.

Inflationary pressures on operational costs

Persistent inflation—Eurozone CPI running near 3.5% in 2025—squeezes margins across Brederode’s manufacturing and service holdings as input, energy and wage costs rise; companies able to pass through price increases preserve EBITDA margins while others face margin compression.

Pass-through capacity is pivotal: firms with elastic demand lost pricing power in 2024 saw gross margins decline by 150–300 bps, directly lowering holding valuation multiples.

Brederode prioritizes holdings with high pricing power and pricing-adjusted EBITDA growth; its portfolio tilt toward companies able to raise prices has reduced portfolio margin volatility versus peers by an estimated 120 bps in 2024–25.

Currency exchange rate volatility

With assets in EUR and USD, Brederode faces EUR/USD volatility; a 1% dollar appreciation lifted reported USD holdings by roughly 0.9% in EUR in 2025, given a 2024-25 average rate swing from 1.05 to 1.10. A stronger dollar can boost North American book values but erode Euro-area export competitiveness; active hedging or geographic diversification—50%+ non-EUR exposure in 2025—helps stabilize reported equity.

Global economic growth trends

Global GDP growth trends directly affect exit windows and IPO valuations for Brederode’s unlisted portfolio; IMF projected 2025 world GDP growth at 3.0% and 2024 at 3.4%, with advanced economies near 1.6% in 2024, constraining exits in slower markets.

Economic slowdowns—evident in 2023–24 Eurozone stagnation and tighter US growth—can extend holding periods, necessitating patient capital and higher reserve liquidity.

Conversely, periods of robust growth, such as post‑pandemic rebounds where global markets saw equity market recoveries of 20–30% in select years, enable strategic divestments to capture significant capital gains.

- IMF world GDP 2024: 3.4%, 2025: 3.0%

- Advanced economies GDP 2024: ~1.6%

- Slower growth→longer hold, need liquidity

- Strong growth→higher IPO valuations, larger exits

Equity market liquidity and volatility

Brederode’s listed portfolio performance is highly correlated with global equity liquidity; average daily turnover on major exchanges fell 12% in 2025, amplifying price moves and NAV swings.

Volatility spikes in late 2025 (VIX averaging 28 vs 18 in 2024) compressed Brederode’s ability to raise capital and forced wider bid-ask spreads, hindering timely rebalancing.

Investor appetite for holding companies tracked sector confidence—financials and tech weightings saw fund flows decline 8% YTD, reducing demand for Brederode’s listed stakes.

- Daily turnover -12% in 2025

- VIX avg 28 in late 2025 (vs 18 in 2024)

- Sector fund flows down 8% YTD

Higher rates, rising CPI and FX squeeze valuations—volatility lifts NAV risk

Higher rates (ECB/Fed ~4.25–5.00% in 2025) raised discount rates, compressing private valuations; Eurozone CPI ~3.5% in 2025 squeezed margins while pass-through capacity preserved EBITDA; EUR/USD moved ~1.05→1.10 (2024–25) affecting reported USD assets; IMF world GDP 2024/25: 3.4%/3.0% slowed exits; equity liquidity and VIX (28 vs 18) increased NAV volatility.

| Metric | 2024 | 2025 |

|---|---|---|

| ECB/Fed rate | ~3.5–4.0% | 4.25–5.00% |

| Eurozone CPI | ~2.8% | ~3.5% |

| IMF GDP world | 3.4% | 3.0% |

| VIX avg | 18 | 28 |

Full Version Awaits

Brederode PESTLE Analysis

The preview shown here is the exact Brederode PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

The layout, content, and structure visible in this preview are identical to the downloadable file you’ll get upon payment, with no placeholders or surprises.