Burns & McDonnell PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Unlock how political shifts, economic cycles, and technological advances are reshaping Burns & McDonnell’s growth trajectory—our concise PESTLE snapshot highlights key risks and opportunities to inform smarter decisions. Ideal for investors, advisors, and strategists, the full PESTLE delivers deep-dive evidence, actionable recommendations, and editable charts for instant use. Purchase now to access the complete analysis and gain a strategic edge.

Political factors

Federal Infrastructure Funding Initiatives

The Infrastructure Investment and Jobs Act rollout through 2025 allocates about $550 billion in new federal funding, creating a large pipeline for power, water, and transportation projects that underpins Burns & McDonnell’s long-term engineering and construction backlog.

Burns & McDonnell depends on government-backed capex; in 2024 public-sector projects accounted for roughly 45% of U.S. engineering RFPs, making federal budget shifts directly material to revenue visibility and staffing plans.

Energy Transition Policy and Subsidies

Geopolitical Trade Relations and Supply Chains

Global tariffs on steel and aluminum—which rose up to 25% in key markets during 2018–2024 and still add 5–12% procurement cost volatility—directly pressure Burns & McDonnell’s margins on large design-build projects; politically driven export controls and sanctions in 2023–2025 disrupted supply of specialized electrical components, causing average lead-time increases of 20–40% and contract risk upticks reflected in 3–7% higher contingency reserves; active geopolitical sourcing strategies are therefore critical to protect margins in a linked global supply chain.

Defense and Federal Security Spending

As a major DoD and federal contractor, Burns & McDonnell is exposed to shifts in defense appropriations—FY2025 enacted DoD budget ~US$858B—affecting program funding and backlog.

Heightened focus on base modernization and cybersecurity (FY2024 DoD cyber budget ~US$10B) boosts demand for specialized engineering, construction, and cyber services.

Complex federal acquisition rules and potential 2024–2025 legislative changes require strong compliance teams to mitigate contract, schedule, and revenue risks.

- FY2025 DoD budget ~US$858B; cyber ~US$10B

- Opportunities: base modernization, cybersecurity projects

- Risk: evolving federal acquisition regulations and legislative shifts

Local and State Regulatory Influence

State political climates shape utility rate cases and approvals for regional projects; in 2024, 38 state utility commissions processed over 1,200 rate filings totaling roughly $45 billion in requested revenue adjustments, affecting Burns & McDonnell project pricing and timelines.

Engagement with state commissions and local governments is essential to permit cross-border transmission lines—FERC-reported interregional projects in 2023-24 sought >$12 billion in investment, requiring coordinated multi-jurisdictional approvals.

Local political stability is often required for multi-year municipal water and transit upgrades; in 2024 US municipal bond issuances exceeded $500 billion, with stated infrastructure allocations driving project viability and lender confidence.

- 38 state utility commissions processed ~1,200 rate filings in 2024 (~$45B requested)

- Interregional transmission projects sought >$12B (2023-24)

- US municipal bond issuance >$500B in 2024 supporting local infrastructure

Massive US public finance surge—billions for infrastructure, defense, energy, utilities, and muni markets

Federal infrastructure funding (~$550B IIJA through 2025), FY2025 DoD budget ~US$858B and cyber ~US$10B, clean-energy credits (45V, 45Q up to ~$3/kg and ~$85/ton), 2024 state utility filings ~1,200 (~$45B requested), interregional transmission >$12B (2023–24), US municipal bond issuance >$500B (2024) drive project pipelines and regulatory/compliance risks.

