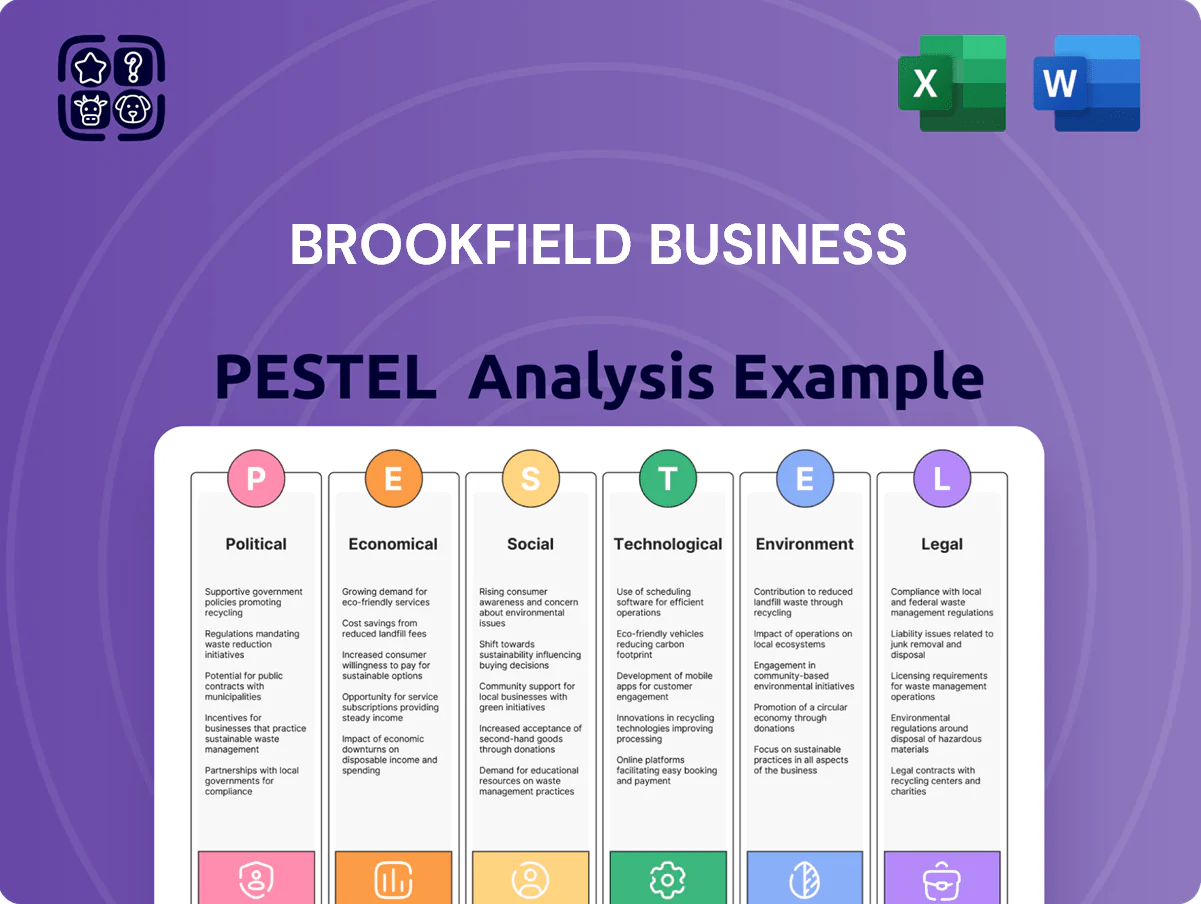

Brookfield Business PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Unlock strategic foresight with our targeted PESTLE Analysis for Brookfield Business—spot regulatory pressures, economic headwinds, and tech shifts that could reshape value drivers. This concise brief pinpoints actionable risks and opportunities to strengthen investment theses or corporate plans. Purchase the full report for the complete, editable analysis and immediate strategic advantage.

Political factors

Geopolitical instability and trade protectionism

As a global operator, Brookfield Business Partners faces supply-chain risks from rising trade protectionism and geopolitical tensions that disrupted 14% of global container flows in 2024, forcing operational pauses in some industrial units.

