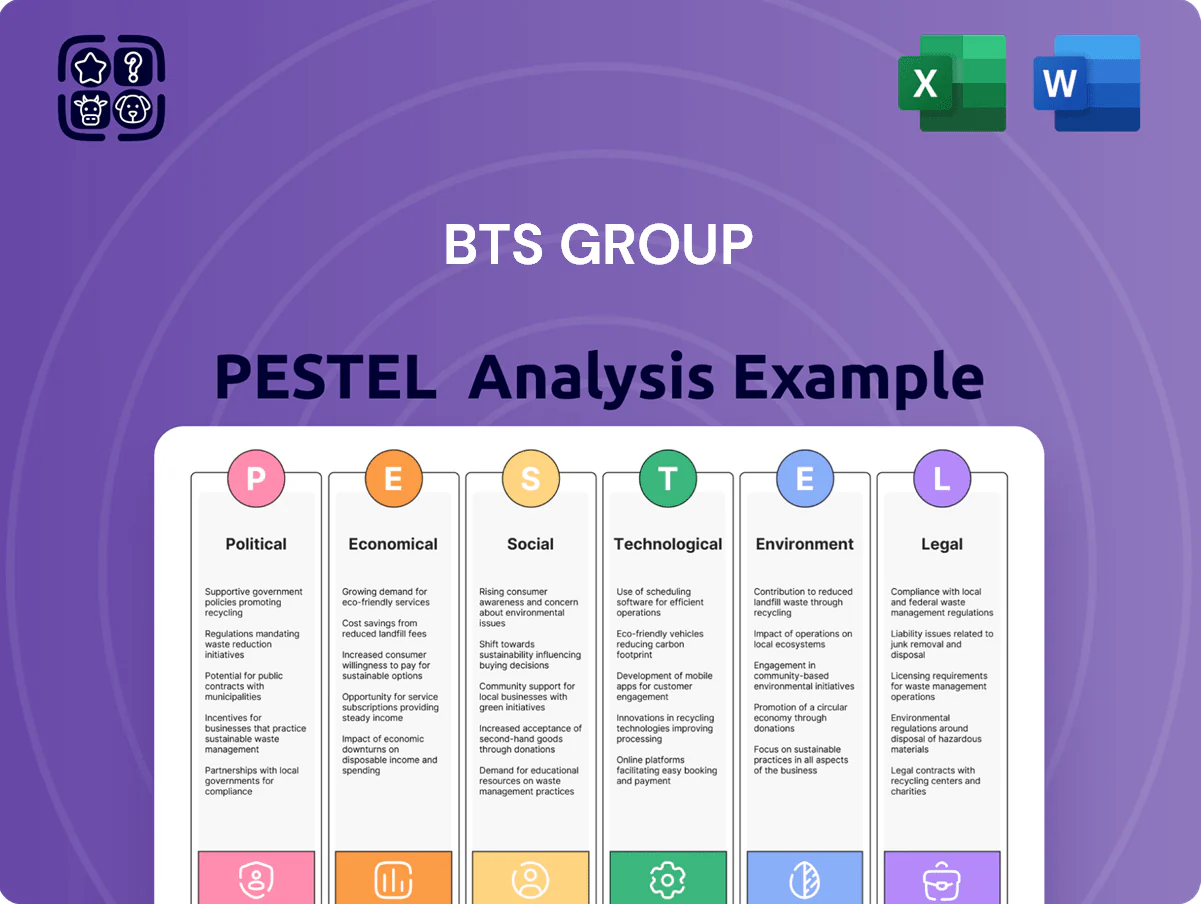

BTS Group PESTLE Analysis

Your Competitive Advantage Starts with This Report

Discover how political shifts, economic cycles, social trends, and technological advances are shaping BTS Group’s strategic outlook—our concise PESTLE snapshot highlights key external forces and their implications for growth and risk management; purchase the full analysis to access the complete, actionable report and ready-to-use slides for strategic planning.

