Busey Porter's Five Forces Analysis

Don't Miss the Bigger Picture

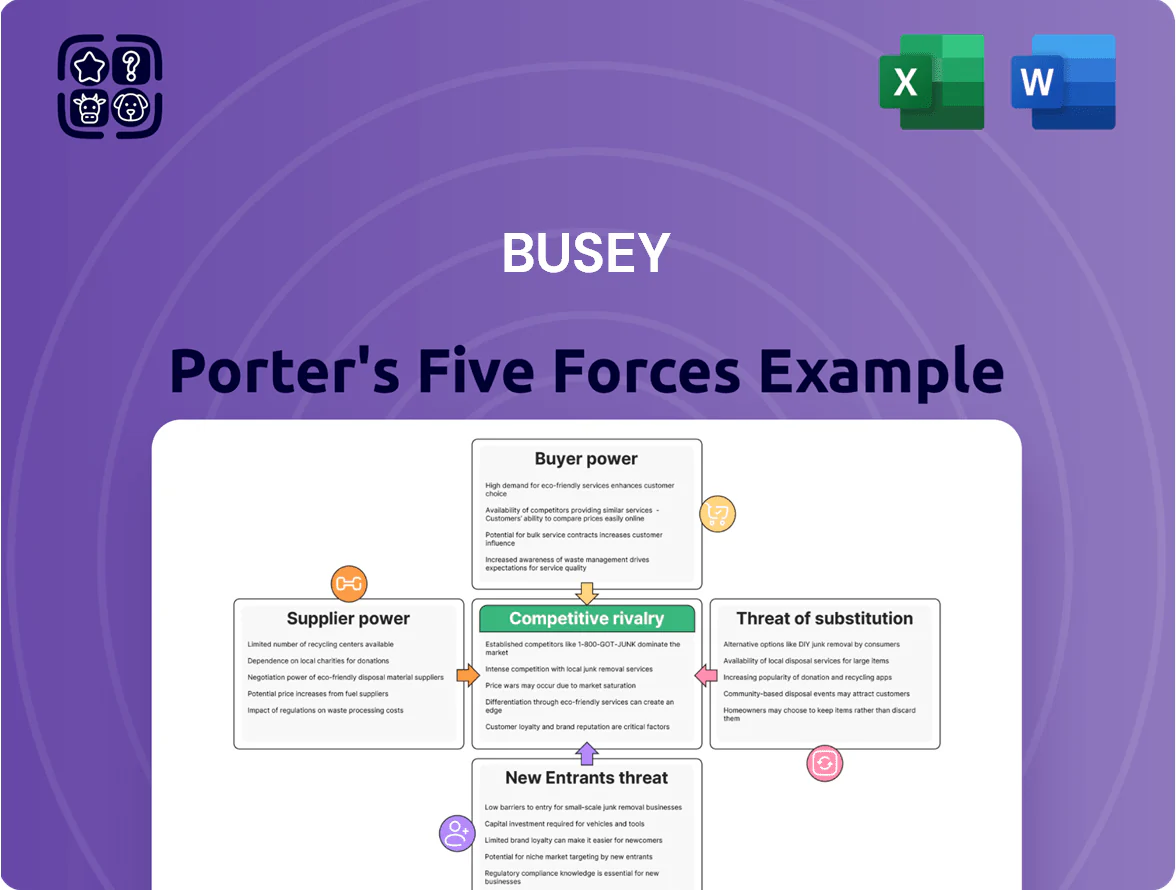

Busey’s Porter's Five Forces snapshot highlights competitive intensity across banking, from regional rivalry to regulatory-driven barriers and evolving fintech substitutes, revealing where margins and growth face pressure.

This brief overview surfaces key supplier, buyer, and entrant dynamics but only scratches the surface of strategic implications and quantified ratings.

Ready for a full, consultant-grade Porter's Five Forces Analysis with visuals, force-by-force scores, and actionable takeaways to inform investment or strategy? Unlock the complete report now.