| Metric | Value |

|---|---|

| IIJA funding | ~$550B |

| FY2025 DoD | ~$858B |

| DoD cyber | ~$10B |

| State filings (2024) | ~1,200 / $45B |

| Interregional TX (23–24) | >$12B |

| Municipal bonds (2024) | >$500B |

What is included in the product

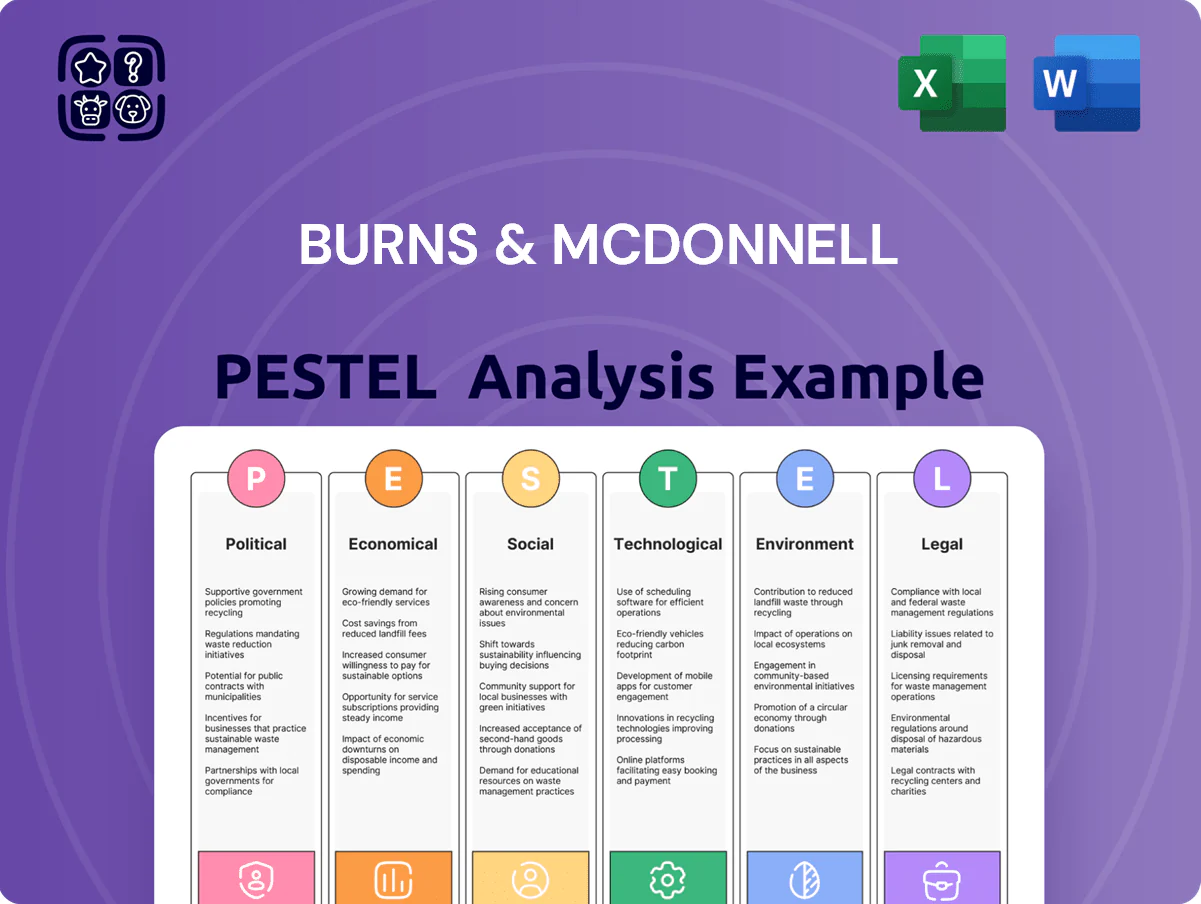

Explores how external macro-environmental factors uniquely affect Burns & McDonnell across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify risks and opportunities, support scenario planning, and inform executives, consultants, and investors with ready-to-use insights for reports and funding pitches.

A concise Burns & McDonnell PESTLE summary that’s easy to drop into presentations or strategy packs, enabling quick alignment across teams and supporting risk discussions during planning sessions.

Economic factors

Interest Rate Environment and Capital Costs

By end-2025, the Federal Reserve funds rate near 5.25–5.50% raises capital costs, reducing feasibility for debt-financed industrial projects and prompting some private clients to defer spend; Moody’s estimates a 15–25% slowdown in new infrastructure financings under such rates. A stabilizing or falling rate trend could cut weighted average cost of capital by 100–200 bps, reviving investment appetite. Burns & McDonnell must embed rate scenarios in cost-benefit models and stress-test returns against rate-sensitive discount rates and loan terms.

