Britvic Porter's Five Forces Analysis

From Overview to Strategy Blueprint

Britvic operates in a competitive, mature soft-drinks market where buyer price sensitivity, strong retail channels, and large rivals keep margins tight, while brand strength and distribution scale reduce entrant threats; supplier risk is moderate and substitutes (RTD coffees, water, private labels) remain a persistent pressure.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Britvic’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Raw Material Providers

The global supply of sugar, fruit concentrates and CO2 is concentrated among a few large suppliers, reducing Britvic’s bargaining power; in 2024 the top 5 sugar exporters supplied ~60% of global sugar, tightening market pricing.

Britvic uses multi-year contracts and hedging to limit volatility, but 2022–24 supply shocks (UK CO2 shortages in 2021–22) show disruptions can force short-term price jumps of 10–30%.

Reliance on premium fruit for Robinsons gives niche growers leverage: if key fruit inputs drop 5–10% in yield, sourcing costs rise materially and margin pressure follows.

Packaging Material Cost Fluctuations

Suppliers of aluminum and PET wield strong bargaining power: global commodity markets and tighter EU/UK recycling rules push premium on compliant inputs—aluminum LME rose 18% in 2024 and PCR (post-consumer recycled) PET premiums hit ~15% vs virgin in 2024.

Britvic’s target of 100% recycled PET raises reliance on a small pool of food-grade PCR suppliers, concentrating supplier leverage and limiting switching options.

Energy and polymer price swings feed through quickly; UK industrial gas rose ~22% in 2023–24 and manufacturers typically pass >80% of raw input cost changes into finished-goods pricing.

Strategic Partnership with PepsiCo

Britvic’s long-term bottling deal with PepsiCo makes suppliers’ power high: PepsiCo supplies concentrates for Pepsi and 7UP, accounting for roughly 40% of Britvic’s UK soft drinks volume in 2024, so Britvic is materially dependent on PepsiCo’s brand strength and secret formulas.

The contracts dictate pricing, marketing support, and product specs, giving PepsiCo leverage over Britvic’s margins and SKU mix; changes to terms could shift Britvic’s 2024 adjusted EBIT margin of ~9.5% by several hundred basis points.

Impact of Sustainability and Ethical Sourcing

Increasingly stringent ESG rules force Britvic to vet suppliers for labor and carbon metrics, shrinking eligible partners; in 2024 Britvic reported a 15% increase in supplier assessments after tightening its supplier code.

Suppliers meeting these standards can charge premiums—sustainable packaging suppliers saw price uplifts of 5–12% in 2023—helping Britvic hit net-zero and reporting targets.

This shifts procurement from cost to value-based sourcing, increasing supplier bargaining power as compliant vendors become scarce and strategically valuable.

- 2024: 15% more supplier assessments

- 2023: sustainable supplier price rise 5–12%

- Net-zero alignment raises supplier strategic value

Logistics and Energy Provider Influence

Britvic is highly exposed to logistics and fuel pricing: in 2024 UK diesel averaged about 1.63 GBP/litre, raising transport costs for its heavy liquid distribution and squeezing margins.

Shifts to electric or hydrogen heavy goods vehicles mean fleet upgrades and joint capex with carriers; UK HGV electrification pilots cost carriers ~£150k–£300k per vehicle, limiting rapid switch-over.

Fixed regional logistics networks give Britvic little bargaining room—switching providers risks route disruption and higher lead times, so supplier power remains high.

- 2024 UK diesel £1.63/litre

- HGV EV capex ~£150k–£300k/unit

- Regional routes hard to reassign

Supplier power squeezes margins: concentrated inputs, PCR limits, energy & logistics shocks

Suppliers exert high bargaining power: concentrated sugar/CO2/aluminum/PET markets, PepsiCo concentrate dependence (~40% UK volume in 2024), PCR supply constraints, and rising energy/logistics costs (UK diesel £1.63/l in 2024) press margins; hedges/contracts blunt but don’t remove 10–30% shock risk.

| Item | 2023–24 |

|---|---|

| PepsiCo share | ~40% |

| Diesel UK | £1.63/l |

| Aluminum LME | +18% (2024) |

| PCR premium | ~+15% |

What is included in the product

Tailored Porter's Five Forces analysis for Britvic, uncovering competitive intensity, buyer and supplier power, substitution threats, and entry barriers—highlighting strategic drivers that shape pricing, profitability, and growth prospects.