Suppliers Bargaining Power

Concentration of Core Banking Technology Vendors

The banking sector depends on a handful of core processing and digital-infrastructure vendors, with the top 5 providers serving over 70% of US regional banks as of 2025; this concentration gives suppliers pricing power versus banks like Busey Financial (Busey). Switching costs are high—projects often exceed $20m and take 12–36 months—raising operational disruption risk and data-migration complexity. As a result, vendors secure favorable terms and can drive price increases or limit customization during renewals and upgrade negotiations.

Competition for Specialized Financial Talent

The Midwest and Florida face tight supply of experienced wealth managers, commercial lenders and cybersecurity experts; Bureau of Labor Statistics data (2024) shows regional shortages with open-to-hire ratios 1.2x above national average in financial services, and cybersecurity roles growing 35% since 2020. National banks expanding locally bid up pay—average senior wealth manager total comp rose to ~$250k in 2024—so Busey must match market wages and enhance benefits to retain its high-touch model.

Access to Wholesale Funding Markets

Busey Bank uses Federal Home Loan Bank advances and brokered deposits to manage liquidity and interest-rate risk; at year-end 2024 wholesale funding made up about 18% of funded liabilities, per 2024 10-K.

Cost and availability track Fed policy and market rates; the 2024 average cost of brokered deposits rose ~120 basis points vs 2022, tightening margins.

When markets swing, institutional lenders can push funding prices higher, compressing Busey’s net interest margin—NIM fell to 3.05% in 2024, showing this pressure.

Regulatory and Compliance Service Requirements

Regulatory bodies function as mandatory suppliers of licenses and legal frameworks for Busey Porter, giving them unilateral power over operations and market access.

Rising AML and consumer-protection complexity drove US bank compliance costs to $50–70 billion industry-wide in 2023; Busey Porter must buy third-party audits and legal advice to avoid fines.

Specialized auditors and legal consultancies hold leverage because their expertise is non-negotiable to maintain regulatory standing and prevent costly penalties.

- Regulators = mandatory suppliers of licenses

- 2023 US bank compliance spend ≈ $50–70B

- Third-party audits/legal advice required

- Specialists hold high bargaining power

Dynamics of the Deposit Base as a Capital Source

Depositors act as Busey Bank’s primary capital suppliers; in 2025 Busey held $22.4 billion in deposits, so shifts in depositor behavior directly affect lending capacity.

Higher market rates raise depositor bargaining power as savers chase yield; between 2022–2024 Busey’s average cost of funds rose from ~0.50% to ~1.75%, squeezing net interest margin.

Busey must protect low-cost core deposits while competing with money-market funds and high-yield online accounts that can quickly pull sophisticated balances.

- Deposits: $22.4B (2025)

- Cost of funds: ~0.50% (2022) → ~1.75% (2024)

- Risk: core outflows to high-yield alternatives

- Action: price selectively, deepen relationship deposits

High supplier power threatens Busey: concentrated vendors, costly switches, tight talent

Suppliers (core processors, talent, wholesale funders, regulators, auditors) hold high bargaining power vs Busey due to vendor concentration (top-5 vendors >70% of regional banks, 2025), high switching costs ($20m+, 12–36 months), regional talent shortages (open-to-hire 1.2x US avg, BLS 2024) and funding cost volatility (cost of funds ~0.50%→1.75%, 2022–24).

| Supplier | Key metric | 2024–25 |

|---|---|---|

| Core vendors | Market share (top 5) | >70% |

| Switch cost | Project size / timeline | $20m+, 12–36m |

| Talent | Open-to-hire vs US | 1.2x (BLS 2024) |

| Deposits | Balance | $22.4B (2025) |

| Funding cost | Cost of funds | ~0.50%→~1.75% |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to Busey, highlighting supplier/buyer power, substitutes, new entrant threats, and rivalry to inform pricing and strategic positioning.