Government infrastructure spending and subsidies

Brookfield benefits from national infrastructure initiatives—US Bipartisan Infrastructure Law and EU recovery funds—supporting its $800bn AUM platform as projects pivot to grids, transport and renewables, boosting construction and services revenue streams.

Government grants and PPPs expand deal flow: Brookfield reported $20bn of infrastructure investments in 2024, driven by subsidy-backed projects and contracted revenues for its service units.

Monitoring fiscal policy is critical: an estimated 35% of certain portfolio revenues in 2024 derived from state-funded contracts or industrial incentives, exposing cash flows to budgetary shifts.

Regulatory shifts in energy and carbon policy

Political mandates for carbon neutrality (over 130 countries pledging net-zero by mid-century) steer Brookfield’s energy holdings toward renewables, influencing capex allocations—Brookfield Renewable’s $20bn+ asset base must align with decarbonization timelines. New laws curbing fossil fuels or mandating grid integration raise compliance costs and shift returns, while government backing for nuclear or clean fuels (tax credits, $369bn US IRA clean energy provisions to 2031) alters valuations of industrial assets.

Foreign investment screening and national security laws

Foreign investment screening, led by agencies like CFIUS in the U.S. and equivalent EU mechanisms, has increased scrutiny of Brookfield’s cross-border deals, with CFIUS notices rising over 25% from 2020–2024 and blocking or conditioning several high-profile transactions.

Stricter national security reviews particularly target high-tech and critical infrastructure assets, risking delays or outright rejections that can derail Brookfield’s acquisition timelines and valuations.

Brookfield must build longer approval buffers into deal timetables, budget for remediation costs, and prepare for potential divestment or mitigation remedies in sensitive sectors.

- CFIUS notices +25% (2020–2024); blocking/conditioning of major deals increased, raising compliance costs and timeline risk.

Taxation policy and international reform

Changes in corporate tax rates and the OECD/G20 Pillar Two global minimum tax (15%) implemented from 2023 can compress Brookfield’s after-tax returns across its $800+ billion AUM, affecting net income for multi-jurisdictional holdings and lowering distributable cash.

Brookfield must navigate varied local tax regimes to optimize capital recycling and dividends, using tax-efficient holding structures and timing to preserve IRR targets (typically mid-to-high teens) on disposals.

Rising capital gains taxes in Canada, Australia, and parts of Europe through 2024–25 can shift asset-exit timing, potentially delaying sales to protect realized returns and tax-advantaged carry structures.

- Global minimum tax: 15% (Pillar Two) adopted 2023

- Brookfield AUM: >$800 billion (2025)

- Target IRRs: mid-to-high teens

- Capital gains law shifts in Canada, Australia, Europe (2024–25)

Brookfield braces for political risk: higher CFIUS, taxes, $20B infra, longer approvals

Political risks shape Brookfield’s deal flow, with 25% rise in CFIUS notices (2020–24), $20bn infra investments (2024), >$800bn AUM (2025), Pillar Two 15% tax from 2023, and 35% of some revenues state-dependent in 2024—requiring longer approvals, compliance buffers, and tax-efficient structures.

| Metric | Value |

|---|---|

| CFIUS notices (2020–24) | +25% |

| Infrastructure spend (2024) | $20bn |

| AUM (2025) | >$800bn |

| Pillar Two rate | 15% |

| State-dependent revenue (2024) | 35% |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely affect Brookfield across its asset classes and regions, with each section grounded in current data and trend analysis to reveal strategic risks and opportunities.

A concise, visually segmented Brookfield Business PESTLE summary that’s easily dropped into presentations or shared across teams to quickly align on external risks, market positioning, and strategic implications.

Economic factors

Interest rate environment and cost of capital

As a highly leveraged acquirer, Brookfield’s borrowing costs move with central bank rates; the US Fed funds rate peaking at 5.25–5.50% in 2023–24 raised average borrowing spreads and pushed blended cost of debt for asset managers toward 4–5% in 2024.

By end‑2025, market forecasts from Bloomberg and the Fed futures implied a 50–100bps easing vs peak, which would lower new deal financing costs and improve interest coverage on portfolio debt by several percentage points.

Brookfield’s active use of hedging—swaps, caps, fixed‑rate issuance—remains central to stabilizing cash flows and protecting returns against rate volatility across its real assets and private equity platforms.

