Brookshire Grocery Porter's Five Forces Analysis

Don't Miss the Bigger Picture

Brookshire Grocery faces intense regional competition, shifting buyer expectations, and margin pressure from suppliers and private-label rivals—all of which shape its strategic choices and growth prospects.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Brookshire Grocery’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Dominance of Global CPG Brands

Growth of Private Label Alternatives

Brookshire Grocery expanded private-label lines across banners, lifting private-label sales to about 18% of store revenue in 2024, which trims reliance on national suppliers and offers lower-cost alternatives to customers. By sourcing and branding in-house, Brookshire captures higher gross margins—private label margins are typically 4–8 percentage points above national brands—boosting bargaining leverage. This control lets Brookshire pressure national vendors on price, promo support, and slotting fees, improving procurement terms and protecting margins.

Supply Chain and Logistics Volatility

Regional suppliers of fresh produce and meat exert moderate bargaining power over Brookshire Grocery because the chain depends on them to sustain its fresh-perishable reputation; in 2025 regional freight rates rose ~12% YoY and USDA reported a 7–9% drop in certain regional meat supplies after climate events.

Consolidation of Wholesale Distributors

The consolidation of wholesale food distributors has cut regional partners by about 30% since 2015, narrowing Brookshire Grocery's supplier options and raising switching costs.

Fewer providers grant larger distributors stronger negotiation power, pushing up contract prices—industry data show larger distributors command 5–8% higher margins on regional contracts in 2024.

Brookshire must deepen long-term partnerships and logistics commitments to lock stable pricing and delivery; expect higher working-capital needs and multi-year contracts.

- ~30% fewer regional distributors since 2015

- 5–8% higher margins from large distributors (2024)

- More multi-year contracts and higher working-capital

Impact of Input Cost Inflation

- Raw material CPI +14% (2024)

- Energy costs up ~8% YoY (2024)

- Trade spend reduced, fewer supplier discounts

- Focus: contracts, private-label, SKU cuts

Suppliers Gain Leverage: CPG Dominance, Rising Costs, and Brookshire’s Private-Label Hedge

| Metric | Value |

|---|---|

| CPG shelf share | 60–70% |

| Slotting fee (avg) | $0.10–$0.50/unit |

| CPG price hikes (2024) | 5–8% |

| Private-label revenue (2024) | 18% |

| Raw material CPI (2024) | +14% |

| Regional distributors since 2015 | −30% |

What is included in the product

Tailored exclusively for Brookshire Grocery, this Porter's Five Forces analysis uncovers competitive drivers, supplier and buyer influence on pricing, entry barriers and substitutes, and highlights disruptive threats to its regional market position.

Concise Porter's Five Forces snapshot for Brookshire Grocery—clearly highlights competitive pressures and supplier/customer dynamics to speed strategic decisions.

