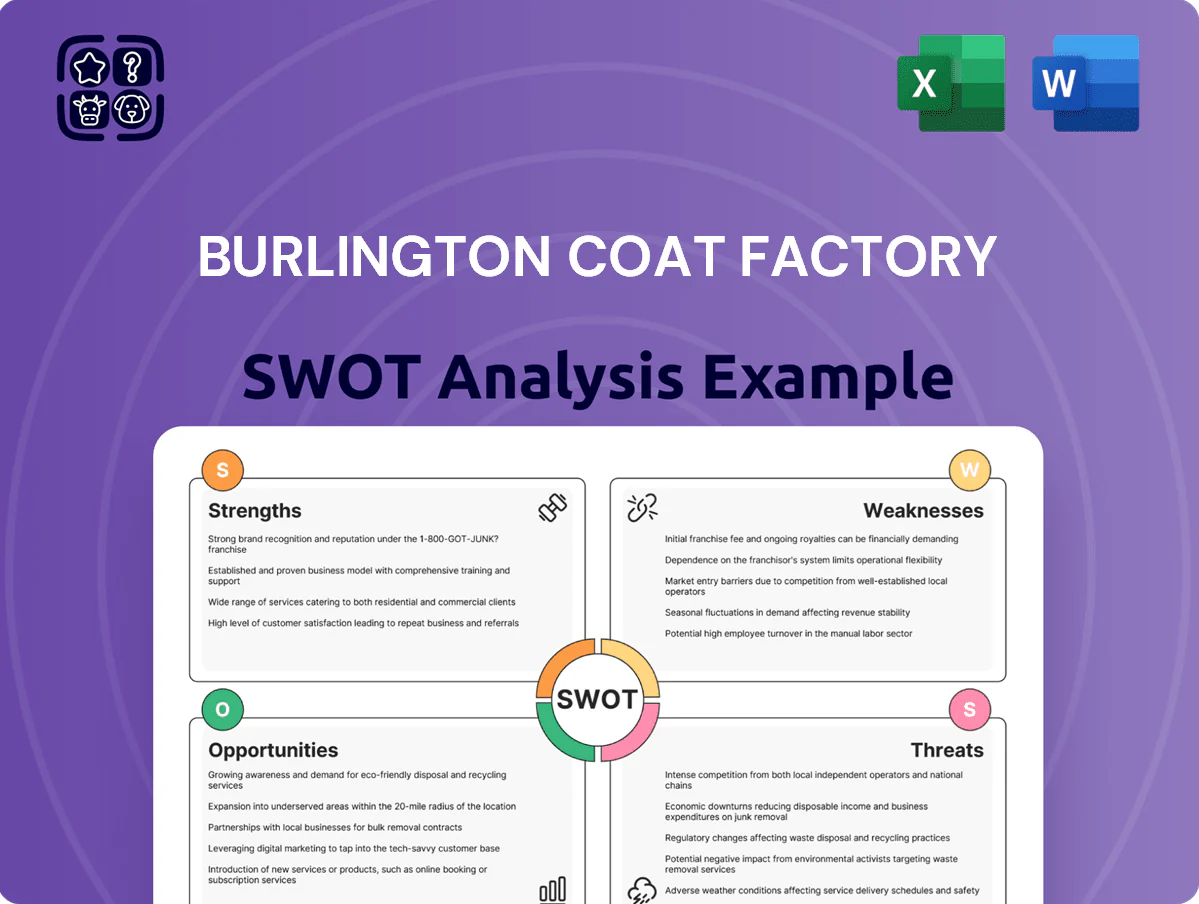

Burlington Coat Factory SWOT Analysis

Elevate Your Analysis with the Complete SWOT Report

Burlington Coat Factory shows resilient off-price appeal with strong value branding and wide geographic reach, yet faces margin pressure from rising costs and intense competition from online and discount rivals; shifting consumer trends and supply-chain risks could amplify vulnerabilities. Discover the full SWOT analysis for a research-backed, editable report and Excel matrix that equips investors and strategists to act with confidence.

Strengths

Resilient Off-Price Business Model

Burlington’s off-price model draws value-seeking shoppers: in FY2024 the chain reported average ticket growth of 3.5% and comparable-store sales up 4.2%, showing demand across income brackets during mixed macro conditions.

