Busey Business Model Canvas

Busey Bank Business Model Canvas: Strategic Blueprint & Ready-to-Use Templates

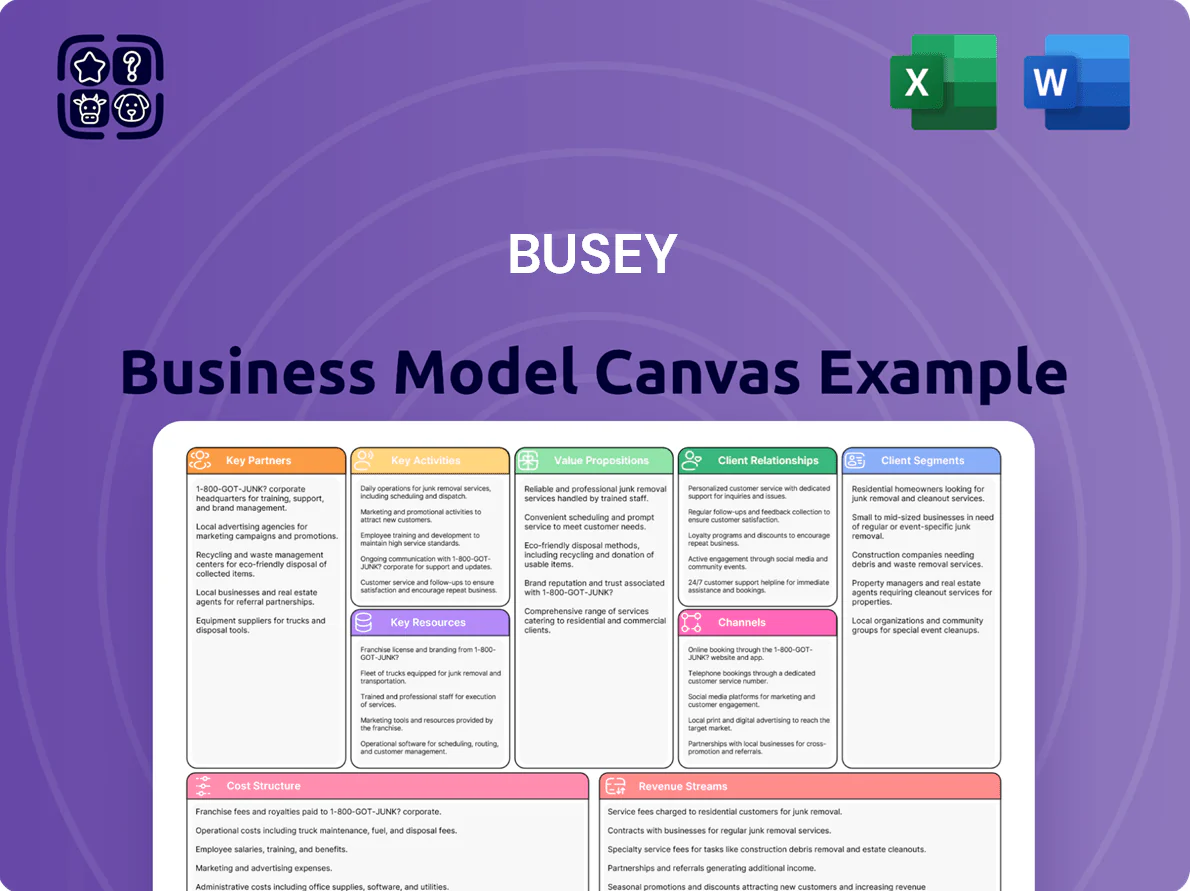

Unlock the full strategic blueprint behind Busey’s business model—this in-depth Business Model Canvas reveals how the bank creates customer value, monetizes services, and sustains competitive advantage; perfect for investors, consultants, and founders seeking actionable insights and ready-to-use templates in Word and Excel.

Partnerships

Fintech and Core System Providers

Busey partners with fintechs and core system providers to run digital banking and processing, cutting development costs while deploying features faster; in 2025 Busey reported ~30% of new digital features delivered via third-party APIs, reducing time-to-market from 12 to 4 months. By using API integrations the bank offers real-time payments and modern security (tokenization, MFA), supporting a 22% year-over-year rise in mobile active users.