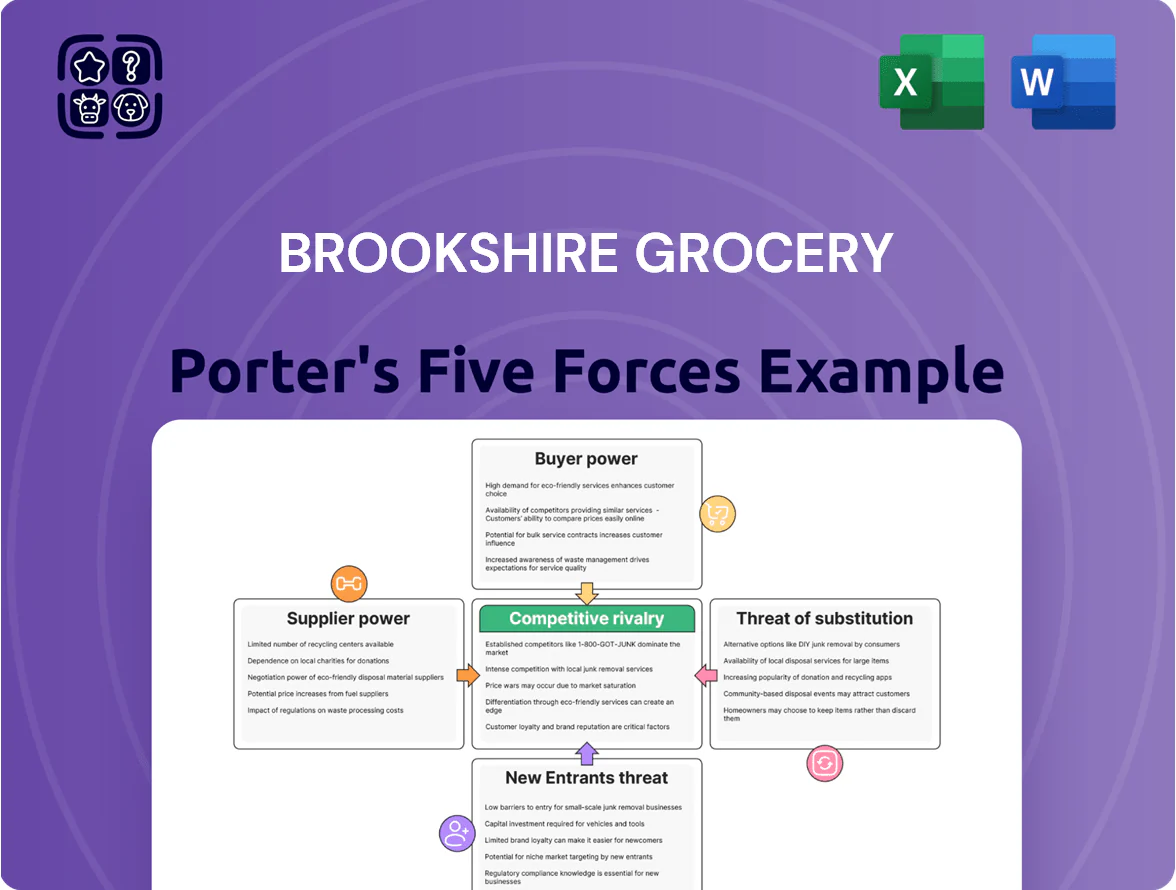

Customers Bargaining Power

Low Switching Costs for Shoppers

Switching costs are minimal in grocery retail, so Texas and Louisiana shoppers freely shift between Brookshire Grocery Company and rivals like H-E-B and Walmart based on price and convenience; NielsenIQ found 72% of US grocery shoppers visited multiple stores weekly in 2024. This mobility cut Brookshire’s implied customer stickiness, pressuring same-store sales—Brookshire’s regional comps rose just 1.8% in 2024 vs national 3.6%. The result: Brookshire must invest in service, store upkeep, and weekly promotions to retain share.

Heightened Price Sensitivity

In 2025, 68% of US grocery shoppers say price drives store choice and 54% use price-comparison apps weekly, raising buyer power for Brookshire Grocery; real-time cross-banner comparisons push margins down. Brookshire must match aggressive promotional pricing and loyalty discounts—Super 1 Foods’ 2024 promo lift showed a 4.2% same-store-sales gain—so targeted price cuts and digital coupons are essential to retain share.

Influence of Loyalty Programs

Brookshire Grocery uses advanced loyalty programs that collected over 120 million customer transactions in 2024, enabling personalized incentives like fuel rewards and targeted coupons that lower churn and discourage switching. These programs create perceived value—fuel savings up to $0.10/gal and coupon redemptions boosting basket spend by ~8%—reducing individual shoppers’ bargaining power. Data-driven forecasts let Brookshire predict buying patterns and tailor offers to keep customers within its ecosystem.

Demand for Omnichannel Convenience

Modern customers expect seamless omnichannel options—online ordering, curbside pickup, and delivery—giving buyers power to switch retailers over digital UX and fulfillment speed.

Brookshire Grocery has invested roughly $120–150 million since 2020 in digital and supply-chain upgrades to support same-day/curbside services and protect share from tech-forward rivals like Instacart and Walmart Grocery.

- Customers choose by app speed and delivery time

- Omnichannel drives retention and market share

- Brookshire capex ~120–150M (2020–2025)

Preference for Fresh and Local Products

Growing demand for fresh, local, and organic foods—US organic food sales rose ~8% to $63.4B in 2024—lets customers shift spend to retailers that verify origin, increasing their bargaining power over Brookshire Grocery.

