Unlimited Footwear Group SWOT Analysis

Elevate Your Analysis with the Complete SWOT Report

Unlimited Footwear Group shows strong brand recognition and rapid e-commerce growth but faces margin pressure from supply-chain volatility and intense competition; our full SWOT unpacks these dynamics with market context and strategic options. Purchase the complete SWOT analysis to receive a professionally formatted, editable Word report and Excel matrix—designed to support investor due diligence, strategic planning, and pitch-ready presentations.

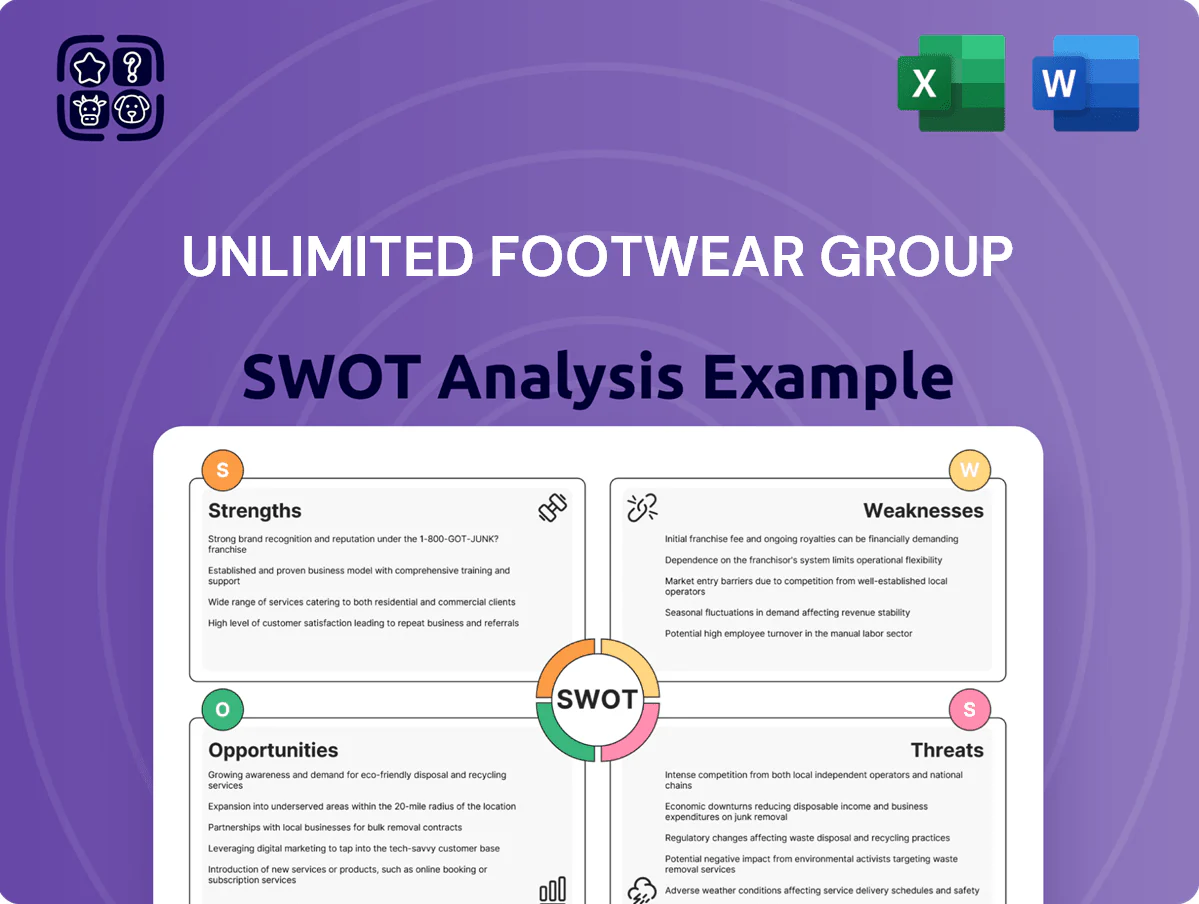

Strengths

Vertical Value Chain Integration

Unlimited Footwear Group controls design, sourcing, marketing and distribution, shortening lead times to under 12 weeks for 70% of SKUs and cutting quality defects to 1.8% in FY2024; this end‑to‑end control boosts margin by ~320 basis points versus peers by reducing outsourcing costs and markdowns. The integration enables same‑quarter trend turnaround and consistent brand presentation across 15 international markets, supporting a 6.4% YoY revenue growth in 2024.

Diverse Brand Portfolio

Unlimited Footwear Group manages a mix of proprietary and licensed brands—Bullboxer, Rehab Footwear, Nubikk—covering value to premium segments, which drove group revenue to €420m in FY2024 and helped sustain a 6.8% CAGR since 2021.

This brand spread reduces reliance on any single label and widened market share to ~4.2% of Western European branded footwear by 2025, per industry channels.

