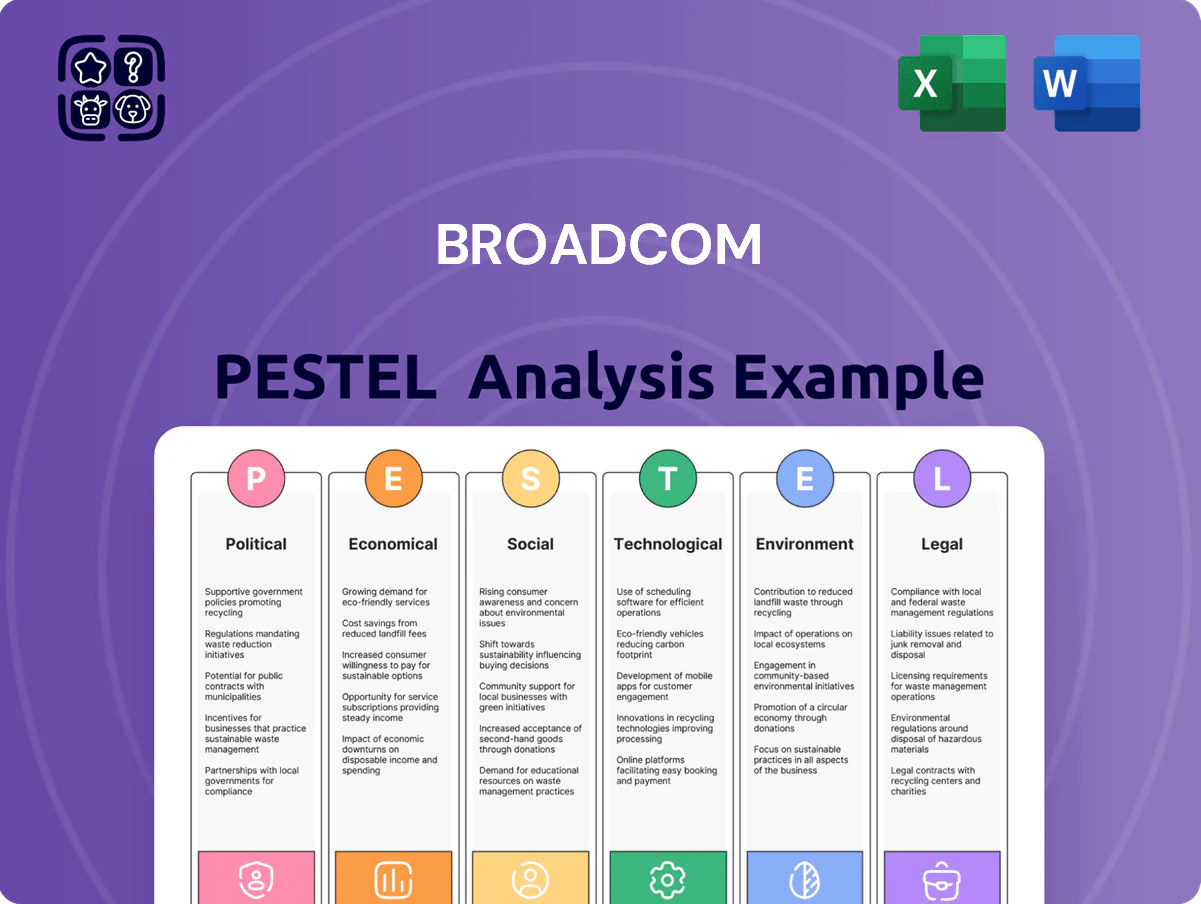

Broadcom PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Explore how political regulation, shifting global demand, rapid technological change, and sustainability pressures are shaping Broadcom’s strategic outlook in our concise PESTLE snapshot—perfect for investors and strategists who need fast, actionable context. Purchase the full PESTLE analysis to access detailed risk assessments, scenario impacts, and strategic recommendations you can apply immediately.

Political factors

US-China Trade Relations

The US-China tensions directly affect Broadcom, which generated about 18% of 2024 revenue from Greater China and sources ~30% of manufacturing capacity there; export controls on semiconductors and high-end networking gear force complex licensing and can restrict AI-chip shipments. Regulators expanded export curbs in 2023–25, and strategists must track changes through 2026 to avoid supply disruptions and potential revenue shortfalls.

CHIPS and Science Act Implementation

US CHIPS and Science Act directs over $39 billion for semiconductor incentives; Broadcom leverages these subsidies to align capex and R&D with US onshore production goals, enhancing fabs and design investment while tapping grant and tax-credit programs. The political backing reduces funding risk for multi-year projects, strengthens Broadcom’s strategic tie to national security supply-chain initiatives, and bolsters its competitive position in the domestic tech ecosystem.

