Brunel International PESTLE Analysis

Skip the Research. Get the Strategy.

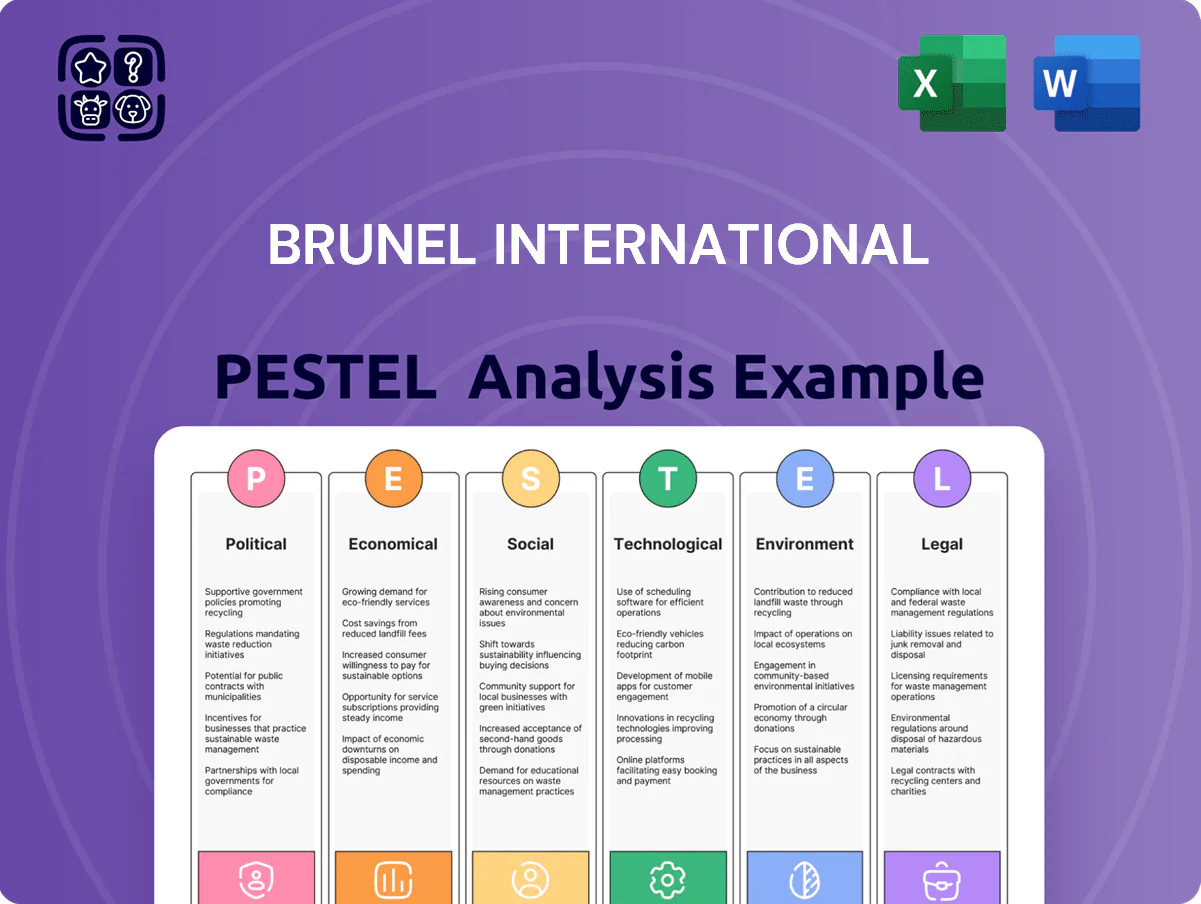

Gain a strategic edge with our PESTLE Analysis tailored for Brunel International—unpack the political, economic, social, technological, legal, and environmental forces shaping its prospects and spot actionable risks and opportunities fast; purchase the full report for the complete, editable breakdown and make decisions with confidence.

Political factors

Geopolitical Instability in Key Regions

Global tensions and conflicts in 2025 increased market volatility and caused project delays for Brunel clients, with industry reports showing a 15–20% contraction in project pipelines as firms postponed infrastructure spending.

Governmental Energy Transition Policies

Immigration and Labor Mobility Regulations

Strict visa rules in the UK and EU have reduced intra‑EU and UK‑to‑EU mobility; UK Skilled Worker visas fell 12% in issuances 2024 vs 2023, tightening supply of engineers and IT specialists Brunel relies on.