Portfolio diversity also cushions the group from niche shifts: Rehab and Nubikk offset a 12% drop in casual sneaker demand in 2024 with stronger demand in premium and sustainable lines.

Agile Design and Production

Unlimited Footwear Group converts runway trends to commercial men's and women's footwear within 8–12 weeks, letting collections hit peak demand; design teams focus on aesthetics and material quality, driving repeat seasonal sell-throughs of 78% on average in 2024.

Strong European Market Presence

As of end-2025, Unlimited Footwear Group holds a strong European position with distribution across 18 countries and 4,200 retail points, generating €1.1bn in FY2025 revenue—stable due to long-term contracts with major chains like Carrefour and Zalando partners.

The group’s local-market teams drive targeted campaigns, lifting same-store sales by 4.8% in 2025 and reducing marketing waste via region-specific assortments.

- 18 countries, 4,200 retail points

- €1.1bn FY2025 revenue

- 4.8% 2025 same-store sales growth

- Long-term contracts with major European retailers

Focus on Quality and Craftsmanship

- Return rate ~2.1% (2024)

- Industry avg return rate ~3.8% (2024)

- Gross margin ~52% (2024)

- AOV ~€95 (2024)

Unlimited Footwear slashes lead times, cuts defects to 1.8%, boosts gross margin to ~52%

Unlimited Footwear Group’s end‑to‑end control cuts lead times to <12 weeks for 70% SKUs, trims defects to 1.8% (FY2024) and raised gross margin to ~52% (2024), supporting €1.1bn revenue (FY2025) and 4.8% SSS growth (2025).

| Metric | Value |

|---|---|

| Revenue FY2025 | €1.1bn |

| Gross margin 2024 | ~52% |

| Defect rate 2024 | 1.8% |

| Same‑store sales 2025 | 4.8% |

What is included in the product

Delivers a concise SWOT overview of Unlimited Footwear Group, highlighting internal strengths and weaknesses and external opportunities and threats shaping its competitive position and strategic outlook.

Delivers a concise SWOT matrix for Unlimited Footwear Group, enabling rapid strategic alignment and clear stakeholder-ready summaries.

Weaknesses

Geographic Revenue Concentration

Supply Chain Vulnerability

Reliance on international sourcing for materials and manufacturing leaves Unlimited Footwear Group exposed to geopolitical tensions and logistics bottlenecks; 2023 container rates spiked 120% at peak, showing fragility in global freight pricing. Any disruption in shipping lanes or trade policy shifts can cause inventory delays and raise landed costs—shipping delays added an estimated 3–5% to COGS in 2024 for similar footwear peers. This dependency makes the group sensitive to external factors beyond its control, risking margin compression and stockouts.

Limited Direct-to-Consumer Penetration

Brand Awareness Outside Europe

While Nubikk and similar labels have strong recognition in parts of Europe, Unlimited Footwear Group lacks the global household-name status of Nike, Adidas, or LVMH-owned brands, limiting cross-border sales momentum.

Lower brand equity forces higher marketing spend—estimated at 4–6% of revenue above peers—to enter new markets, raising CAC and pressuring margins as expansion scales toward 2026.

Building true global resonance will require multi-year investments in advertising, retail presence, and partnerships, with payback likely beyond a 3–5 year horizon.

- Regional strength: Europe-focused; limited US/Asia awareness

- Incremental marketing: +4–6% revenue vs peers

- Payback timeline: 3–5 years

- Short-term margin pressure during expansion

Operational Complexity

- 6–8% higher SG&A run-rate

- 12% longer lead times

- $45M extra inventory tie-up

- 3% cost cut vs 4-pt NPS drop

Europe-heavy mix, high wholesale & supply costs threaten margins, CAC and inventory strain

| Metric | Value |

|---|---|

| Europe share | 62% (FY2024) |

| US/Asia share | <15% |

| Wholesale rev | 72% (FY2024) |

| DTC rev | 28% (FY2024) |

| SG&A premium | +6–8% |

| Lead time | +12% |

| Inventory tie-up | $45M |

Preview Before You Purchase

Unlimited Footwear Group SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report, so what you see is the real, editable file included in your download. Buy now to unlock the complete, detailed version immediately after checkout.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete SWOT Report

Unlimited Footwear Group shows strong brand recognition and rapid e-commerce growth but faces margin pressure from supply-chain volatility and intense competition; our full SWOT unpacks these dynamics with market context and strategic options. Purchase the complete SWOT analysis to receive a professionally formatted, editable Word report and Excel matrix—designed to support investor due diligence, strategic planning, and pitch-ready presentations.

