Buzzi Unicem Boston Consulting Group Matrix

Actionable Strategy Starts Here

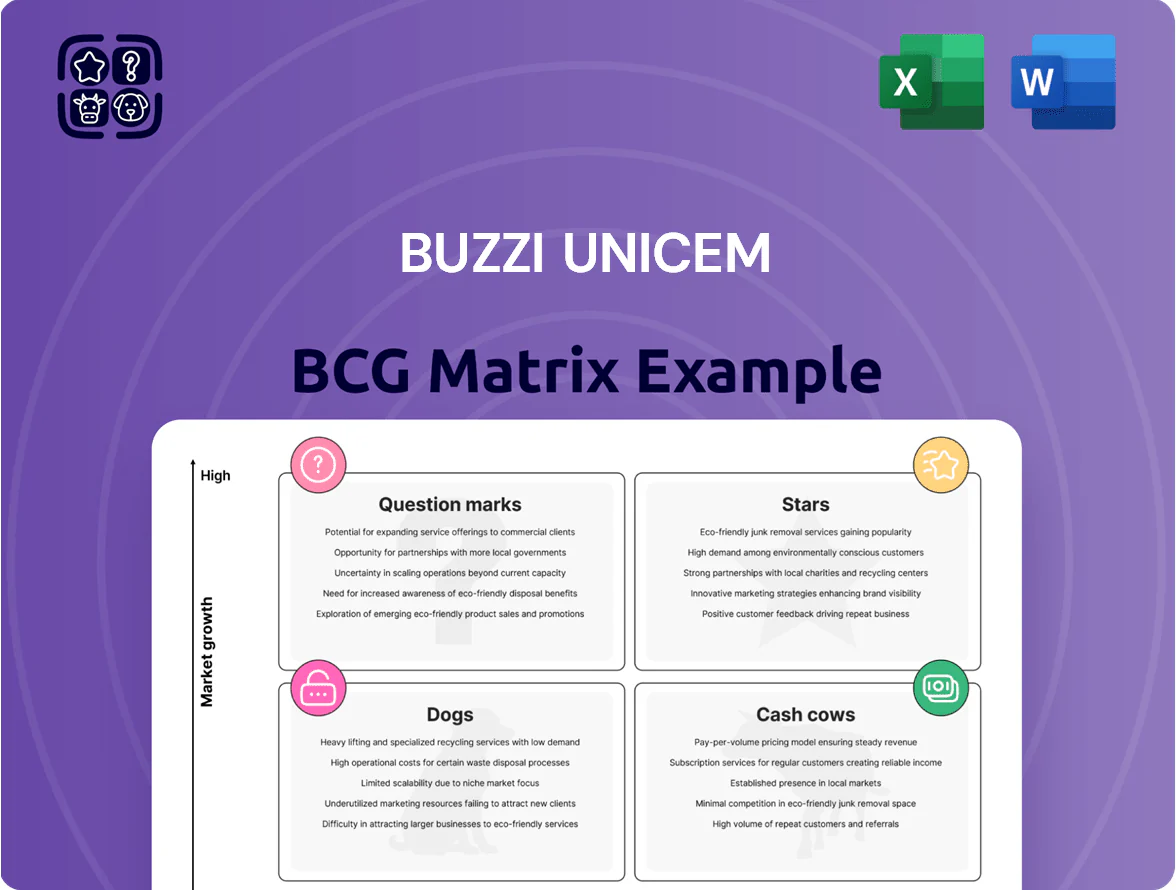

Buzzi Unicem’s BCG Matrix preview highlights how its cement and building-materials businesses likely map across Stars, Cash Cows, Question Marks, and Dogs amid shifting construction demand and regional growth dynamics. This snapshot signals where cash generation, reinvestment, or divestment may be needed to optimize portfolio performance. Dive deeper into the full BCG Matrix for quadrant-by-quadrant data, actionable strategies, and a ready-to-use Word + Excel package to guide smart capital allocation and operational decisions—purchase now for instant access.

Stars

Low-Carbon Cement Solutions

Buzzi Unicem’s CGreen low-clinker cements sit in the Stars quadrant—market growth >15% CAGR and the company holding ~20–25% share in sustainable binders by 2025, driven by EU Fit for 55 and US state rules tightening by end-2025.

R&D spend rose to €45m in 2024 (up 30% YoY) to improve clinker substitution and scale demo plants; capex of €150–200m is planned 2025–2027 to expand low-carbon capacity and meet surging demand.

United States Infrastructure Projects

United States Infrastructure Projects sits as a Star in Buzzi Unicem’s BCG matrix: the unit held about 30–35% market share in key regions in 2025, driven by $1.2 trillion federal infrastructure funding (IIJA/2021 carryover) and 6–8% annual cement demand growth for highways and bridges.

Revenue exceeded €520 million in 2024, but capital expenditures of ~€110–130 million planned for 2025–26 for plant upgrades and logistics expansion keep free cash flow tight.