Political factors

Geopolitical fragmentation and global operations

As of late 2025, BTS Group faces geopolitical fragmentation requiring localized strategy execution; 62% of its revenue in FY2024 came from outside Scandinavia, intensifying exposure to divergent US, EU and China trade policies that affect client deployment of training and leadership programs.

Rising tariffs and data localization laws have increased compliance costs by an estimated 4–6% of operating expenses, forcing BTS to adapt proprietary frameworks to national regulatory requirements while protecting a cohesive global brand.

Government investment in workforce reskilling

Many governments increased reskilling funding—OECD reported public spending on active labour market policies rose 8% in 2023, with EU NextGenerationEU allocating €150bn for digital/skills; such subsidies boost demand for BTS Group’s strategy services. BTS is well placed to win public-private contracts as nations treat workforce upskilling as economic security, driving higher consulting revenues in large-scale AI-era programs.

Trade policy and professional mobility

Changes in visa regulations and professional service trade agreements have reduced cross-border mobility for BTS consultants, with 2025 data showing a 22% decline in short-term business visas in key markets, forcing greater reliance on local talent hubs over the previous fly-in-fly-out model.

This shift raises operational costs—estimated 8–12% higher due to local hiring and training—and pushes BTS toward a decentralized structure to maintain delivery quality for multinational clients across 30+ markets.

Regulatory shifts in major markets

Political shifts in major markets have prompted tighter corporate governance and reporting—EU CSRD expands scope to ~50,000 companies from 2024, while SEC climate rules target ~14,000 filers—forcing BTS Group to rapidly update advisory frameworks.

BTS integrates these regulatory variables into leader simulations; clients practicing under scenarios reflecting a 20–40% rise in compliance costs see faster strategic alignment and reduced policy-risk exposure.

- CSRD: ~50,000 EU firms impacted

- SEC: ~14,000 US filers affected

- Compliance cost rise modeled: 20–40%

- Simulations include regulatory volatility scenarios

Stability in emerging market expansions

BTS Group’s expansion into emerging markets—which accounted for about 28% of FY2024 revenue—faces political stability risks that can affect contracts, staff safety and ROI; rigorous political risk assessments and scenario planning are essential to protect investments in countries with high administrative turnover.

Forming local partnerships and joint ventures—BTS closed 3 regional alliances in SE Asia in 2024—reduces exposure, improves compliance, and supports sustainable operations in non-traditional markets.

- 28% FY2024 revenue from emerging markets

- 3 regional partnerships established in SE Asia (2024)

- Mandatory political risk assessments and scenario planning

- Local JV/partnerships mitigate administrative volatility

Compliance costs soar as reskilling demand and visa cuts reshape global delivery

Political fragmentation, trade/data rules and visa limits raised compliance and delivery costs (FY2024: 62% revenue outside Scandinavia; emerging markets 28%); public reskilling funds (OECD +8% in 2023; EU €150bn NextGenerationEU) lift demand; CSRD (~50,000 firms) and SEC (~14,000) expand advisory scope; local hiring up 8–12% cost, short-term business visas down 22% (2025).

| Metric | Value |

|---|---|

| Revenue outside Scandinavia (FY2024) | 62% |

| Emerging markets share (FY2024) | 28% |

| Visa decline (key markets, 2025) | -22% |

| Local hiring cost increase | +8–12% |

| Public reskilling spend change (OECD, 2023) | +8% |

| NextGenerationEU allocation | €150bn |

| CSRD affected firms | ~50,000 |

| SEC affected filers | ~14,000 |

What is included in the product

Explores how macro-environmental factors uniquely affect BTS Group across Political, Economic, Social, Technological, Environmental and Legal dimensions, with each section grounded in current market and regulatory dynamics relevant to its regions and services.

A concise BTS Group PESTLE summary that’s visually segmented for quick interpretation, easily dropped into presentations or shared across teams to support planning and risk discussions.

Economic factors

Corporate L&D budget resilience

Despite economic swings, corporate L&D spending rose to an estimated global total of about USD 420 billion in 2024, with surveys showing 72% of firms prioritizing leadership development for strategy execution over headcount growth.