A concise Porter's Five Forces snapshot for Britvic that clarifies competitive pressures and helps prioritize strategic moves.

Customers Bargaining Power

Consolidation of Major Retailers

In the UK and Ireland a handful of retailers—Tesco, Sainsbury's, Asda and Morrisons—account for roughly 70% of grocery sales, giving them major leverage over suppliers like Britvic. These chains can demand lower wholesale prices, promotional funding, and prime shelf space because they move high volumes of Britvic brands such as Robinsons and J2O. A single delist by a major retailer can cut Britvic’s annual revenue by several percentage points; Britvic reported UK retail sales of £541m in 2024, so a 3–5% hit equals £16–27m.

Growth of Hard Discounters

The rise of Aldi and Lidl shifted UK grocery share toward value: discounters held about 14.2% of market share in 2024, pushing Britvic to accept tighter margins to stay listed on low-price shelves.

Discounters' narrow, high-turnover ranges favor own-labels, so Britvic competes for scarce SKU space versus rivals and private labels, reducing promotional leverage.

Customers now dictate lower price points aligned to the discounter model; in 2024 average soft-drink promotional depth grew ~3 percentage points, squeezing branded margins further.

Rise of Private Label Alternatives

Supermarkets like Tesco and Sainsbury’s have grown private-label soft drinks to 14–18% market share in UK grocery soft drinks by 2024, closely matching premium taste at 20–30% lower prices, which boosts retailer leverage to push Britvic on shelf space and margins.

That leverage lets retailers threaten greater private-label prominence, risking a 50–150bps hit to Britvic’s gross margin if listings shift; in 2024 Britvic reported a UK concentrate & soft drinks segment margin around mid-30s percent, so slippage matters.

Britvic must therefore invest in brand equity and product innovation—R&D and marketing spend focused on NPD (new product development) and premiumization—to defend a price premium and retailer support.

Fragmented Hospitality and Foodservice Channel

Fragmented pubs and independents give low individual bargaining power, but large buying groups and national chains like Whitbread (owner of Premier Inn and valued at £3.9bn market cap as of Dec 2025) and major fast-food groups have strong leverage over Britvic.

These customers push for exclusive pouring rights, forcing Britvic to match Coca-Cola Europacific Partners on price, promotion, and logistics; losing a national account can cut single-digit percentages of on-trade volume and dent brand visibility.

- Large chains drive terms, not independents

- Exclusive deals raise price/service pressure

- Competitor wins cost Britvic market share

Price Sensitivity of the End Consumer

End consumers have high bargaining power: switching costs between soft-drink brands are effectively zero, so in 2024 Britvic faced strong price sensitivity as UK food inflation hit 16% year-on-year at peak (ONS) and private-label share rose 2.1ppt across grocery channels (Kantar, 2024).

If Britvic passes on input-cost inflation, consumers can switch to cheaper brands or water, forcing a trade-off between price rises and marketing spend to protect market share; Britvic spent £66m on marketing in 2023.

- Zero switching costs raise consumer power

- UK food inflation ~16% peak (ONS, 2024)

- Private-label share +2.1ppt (Kantar, 2024)

- Marketing spend £66m (Britvic 2023)

Britvic squeezed by Big-4 retailers and discounters: 3–5% delist risk (£16–27m)

Retailers (Tesco, Sainsbury’s, Asda, Morrisons) control ~70% UK grocery sales, forcing Britvic to concede lower wholesale prices and promo funding; a 3–5% delist hit equals £16–27m of £541m UK retail sales (2024). Discounters held 14.2% share (2024), pushing tighter margins; private-label soft drinks 14–18% share (2024) and Britvic marketing was £66m (2023).

| Metric | Value |

|---|---|

| Top-4 retailer share | ~70% (2024) |

| Discounters | 14.2% (2024) |

| Private-label soft drinks | 14–18% (2024) |

| Britvic UK retail sales | £541m (2024) |

| Marketing spend | £66m (2023) |

Preview the Actual Deliverable

Britvic Porter's Five Forces Analysis

This preview shows the exact Britvic Porter's Five Forces analysis you'll receive after purchase—no placeholders, no mockups, fully formatted and ready for immediate download.