Brookshire counters by prioritizing fresh departments and local supplier partnerships, driving traffic to FRESH by Brookshire’s stores and aligning inventory with traceability expectations.

- Organic sales $63.4B (2024)

- Local sourcing boosts basket size ~5–10%

- FRESH banner focuses on produce, deli, meat traceability

Price-savvy customers squeeze Brookshire margins despite loyalty data and capex

Customers have high bargaining power: low switching costs, price-driven choice (68% in 2025), and app-based comparison (54% weekly) compress margins; Brookshire’s 1.8% comp growth (2024) lags the US 3.6% mark. Loyalty data (120M transactions, 2024) and $120–150M capex (2020–2025) mitigate churn; organic demand ($63.4B, 2024) shifts spend to traceable fresh offerings.

| Metric | Value |

|---|---|

| 2024 comp growth | 1.8% |

| US grocery comp (2024) | 3.6% |

| Price-driven shoppers (2025) | 68% |

| Use price apps weekly (2025) | 54% |

| Loyalty transactions (2024) | 120M |

| Capex (2020–2025) | $120–150M |

| US organic sales (2024) | $63.4B |

Preview the Actual Deliverable

Brookshire Grocery Porter's Five Forces Analysis

This preview shows the exact Brookshire Grocery Porter’s Five Forces analysis you'll receive immediately after purchase—fully formatted, professionally written, and ready for use.

No samples or placeholders: the document displayed here is the complete deliverable, available for instant download once your purchase is confirmed.

You're viewing the final file; post-purchase you'll have access to this identical analysis with no further setup or customization required.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

Brookshire Grocery faces intense regional competition, shifting buyer expectations, and margin pressure from suppliers and private-label rivals—all of which shape its strategic choices and growth prospects.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Brookshire Grocery’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Dominance of Global CPG Brands

Growth of Private Label Alternatives

Brookshire Grocery expanded private-label lines across banners, lifting private-label sales to about 18% of store revenue in 2024, which trims reliance on national suppliers and offers lower-cost alternatives to customers. By sourcing and branding in-house, Brookshire captures higher gross margins—private label margins are typically 4–8 percentage points above national brands—boosting bargaining leverage. This control lets Brookshire pressure national vendors on price, promo support, and slotting fees, improving procurement terms and protecting margins.

Supply Chain and Logistics Volatility

Regional suppliers of fresh produce and meat exert moderate bargaining power over Brookshire Grocery because the chain depends on them to sustain its fresh-perishable reputation; in 2025 regional freight rates rose ~12% YoY and USDA reported a 7–9% drop in certain regional meat supplies after climate events.

Consolidation of Wholesale Distributors

The consolidation of wholesale food distributors has cut regional partners by about 30% since 2015, narrowing Brookshire Grocery's supplier options and raising switching costs.

Fewer providers grant larger distributors stronger negotiation power, pushing up contract prices—industry data show larger distributors command 5–8% higher margins on regional contracts in 2024.

Brookshire must deepen long-term partnerships and logistics commitments to lock stable pricing and delivery; expect higher working-capital needs and multi-year contracts.

- ~30% fewer regional distributors since 2015

- 5–8% higher margins from large distributors (2024)

- More multi-year contracts and higher working-capital

Impact of Input Cost Inflation

- Raw material CPI +14% (2024)

- Energy costs up ~8% YoY (2024)

- Trade spend reduced, fewer supplier discounts

- Focus: contracts, private-label, SKU cuts

Suppliers Gain Leverage: CPG Dominance, Rising Costs, and Brookshire’s Private-Label Hedge

| Metric | Value |

|---|---|

| CPG shelf share | 60–70% |

| Slotting fee (avg) | $0.10–$0.50/unit |

| CPG price hikes (2024) | 5–8% |

| Private-label revenue (2024) | 18% |

| Raw material CPI (2024) | +14% |

| Regional distributors since 2015 | −30% |

What is included in the product

Tailored exclusively for Brookshire Grocery, this Porter's Five Forces analysis uncovers competitive drivers, supplier and buyer influence on pricing, entry barriers and substitutes, and highlights disruptive threats to its regional market position.