Secondary Mortgage Market Entities

Busey sells mortgages to GSEs (Fannie Mae, Freddie Mac) and private investors while often keeping servicing rights, using secondary-market sales to trim interest-rate and credit exposure and free up capital; in 2024 Busey reported about $1.8 billion in loan sales and $3.2 billion MSR (mortgage servicing rights) carrying value across its mortgage footprint.

Payment and Card Networks

Membership in global networks like Visa and Mastercard lets Busey issue debit and credit cards for retail and commercial clients, supporting ~99% merchant acceptance worldwide and processing billions in annual card volume (Busey reported $3.1bn payments volume in 2024). These partnerships enable seamless transaction routing, rewards programs and layered fraud protection (EMV, tokenization, real-time monitoring) that raise deposit-account stickiness and reduce charge-off risk.

Community and Economic Development Organizations

Busey partners with local chambers and nonprofits to drive regional growth, sourcing $420M in community loans and $18.5M in CRA-qualified investments in 2024 to meet regulatory obligations and lend where local demand is highest.

These partnerships boost brand presence and customer loyalty across Illinois and adjacent states, contributing to a 6.2% increase in small-business deposits in core markets in 2024.

- 2024 community loans: $420M

- 2024 CRA investments: $18.5M

- Small-business deposit growth (2024): 6.2%

Third-Party Investment and Insurance Platforms

Busey Wealth Management partners with external asset managers and insurance underwriters to offer expanded investment and risk-management solutions, enabling advisors to provide objective recommendations under an open-architecture model.

In 2024 Busey reported $30.5B in total assets under custody/administration, and these partnerships increased third-party product shelf breadth by ~40%, supporting HNW clients with diversified portfolios and bespoke insurance strategies.

- Open architecture: objective product selection

- Third-party breadth: ~40% more products (2024)

- Assets under custody: $30.5B (2024)

- Targets: HNW clients, bespoke insurance

Busey’s fintech-led push: $30.5B AUC, $3.1B cards, +22% mobile users

Busey leverages fintechs, Visa/Mastercard, GSEs, local nonprofits, and asset managers to speed digital delivery (30% of new features via APIs in 2025), enable $3.1B card volume (2024), $1.8B loan sales (2024), $420M community loans (2024), and $30.5B AUC (2024), driving mobile user growth (+22% YoY) and 6.2% small-business deposit growth (2024).

| Metric | Value |

|---|---|

| New features via APIs (2025) | 30% |

| Card volume (2024) | $3.1B |

| Loan sales (2024) | $1.8B |

| Community loans (2024) | $420M |

| AUC (2024) | $30.5B |

| Mobile active users YoY | +22% |

| Small-business deposit growth (2024) | 6.2% |

What is included in the product

A comprehensive, pre-written business model aligned with Busey’s strategic priorities, covering customer segments, channels, value propositions, revenue streams, key resources, activities, partnerships, cost structure, and metrics with narrative insights and competitive analysis for investor-ready presentations and strategic decision-making.

Condenses Busey’s strategy into a digestible one-page Business Model Canvas, saving hours of formatting while remaining fully editable for team collaboration and quick comparison across scenarios.

Activities

Credit Underwriting and Loan Portfolio Management

Busey performs rigorous credit underwriting—using cash-flow models and collateral stress tests—to keep nonperforming assets low (0.42% NPAs at 2025 Q3) and protect a net interest margin around 3.45% (2024 annual).

Wealth Management and Fiduciary Services

Digital Transformation and Cybersecurity

Busey invests to keep digital banking secure and easy to use, targeting a 15% annual tech spend increase to about $120M in 2025; it automates back‑office processes to cut operational costs 10–20% and deploys multi‑layer cybersecurity—including MFA and zero trust—to reduce fraud losses, which averaged $2.4M annually in regional peers, keeping Busey competitive in a digital‑first market.

Deposit Gathering and Liquidity Management

The bank markets checking, savings and CD products to retail and commercial clients to secure low‑cost funding; Busey reported $17.3 billion in deposits as of 2025 Q3, supporting a loan/deposit ratio near 85%.

Management tracks liquidity coverage and net interest margin, adjusting pricing as rates shift so capital remains available for lending and to protect interest income.