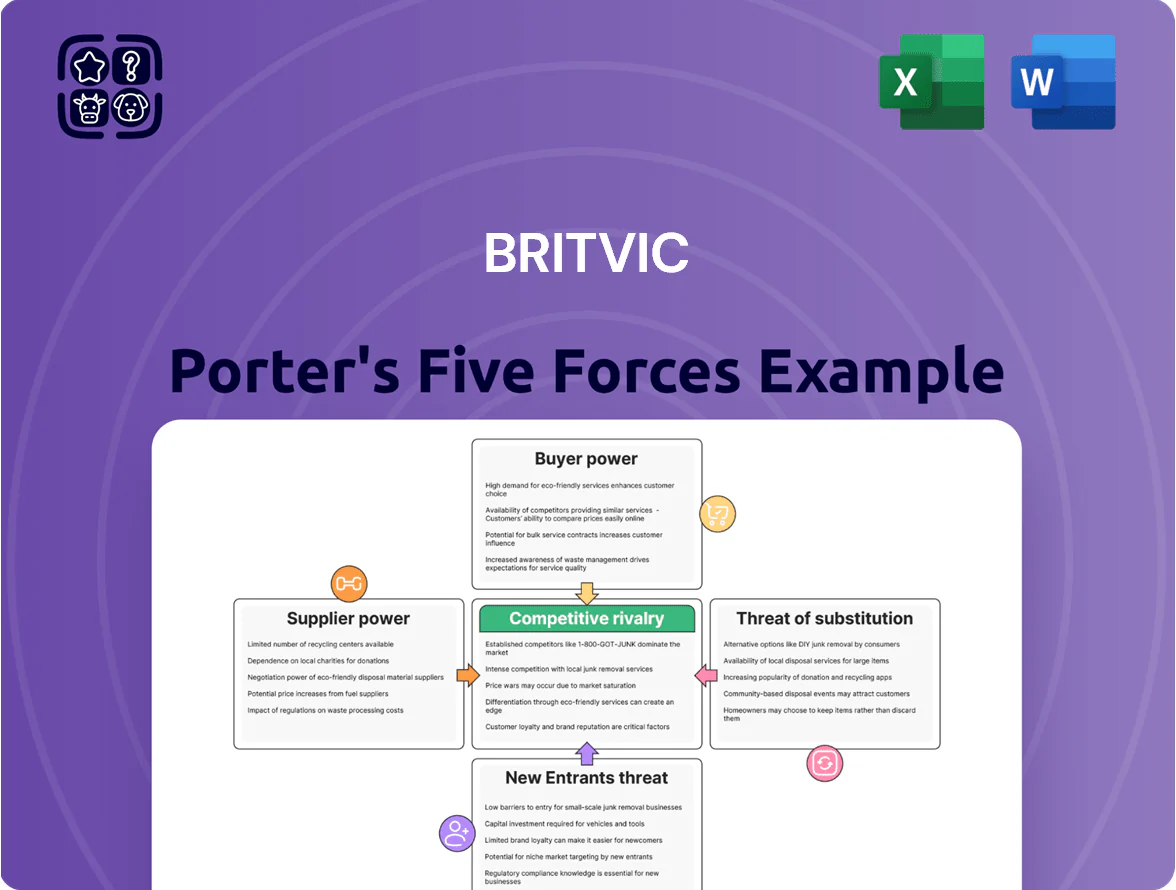

The document displayed is the complete, professionally written deliverable, containing supplier power, buyer power, competitive rivalry, threat of substitutes, and barriers to entry assessments tailored to Britvic.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

Britvic operates in a competitive, mature soft-drinks market where buyer price sensitivity, strong retail channels, and large rivals keep margins tight, while brand strength and distribution scale reduce entrant threats; supplier risk is moderate and substitutes (RTD coffees, water, private labels) remain a persistent pressure.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Britvic’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Raw Material Providers

The global supply of sugar, fruit concentrates and CO2 is concentrated among a few large suppliers, reducing Britvic’s bargaining power; in 2024 the top 5 sugar exporters supplied ~60% of global sugar, tightening market pricing.