A concise, one-sheet Busey Porter's Five Forces summary that highlights competitive pressures and actionable levers—ideal for rapid decision-making and slide-ready presentation.

Customers Bargaining Power

Low Switching Costs for Retail Banking Clients

Individual consumers face minimal financial penalty moving checking/savings accounts; 2024 U.S. deposit-switching surveys show ~28% of retail customers considered switching in 12 months and 14% actually moved accounts, so churn risk is tangible.

Digital onboarding cut account-opening time to 5–10 minutes at many neobanks; fintechs captured ~12% of new deposit flows in 2023, forcing faster digital upgrades.

As a result, Busey must spend on CX and loyalty: industry median spending on digital customer acquisition rose to 1.8% of deposits in 2024, else retention rates drop.

High Price Sensitivity in Commercial Lending

Business clients routinely solicit bids from multiple banks for CRE and equipment loans, treating loans as commodities—88% of mid-market firms sought multiple lender bids in 2024—so customers can push for lower spreads and looser covenants. Busey’s pricing power weakens unless it offsets rate pressure with relationship-based service, sector-specific expertise, and faster decision times; deals won by relationship factors rose 22% at regional banks in 2024.

Sophistication of Wealth Management Clients

The high-net-worth clients in Busey’s wealth management are well informed and compare returns and fees; as of 2024 UHNW/HNW investors shifted 18% of assets to lower-fee providers, per Cerulli Associates. These clients routinely benchmark performance vs. national brokers and RIAs and can move multi-million-dollar portfolios, giving them leverage to demand bespoke service, fee transparency, and negotiated pricing.

Information Symmetry via Digital Comparison Tools

Online aggregators let customers compare mortgage rates and deposit yields across hundreds of banks instantly, with platforms like Bankrate and LendingTree showing median 30-year mortgage spreads within 0.2–0.4 percentage points as of Dec 2025; this transparency erodes local banks’ info advantage.

Customers enter negotiations armed with real-time quotes and rate alerts, limiting Busey’s pricing flexibility and raising price competition.

Demand for Integrated Digital and Physical Channels

Modern banking customers expect a seamless omnichannel experience combining strong mobile apps with branch access; J.D. Power 2024 found 68% of US customers value digital-plus-branch options when choosing a bank.

If Busey lags in digital features, customers can switch fast—Chime, Ally, and regional rivals raised deposit share by 2.1% nationally in 2023–24, pressuring Busey to innovate.

Busey must keep investing in mobile UX, APIs, and branch-digital integration to protect its market share; digital deposits grew 14% YoY in community banks in 2024, so slow adopters lose ground.

- 68% value digital+branch (J.D. Power 2024)

- Digital deposits +14% YoY (community banks, 2024)

- Competitors gained +2.1% deposit share (2023–24)

Customers Drive Banking Shifts: High Churn, Fintech Gains, Demand for Digital+Branch

Customers have strong bargaining power: 2024 surveys show 14% retail deposit churn and 28% considered switching; fintechs took ~12% new deposits in 2023; 68% value digital+branch (J.D. Power 2024); HNW shifted 18% assets to lower-fee providers (2024).

| Metric | Value |

|---|---|

| Retail churn (12m) | 14% |

| Consider switching | 28% |

| Fintech new deposits | 12% |

| Digital+branch importance | 68% |

| HNW asset shift | 18% |

What You See Is What You Get

Busey Porter's Five Forces Analysis

This preview shows the exact Busey Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders, no edits needed.

The document displayed here is the actual, fully formatted analysis file—ready to download and use the moment you buy.

No mockups or samples: what you see is the complete deliverable you'll get instantly after payment.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

Busey’s Porter's Five Forces snapshot highlights competitive intensity across banking, from regional rivalry to regulatory-driven barriers and evolving fintech substitutes, revealing where margins and growth face pressure.