By end-2025 many companies treat leadership programs as risk mitigation; 65% plan stable or increased L&D budgets according to 2024–25 corporate surveys.

BTS Group capitalizes on this by linking behavioral simulations to ROI, citing client case studies reporting average productivity gains of 8–12% and payback within 12–18 months.

Currency volatility and hedging

As a Swedish firm with a large global footprint, BTS Group faces material SEK volatility versus USD and EUR; in 2024 SEK weakened ~6% vs USD and ~3% vs EUR, amplifying translation effects on reported revenue. Revenue translation and cross-border cost management require layered hedging—currency forwards, options and natural hedges—to shield the 2024–2025 operating margin (reported 8.9% in FY2024) from sudden swings. The firm’s financial performance closely tracks its hedge effectiveness across North America, Europe and APAC segments, where FX-adjusted revenue growth varied by up to 7 percentage points in 2024.

Global interest rate stabilization

By end-2025, global policy rates largely stabilized—OECD average policy rate ~3.5%—giving firms clearer capital-allocation signals and prompting BTS clients to shift toward multi-year strategic engagements over ad-hoc projects.

Lower corporate borrowing costs—global corporate bond yields down ~120 bps vs 2023—enabled larger-scale digital transformations, increasing demand for BTS change-management services tied to multi-year contracts.

Labor market tightness and talent wars

The global shortage of senior strategic talent—McKinsey estimated a 25% gap in leadership readiness in 2024—heightens demand for BTS Group’s leadership development, boosting its value proposition as firms avoid costly external hires amid rising recruitment costs (US average manager hire cost up 18% in 2024).

Firms prioritize internal development: 68% of companies in a 2025 Deloitte survey planned to upskill mid-level managers, enabling BTS to scale programs that cut promotion-to-readiness time by ~30% and support executive pipelines efficiently.

- BTS revenue leverage: higher client retention from leadership programs;

- Market tailwind: rising L&D spend—global corporate training market ~USD 440bn (2024);

- Competitive edge: scalable simulations reduce time-to-ready for promotions ~30%;

- Risk: talent scarcity increases demand but also competition from tech-enabled providers.

Emerging market growth trajectories

Economic growth in Southeast Asia (GDP growth ~4.5%–5.5% in 2024–25) and select Latin American markets (2024 GDP ~2.5% with faster recovery pockets) offers BTS diversification opportunities as corporates scale strategy and leadership programs.

Rapid market maturation increases demand for sophisticated strategy-alignment tools; BTS’s localized high-tech simulations support premium pricing and higher adoption, contributing to its late-2025 valuation uplift.

Localization capability, combined with regional revenue mix expansion (EM revenue share potential +10–15% by 2025), is a key value driver for BTS.

- SE Asia GDP growth ~4.5%–5.5% (2024–25)

- LatAm recovery ~2.5% GDP (2024) with accelerating segments

- EM revenue share upside +10–15% by 2025

- Localization of simulations supports premium pricing

BTS: Rising L&D spend, EM upside and hedging amid SEK volatility

BTS benefits from rising L&D spend (global training market ~USD 440bn in 2024) and stable policy rates (~3.5% OECD avg, 2025), driving multi-year contracts; FY2024 margin 8.9% with SEK volatility (SEK -6% vs USD, -3% vs EUR in 2024) requiring layered hedging; EM growth (SE Asia GDP ~4.5–5.5% 2024–25) offers +10–15% revenue mix upside; leadership gaps (25% readiness shortfall, 2024) boost demand.

| Metric | 2024/25 |

|---|---|

| Global L&D market | ~USD 440bn |

| OECD policy rate | ~3.5% |

| FY2024 margin | 8.9% |

| SEK vs USD/EUR 2024 | -6% / -3% |

What You See Is What You Get

BTS Group PESTLE Analysis

The preview shown here is the exact BTS Group PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Competitive Advantage Starts with This Report

Discover how political shifts, economic cycles, social trends, and technological advances are shaping BTS Group’s strategic outlook—our concise PESTLE snapshot highlights key external forces and their implications for growth and risk management; purchase the full analysis to access the complete, actionable report and ready-to-use slides for strategic planning.