Its flexible buying lets merchandising shift fast to trending categories and seasonal items, supported by inventory turn of ~4.6x in 2024, keeping assortments fresh.

This agility drives steady foot traffic and market share while many full‑price department stores saw traffic declines of 6–10% in 2023–24.

Successful Burlington 2.0 Execution

Strong Global Vendor Relationships

Burlington’s relationships with thousands of brands and vendors supply a steady stream of discounted designer and high-quality merchandise—Burlington reported 2024 inventory purchases up 8% vs 2023, enabling gross margin expansion to 36.2% in FY2024.

These deep partnerships let Burlington buy opportunistically, keeping assortments diverse across apparel, home, and footwear, which supports average transaction growth of 4.1% in 2024.

The curated “treasure hunt” assortment drives loyalty—Burlington recorded 60% of sales from repeat customers in 2024, underlining this advantage.

Aggressive Store Expansion Pipeline

- 65 net new stores in FY2024

- ~1,000 stores end-2024; target 1,070+ in 2025

- ~9% revenue lift from unit growth in 2024

Enhanced Inventory Management Systems

Lower days‑in‑stock reduced end‑of‑season markdowns, protecting gross margin; Burlington reported a 60 bps gross margin improvement in fiscal 2024 versus 2023.

These efficiency gains boosted operating cash flow, freeing roughly $120 million in working capital in 2024 for faster reinvestment into new inventory assortments.

- 12% drop in days‑in‑stock (2024)

- 60 bps gross margin improvement (FY2024)

- $120M working capital freed (2024)

Burlington boosts margins and sales with faster turns, 65 new stores and $120M freed

Burlington’s off‑price model and treasure‑hunt assortments drove FY2024 comps +4.2% and average ticket +3.5%; inventory turn ~4.6x and days‑in‑stock down 12% cut markdowns and raised gross margin to 36.2% (↑60 bps). Burlington opened 65 net new stores (≈1,000 total end‑2024; target 1,070+ in 2025), lifting sales per sq ft ~12% and freeing ~$120M working capital.

| Metric | FY2024 |

|---|---|

| Comparable sales | +4.2% |

| Average ticket | +3.5% |

| Inventory turn | ~4.6x |

| Days‑in‑stock | ↓12% |

| Gross margin | 36.2% (↑60 bps) |

| Net new stores | 65 |

| Store count | ~1,000 |

| Working capital freed | $120M |

What is included in the product

Provides a concise SWOT analysis of Burlington Coat Factory, mapping its retail strengths and operational weaknesses while highlighting growth opportunities and external threats shaping its competitive position.

Provides a concise Burlington Coat Factory SWOT matrix for fast, visual strategy alignment and quick executive snapshots.

Weaknesses

Lower Operating Margins Than Peer Leaders

Despite margin gains, Burlington Stores reported a 2024 adjusted operating margin of 7.1%, still below TJX Companies’ 9.8% and Ross Stores’ 10.4% (FY 2024), reflecting persistent profitability lag.

Higher SG&A and distribution costs—about 21.5% of revenue in 2024 versus TJX 18.2%—compress earnings and limit cash flexibility.

These tighter margins reduce buffer for demand shocks, raising downside risk in abrupt retail downturns.

Limited E-commerce Presence

The strategic decision to de-emphasize online sales limits Burlington Stores’ reach to younger, digital-first shoppers; US e-commerce apparel sales grew 12% in 2024 to about $171B, where Burlington’s online share remains under 2% of company sales.

The off-price model is hard to replicate digitally, but Burlington’s weak digital storefront and 2024 digital conversion rates near 1% create friction versus omnichannel rivals like TJX and Ross.

This absence keeps Burlington from capturing more of the omnichannel market, which accounted for roughly 40% of US retail sales in 2024, constraining growth and customer lifetime value.

Smaller Scale Relative to Top Competitors

Burlington operates about 847 stores vs TJX's ~5,800 and Ross Stores' ~2,300 (FY2024), and reported $9.9B revenue in FY2024 versus TJX $57B and Ross $21B, giving Burlington weaker supplier bargaining power and higher per-store procurement costs.