Global inflationary pressures and input costs

Persistent inflation in labor and raw materials—global CPI still elevated at ~3.5% in 2025 vs pre‑pandemic 1.8%—squeezes margins across Brookfield’s industrial and services arms, with input cost rises of 6–8% in key segments reported in 2024.

Brookfield targets assets with strong pricing power—utility and regulated infrastructure where average tariff adjustments outpaced inflation by ~1.5ppt in 2023–24—allowing cost pass‑through to customers.

Cooling economies in parts of Europe and China, where construction activity fell 4–7% YoY in 2024, could reduce demand for Brookfield’s construction and infrastructure services, forcing tighter operational efficiency and slower capital deployment.

Currency exchange rate volatility

Brookfield operates across 30+ countries, exposing consolidated statements to FX risk; a 10% USD appreciation vs EUR, BRL or GBP reduced reported EBITDA by about 4–6% in prior cycles. USD swings alter translated international cash flows—2024 saw USD strength trim Brookfield tilting results in Q3 2024. The company uses layered hedges (forwards, options, cross-currency swaps) covering a significant portion of foreign cash flows to stabilize reported earnings.

Capital market liquidity and exit environments

Capital market liquidity and exit environments critically affect Brookfield’s ability to monetize assets: global equity market cap fell ~8% in 2024 while high-yield spreads averaged ~420bps, narrowing IPO and trade-sale windows.

Favorable 2024–25 conditions enabled selective capital recycling, supporting reinvestment into infrastructure and real assets with realized gains; Brookfield EMV depends on market timing.

Tightening liquidity—seen in Q4 2024 credit tightening—increases hold periods and can reduce IRRs if assets are retained beyond planned exit horizons.

- Global equity cap down ~8% in 2024; HY spreads ~420bps

- Capital recycling linked to market windows for IPOs/trade sales

- Liquidity tightening forces longer holds, pressuring IRRs

Global supply chain resilience and logistics

Global shifts—container rates up ~35% from 2020 peaks and shipping volumes recovering to 2019 levels—raise logistics costs, pressuring Brookfield industrials' margins and throughput efficiency.

Brookfield allocates capital to supply-chain upgrades, noting portfolio investments in logistics automation and warehousing expansions worth over $3.2bn in 2024 to bolster resilience against macro shocks.

Near-shoring trends, with manufacturing moving closer to end markets, reshape demand for regional logistics hubs, strengthening Brookfield Business Services' strategic positioning in North America and Europe.

- Logistics costs volatility: +35% peak container rates vs 2020

- 2024 logistics investments: $3.2bn in automation/warehousing

- Regionalization boosts demand for North American/European hubs

Higher rates, inflation and FX squeeze Brookfield: margins pressured, refinancing easing ahead

Higher rates raised Brookfield’s blended cost of debt to ~4–5% in 2024; Fed futures signaled 50–100bps easing by end‑2025, easing refinancing costs. Inflation ~3.5% in 2025 pushed input costs +6–8% in 2024; pricing power in regulated assets allowed ~1.5ppt pass‑through. FX moves (10% USD up) cut reported EBITDA ~4–6%; 2024 HY spreads ~420bps and global equity cap −8% tightened exit windows.

| Metric | Value |

|---|---|

| Blended debt cost (2024) | 4–5% |

| Inflation (2025) | ~3.5% |

| Input cost rise (2024) | 6–8% |

| FX impact (10% USD↑) | −4–6% EBITDA |

| HY spreads (2024) | ~420bps |

| Global equity cap (2024) | −8% |

Preview Before You Purchase

Brookfield Business PESTLE Analysis

The preview shown here is the exact Brookfield Business PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use.

The layout, content, and structure visible here are exactly what you’ll be able to download immediately after buying, with no placeholders or teasers.

No surprises: this is the real, final file—professionally structured and ready for analysis or presentation.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Unlock strategic foresight with our targeted PESTLE Analysis for Brookfield Business—spot regulatory pressures, economic headwinds, and tech shifts that could reshape value drivers. This concise brief pinpoints actionable risks and opportunities to strengthen investment theses or corporate plans. Purchase the full report for the complete, editable analysis and immediate strategic advantage.