Brunel must adapt to shifting legal-political frameworks to staff specialized engineering and IT roles across markets while maintaining compliance and client delivery timelines.

Work permit changes raised average recruitment lead times by ~20% in 2024, increasing placement costs and affecting secondment margins.

Public Infrastructure and Defense Spending

In the DACH region, a 2025 increase in government defense and infrastructure budgets—Germany raised defense spending to 2.5% of GDP and Austria/Switzerland boosted infrastructure outlays by ~4% YoY—has strengthened demand for Brunel’s engineering services, offsetting weakness in automotive and industrial manufacturing.

The political focus on energy independence kept public-sector energy projects resilient in 2025, enabling Brunel to expand into defense and government contracts and diversify revenue toward less cyclical streams.

- Germany defense spend ~2.5% of GDP (2025)

- Regional public infrastructure +4% YoY (2025)

- Defense/energy projects showed resilience vs. private-sector softness

- Opportunity to shift revenue mix away from cyclical automotive

Trade Agreements and Tariff Volatility

- 12% average tariff rise on select auto parts (2024)

- 15% decline in regional specialist demand post-tariff alerts

- Focus on EU, US, China, ASEAN policy monitoring

Brunel pivots: +28% renewables, $1.2bn clean contracts as visas, tariffs reshape workforce

Political shifts—net‑zero mandates, defense spend rise, stricter visas and trade tariffs—reshaped Brunel’s 2024–25 pipeline: renewables demand +28% YoY, $1.2bn contracted clean-energy work, 22% headcount reallocated, UK Skilled Worker visas −12%, recruitment lead times +20%, Germany defense ≈2.5% GDP, auto-part tariffs +12% causing a 15% drop in regional specialist demand.

| Metric | Value |

|---|---|

| Renewables demand | +28% YoY |

| Clean-energy contracts | $1.2bn |

| Headcount reallocated | 22% |

| UK Skilled Worker visas | −12% |

| Recruitment lead time | +20% |

| Germany defense spend | ≈2.5% GDP |

| Auto-part tariffs | +12% |

| Specialist demand drop | −15% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Brunel International across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify threats and opportunities for executives, consultants, and entrepreneurs.

A concise, PESTLE-segmented summary of Brunel International that’s easy to drop into presentations or share across teams, helping stakeholders quickly assess external risks and market positioning and add customised notes for their region or business line.

Economic factors

Global Economic Slowdown and Recession Risks

Persistent economic uncertainty through 2025 drove a 10% y/y revenue decline for Brunel as clients deferred permanent hires and large-scale projects, aligning with OECD forecasts of 0.8% global GDP growth in 2025 versus 3.4% in 2021. Elevated interest rates—US fed funds at ~5.25% and ECB ~4.5% in mid-2025—increased capital costs for clients in oil, gas and construction, tightening project pipelines. Brunel implemented targeted cost-reduction programs, preserving underlying EBIT margin near 6% despite softer demand and liquidity pressures.

Fluctuations in Energy and Commodity Prices

Brunel’s revenue and margins remain highly correlated with global oil and gas cycles; oil prices fell from an average Brent of $96/bbl in 2022 to $84/bbl in 2024, and with 2024 estimates showing ~55–65% of gross profit still from traditional energy, client capex shifts directly alter demand for Brunel’s exploration and production staffing. Commodity price volatility—yearly Brent swings of 20–30% since 2022—creates rapid changes in demand for specialized project management and technical contractors, impacting utilization and billing rates.

Currency Exchange Rate Volatility

Reporting in euros, Brunel faced a notable headwind as the US dollar weakened about 8% versus the euro in H2 2025, cutting reported Americas revenue and compressing group EBIT margin by an estimated 60–120 basis points; Asia exposures also saw translation losses given regional invoicing in dollars and local currencies. Brunel uses forward contracts and options to hedge up to 70% of forecasted FX exposure and closely monitors organic growth in USD-denominated markets to offset translation volatility. Management noted FX sensitivity of roughly €1.5m EBITDA per 1% USD/EUR move in the 2025 annual report, guiding continued selective hedging and pricing adjustments into 2026.

Shift from Permanent to Flexible Staffing

The 2025 economic downturn drove permanent recruitment revenue down nearly 40% for many staffing firms as companies shifted to flexible deployment to cut payroll costs and boost operational agility; Brunel saw revenue mix tilt toward secondments and project-based staffing, aligning with its core model.

While total recruitment fees contracted (industrywide fee pressure ~15% in 2025), Brunel benefited from higher-margin flexible engagements and increased utilization of contractors across energy and engineering sectors.