Smaller scale limits spreading fixed costs—distribution, rent, and IT—across fewer locations, raising unit SG&A versus larger rivals; matching their $1B+ marketing and expansive logistics investments remains a material challenge.

Historical Brand Perception Challenges

Many shoppers still see Burlington primarily as a coat retailer despite 2024 revenue showing 70% of sales from non-outerwear categories (Burlington Stores, FY2024), so reshaping perception needs sustained marketing spend—Burlington's SG&A was $1.28B in 2024, underscoring cost pressure.

Older, unrenovated stores create inconsistent layouts that hurt a unified brand image; 15% of stores remained in legacy formats at end-2024, complicating experiential upgrades.

- 70% sales non-outerwear (FY2024)

- $1.28B SG&A (2024)

- 15% legacy-format stores (end-2024)

Heavy Dependence on Third-Party Brands

- ~78% branded purchases (2024)

- U.S. DTC apparel +9% (2023)

- Higher sourcing cost risk, lower assort consistency

Burlington lagging peers: tight margins, high SG&A and weak e‑commerce constrain growth

Burlington’s margins lag peers (7.1% adj. op. margin vs TJX 9.8%, Ross 10.4% FY2024), high SG&A (21.5% revenue; $1.28B 2024) and weak e‑commerce (<2% sales; ~1% conversion) constrain growth; smaller scale (847 stores; $9.9B revenue 2024) reduces bargaining power and raises sourcing risk (~78% branded purchases).

| Metric | 2024 |

|---|---|

| Adj. op. margin | 7.1% |

| SG&A | $1.28B (21.5%) |

| Stores | 847 |

| Online share | <2% |

Same Document Delivered

Burlington Coat Factory SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get and reflects the same structure, insights, and editable content included in the downloadable file. Purchase unlocks the complete, in-depth version with full strengths, weaknesses, opportunities, and threats for Burlington Coat Factory.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete SWOT Report

Burlington Coat Factory shows resilient off-price appeal with strong value branding and wide geographic reach, yet faces margin pressure from rising costs and intense competition from online and discount rivals; shifting consumer trends and supply-chain risks could amplify vulnerabilities. Discover the full SWOT analysis for a research-backed, editable report and Excel matrix that equips investors and strategists to act with confidence.

Strengths

Resilient Off-Price Business Model

Burlington’s off-price model draws value-seeking shoppers: in FY2024 the chain reported average ticket growth of 3.5% and comparable-store sales up 4.2%, showing demand across income brackets during mixed macro conditions.

Its flexible buying lets merchandising shift fast to trending categories and seasonal items, supported by inventory turn of ~4.6x in 2024, keeping assortments fresh.

This agility drives steady foot traffic and market share while many full‑price department stores saw traffic declines of 6–10% in 2023–24.

Successful Burlington 2.0 Execution

Strong Global Vendor Relationships

Burlington’s relationships with thousands of brands and vendors supply a steady stream of discounted designer and high-quality merchandise—Burlington reported 2024 inventory purchases up 8% vs 2023, enabling gross margin expansion to 36.2% in FY2024.

These deep partnerships let Burlington buy opportunistically, keeping assortments diverse across apparel, home, and footwear, which supports average transaction growth of 4.1% in 2024.

The curated “treasure hunt” assortment drives loyalty—Burlington recorded 60% of sales from repeat customers in 2024, underlining this advantage.

Aggressive Store Expansion Pipeline

- 65 net new stores in FY2024

- ~1,000 stores end-2024; target 1,070+ in 2025

- ~9% revenue lift from unit growth in 2024

Enhanced Inventory Management Systems

Lower days‑in‑stock reduced end‑of‑season markdowns, protecting gross margin; Burlington reported a 60 bps gross margin improvement in fiscal 2024 versus 2023.

These efficiency gains boosted operating cash flow, freeing roughly $120 million in working capital in 2024 for faster reinvestment into new inventory assortments.