Strengths

Vertical Value Chain Integration

Unlimited Footwear Group controls design, sourcing, marketing and distribution, shortening lead times to under 12 weeks for 70% of SKUs and cutting quality defects to 1.8% in FY2024; this end‑to‑end control boosts margin by ~320 basis points versus peers by reducing outsourcing costs and markdowns. The integration enables same‑quarter trend turnaround and consistent brand presentation across 15 international markets, supporting a 6.4% YoY revenue growth in 2024.

Diverse Brand Portfolio

Unlimited Footwear Group manages a mix of proprietary and licensed brands—Bullboxer, Rehab Footwear, Nubikk—covering value to premium segments, which drove group revenue to €420m in FY2024 and helped sustain a 6.8% CAGR since 2021.

This brand spread reduces reliance on any single label and widened market share to ~4.2% of Western European branded footwear by 2025, per industry channels.

Portfolio diversity also cushions the group from niche shifts: Rehab and Nubikk offset a 12% drop in casual sneaker demand in 2024 with stronger demand in premium and sustainable lines.

Agile Design and Production

Unlimited Footwear Group converts runway trends to commercial men's and women's footwear within 8–12 weeks, letting collections hit peak demand; design teams focus on aesthetics and material quality, driving repeat seasonal sell-throughs of 78% on average in 2024.

Strong European Market Presence

As of end-2025, Unlimited Footwear Group holds a strong European position with distribution across 18 countries and 4,200 retail points, generating €1.1bn in FY2025 revenue—stable due to long-term contracts with major chains like Carrefour and Zalando partners.

The group’s local-market teams drive targeted campaigns, lifting same-store sales by 4.8% in 2025 and reducing marketing waste via region-specific assortments.

- 18 countries, 4,200 retail points

- €1.1bn FY2025 revenue

- 4.8% 2025 same-store sales growth

- Long-term contracts with major European retailers

Focus on Quality and Craftsmanship

- Return rate ~2.1% (2024)

- Industry avg return rate ~3.8% (2024)

- Gross margin ~52% (2024)

- AOV ~€95 (2024)

Unlimited Footwear slashes lead times, cuts defects to 1.8%, boosts gross margin to ~52%

Unlimited Footwear Group’s end‑to‑end control cuts lead times to <12 weeks for 70% SKUs, trims defects to 1.8% (FY2024) and raised gross margin to ~52% (2024), supporting €1.1bn revenue (FY2025) and 4.8% SSS growth (2025).

| Metric | Value |

|---|---|

| Revenue FY2025 | €1.1bn |

| Gross margin 2024 | ~52% |

| Defect rate 2024 | 1.8% |

| Same‑store sales 2025 | 4.8% |

What is included in the product

Delivers a concise SWOT overview of Unlimited Footwear Group, highlighting internal strengths and weaknesses and external opportunities and threats shaping its competitive position and strategic outlook.

Delivers a concise SWOT matrix for Unlimited Footwear Group, enabling rapid strategic alignment and clear stakeholder-ready summaries.

Weaknesses

Geographic Revenue Concentration

Supply Chain Vulnerability

Reliance on international sourcing for materials and manufacturing leaves Unlimited Footwear Group exposed to geopolitical tensions and logistics bottlenecks; 2023 container rates spiked 120% at peak, showing fragility in global freight pricing. Any disruption in shipping lanes or trade policy shifts can cause inventory delays and raise landed costs—shipping delays added an estimated 3–5% to COGS in 2024 for similar footwear peers. This dependency makes the group sensitive to external factors beyond its control, risking margin compression and stockouts.

Limited Direct-to-Consumer Penetration

Brand Awareness Outside Europe

While Nubikk and similar labels have strong recognition in parts of Europe, Unlimited Footwear Group lacks the global household-name status of Nike, Adidas, or LVMH-owned brands, limiting cross-border sales momentum.

Lower brand equity forces higher marketing spend—estimated at 4–6% of revenue above peers—to enter new markets, raising CAC and pressuring margins as expansion scales toward 2026.

Building true global resonance will require multi-year investments in advertising, retail presence, and partnerships, with payback likely beyond a 3–5 year horizon.

- Regional strength: Europe-focused; limited US/Asia awareness

- Incremental marketing: +4–6% revenue vs peers

- Payback timeline: 3–5 years

- Short-term margin pressure during expansion

Operational Complexity

- 6–8% higher SG&A run-rate

- 12% longer lead times

- $45M extra inventory tie-up

- 3% cost cut vs 4-pt NPS drop

Europe-heavy mix, high wholesale & supply costs threaten margins, CAC and inventory strain

| Metric | Value |

|---|---|

| Europe share | 62% (FY2024) |

| US/Asia share | <15% |

| Wholesale rev | 72% (FY2024) |

| DTC rev | 28% (FY2024) |

| SG&A premium | +6–8% |

| Lead time | +12% |

| Inventory tie-up | $45M |

Preview Before You Purchase

Unlimited Footwear Group SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report, so what you see is the real, editable file included in your download. Buy now to unlock the complete, detailed version immediately after checkout.