- Deposits: $17.3B (2025 Q3)

- Loan/Deposit ~85%

- Focus: LCR, NIM, funding cost

Regulatory Compliance and Risk Mitigation

As a financial holding company, Busey must continuously meet federal and state banking rules; in 2024 Busey allocated about 2.1% of noninterest expense to compliance and risk functions and completed 18 full internal audits to satisfy Federal Reserve and FDIC standards.

This work—training, reporting, audits—protects the bank charter, avoids fines (industry median enforcement actions fell 12% in 2024) and limits reputational damage.

- 2.1% of noninterest expense to compliance (2024)

- 18 internal audits completed (2024)

- Compliance reduces enforcement risk; industry actions down 12% (2024)

Busey: Tight underwriting, 3.45% NIM, $17.3B deposits and $8.4B AUM

Busey underwrites loans tightly (0.42% NPAs at 2025 Q3) and maintains NIM ~3.45% (2024), while wealth services (AUM $8.4B at 12/31/2024) provide ~22% of noninterest income; deposits $17.3B (2025 Q3) support a ~85% loan/deposit ratio and tech spend targets ~$120M in 2025 to boost automation and security.

| Metric | Value |

|---|---|

| NPAs | 0.42% (2025 Q3) |

| NIM | 3.45% (2024) |

| Deposits | $17.3B (2025 Q3) |

| Loan/Deposit | ~85% |

| AUM | $8.4B (12/31/2024) |

| Wealth income | ~22% noninterest (2024) |

| Tech spend | ~$120M target (2025) |

Delivered as Displayed

Business Model Canvas

The document you're previewing is the actual Busey Business Model Canvas—not a mockup—and it reflects the exact content and layout you will receive after purchase.

When you complete your order, you’ll instantly get this same professional, ready-to-edit file in Word and Excel formats, with all sections and pages included.

No placeholders, no surprises—what you see here is the full deliverable, formatted for presentation, editing, and sharing.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Busey Bank Business Model Canvas: Strategic Blueprint & Ready-to-Use Templates

Unlock the full strategic blueprint behind Busey’s business model—this in-depth Business Model Canvas reveals how the bank creates customer value, monetizes services, and sustains competitive advantage; perfect for investors, consultants, and founders seeking actionable insights and ready-to-use templates in Word and Excel.

Partnerships

Fintech and Core System Providers

Busey partners with fintechs and core system providers to run digital banking and processing, cutting development costs while deploying features faster; in 2025 Busey reported ~30% of new digital features delivered via third-party APIs, reducing time-to-market from 12 to 4 months. By using API integrations the bank offers real-time payments and modern security (tokenization, MFA), supporting a 22% year-over-year rise in mobile active users.

Secondary Mortgage Market Entities

Busey sells mortgages to GSEs (Fannie Mae, Freddie Mac) and private investors while often keeping servicing rights, using secondary-market sales to trim interest-rate and credit exposure and free up capital; in 2024 Busey reported about $1.8 billion in loan sales and $3.2 billion MSR (mortgage servicing rights) carrying value across its mortgage footprint.

Payment and Card Networks

Membership in global networks like Visa and Mastercard lets Busey issue debit and credit cards for retail and commercial clients, supporting ~99% merchant acceptance worldwide and processing billions in annual card volume (Busey reported $3.1bn payments volume in 2024). These partnerships enable seamless transaction routing, rewards programs and layered fraud protection (EMV, tokenization, real-time monitoring) that raise deposit-account stickiness and reduce charge-off risk.

Community and Economic Development Organizations

Busey partners with local chambers and nonprofits to drive regional growth, sourcing $420M in community loans and $18.5M in CRA-qualified investments in 2024 to meet regulatory obligations and lend where local demand is highest.

These partnerships boost brand presence and customer loyalty across Illinois and adjacent states, contributing to a 6.2% increase in small-business deposits in core markets in 2024.

- 2024 community loans: $420M

- 2024 CRA investments: $18.5M

- Small-business deposit growth (2024): 6.2%

Third-Party Investment and Insurance Platforms

Busey Wealth Management partners with external asset managers and insurance underwriters to offer expanded investment and risk-management solutions, enabling advisors to provide objective recommendations under an open-architecture model.

In 2024 Busey reported $30.5B in total assets under custody/administration, and these partnerships increased third-party product shelf breadth by ~40%, supporting HNW clients with diversified portfolios and bespoke insurance strategies.