High growth and strategic importance mean Buzzi must keep investing to secure margin gains and capture the multi-year North American construction boom.

Mexican Market Joint Ventures

Operating via its strategic stake in Corporación Moctezuma, Buzzi Unicem commands a leading market share in Mexico, where cement consumption rose 4.5% in 2025 year-on-year versus OECD average near 1.2%—fueling above-market revenue growth for the segment.

The region accounts for roughly 18% of group volumes in 2025 and drives geographic diversification, offsetting slower European demand.

High share gives pricing leverage but requires steady capex—management signaled MXN 1.2bn (≈€63m) reinvestment for 2026 to expand clinker and grinding capacity.

Digitalized Concrete Logistics

Digitalized Concrete Logistics is a Star: Buzzi Unicem’s use of telematics and AI dispatching has driven rapid share gains in tech-enabled deliveries, capturing an estimated 18–22% of Europe’s smart ready-mix market by 2024 and winning large commercial developers focused on time and cost savings.

The unit needs steady capex for sensors, fleet connectivity, and ML models—roughly €10–15m annually—to fend off rivals; digital construction services grew ~28% CAGR 2021–2024, keeping this a high-growth, high-investment performer.

- Market share 18–22% (2024)

- Digital services CAGR ~28% (2021–24)

- Annual digital capex €10–15m

- Target: large commercial developers

Advanced Pozzolanic Cements

Advanced Pozzolanic Cements: demand for specialty cements for marine and extreme environments grew ~7–9% CAGR globally 2020–2024, outpacing standard cement; Buzzi Unicem holds a leading share in technical formulations, supplying >10% of European specialty volumes in 2024 and showing higher margin mix.

Protecting this lead needs continued capex: Buzzi spent ~€45–60m/year on R&D and specialty plants in 2023–2024; technical service teams reduce project failures and support climate-resilient infrastructure wins.

- Market CAGR ~8% (2020–24)

- Buzzi >10% share Europe (2024)

- Higher margins vs standard cement

- Capex €45–60m/yr (2023–24)

- Requires skilled technical teams

High‑growth Stars: CGreen, Digital Logistics, US Infra & Mexico drive €520m revenue surge

Stars: CGreen, US infrastructure, Mexico, Digital Logistics, and Advanced Pozzolanic cements — high growth (>7–15% CAGR), 2024–25 shares 18–35%, 2024 revenue €520m for Stars, R&D €45m (2024), group capex planned €150–200m (2025–27); steady annual digital capex €10–15m and MX reinvestment MXN1.2bn (€63m) for 2026.

| Unit | Growth CAGR | Share (2024/25) | 2024–25 spend |

|---|---|---|---|

| CGreen | 15%+ | 20–25% | R&D €45m |

| US Infra | 6–8% | 30–35% | Capex €110–130m (2025–26) |

| Mexico | 4.5% (2025) | ~18% volumes | MXN1.2bn (€63m) 2026 |

| Digital | 28% (2021–24) | 18–22% | €10–15m/yr |

| Pozzolanic | 8% | >10% | €45–60m/yr |

What is included in the product

Comprehensive BCG Matrix review of Buzzi Unicem’s units with strategic moves—invest, hold, or divest—plus risks and market trend context.

One-page BCG matrix placing Buzzi Unicem units in quadrants for quick strategic decisions and C-level presentations.

Cash Cows

Italian Domestic Cement Operations

Italy remains a mature market where Buzzi Unicem holds a commanding ~25% national cement market share (2024) and stable pricing; growth in construction was just 0.8% in 2024, so volume rises are limited. These domestic operations produced roughly €420m EBITDA in FY2024, delivering consistent, significant cash flow. Existing plants need minimal capex—maintenance capex ~€60m in 2024 versus revenues of €1.9bn—so free cash funds greener tech and expansion.

Central European Aggregates

Central European Aggregates (sand, gravel, crushed stone) in Germany and neighboring regions is a high-market-share, low-growth cash cow for Buzzi Unicem, with market growth around 1%–2% annually and estimated regional volumes ~120–150 Mt/year in 2024.

High barriers—strict permits, limited quarry sites—and optimized logistics yield EBITDA margins near 25%–30% for mature operators; Buzzi’s units benefit from multi-decade permits and rail/truck networks.

Annual cash generation (estimated €200–€350m free cash flow run-rate in 2024 for the segment) is key to servicing corporate net debt (~€1.2–€1.5bn group-level at end-2024) and maintaining dividend payouts to shareholders.

Standard Ready-Mix Concrete in USA

In established U.S. urban centers, Buzzi Unicem’s standard ready‑mix concrete yields steady cash, with estimated 2024 revenues around $850–900M from North American ops and market share north of 15% in key metros, while national demand growth for basic concrete has stabilized near 1–2% annually.

Brand recognition and high utilization let the unit run with maintenance capex (~2–3% of revenues), freeing operating cash flow to fund higher‑growth projects and acquisitions.