Britvic uses multi-year contracts and hedging to limit volatility, but 2022–24 supply shocks (UK CO2 shortages in 2021–22) show disruptions can force short-term price jumps of 10–30%.

Reliance on premium fruit for Robinsons gives niche growers leverage: if key fruit inputs drop 5–10% in yield, sourcing costs rise materially and margin pressure follows.

Packaging Material Cost Fluctuations

Suppliers of aluminum and PET wield strong bargaining power: global commodity markets and tighter EU/UK recycling rules push premium on compliant inputs—aluminum LME rose 18% in 2024 and PCR (post-consumer recycled) PET premiums hit ~15% vs virgin in 2024.

Britvic’s target of 100% recycled PET raises reliance on a small pool of food-grade PCR suppliers, concentrating supplier leverage and limiting switching options.

Energy and polymer price swings feed through quickly; UK industrial gas rose ~22% in 2023–24 and manufacturers typically pass >80% of raw input cost changes into finished-goods pricing.

Strategic Partnership with PepsiCo

Britvic’s long-term bottling deal with PepsiCo makes suppliers’ power high: PepsiCo supplies concentrates for Pepsi and 7UP, accounting for roughly 40% of Britvic’s UK soft drinks volume in 2024, so Britvic is materially dependent on PepsiCo’s brand strength and secret formulas.

The contracts dictate pricing, marketing support, and product specs, giving PepsiCo leverage over Britvic’s margins and SKU mix; changes to terms could shift Britvic’s 2024 adjusted EBIT margin of ~9.5% by several hundred basis points.

Impact of Sustainability and Ethical Sourcing

Increasingly stringent ESG rules force Britvic to vet suppliers for labor and carbon metrics, shrinking eligible partners; in 2024 Britvic reported a 15% increase in supplier assessments after tightening its supplier code.

Suppliers meeting these standards can charge premiums—sustainable packaging suppliers saw price uplifts of 5–12% in 2023—helping Britvic hit net-zero and reporting targets.

This shifts procurement from cost to value-based sourcing, increasing supplier bargaining power as compliant vendors become scarce and strategically valuable.

- 2024: 15% more supplier assessments

- 2023: sustainable supplier price rise 5–12%

- Net-zero alignment raises supplier strategic value

Logistics and Energy Provider Influence

Britvic is highly exposed to logistics and fuel pricing: in 2024 UK diesel averaged about 1.63 GBP/litre, raising transport costs for its heavy liquid distribution and squeezing margins.

Shifts to electric or hydrogen heavy goods vehicles mean fleet upgrades and joint capex with carriers; UK HGV electrification pilots cost carriers ~£150k–£300k per vehicle, limiting rapid switch-over.

Fixed regional logistics networks give Britvic little bargaining room—switching providers risks route disruption and higher lead times, so supplier power remains high.

- 2024 UK diesel £1.63/litre

- HGV EV capex ~£150k–£300k/unit

- Regional routes hard to reassign

Supplier power squeezes margins: concentrated inputs, PCR limits, energy & logistics shocks

Suppliers exert high bargaining power: concentrated sugar/CO2/aluminum/PET markets, PepsiCo concentrate dependence (~40% UK volume in 2024), PCR supply constraints, and rising energy/logistics costs (UK diesel £1.63/l in 2024) press margins; hedges/contracts blunt but don’t remove 10–30% shock risk.

| Item | 2023–24 |

|---|---|

| PepsiCo share | ~40% |

| Diesel UK | £1.63/l |

| Aluminum LME | +18% (2024) |

| PCR premium | ~+15% |

What is included in the product

Tailored Porter's Five Forces analysis for Britvic, uncovering competitive intensity, buyer and supplier power, substitution threats, and entry barriers—highlighting strategic drivers that shape pricing, profitability, and growth prospects.

A concise Porter's Five Forces snapshot for Britvic that clarifies competitive pressures and helps prioritize strategic moves.