- Open architecture: objective product selection

- Third-party breadth: ~40% more products (2024)

- Assets under custody: $30.5B (2024)

- Targets: HNW clients, bespoke insurance

Busey’s fintech-led push: $30.5B AUC, $3.1B cards, +22% mobile users

Busey leverages fintechs, Visa/Mastercard, GSEs, local nonprofits, and asset managers to speed digital delivery (30% of new features via APIs in 2025), enable $3.1B card volume (2024), $1.8B loan sales (2024), $420M community loans (2024), and $30.5B AUC (2024), driving mobile user growth (+22% YoY) and 6.2% small-business deposit growth (2024).

| Metric | Value |

|---|---|

| New features via APIs (2025) | 30% |

| Card volume (2024) | $3.1B |

| Loan sales (2024) | $1.8B |

| Community loans (2024) | $420M |

| AUC (2024) | $30.5B |

| Mobile active users YoY | +22% |

| Small-business deposit growth (2024) | 6.2% |

What is included in the product

A comprehensive, pre-written business model aligned with Busey’s strategic priorities, covering customer segments, channels, value propositions, revenue streams, key resources, activities, partnerships, cost structure, and metrics with narrative insights and competitive analysis for investor-ready presentations and strategic decision-making.

Condenses Busey’s strategy into a digestible one-page Business Model Canvas, saving hours of formatting while remaining fully editable for team collaboration and quick comparison across scenarios.

Activities

Credit Underwriting and Loan Portfolio Management

Busey performs rigorous credit underwriting—using cash-flow models and collateral stress tests—to keep nonperforming assets low (0.42% NPAs at 2025 Q3) and protect a net interest margin around 3.45% (2024 annual).

Wealth Management and Fiduciary Services

Digital Transformation and Cybersecurity

Busey invests to keep digital banking secure and easy to use, targeting a 15% annual tech spend increase to about $120M in 2025; it automates back‑office processes to cut operational costs 10–20% and deploys multi‑layer cybersecurity—including MFA and zero trust—to reduce fraud losses, which averaged $2.4M annually in regional peers, keeping Busey competitive in a digital‑first market.

Deposit Gathering and Liquidity Management

The bank markets checking, savings and CD products to retail and commercial clients to secure low‑cost funding; Busey reported $17.3 billion in deposits as of 2025 Q3, supporting a loan/deposit ratio near 85%.

Management tracks liquidity coverage and net interest margin, adjusting pricing as rates shift so capital remains available for lending and to protect interest income.

- Deposits: $17.3B (2025 Q3)

- Loan/Deposit ~85%

- Focus: LCR, NIM, funding cost

Regulatory Compliance and Risk Mitigation

As a financial holding company, Busey must continuously meet federal and state banking rules; in 2024 Busey allocated about 2.1% of noninterest expense to compliance and risk functions and completed 18 full internal audits to satisfy Federal Reserve and FDIC standards.

This work—training, reporting, audits—protects the bank charter, avoids fines (industry median enforcement actions fell 12% in 2024) and limits reputational damage.

- 2.1% of noninterest expense to compliance (2024)

- 18 internal audits completed (2024)

- Compliance reduces enforcement risk; industry actions down 12% (2024)

Busey: Tight underwriting, 3.45% NIM, $17.3B deposits and $8.4B AUM

Busey underwrites loans tightly (0.42% NPAs at 2025 Q3) and maintains NIM ~3.45% (2024), while wealth services (AUM $8.4B at 12/31/2024) provide ~22% of noninterest income; deposits $17.3B (2025 Q3) support a ~85% loan/deposit ratio and tech spend targets ~$120M in 2025 to boost automation and security.

| Metric | Value |

|---|---|

| NPAs | 0.42% (2025 Q3) |

| NIM | 3.45% (2024) |

| Deposits | $17.3B (2025 Q3) |

| Loan/Deposit | ~85% |

| AUM | $8.4B (12/31/2024) |

| Wealth income | ~22% noninterest (2024) |

| Tech spend | ~$120M target (2025) |

Delivered as Displayed

Business Model Canvas

The document you're previewing is the actual Busey Business Model Canvas—not a mockup—and it reflects the exact content and layout you will receive after purchase.

When you complete your order, you’ll instantly get this same professional, ready-to-edit file in Word and Excel formats, with all sections and pages included.

No placeholders, no surprises—what you see here is the full deliverable, formatted for presentation, editing, and sharing.