Inflationary Pressures on Construction Inputs

Fluctuations in labor and raw material costs erode margins on fixed-price contracts; US construction input prices rose 6.1% year-over-year in 2025 Q4, pressuring profitability. Burns & McDonnell uses economic forecasting and scenario modelling—reducing commodity exposure by hedging and forward procurement—to manage volatility. Persistent inflation has led the firm to tighten escalation clauses and expand strategic sourcing, lowering input-cost variability by an estimated 8–12% per project.

Labor Market Dynamics and Skilled Shortages

The scarcity of specialized engineers and skilled trades remains a major headwind for Burns & McDonnell; US Bureau of Labor Statistics data to 2024 show construction and engineering occupations facing 7–9% vacancy growth year-over-year in specialist roles, tightening supply for complex projects.

Competitive wage inflation—average annual pay growth near 5–6% in 2023–24 for engineering and skilled trades—raises overhead and compresses project margins, increasing bid prices and delivery risk.

Investing in employee ownership and internal training is economically necessary: firms reporting ESOPs or robust apprenticeship pipelines saw 10–15% lower turnover and 3–5% higher productivity in recent industry studies, preserving technical capacity for high-complexity projects.

Global Economic Growth and Industrial Demand

Demand for Burns & McDonnell services tracks global GDP and industrial output; world GDP grew 3.1% in 2024 and manufacturing PMI averaged ~50.8, supporting project pipelines in construction and engineering.

Sector downturns hit spending—global air traffic was still ~10% below 2019 levels in 2024 and oil & gas capex fell ~8% YoY in 2024, reducing facility upgrade projects.

Conversely resilient growth fuels logistics and data center demand: hyperscale data center capacity grew ~20% YoY in 2024 and global e-commerce sales rose 10%, driving modernization projects.

- World GDP +3.1% (2024)

- Manufacturing PMI ~50.8 (2024)

- Air traffic -10% vs 2019 (2024)

- Oil & gas capex -8% YoY (2024)

- Hyperscale data center capacity +20% YoY (2024)

- E‑commerce sales +10% (2024)

Energy Market Volatility

The price gap between natural gas ($2.50–4.00/MMBtu in 2024–25) and levelized cost declines for utility-scale solar ($20–30/MWh) shifts utility/industrial capex, directly affecting Burns & McDonnell project mix and margins.

Rapid policy-driven renewables growth—global clean energy investment hit $1.7T in 2023—can pivot workload from fossil projects to grid, storage, and hydrogen engagements.

Continuous monitoring of global markets (oil near $80/bbl in 2025, power price spikes regionally) lets the firm target consulting where capital is flowing.

- Natural gas $2.50–4.00/MMBtu (2024–25)

- Solar LCOE ~$20–30/MWh

- Global clean energy investment $1.7T (2023)

- Oil ≈ $80/bbl (2025)

Higher rates squeeze infra margins; renewables & hyperscale data centers offset fossil cuts

Higher rates (Fed funds ~5.25–5.50% end-2025) raise WACC, slowing infrastructure financing 15–25%; construction input inflation 6.1% YoY (2025 Q4) and wage growth 5–6% compress margins; labor vacancies up 7–9% for specialists; renewables and data centers (hyperscale +20% YoY) offset fossil capex declines (-8% oil & gas 2024).

| Metric | Value |

|---|---|

| Fed funds | 5.25–5.50% |

| Input inflation | 6.1% YoY |

| Wage growth | 5–6% |

| Labor vacancy | 7–9% |

| Hyperscale DC | +20% YoY |

| Oil & gas capex | -8% YoY |

Preview Before You Purchase

Burns & McDonnell PESTLE Analysis

The preview shown here is the exact Burns & McDonnell PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. It contains the complete political, economic, social, technological, legal, and environmental assessment as displayed, with no placeholders or hidden sections. The layout, content, and structure visible here are exactly what you’ll download immediately after buying. What you see is the final, professionally structured file you’ll own upon checkout.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Unlock how political shifts, economic cycles, and technological advances are reshaping Burns & McDonnell’s growth trajectory—our concise PESTLE snapshot highlights key risks and opportunities to inform smarter decisions. Ideal for investors, advisors, and strategists, the full PESTLE delivers deep-dive evidence, actionable recommendations, and editable charts for instant use. Purchase now to access the complete analysis and gain a strategic edge.