Political factors

Geopolitical fragmentation and global operations

As of late 2025, BTS Group faces geopolitical fragmentation requiring localized strategy execution; 62% of its revenue in FY2024 came from outside Scandinavia, intensifying exposure to divergent US, EU and China trade policies that affect client deployment of training and leadership programs.

Rising tariffs and data localization laws have increased compliance costs by an estimated 4–6% of operating expenses, forcing BTS to adapt proprietary frameworks to national regulatory requirements while protecting a cohesive global brand.

Government investment in workforce reskilling

Many governments increased reskilling funding—OECD reported public spending on active labour market policies rose 8% in 2023, with EU NextGenerationEU allocating €150bn for digital/skills; such subsidies boost demand for BTS Group’s strategy services. BTS is well placed to win public-private contracts as nations treat workforce upskilling as economic security, driving higher consulting revenues in large-scale AI-era programs.

Trade policy and professional mobility

Changes in visa regulations and professional service trade agreements have reduced cross-border mobility for BTS consultants, with 2025 data showing a 22% decline in short-term business visas in key markets, forcing greater reliance on local talent hubs over the previous fly-in-fly-out model.

This shift raises operational costs—estimated 8–12% higher due to local hiring and training—and pushes BTS toward a decentralized structure to maintain delivery quality for multinational clients across 30+ markets.

Regulatory shifts in major markets

Political shifts in major markets have prompted tighter corporate governance and reporting—EU CSRD expands scope to ~50,000 companies from 2024, while SEC climate rules target ~14,000 filers—forcing BTS Group to rapidly update advisory frameworks.

BTS integrates these regulatory variables into leader simulations; clients practicing under scenarios reflecting a 20–40% rise in compliance costs see faster strategic alignment and reduced policy-risk exposure.

- CSRD: ~50,000 EU firms impacted

- SEC: ~14,000 US filers affected

- Compliance cost rise modeled: 20–40%

- Simulations include regulatory volatility scenarios

Stability in emerging market expansions

BTS Group’s expansion into emerging markets—which accounted for about 28% of FY2024 revenue—faces political stability risks that can affect contracts, staff safety and ROI; rigorous political risk assessments and scenario planning are essential to protect investments in countries with high administrative turnover.

Forming local partnerships and joint ventures—BTS closed 3 regional alliances in SE Asia in 2024—reduces exposure, improves compliance, and supports sustainable operations in non-traditional markets.

- 28% FY2024 revenue from emerging markets

- 3 regional partnerships established in SE Asia (2024)

- Mandatory political risk assessments and scenario planning

- Local JV/partnerships mitigate administrative volatility

Compliance costs soar as reskilling demand and visa cuts reshape global delivery

Political fragmentation, trade/data rules and visa limits raised compliance and delivery costs (FY2024: 62% revenue outside Scandinavia; emerging markets 28%); public reskilling funds (OECD +8% in 2023; EU €150bn NextGenerationEU) lift demand; CSRD (~50,000 firms) and SEC (~14,000) expand advisory scope; local hiring up 8–12% cost, short-term business visas down 22% (2025).

| Metric | Value |

|---|---|

| Revenue outside Scandinavia (FY2024) | 62% |

| Emerging markets share (FY2024) | 28% |

| Visa decline (key markets, 2025) | -22% |

| Local hiring cost increase | +8–12% |

| Public reskilling spend change (OECD, 2023) | +8% |

| NextGenerationEU allocation | €150bn |

| CSRD affected firms | ~50,000 |

| SEC affected filers | ~14,000 |

What is included in the product

Explores how macro-environmental factors uniquely affect BTS Group across Political, Economic, Social, Technological, Environmental and Legal dimensions, with each section grounded in current market and regulatory dynamics relevant to its regions and services.

A concise BTS Group PESTLE summary that’s visually segmented for quick interpretation, easily dropped into presentations or shared across teams to support planning and risk discussions.