Concise Porter's Five Forces snapshot for Brookshire Grocery—clearly highlights competitive pressures and supplier/customer dynamics to speed strategic decisions.

Customers Bargaining Power

Low Switching Costs for Shoppers

Switching costs are minimal in grocery retail, so Texas and Louisiana shoppers freely shift between Brookshire Grocery Company and rivals like H-E-B and Walmart based on price and convenience; NielsenIQ found 72% of US grocery shoppers visited multiple stores weekly in 2024. This mobility cut Brookshire’s implied customer stickiness, pressuring same-store sales—Brookshire’s regional comps rose just 1.8% in 2024 vs national 3.6%. The result: Brookshire must invest in service, store upkeep, and weekly promotions to retain share.

Heightened Price Sensitivity

In 2025, 68% of US grocery shoppers say price drives store choice and 54% use price-comparison apps weekly, raising buyer power for Brookshire Grocery; real-time cross-banner comparisons push margins down. Brookshire must match aggressive promotional pricing and loyalty discounts—Super 1 Foods’ 2024 promo lift showed a 4.2% same-store-sales gain—so targeted price cuts and digital coupons are essential to retain share.

Influence of Loyalty Programs

Brookshire Grocery uses advanced loyalty programs that collected over 120 million customer transactions in 2024, enabling personalized incentives like fuel rewards and targeted coupons that lower churn and discourage switching. These programs create perceived value—fuel savings up to $0.10/gal and coupon redemptions boosting basket spend by ~8%—reducing individual shoppers’ bargaining power. Data-driven forecasts let Brookshire predict buying patterns and tailor offers to keep customers within its ecosystem.

Demand for Omnichannel Convenience

Modern customers expect seamless omnichannel options—online ordering, curbside pickup, and delivery—giving buyers power to switch retailers over digital UX and fulfillment speed.

Brookshire Grocery has invested roughly $120–150 million since 2020 in digital and supply-chain upgrades to support same-day/curbside services and protect share from tech-forward rivals like Instacart and Walmart Grocery.

- Customers choose by app speed and delivery time

- Omnichannel drives retention and market share

- Brookshire capex ~120–150M (2020–2025)

Preference for Fresh and Local Products

Growing demand for fresh, local, and organic foods—US organic food sales rose ~8% to $63.4B in 2024—lets customers shift spend to retailers that verify origin, increasing their bargaining power over Brookshire Grocery.

Brookshire counters by prioritizing fresh departments and local supplier partnerships, driving traffic to FRESH by Brookshire’s stores and aligning inventory with traceability expectations.

- Organic sales $63.4B (2024)

- Local sourcing boosts basket size ~5–10%

- FRESH banner focuses on produce, deli, meat traceability

Price-savvy customers squeeze Brookshire margins despite loyalty data and capex

Customers have high bargaining power: low switching costs, price-driven choice (68% in 2025), and app-based comparison (54% weekly) compress margins; Brookshire’s 1.8% comp growth (2024) lags the US 3.6% mark. Loyalty data (120M transactions, 2024) and $120–150M capex (2020–2025) mitigate churn; organic demand ($63.4B, 2024) shifts spend to traceable fresh offerings.

| Metric | Value |

|---|---|

| 2024 comp growth | 1.8% |

| US grocery comp (2024) | 3.6% |

| Price-driven shoppers (2025) | 68% |

| Use price apps weekly (2025) | 54% |

| Loyalty transactions (2024) | 120M |

| Capex (2020–2025) | $120–150M |

| US organic sales (2024) | $63.4B |

Preview the Actual Deliverable

Brookshire Grocery Porter's Five Forces Analysis

This preview shows the exact Brookshire Grocery Porter’s Five Forces analysis you'll receive immediately after purchase—fully formatted, professionally written, and ready for use.

No samples or placeholders: the document displayed here is the complete deliverable, available for instant download once your purchase is confirmed.

You're viewing the final file; post-purchase you'll have access to this identical analysis with no further setup or customization required.