- Permanent recruitment revenue fell ~40% in 2025

- Industry recruitment fees down ~15% in 2025

- Higher demand for secondments/project staffing boosts Brunel’s model

- Contractor utilization rose, supporting margins despite fee pressure

Labor Cost Inflation and Wage Standards

Rising minimum wages and labor cost inflation across Europe and the Americas have pushed Brunel’s operating costs higher; Euro area wages rose ~5.8% y/y in 2024 and US average hourly earnings grew ~4.1% in 2024, tightening margins.

To protect gross margin Brunel must pass costs to clients via higher day rates; success depends on contract renegotiation and client acceptance amid competitive pressure.

Brunel’s pricing power hinges on scarcity of high-end technical talent—specialist contractor rates rose ~6–8% in 2024, aiding negotiation leverage.

- Europe wages +5.8% y/y (2024)

- US avg hourly earnings +4.1% (2024)

- Specialist contractor rates +6–8% (2024)

- Margin survival tied to client pass-through and talent scarcity

Brunel weathers weak 2025 revenue (-10%) as contractor mix preserves ~6% underlying EBIT

Economic weakness through 2025 cut Brunel revenue ~10% y/y; oil volatility (Brent $84 in 2024) and higher rates (US ~5.25%, ECB ~4.5% mid-2025) raised capex costs and pushed clients to flexible staffing, improving contractor utilization and preserving ~6% underlying EBIT.

| Metric | 2024/2025 |

|---|---|

| Revenue change | -10% y/y (2025) |

| Brent avg | $84/bbl (2024) |

| Fed/ECB | ~5.25% / ~4.5% (mid-2025) |

| Underlying EBIT | ~6% |

Preview the Actual Deliverable

Brunel International PESTLE Analysis

The preview shown here is the exact Brunel International PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic or investment decisions.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Skip the Research. Get the Strategy.

Gain a strategic edge with our PESTLE Analysis tailored for Brunel International—unpack the political, economic, social, technological, legal, and environmental forces shaping its prospects and spot actionable risks and opportunities fast; purchase the full report for the complete, editable breakdown and make decisions with confidence.

Political factors

Geopolitical Instability in Key Regions

Global tensions and conflicts in 2025 increased market volatility and caused project delays for Brunel clients, with industry reports showing a 15–20% contraction in project pipelines as firms postponed infrastructure spending.

Governmental Energy Transition Policies

Immigration and Labor Mobility Regulations

Strict visa rules in the UK and EU have reduced intra‑EU and UK‑to‑EU mobility; UK Skilled Worker visas fell 12% in issuances 2024 vs 2023, tightening supply of engineers and IT specialists Brunel relies on.

Brunel must adapt to shifting legal-political frameworks to staff specialized engineering and IT roles across markets while maintaining compliance and client delivery timelines.

Work permit changes raised average recruitment lead times by ~20% in 2024, increasing placement costs and affecting secondment margins.

Public Infrastructure and Defense Spending

In the DACH region, a 2025 increase in government defense and infrastructure budgets—Germany raised defense spending to 2.5% of GDP and Austria/Switzerland boosted infrastructure outlays by ~4% YoY—has strengthened demand for Brunel’s engineering services, offsetting weakness in automotive and industrial manufacturing.

The political focus on energy independence kept public-sector energy projects resilient in 2025, enabling Brunel to expand into defense and government contracts and diversify revenue toward less cyclical streams.

- Germany defense spend ~2.5% of GDP (2025)

- Regional public infrastructure +4% YoY (2025)

- Defense/energy projects showed resilience vs. private-sector softness

- Opportunity to shift revenue mix away from cyclical automotive

Trade Agreements and Tariff Volatility

- 12% average tariff rise on select auto parts (2024)

- 15% decline in regional specialist demand post-tariff alerts

- Focus on EU, US, China, ASEAN policy monitoring

Brunel pivots: +28% renewables, $1.2bn clean contracts as visas, tariffs reshape workforce

Political shifts—net‑zero mandates, defense spend rise, stricter visas and trade tariffs—reshaped Brunel’s 2024–25 pipeline: renewables demand +28% YoY, $1.2bn contracted clean-energy work, 22% headcount reallocated, UK Skilled Worker visas −12%, recruitment lead times +20%, Germany defense ≈2.5% GDP, auto-part tariffs +12% causing a 15% drop in regional specialist demand.

| Metric | Value |

|---|---|

| Renewables demand | +28% YoY |

| Clean-energy contracts | $1.2bn |

| Headcount reallocated | 22% |

| UK Skilled Worker visas | −12% |

| Recruitment lead time | +20% |

| Germany defense spend | ≈2.5% GDP |

| Auto-part tariffs | +12% |

| Specialist demand drop | −15% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Brunel International across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify threats and opportunities for executives, consultants, and entrepreneurs.