Political factors

Federal Infrastructure Funding Initiatives

The Infrastructure Investment and Jobs Act rollout through 2025 allocates about $550 billion in new federal funding, creating a large pipeline for power, water, and transportation projects that underpins Burns & McDonnell’s long-term engineering and construction backlog.

Burns & McDonnell depends on government-backed capex; in 2024 public-sector projects accounted for roughly 45% of U.S. engineering RFPs, making federal budget shifts directly material to revenue visibility and staffing plans.

Energy Transition Policy and Subsidies

Geopolitical Trade Relations and Supply Chains

Global tariffs on steel and aluminum—which rose up to 25% in key markets during 2018–2024 and still add 5–12% procurement cost volatility—directly pressure Burns & McDonnell’s margins on large design-build projects; politically driven export controls and sanctions in 2023–2025 disrupted supply of specialized electrical components, causing average lead-time increases of 20–40% and contract risk upticks reflected in 3–7% higher contingency reserves; active geopolitical sourcing strategies are therefore critical to protect margins in a linked global supply chain.

Defense and Federal Security Spending

As a major DoD and federal contractor, Burns & McDonnell is exposed to shifts in defense appropriations—FY2025 enacted DoD budget ~US$858B—affecting program funding and backlog.

Heightened focus on base modernization and cybersecurity (FY2024 DoD cyber budget ~US$10B) boosts demand for specialized engineering, construction, and cyber services.

Complex federal acquisition rules and potential 2024–2025 legislative changes require strong compliance teams to mitigate contract, schedule, and revenue risks.

- FY2025 DoD budget ~US$858B; cyber ~US$10B

- Opportunities: base modernization, cybersecurity projects

- Risk: evolving federal acquisition regulations and legislative shifts

Local and State Regulatory Influence

State political climates shape utility rate cases and approvals for regional projects; in 2024, 38 state utility commissions processed over 1,200 rate filings totaling roughly $45 billion in requested revenue adjustments, affecting Burns & McDonnell project pricing and timelines.

Engagement with state commissions and local governments is essential to permit cross-border transmission lines—FERC-reported interregional projects in 2023-24 sought >$12 billion in investment, requiring coordinated multi-jurisdictional approvals.

Local political stability is often required for multi-year municipal water and transit upgrades; in 2024 US municipal bond issuances exceeded $500 billion, with stated infrastructure allocations driving project viability and lender confidence.

- 38 state utility commissions processed ~1,200 rate filings in 2024 (~$45B requested)

- Interregional transmission projects sought >$12B (2023-24)

- US municipal bond issuance >$500B in 2024 supporting local infrastructure

Massive US public finance surge—billions for infrastructure, defense, energy, utilities, and muni markets

Federal infrastructure funding (~$550B IIJA through 2025), FY2025 DoD budget ~US$858B and cyber ~US$10B, clean-energy credits (45V, 45Q up to ~$3/kg and ~$85/ton), 2024 state utility filings ~1,200 (~$45B requested), interregional transmission >$12B (2023–24), US municipal bond issuance >$500B (2024) drive project pipelines and regulatory/compliance risks.

| Metric | Value |

|---|---|

| IIJA funding | ~$550B |

| FY2025 DoD | ~$858B |

| DoD cyber | ~$10B |

| State filings (2024) | ~1,200 / $45B |

| Interregional TX (23–24) | >$12B |

| Municipal bonds (2024) | >$500B |

What is included in the product

Explores how external macro-environmental factors uniquely affect Burns & McDonnell across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify risks and opportunities, support scenario planning, and inform executives, consultants, and investors with ready-to-use insights for reports and funding pitches.

A concise Burns & McDonnell PESTLE summary that’s easy to drop into presentations or strategy packs, enabling quick alignment across teams and supporting risk discussions during planning sessions.

Economic factors

Interest Rate Environment and Capital Costs

By end-2025, the Federal Reserve funds rate near 5.25–5.50% raises capital costs, reducing feasibility for debt-financed industrial projects and prompting some private clients to defer spend; Moody’s estimates a 15–25% slowdown in new infrastructure financings under such rates. A stabilizing or falling rate trend could cut weighted average cost of capital by 100–200 bps, reviving investment appetite. Burns & McDonnell must embed rate scenarios in cost-benefit models and stress-test returns against rate-sensitive discount rates and loan terms.