This brief overview surfaces key supplier, buyer, and entrant dynamics but only scratches the surface of strategic implications and quantified ratings.

Ready for a full, consultant-grade Porter's Five Forces Analysis with visuals, force-by-force scores, and actionable takeaways to inform investment or strategy? Unlock the complete report now.

Suppliers Bargaining Power

Concentration of Core Banking Technology Vendors

The banking sector depends on a handful of core processing and digital-infrastructure vendors, with the top 5 providers serving over 70% of US regional banks as of 2025; this concentration gives suppliers pricing power versus banks like Busey Financial (Busey). Switching costs are high—projects often exceed $20m and take 12–36 months—raising operational disruption risk and data-migration complexity. As a result, vendors secure favorable terms and can drive price increases or limit customization during renewals and upgrade negotiations.

Competition for Specialized Financial Talent

The Midwest and Florida face tight supply of experienced wealth managers, commercial lenders and cybersecurity experts; Bureau of Labor Statistics data (2024) shows regional shortages with open-to-hire ratios 1.2x above national average in financial services, and cybersecurity roles growing 35% since 2020. National banks expanding locally bid up pay—average senior wealth manager total comp rose to ~$250k in 2024—so Busey must match market wages and enhance benefits to retain its high-touch model.

Access to Wholesale Funding Markets

Busey Bank uses Federal Home Loan Bank advances and brokered deposits to manage liquidity and interest-rate risk; at year-end 2024 wholesale funding made up about 18% of funded liabilities, per 2024 10-K.

Cost and availability track Fed policy and market rates; the 2024 average cost of brokered deposits rose ~120 basis points vs 2022, tightening margins.

When markets swing, institutional lenders can push funding prices higher, compressing Busey’s net interest margin—NIM fell to 3.05% in 2024, showing this pressure.

Regulatory and Compliance Service Requirements

Regulatory bodies function as mandatory suppliers of licenses and legal frameworks for Busey Porter, giving them unilateral power over operations and market access.

Rising AML and consumer-protection complexity drove US bank compliance costs to $50–70 billion industry-wide in 2023; Busey Porter must buy third-party audits and legal advice to avoid fines.

Specialized auditors and legal consultancies hold leverage because their expertise is non-negotiable to maintain regulatory standing and prevent costly penalties.

- Regulators = mandatory suppliers of licenses

- 2023 US bank compliance spend ≈ $50–70B

- Third-party audits/legal advice required

- Specialists hold high bargaining power

Dynamics of the Deposit Base as a Capital Source

Depositors act as Busey Bank’s primary capital suppliers; in 2025 Busey held $22.4 billion in deposits, so shifts in depositor behavior directly affect lending capacity.

Higher market rates raise depositor bargaining power as savers chase yield; between 2022–2024 Busey’s average cost of funds rose from ~0.50% to ~1.75%, squeezing net interest margin.

Busey must protect low-cost core deposits while competing with money-market funds and high-yield online accounts that can quickly pull sophisticated balances.

- Deposits: $22.4B (2025)

- Cost of funds: ~0.50% (2022) → ~1.75% (2024)

- Risk: core outflows to high-yield alternatives

- Action: price selectively, deepen relationship deposits

High supplier power threatens Busey: concentrated vendors, costly switches, tight talent

Suppliers (core processors, talent, wholesale funders, regulators, auditors) hold high bargaining power vs Busey due to vendor concentration (top-5 vendors >70% of regional banks, 2025), high switching costs ($20m+, 12–36 months), regional talent shortages (open-to-hire 1.2x US avg, BLS 2024) and funding cost volatility (cost of funds ~0.50%→1.75%, 2022–24).

| Supplier | Key metric | 2024–25 |

|---|---|---|

| Core vendors | Market share (top 5) | >70% |

| Switch cost | Project size / timeline | $20m+, 12–36m |

| Talent | Open-to-hire vs US | 1.2x (BLS 2024) |

| Deposits | Balance | $22.4B (2025) |

| Funding cost | Cost of funds | ~0.50%→~1.75% |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to Busey, highlighting supplier/buyer power, substitutes, new entrant threats, and rivalry to inform pricing and strategic positioning.