Taiwanese Geopolitical Stability

As a fabless chipmaker, Broadcom relies on TSMC for >90% of its advanced logic wafers, so any Taiwan Strait escalation threatens delivery of high-performance networking and AI ASICs; 2024 revenues tied to chips manufactured in Taiwan represented an estimated majority of Broadcom’s $39.6B semiconductor-related sales, making regional instability a systemic supply-chain risk decision-makers must price into resilience planning.

Global Minimum Tax Standards

The OECD Pillar Two rollout, adopted by 140+ jurisdictions by 2024, raises effective minimum tax to 15%, complicating Broadcom's tax planning and potentially increasing cash taxes versus historical low-tax structures.

Higher statutory rates and curbs on incentives in key hubs could lower Broadcom's net income and free cash flow; a 1–2% ETR uplift on $14.7B FY2024 revenue implies impactful absolute tax cash changes.

Financial teams must reassess capital allocation and M&A models—higher post-tax returns thresholds and updated DCFs—while monitoring country-by-country implementation timing and carve-outs.

- 15% global minimum tax adopted by 140+ jurisdictions (2024)

- Broadcom FY2024 revenue $14.7B—1–2% ETR rise equals meaningful cash tax increase

- Revised DCF/M&A hurdles; monitor implementation timelines and exemptions

Infrastructure Software Regulation

- 2023 VMware acquisition value: $61 billion

- Global antitrust fines in 2024: $11.6 billion

- Regulatory reviews (EC/DOJ) drive remedies impacting transaction timelines and valuations

Broadcom faces China export, Taiwan Strait & tax headwinds despite $39B CHIPS boost

US-China export controls and Taiwan Strait risks threaten Broadcom supply and ~18% 2024 revenue from Greater China; US CHIPS provides $39B+ incentives boosting onshore capex; OECD Pillar Two (15% min tax, 140+ jurisdictions) likely raises ETR 1–2% on $14.7B FY2024 revenue; regulatory antitrust scrutiny (VMware $61B, global fines $11.6B in 2024) increases deal risk.

| Metric | Value |

|---|---|

| Greater China rev (2024) | ~18% |

| FY2024 revenue | $14.7B |

| CHIPS funding | $39B+ |

| Pillar Two adoption (2024) | 140+ jurisdictions |

| VMware deal | $61B |

| Global antitrust fines (2024) | $11.6B |

What is included in the product

Explores how macro-environmental forces uniquely affect Broadcom across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights to support executives, consultants, and investors in identifying strategic risks and opportunities.

A concise Broadcom PESTLE summary that’s visually segmented by category for quick interpretation, easily dropped into presentations or shared across teams to streamline risk discussions and strategic planning.

Economic factors

Interest Rate Environment

The rising interest rate environment raises Broadcom's weighted average cost of capital, increasing annual interest expense on its roughly $67 billion net debt (2025 year-end) and tightening free cash flow available for reinvestment.

Higher rates compress DCF valuations by increasing discount rates; a 100 bps rise can lower terminal value materially given Broadcom's long-duration cash flows from software acquisitions.

Investors should monitor Fed policy and global central bank moves through 2026, as shifts in the U.S. funds rate from 2024's ~5.25–5.50% range will directly affect borrowing costs and profitability.

AI Infrastructure Spending

The surge in AI infrastructure spending—hyperscaler capex rose to about $160B in 2024, driving strong demand for Broadcom’s custom ASICs and 400/800Gb switches, with Broadcom reporting 2024 semiconductor revenue up ~18% YoY tied to networking and ASICs.

Cyclical Semiconductor Demand

Broadcom faces the semiconductor cycle of boom and bust—2018–2021 saw strong demand then 2022–2023 inventory corrections; by FY2025 Broadcom reported a 6% YoY revenue decline in hardware segments amid softer enterprise spend. Its diversified portfolio cushions swings, but downturns hit broadband and wireless demand; monitoring IMF 2024–25 global GDP forecasts (≈3.0%–3.2%) and consumer electronics spending trends is critical for revenue forecasting.

Inflationary Pressure on Manufacturing

Persistent inflation in raw materials and specialized labor—DRAM, NAND and substrate prices rose ~8–12% in 2024—can compress Broadcom’s gross margins unless offset by pricing or efficiency.

Costs for advanced EUV lithography and heterogeneous packaging climbed ~10–15% as nodes approach physical limits, raising per-die manufacturing expense.

With ~70% of revenue tied to a concentrated set of hyperscaler and enterprise customers, strategists must assess Broadcom’s pricing power to pass through rising costs without eroding volume.

- Raw material/labor inflation: +8–12% (2024)

- Advanced lithography/packaging cost rise: +10–15%

- Revenue concentration: ~70% from large customers

Currency Exchange Volatility

As a global semiconductor leader with ~54% of revenue generated outside the US in FY2024, Broadcom is exposed to USD swings against EUR, CNY and TWD; a 10% USD appreciation versus major peers could erode reported non‑USD revenue by roughly that magnitude, pressuring competitive pricing in EMEA and APAC.