Political factors

Geopolitical instability and trade protectionism

As a global operator, Brookfield Business Partners faces supply-chain risks from rising trade protectionism and geopolitical tensions that disrupted 14% of global container flows in 2024, forcing operational pauses in some industrial units.

Government infrastructure spending and subsidies

Brookfield benefits from national infrastructure initiatives—US Bipartisan Infrastructure Law and EU recovery funds—supporting its $800bn AUM platform as projects pivot to grids, transport and renewables, boosting construction and services revenue streams.

Government grants and PPPs expand deal flow: Brookfield reported $20bn of infrastructure investments in 2024, driven by subsidy-backed projects and contracted revenues for its service units.

Monitoring fiscal policy is critical: an estimated 35% of certain portfolio revenues in 2024 derived from state-funded contracts or industrial incentives, exposing cash flows to budgetary shifts.

Regulatory shifts in energy and carbon policy

Political mandates for carbon neutrality (over 130 countries pledging net-zero by mid-century) steer Brookfield’s energy holdings toward renewables, influencing capex allocations—Brookfield Renewable’s $20bn+ asset base must align with decarbonization timelines. New laws curbing fossil fuels or mandating grid integration raise compliance costs and shift returns, while government backing for nuclear or clean fuels (tax credits, $369bn US IRA clean energy provisions to 2031) alters valuations of industrial assets.

Foreign investment screening and national security laws

Foreign investment screening, led by agencies like CFIUS in the U.S. and equivalent EU mechanisms, has increased scrutiny of Brookfield’s cross-border deals, with CFIUS notices rising over 25% from 2020–2024 and blocking or conditioning several high-profile transactions.

Stricter national security reviews particularly target high-tech and critical infrastructure assets, risking delays or outright rejections that can derail Brookfield’s acquisition timelines and valuations.

Brookfield must build longer approval buffers into deal timetables, budget for remediation costs, and prepare for potential divestment or mitigation remedies in sensitive sectors.

- CFIUS notices +25% (2020–2024); blocking/conditioning of major deals increased, raising compliance costs and timeline risk.

Taxation policy and international reform

Changes in corporate tax rates and the OECD/G20 Pillar Two global minimum tax (15%) implemented from 2023 can compress Brookfield’s after-tax returns across its $800+ billion AUM, affecting net income for multi-jurisdictional holdings and lowering distributable cash.

Brookfield must navigate varied local tax regimes to optimize capital recycling and dividends, using tax-efficient holding structures and timing to preserve IRR targets (typically mid-to-high teens) on disposals.

Rising capital gains taxes in Canada, Australia, and parts of Europe through 2024–25 can shift asset-exit timing, potentially delaying sales to protect realized returns and tax-advantaged carry structures.

- Global minimum tax: 15% (Pillar Two) adopted 2023

- Brookfield AUM: >$800 billion (2025)

- Target IRRs: mid-to-high teens

- Capital gains law shifts in Canada, Australia, Europe (2024–25)

Brookfield braces for political risk: higher CFIUS, taxes, $20B infra, longer approvals

Political risks shape Brookfield’s deal flow, with 25% rise in CFIUS notices (2020–24), $20bn infra investments (2024), >$800bn AUM (2025), Pillar Two 15% tax from 2023, and 35% of some revenues state-dependent in 2024—requiring longer approvals, compliance buffers, and tax-efficient structures.

| Metric | Value |

|---|---|

| CFIUS notices (2020–24) | +25% |

| Infrastructure spend (2024) | $20bn |

| AUM (2025) | >$800bn |

| Pillar Two rate | 15% |

| State-dependent revenue (2024) | 35% |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely affect Brookfield across its asset classes and regions, with each section grounded in current data and trend analysis to reveal strategic risks and opportunities.

A concise, visually segmented Brookfield Business PESTLE summary that’s easily dropped into presentations or shared across teams to quickly align on external risks, market positioning, and strategic implications.

Economic factors

Interest rate environment and cost of capital

As a highly leveraged acquirer, Brookfield’s borrowing costs move with central bank rates; the US Fed funds rate peaking at 5.25–5.50% in 2023–24 raised average borrowing spreads and pushed blended cost of debt for asset managers toward 4–5% in 2024.