A concise, one-sheet Busey Porter's Five Forces summary that highlights competitive pressures and actionable levers—ideal for rapid decision-making and slide-ready presentation.

Customers Bargaining Power

Low Switching Costs for Retail Banking Clients

Individual consumers face minimal financial penalty moving checking/savings accounts; 2024 U.S. deposit-switching surveys show ~28% of retail customers considered switching in 12 months and 14% actually moved accounts, so churn risk is tangible.

Digital onboarding cut account-opening time to 5–10 minutes at many neobanks; fintechs captured ~12% of new deposit flows in 2023, forcing faster digital upgrades.

As a result, Busey must spend on CX and loyalty: industry median spending on digital customer acquisition rose to 1.8% of deposits in 2024, else retention rates drop.

High Price Sensitivity in Commercial Lending

Business clients routinely solicit bids from multiple banks for CRE and equipment loans, treating loans as commodities—88% of mid-market firms sought multiple lender bids in 2024—so customers can push for lower spreads and looser covenants. Busey’s pricing power weakens unless it offsets rate pressure with relationship-based service, sector-specific expertise, and faster decision times; deals won by relationship factors rose 22% at regional banks in 2024.

Sophistication of Wealth Management Clients

The high-net-worth clients in Busey’s wealth management are well informed and compare returns and fees; as of 2024 UHNW/HNW investors shifted 18% of assets to lower-fee providers, per Cerulli Associates. These clients routinely benchmark performance vs. national brokers and RIAs and can move multi-million-dollar portfolios, giving them leverage to demand bespoke service, fee transparency, and negotiated pricing.

Information Symmetry via Digital Comparison Tools

Online aggregators let customers compare mortgage rates and deposit yields across hundreds of banks instantly, with platforms like Bankrate and LendingTree showing median 30-year mortgage spreads within 0.2–0.4 percentage points as of Dec 2025; this transparency erodes local banks’ info advantage.

Customers enter negotiations armed with real-time quotes and rate alerts, limiting Busey’s pricing flexibility and raising price competition.

Demand for Integrated Digital and Physical Channels

Modern banking customers expect a seamless omnichannel experience combining strong mobile apps with branch access; J.D. Power 2024 found 68% of US customers value digital-plus-branch options when choosing a bank.

If Busey lags in digital features, customers can switch fast—Chime, Ally, and regional rivals raised deposit share by 2.1% nationally in 2023–24, pressuring Busey to innovate.

Busey must keep investing in mobile UX, APIs, and branch-digital integration to protect its market share; digital deposits grew 14% YoY in community banks in 2024, so slow adopters lose ground.

- 68% value digital+branch (J.D. Power 2024)

- Digital deposits +14% YoY (community banks, 2024)

- Competitors gained +2.1% deposit share (2023–24)

Customers Drive Banking Shifts: High Churn, Fintech Gains, Demand for Digital+Branch

Customers have strong bargaining power: 2024 surveys show 14% retail deposit churn and 28% considered switching; fintechs took ~12% new deposits in 2023; 68% value digital+branch (J.D. Power 2024); HNW shifted 18% assets to lower-fee providers (2024).

| Metric | Value |

|---|---|

| Retail churn (12m) | 14% |

| Consider switching | 28% |

| Fintech new deposits | 12% |

| Digital+branch importance | 68% |

| HNW asset shift | 18% |

What You See Is What You Get

Busey Porter's Five Forces Analysis

This preview shows the exact Busey Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders, no edits needed.

The document displayed here is the actual, fully formatted analysis file—ready to download and use the moment you buy.

No mockups or samples: what you see is the complete deliverable you'll get instantly after payment.