- 12% drop in days‑in‑stock (2024)

- 60 bps gross margin improvement (FY2024)

- $120M working capital freed (2024)

Burlington boosts margins and sales with faster turns, 65 new stores and $120M freed

Burlington’s off‑price model and treasure‑hunt assortments drove FY2024 comps +4.2% and average ticket +3.5%; inventory turn ~4.6x and days‑in‑stock down 12% cut markdowns and raised gross margin to 36.2% (↑60 bps). Burlington opened 65 net new stores (≈1,000 total end‑2024; target 1,070+ in 2025), lifting sales per sq ft ~12% and freeing ~$120M working capital.

| Metric | FY2024 |

|---|---|

| Comparable sales | +4.2% |

| Average ticket | +3.5% |

| Inventory turn | ~4.6x |

| Days‑in‑stock | ↓12% |

| Gross margin | 36.2% (↑60 bps) |

| Net new stores | 65 |

| Store count | ~1,000 |

| Working capital freed | $120M |

What is included in the product

Provides a concise SWOT analysis of Burlington Coat Factory, mapping its retail strengths and operational weaknesses while highlighting growth opportunities and external threats shaping its competitive position.

Provides a concise Burlington Coat Factory SWOT matrix for fast, visual strategy alignment and quick executive snapshots.

Weaknesses

Lower Operating Margins Than Peer Leaders

Despite margin gains, Burlington Stores reported a 2024 adjusted operating margin of 7.1%, still below TJX Companies’ 9.8% and Ross Stores’ 10.4% (FY 2024), reflecting persistent profitability lag.

Higher SG&A and distribution costs—about 21.5% of revenue in 2024 versus TJX 18.2%—compress earnings and limit cash flexibility.

These tighter margins reduce buffer for demand shocks, raising downside risk in abrupt retail downturns.

Limited E-commerce Presence

The strategic decision to de-emphasize online sales limits Burlington Stores’ reach to younger, digital-first shoppers; US e-commerce apparel sales grew 12% in 2024 to about $171B, where Burlington’s online share remains under 2% of company sales.

The off-price model is hard to replicate digitally, but Burlington’s weak digital storefront and 2024 digital conversion rates near 1% create friction versus omnichannel rivals like TJX and Ross.

This absence keeps Burlington from capturing more of the omnichannel market, which accounted for roughly 40% of US retail sales in 2024, constraining growth and customer lifetime value.

Smaller Scale Relative to Top Competitors

Burlington operates about 847 stores vs TJX's ~5,800 and Ross Stores' ~2,300 (FY2024), and reported $9.9B revenue in FY2024 versus TJX $57B and Ross $21B, giving Burlington weaker supplier bargaining power and higher per-store procurement costs.

Smaller scale limits spreading fixed costs—distribution, rent, and IT—across fewer locations, raising unit SG&A versus larger rivals; matching their $1B+ marketing and expansive logistics investments remains a material challenge.

Historical Brand Perception Challenges

Many shoppers still see Burlington primarily as a coat retailer despite 2024 revenue showing 70% of sales from non-outerwear categories (Burlington Stores, FY2024), so reshaping perception needs sustained marketing spend—Burlington's SG&A was $1.28B in 2024, underscoring cost pressure.

Older, unrenovated stores create inconsistent layouts that hurt a unified brand image; 15% of stores remained in legacy formats at end-2024, complicating experiential upgrades.

- 70% sales non-outerwear (FY2024)

- $1.28B SG&A (2024)

- 15% legacy-format stores (end-2024)

Heavy Dependence on Third-Party Brands

- ~78% branded purchases (2024)

- U.S. DTC apparel +9% (2023)

- Higher sourcing cost risk, lower assort consistency

Burlington lagging peers: tight margins, high SG&A and weak e‑commerce constrain growth

Burlington’s margins lag peers (7.1% adj. op. margin vs TJX 9.8%, Ross 10.4% FY2024), high SG&A (21.5% revenue; $1.28B 2024) and weak e‑commerce (<2% sales; ~1% conversion) constrain growth; smaller scale (847 stores; $9.9B revenue 2024) reduces bargaining power and raises sourcing risk (~78% branded purchases).

| Metric | 2024 |

|---|---|

| Adj. op. margin | 7.1% |

| SG&A | $1.28B (21.5%) |

| Stores | 847 |

| Online share | <2% |

Same Document Delivered

Burlington Coat Factory SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get and reflects the same structure, insights, and editable content included in the downloadable file. Purchase unlocks the complete, in-depth version with full strengths, weaknesses, opportunities, and threats for Burlington Coat Factory.