Customers Bargaining Power

Consolidation of Major Retailers

In the UK and Ireland a handful of retailers—Tesco, Sainsbury's, Asda and Morrisons—account for roughly 70% of grocery sales, giving them major leverage over suppliers like Britvic. These chains can demand lower wholesale prices, promotional funding, and prime shelf space because they move high volumes of Britvic brands such as Robinsons and J2O. A single delist by a major retailer can cut Britvic’s annual revenue by several percentage points; Britvic reported UK retail sales of £541m in 2024, so a 3–5% hit equals £16–27m.

Growth of Hard Discounters

The rise of Aldi and Lidl shifted UK grocery share toward value: discounters held about 14.2% of market share in 2024, pushing Britvic to accept tighter margins to stay listed on low-price shelves.

Discounters' narrow, high-turnover ranges favor own-labels, so Britvic competes for scarce SKU space versus rivals and private labels, reducing promotional leverage.

Customers now dictate lower price points aligned to the discounter model; in 2024 average soft-drink promotional depth grew ~3 percentage points, squeezing branded margins further.

Rise of Private Label Alternatives

Supermarkets like Tesco and Sainsbury’s have grown private-label soft drinks to 14–18% market share in UK grocery soft drinks by 2024, closely matching premium taste at 20–30% lower prices, which boosts retailer leverage to push Britvic on shelf space and margins.

That leverage lets retailers threaten greater private-label prominence, risking a 50–150bps hit to Britvic’s gross margin if listings shift; in 2024 Britvic reported a UK concentrate & soft drinks segment margin around mid-30s percent, so slippage matters.

Britvic must therefore invest in brand equity and product innovation—R&D and marketing spend focused on NPD (new product development) and premiumization—to defend a price premium and retailer support.

Fragmented Hospitality and Foodservice Channel

Fragmented pubs and independents give low individual bargaining power, but large buying groups and national chains like Whitbread (owner of Premier Inn and valued at £3.9bn market cap as of Dec 2025) and major fast-food groups have strong leverage over Britvic.

These customers push for exclusive pouring rights, forcing Britvic to match Coca-Cola Europacific Partners on price, promotion, and logistics; losing a national account can cut single-digit percentages of on-trade volume and dent brand visibility.

- Large chains drive terms, not independents

- Exclusive deals raise price/service pressure

- Competitor wins cost Britvic market share

Price Sensitivity of the End Consumer

End consumers have high bargaining power: switching costs between soft-drink brands are effectively zero, so in 2024 Britvic faced strong price sensitivity as UK food inflation hit 16% year-on-year at peak (ONS) and private-label share rose 2.1ppt across grocery channels (Kantar, 2024).

If Britvic passes on input-cost inflation, consumers can switch to cheaper brands or water, forcing a trade-off between price rises and marketing spend to protect market share; Britvic spent £66m on marketing in 2023.

- Zero switching costs raise consumer power

- UK food inflation ~16% peak (ONS, 2024)

- Private-label share +2.1ppt (Kantar, 2024)

- Marketing spend £66m (Britvic 2023)

Britvic squeezed by Big-4 retailers and discounters: 3–5% delist risk (£16–27m)

Retailers (Tesco, Sainsbury’s, Asda, Morrisons) control ~70% UK grocery sales, forcing Britvic to concede lower wholesale prices and promo funding; a 3–5% delist hit equals £16–27m of £541m UK retail sales (2024). Discounters held 14.2% share (2024), pushing tighter margins; private-label soft drinks 14–18% share (2024) and Britvic marketing was £66m (2023).

| Metric | Value |

|---|---|

| Top-4 retailer share | ~70% (2024) |

| Discounters | 14.2% (2024) |

| Private-label soft drinks | 14–18% (2024) |

| Britvic UK retail sales | £541m (2024) |

| Marketing spend | £66m (2023) |

Preview the Actual Deliverable

Britvic Porter's Five Forces Analysis

This preview shows the exact Britvic Porter's Five Forces analysis you'll receive after purchase—no placeholders, no mockups, fully formatted and ready for immediate download.

The document displayed is the complete, professionally written deliverable, containing supplier power, buyer power, competitive rivalry, threat of substitutes, and barriers to entry assessments tailored to Britvic.