By end‑2025, market forecasts from Bloomberg and the Fed futures implied a 50–100bps easing vs peak, which would lower new deal financing costs and improve interest coverage on portfolio debt by several percentage points.

Brookfield’s active use of hedging—swaps, caps, fixed‑rate issuance—remains central to stabilizing cash flows and protecting returns against rate volatility across its real assets and private equity platforms.

Global inflationary pressures and input costs

Persistent inflation in labor and raw materials—global CPI still elevated at ~3.5% in 2025 vs pre‑pandemic 1.8%—squeezes margins across Brookfield’s industrial and services arms, with input cost rises of 6–8% in key segments reported in 2024.

Brookfield targets assets with strong pricing power—utility and regulated infrastructure where average tariff adjustments outpaced inflation by ~1.5ppt in 2023–24—allowing cost pass‑through to customers.

Cooling economies in parts of Europe and China, where construction activity fell 4–7% YoY in 2024, could reduce demand for Brookfield’s construction and infrastructure services, forcing tighter operational efficiency and slower capital deployment.

Currency exchange rate volatility

Brookfield operates across 30+ countries, exposing consolidated statements to FX risk; a 10% USD appreciation vs EUR, BRL or GBP reduced reported EBITDA by about 4–6% in prior cycles. USD swings alter translated international cash flows—2024 saw USD strength trim Brookfield tilting results in Q3 2024. The company uses layered hedges (forwards, options, cross-currency swaps) covering a significant portion of foreign cash flows to stabilize reported earnings.

Capital market liquidity and exit environments

Capital market liquidity and exit environments critically affect Brookfield’s ability to monetize assets: global equity market cap fell ~8% in 2024 while high-yield spreads averaged ~420bps, narrowing IPO and trade-sale windows.

Favorable 2024–25 conditions enabled selective capital recycling, supporting reinvestment into infrastructure and real assets with realized gains; Brookfield EMV depends on market timing.

Tightening liquidity—seen in Q4 2024 credit tightening—increases hold periods and can reduce IRRs if assets are retained beyond planned exit horizons.

- Global equity cap down ~8% in 2024; HY spreads ~420bps

- Capital recycling linked to market windows for IPOs/trade sales

- Liquidity tightening forces longer holds, pressuring IRRs

Global supply chain resilience and logistics

Global shifts—container rates up ~35% from 2020 peaks and shipping volumes recovering to 2019 levels—raise logistics costs, pressuring Brookfield industrials' margins and throughput efficiency.

Brookfield allocates capital to supply-chain upgrades, noting portfolio investments in logistics automation and warehousing expansions worth over $3.2bn in 2024 to bolster resilience against macro shocks.

Near-shoring trends, with manufacturing moving closer to end markets, reshape demand for regional logistics hubs, strengthening Brookfield Business Services' strategic positioning in North America and Europe.

- Logistics costs volatility: +35% peak container rates vs 2020

- 2024 logistics investments: $3.2bn in automation/warehousing

- Regionalization boosts demand for North American/European hubs

Higher rates, inflation and FX squeeze Brookfield: margins pressured, refinancing easing ahead

Higher rates raised Brookfield’s blended cost of debt to ~4–5% in 2024; Fed futures signaled 50–100bps easing by end‑2025, easing refinancing costs. Inflation ~3.5% in 2025 pushed input costs +6–8% in 2024; pricing power in regulated assets allowed ~1.5ppt pass‑through. FX moves (10% USD up) cut reported EBITDA ~4–6%; 2024 HY spreads ~420bps and global equity cap −8% tightened exit windows.

| Metric | Value |

|---|---|

| Blended debt cost (2024) | 4–5% |

| Inflation (2025) | ~3.5% |

| Input cost rise (2024) | 6–8% |

| FX impact (10% USD↑) | −4–6% EBITDA |

| HY spreads (2024) | ~420bps |

| Global equity cap (2024) | −8% |

Preview Before You Purchase

Brookfield Business PESTLE Analysis

The preview shown here is the exact Brookfield Business PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use.

The layout, content, and structure visible here are exactly what you’ll be able to download immediately after buying, with no placeholders or teasers.

No surprises: this is the real, final file—professionally structured and ready for analysis or presentation.