Inflationary Pressures on Construction Inputs

Fluctuations in labor and raw material costs erode margins on fixed-price contracts; US construction input prices rose 6.1% year-over-year in 2025 Q4, pressuring profitability. Burns & McDonnell uses economic forecasting and scenario modelling—reducing commodity exposure by hedging and forward procurement—to manage volatility. Persistent inflation has led the firm to tighten escalation clauses and expand strategic sourcing, lowering input-cost variability by an estimated 8–12% per project.

Labor Market Dynamics and Skilled Shortages

The scarcity of specialized engineers and skilled trades remains a major headwind for Burns & McDonnell; US Bureau of Labor Statistics data to 2024 show construction and engineering occupations facing 7–9% vacancy growth year-over-year in specialist roles, tightening supply for complex projects.

Competitive wage inflation—average annual pay growth near 5–6% in 2023–24 for engineering and skilled trades—raises overhead and compresses project margins, increasing bid prices and delivery risk.

Investing in employee ownership and internal training is economically necessary: firms reporting ESOPs or robust apprenticeship pipelines saw 10–15% lower turnover and 3–5% higher productivity in recent industry studies, preserving technical capacity for high-complexity projects.

Global Economic Growth and Industrial Demand

Demand for Burns & McDonnell services tracks global GDP and industrial output; world GDP grew 3.1% in 2024 and manufacturing PMI averaged ~50.8, supporting project pipelines in construction and engineering.

Sector downturns hit spending—global air traffic was still ~10% below 2019 levels in 2024 and oil & gas capex fell ~8% YoY in 2024, reducing facility upgrade projects.

Conversely resilient growth fuels logistics and data center demand: hyperscale data center capacity grew ~20% YoY in 2024 and global e-commerce sales rose 10%, driving modernization projects.

- World GDP +3.1% (2024)

- Manufacturing PMI ~50.8 (2024)

- Air traffic -10% vs 2019 (2024)

- Oil & gas capex -8% YoY (2024)

- Hyperscale data center capacity +20% YoY (2024)

- E‑commerce sales +10% (2024)

Energy Market Volatility

The price gap between natural gas ($2.50–4.00/MMBtu in 2024–25) and levelized cost declines for utility-scale solar ($20–30/MWh) shifts utility/industrial capex, directly affecting Burns & McDonnell project mix and margins.

Rapid policy-driven renewables growth—global clean energy investment hit $1.7T in 2023—can pivot workload from fossil projects to grid, storage, and hydrogen engagements.

Continuous monitoring of global markets (oil near $80/bbl in 2025, power price spikes regionally) lets the firm target consulting where capital is flowing.

- Natural gas $2.50–4.00/MMBtu (2024–25)

- Solar LCOE ~$20–30/MWh

- Global clean energy investment $1.7T (2023)

- Oil ≈ $80/bbl (2025)

Higher rates squeeze infra margins; renewables & hyperscale data centers offset fossil cuts

Higher rates (Fed funds ~5.25–5.50% end-2025) raise WACC, slowing infrastructure financing 15–25%; construction input inflation 6.1% YoY (2025 Q4) and wage growth 5–6% compress margins; labor vacancies up 7–9% for specialists; renewables and data centers (hyperscale +20% YoY) offset fossil capex declines (-8% oil & gas 2024).

| Metric | Value |

|---|---|

| Fed funds | 5.25–5.50% |

| Input inflation | 6.1% YoY |

| Wage growth | 5–6% |

| Labor vacancy | 7–9% |

| Hyperscale DC | +20% YoY |

| Oil & gas capex | -8% YoY |

Preview Before You Purchase

Burns & McDonnell PESTLE Analysis

The preview shown here is the exact Burns & McDonnell PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. It contains the complete political, economic, social, technological, legal, and environmental assessment as displayed, with no placeholders or hidden sections. The layout, content, and structure visible here are exactly what you’ll download immediately after buying. What you see is the final, professionally structured file you’ll own upon checkout.