Economic factors

Corporate L&D budget resilience

Despite economic swings, corporate L&D spending rose to an estimated global total of about USD 420 billion in 2024, with surveys showing 72% of firms prioritizing leadership development for strategy execution over headcount growth.

By end-2025 many companies treat leadership programs as risk mitigation; 65% plan stable or increased L&D budgets according to 2024–25 corporate surveys.

BTS Group capitalizes on this by linking behavioral simulations to ROI, citing client case studies reporting average productivity gains of 8–12% and payback within 12–18 months.

Currency volatility and hedging

As a Swedish firm with a large global footprint, BTS Group faces material SEK volatility versus USD and EUR; in 2024 SEK weakened ~6% vs USD and ~3% vs EUR, amplifying translation effects on reported revenue. Revenue translation and cross-border cost management require layered hedging—currency forwards, options and natural hedges—to shield the 2024–2025 operating margin (reported 8.9% in FY2024) from sudden swings. The firm’s financial performance closely tracks its hedge effectiveness across North America, Europe and APAC segments, where FX-adjusted revenue growth varied by up to 7 percentage points in 2024.

Global interest rate stabilization

By end-2025, global policy rates largely stabilized—OECD average policy rate ~3.5%—giving firms clearer capital-allocation signals and prompting BTS clients to shift toward multi-year strategic engagements over ad-hoc projects.

Lower corporate borrowing costs—global corporate bond yields down ~120 bps vs 2023—enabled larger-scale digital transformations, increasing demand for BTS change-management services tied to multi-year contracts.

Labor market tightness and talent wars

The global shortage of senior strategic talent—McKinsey estimated a 25% gap in leadership readiness in 2024—heightens demand for BTS Group’s leadership development, boosting its value proposition as firms avoid costly external hires amid rising recruitment costs (US average manager hire cost up 18% in 2024).

Firms prioritize internal development: 68% of companies in a 2025 Deloitte survey planned to upskill mid-level managers, enabling BTS to scale programs that cut promotion-to-readiness time by ~30% and support executive pipelines efficiently.

- BTS revenue leverage: higher client retention from leadership programs;

- Market tailwind: rising L&D spend—global corporate training market ~USD 440bn (2024);

- Competitive edge: scalable simulations reduce time-to-ready for promotions ~30%;

- Risk: talent scarcity increases demand but also competition from tech-enabled providers.

Emerging market growth trajectories

Economic growth in Southeast Asia (GDP growth ~4.5%–5.5% in 2024–25) and select Latin American markets (2024 GDP ~2.5% with faster recovery pockets) offers BTS diversification opportunities as corporates scale strategy and leadership programs.

Rapid market maturation increases demand for sophisticated strategy-alignment tools; BTS’s localized high-tech simulations support premium pricing and higher adoption, contributing to its late-2025 valuation uplift.

Localization capability, combined with regional revenue mix expansion (EM revenue share potential +10–15% by 2025), is a key value driver for BTS.

- SE Asia GDP growth ~4.5%–5.5% (2024–25)

- LatAm recovery ~2.5% GDP (2024) with accelerating segments

- EM revenue share upside +10–15% by 2025

- Localization of simulations supports premium pricing

BTS: Rising L&D spend, EM upside and hedging amid SEK volatility

BTS benefits from rising L&D spend (global training market ~USD 440bn in 2024) and stable policy rates (~3.5% OECD avg, 2025), driving multi-year contracts; FY2024 margin 8.9% with SEK volatility (SEK -6% vs USD, -3% vs EUR in 2024) requiring layered hedging; EM growth (SE Asia GDP ~4.5–5.5% 2024–25) offers +10–15% revenue mix upside; leadership gaps (25% readiness shortfall, 2024) boost demand.

| Metric | 2024/25 |

|---|---|

| Global L&D market | ~USD 440bn |

| OECD policy rate | ~3.5% |

| FY2024 margin | 8.9% |

| SEK vs USD/EUR 2024 | -6% / -3% |

What You See Is What You Get

BTS Group PESTLE Analysis

The preview shown here is the exact BTS Group PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.