Broadcom employs hedging and natural offsets—FY2024 FX losses were limited to ~$120m—but persistent dollar strength still compresses consolidated revenue and margins over multi‑year trends.

- ~54% revenue ex‑US (FY2024)

- 10% USD rise ≈ 10% reported non‑USD revenue impact

- FY2024 FX losses ≈ $120m

Rising rates squeeze Broadcom DCF; AI capex lifts demand amid cost, FX pressures

Rising rates boost Broadcom’s WACC and interest on ~$67B net debt (2025), compressing DCF valuations; 100 bps hike materially lowers terminal value. AI capex (~$160B hyperscaler spend 2024) and 18% YoY semiconductor revenue growth (2024) support ASIC/switch demand, while raw material/litho cost inflation (+8–15% 2024) and ~54% revenue ex‑US expose results to FX (FY2024 FX losses ≈ $120m).

| Metric | Value |

|---|---|

| Net debt (2025) | $67B |

| Hyperscaler capex (2024) | $160B |

| Semiconductor rev growth (2024) | +18% YoY |

| Raw/litho cost rise (2024) | +8–15% |

| Rev ex‑US (FY2024) | ~54% |

| FY2024 FX losses | $120M |

Full Version Awaits

Broadcom PESTLE Analysis

The preview shown here is the exact Broadcom PESTLE document you’ll receive after purchase—fully formatted and ready to use. This is a real screenshot of the product you’re buying—delivered exactly as shown, no surprises. The content and structure visible in the preview are the same file you’ll download immediately after payment. No placeholders or teasers—this is the final, professionally structured document.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Plan Smarter. Present Sharper. Compete Stronger.

Explore how political regulation, shifting global demand, rapid technological change, and sustainability pressures are shaping Broadcom’s strategic outlook in our concise PESTLE snapshot—perfect for investors and strategists who need fast, actionable context. Purchase the full PESTLE analysis to access detailed risk assessments, scenario impacts, and strategic recommendations you can apply immediately.

Political factors

US-China Trade Relations

The US-China tensions directly affect Broadcom, which generated about 18% of 2024 revenue from Greater China and sources ~30% of manufacturing capacity there; export controls on semiconductors and high-end networking gear force complex licensing and can restrict AI-chip shipments. Regulators expanded export curbs in 2023–25, and strategists must track changes through 2026 to avoid supply disruptions and potential revenue shortfalls.

CHIPS and Science Act Implementation

US CHIPS and Science Act directs over $39 billion for semiconductor incentives; Broadcom leverages these subsidies to align capex and R&D with US onshore production goals, enhancing fabs and design investment while tapping grant and tax-credit programs. The political backing reduces funding risk for multi-year projects, strengthens Broadcom’s strategic tie to national security supply-chain initiatives, and bolsters its competitive position in the domestic tech ecosystem.

Taiwanese Geopolitical Stability

As a fabless chipmaker, Broadcom relies on TSMC for >90% of its advanced logic wafers, so any Taiwan Strait escalation threatens delivery of high-performance networking and AI ASICs; 2024 revenues tied to chips manufactured in Taiwan represented an estimated majority of Broadcom’s $39.6B semiconductor-related sales, making regional instability a systemic supply-chain risk decision-makers must price into resilience planning.

Global Minimum Tax Standards

The OECD Pillar Two rollout, adopted by 140+ jurisdictions by 2024, raises effective minimum tax to 15%, complicating Broadcom's tax planning and potentially increasing cash taxes versus historical low-tax structures.

Higher statutory rates and curbs on incentives in key hubs could lower Broadcom's net income and free cash flow; a 1–2% ETR uplift on $14.7B FY2024 revenue implies impactful absolute tax cash changes.

Financial teams must reassess capital allocation and M&A models—higher post-tax returns thresholds and updated DCFs—while monitoring country-by-country implementation timing and carve-outs.

- 15% global minimum tax adopted by 140+ jurisdictions (2024)

- Broadcom FY2024 revenue $14.7B—1–2% ETR rise equals meaningful cash tax increase

- Revised DCF/M&A hurdles; monitor implementation timelines and exemptions

Infrastructure Software Regulation

- 2023 VMware acquisition value: $61 billion

- Global antitrust fines in 2024: $11.6 billion

- Regulatory reviews (EC/DOJ) drive remedies impacting transaction timelines and valuations

Broadcom faces China export, Taiwan Strait & tax headwinds despite $39B CHIPS boost

US-China export controls and Taiwan Strait risks threaten Broadcom supply and ~18% 2024 revenue from Greater China; US CHIPS provides $39B+ incentives boosting onshore capex; OECD Pillar Two (15% min tax, 140+ jurisdictions) likely raises ETR 1–2% on $14.7B FY2024 revenue; regulatory antitrust scrutiny (VMware $61B, global fines $11.6B in 2024) increases deal risk.

| Metric | Value |

|---|---|

| Greater China rev (2024) | ~18% |

| FY2024 revenue | $14.7B |

| CHIPS funding | $39B+ |

| Pillar Two adoption (2024) | 140+ jurisdictions |

| VMware deal | $61B |

| Global antitrust fines (2024) | $11.6B |

What is included in the product

Explores how macro-environmental forces uniquely affect Broadcom across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights to support executives, consultants, and investors in identifying strategic risks and opportunities.