A concise, PESTLE-segmented summary of Brunel International that’s easy to drop into presentations or share across teams, helping stakeholders quickly assess external risks and market positioning and add customised notes for their region or business line.

Economic factors

Global Economic Slowdown and Recession Risks

Persistent economic uncertainty through 2025 drove a 10% y/y revenue decline for Brunel as clients deferred permanent hires and large-scale projects, aligning with OECD forecasts of 0.8% global GDP growth in 2025 versus 3.4% in 2021. Elevated interest rates—US fed funds at ~5.25% and ECB ~4.5% in mid-2025—increased capital costs for clients in oil, gas and construction, tightening project pipelines. Brunel implemented targeted cost-reduction programs, preserving underlying EBIT margin near 6% despite softer demand and liquidity pressures.

Fluctuations in Energy and Commodity Prices

Brunel’s revenue and margins remain highly correlated with global oil and gas cycles; oil prices fell from an average Brent of $96/bbl in 2022 to $84/bbl in 2024, and with 2024 estimates showing ~55–65% of gross profit still from traditional energy, client capex shifts directly alter demand for Brunel’s exploration and production staffing. Commodity price volatility—yearly Brent swings of 20–30% since 2022—creates rapid changes in demand for specialized project management and technical contractors, impacting utilization and billing rates.

Currency Exchange Rate Volatility

Reporting in euros, Brunel faced a notable headwind as the US dollar weakened about 8% versus the euro in H2 2025, cutting reported Americas revenue and compressing group EBIT margin by an estimated 60–120 basis points; Asia exposures also saw translation losses given regional invoicing in dollars and local currencies. Brunel uses forward contracts and options to hedge up to 70% of forecasted FX exposure and closely monitors organic growth in USD-denominated markets to offset translation volatility. Management noted FX sensitivity of roughly €1.5m EBITDA per 1% USD/EUR move in the 2025 annual report, guiding continued selective hedging and pricing adjustments into 2026.

Shift from Permanent to Flexible Staffing

The 2025 economic downturn drove permanent recruitment revenue down nearly 40% for many staffing firms as companies shifted to flexible deployment to cut payroll costs and boost operational agility; Brunel saw revenue mix tilt toward secondments and project-based staffing, aligning with its core model.

While total recruitment fees contracted (industrywide fee pressure ~15% in 2025), Brunel benefited from higher-margin flexible engagements and increased utilization of contractors across energy and engineering sectors.

- Permanent recruitment revenue fell ~40% in 2025

- Industry recruitment fees down ~15% in 2025

- Higher demand for secondments/project staffing boosts Brunel’s model

- Contractor utilization rose, supporting margins despite fee pressure

Labor Cost Inflation and Wage Standards

Rising minimum wages and labor cost inflation across Europe and the Americas have pushed Brunel’s operating costs higher; Euro area wages rose ~5.8% y/y in 2024 and US average hourly earnings grew ~4.1% in 2024, tightening margins.

To protect gross margin Brunel must pass costs to clients via higher day rates; success depends on contract renegotiation and client acceptance amid competitive pressure.

Brunel’s pricing power hinges on scarcity of high-end technical talent—specialist contractor rates rose ~6–8% in 2024, aiding negotiation leverage.

- Europe wages +5.8% y/y (2024)

- US avg hourly earnings +4.1% (2024)

- Specialist contractor rates +6–8% (2024)

- Margin survival tied to client pass-through and talent scarcity

Brunel weathers weak 2025 revenue (-10%) as contractor mix preserves ~6% underlying EBIT

Economic weakness through 2025 cut Brunel revenue ~10% y/y; oil volatility (Brent $84 in 2024) and higher rates (US ~5.25%, ECB ~4.5% mid-2025) raised capex costs and pushed clients to flexible staffing, improving contractor utilization and preserving ~6% underlying EBIT.

| Metric | 2024/2025 |

|---|---|

| Revenue change | -10% y/y (2025) |

| Brent avg | $84/bbl (2024) |

| Fed/ECB | ~5.25% / ~4.5% (mid-2025) |

| Underlying EBIT | ~6% |

Preview the Actual Deliverable

Brunel International PESTLE Analysis

The preview shown here is the exact Brunel International PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic or investment decisions.