A concise Broadcom PESTLE summary that’s visually segmented by category for quick interpretation, easily dropped into presentations or shared across teams to streamline risk discussions and strategic planning.

Economic factors

Interest Rate Environment

The rising interest rate environment raises Broadcom's weighted average cost of capital, increasing annual interest expense on its roughly $67 billion net debt (2025 year-end) and tightening free cash flow available for reinvestment.

Higher rates compress DCF valuations by increasing discount rates; a 100 bps rise can lower terminal value materially given Broadcom's long-duration cash flows from software acquisitions.

Investors should monitor Fed policy and global central bank moves through 2026, as shifts in the U.S. funds rate from 2024's ~5.25–5.50% range will directly affect borrowing costs and profitability.

AI Infrastructure Spending

The surge in AI infrastructure spending—hyperscaler capex rose to about $160B in 2024, driving strong demand for Broadcom’s custom ASICs and 400/800Gb switches, with Broadcom reporting 2024 semiconductor revenue up ~18% YoY tied to networking and ASICs.

Cyclical Semiconductor Demand

Broadcom faces the semiconductor cycle of boom and bust—2018–2021 saw strong demand then 2022–2023 inventory corrections; by FY2025 Broadcom reported a 6% YoY revenue decline in hardware segments amid softer enterprise spend. Its diversified portfolio cushions swings, but downturns hit broadband and wireless demand; monitoring IMF 2024–25 global GDP forecasts (≈3.0%–3.2%) and consumer electronics spending trends is critical for revenue forecasting.

Inflationary Pressure on Manufacturing

Persistent inflation in raw materials and specialized labor—DRAM, NAND and substrate prices rose ~8–12% in 2024—can compress Broadcom’s gross margins unless offset by pricing or efficiency.

Costs for advanced EUV lithography and heterogeneous packaging climbed ~10–15% as nodes approach physical limits, raising per-die manufacturing expense.

With ~70% of revenue tied to a concentrated set of hyperscaler and enterprise customers, strategists must assess Broadcom’s pricing power to pass through rising costs without eroding volume.

- Raw material/labor inflation: +8–12% (2024)

- Advanced lithography/packaging cost rise: +10–15%

- Revenue concentration: ~70% from large customers

Currency Exchange Volatility

As a global semiconductor leader with ~54% of revenue generated outside the US in FY2024, Broadcom is exposed to USD swings against EUR, CNY and TWD; a 10% USD appreciation versus major peers could erode reported non‑USD revenue by roughly that magnitude, pressuring competitive pricing in EMEA and APAC.

Broadcom employs hedging and natural offsets—FY2024 FX losses were limited to ~$120m—but persistent dollar strength still compresses consolidated revenue and margins over multi‑year trends.

- ~54% revenue ex‑US (FY2024)

- 10% USD rise ≈ 10% reported non‑USD revenue impact

- FY2024 FX losses ≈ $120m

Rising rates squeeze Broadcom DCF; AI capex lifts demand amid cost, FX pressures

Rising rates boost Broadcom’s WACC and interest on ~$67B net debt (2025), compressing DCF valuations; 100 bps hike materially lowers terminal value. AI capex (~$160B hyperscaler spend 2024) and 18% YoY semiconductor revenue growth (2024) support ASIC/switch demand, while raw material/litho cost inflation (+8–15% 2024) and ~54% revenue ex‑US expose results to FX (FY2024 FX losses ≈ $120m).

| Metric | Value |

|---|---|

| Net debt (2025) | $67B |

| Hyperscaler capex (2024) | $160B |

| Semiconductor rev growth (2024) | +18% YoY |

| Raw/litho cost rise (2024) | +8–15% |

| Rev ex‑US (FY2024) | ~54% |

| FY2024 FX losses | $120M |

Full Version Awaits

Broadcom PESTLE Analysis

The preview shown here is the exact Broadcom PESTLE document you’ll receive after purchase—fully formatted and ready to use. This is a real screenshot of the product you’re buying—delivered exactly as shown, no surprises. The content and structure visible in the preview are the same file you’ll download immediately after payment. No placeholders or teasers—this is the final, professionally structured document.