Luxembourg Specialty Binder Market

Buzzi Unicem runs a highly efficient, dominant specialty binder operation in Luxembourg, delivering ~18–22% EBITDA margins in 2024 on annual revenues of roughly €40–45m thanks to niche demand and long-term local contracts.

Country size caps growth to ~1–2% annually, but weak competition and low capex needs keep free cash flow high, making this a textbook cash cow requiring minimal reinvestment.

- 2024 revenue ~€40–45m

- EBITDA margin 18–22% (2024)

- Growth 1–2%/yr

- Low capex, high FCF

Traditional Portland Cement Production

Traditional Portland cement production remains Buzzi Unicem's highest-volume activity across Italy, US and Central Europe, accounting for roughly 55–60% of clinker throughput in 2024 and anchoring group revenue—about €2.1–2.3bn of sales from building materials in 2024.

Even as green cements grow, the traditional market is mature and stable; Buzzi’s ~20–30% regional market shares plus plant-scale efficiencies keep unit costs low and EBITDA margins above peer averages (2024 EBITDA margin ~18%).

The unit leverages existing assets to extract cash while the sector shifts to lower-carbon standards, with capex for decarbonization staged—only ~€150–200m allocated 2024–2025—so traditional lines still milk returns.

- High volume: 55–60% clinker throughput (2024)

- Revenue tied: ~€2.1–2.3bn from building materials (2024)

- Market share: ~20–30% regionally

- EBITDA margin: ~18% (2024)

- Decarbonization capex: ~€150–200m (2024–25)

High‑margin cash cows (€450–700m FCF) underpin €1.2–1.5bn net debt and dividends

Cash cows: Italy cement, Central European aggregates, US ready‑mix, Luxembourg specialty binders—stable volumes (0.8–2% growth), high margins (EBITDA 18–30% in 2024), low maintenance capex (2–3% revenues), estimated FCF contribution €450–700m in 2024, supports group net debt €1.2–1.5bn and dividends.

| Segment | 2024 rev | EBITDA% | FCF |

|---|---|---|---|

| Italy | €1.9bn | ~22% | €420m |

| Aggregates CE | — | 25–30% | €200–350m |

What You’re Viewing Is Included

Buzzi Unicem BCG Matrix

The file you're previewing is the exact Buzzi Unicem BCG Matrix you'll receive after purchase—no watermarks, no placeholders—just a fully formatted, market-informed strategic matrix ready for presentation or analysis.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Actionable Strategy Starts Here

Buzzi Unicem’s BCG Matrix preview highlights how its cement and building-materials businesses likely map across Stars, Cash Cows, Question Marks, and Dogs amid shifting construction demand and regional growth dynamics. This snapshot signals where cash generation, reinvestment, or divestment may be needed to optimize portfolio performance. Dive deeper into the full BCG Matrix for quadrant-by-quadrant data, actionable strategies, and a ready-to-use Word + Excel package to guide smart capital allocation and operational decisions—purchase now for instant access.

Stars

Low-Carbon Cement Solutions

Buzzi Unicem’s CGreen low-clinker cements sit in the Stars quadrant—market growth >15% CAGR and the company holding ~20–25% share in sustainable binders by 2025, driven by EU Fit for 55 and US state rules tightening by end-2025.

R&D spend rose to €45m in 2024 (up 30% YoY) to improve clinker substitution and scale demo plants; capex of €150–200m is planned 2025–2027 to expand low-carbon capacity and meet surging demand.

United States Infrastructure Projects

United States Infrastructure Projects sits as a Star in Buzzi Unicem’s BCG matrix: the unit held about 30–35% market share in key regions in 2025, driven by $1.2 trillion federal infrastructure funding (IIJA/2021 carryover) and 6–8% annual cement demand growth for highways and bridges.

Revenue exceeded €520 million in 2024, but capital expenditures of ~€110–130 million planned for 2025–26 for plant upgrades and logistics expansion keep free cash flow tight.

High growth and strategic importance mean Buzzi must keep investing to secure margin gains and capture the multi-year North American construction boom.

Mexican Market Joint Ventures

Operating via its strategic stake in Corporación Moctezuma, Buzzi Unicem commands a leading market share in Mexico, where cement consumption rose 4.5% in 2025 year-on-year versus OECD average near 1.2%—fueling above-market revenue growth for the segment.

The region accounts for roughly 18% of group volumes in 2025 and drives geographic diversification, offsetting slower European demand.

High share gives pricing leverage but requires steady capex—management signaled MXN 1.2bn (≈€63m) reinvestment for 2026 to expand clinker and grinding capacity.

Digitalized Concrete Logistics

Digitalized Concrete Logistics is a Star: Buzzi Unicem’s use of telematics and AI dispatching has driven rapid share gains in tech-enabled deliveries, capturing an estimated 18–22% of Europe’s smart ready-mix market by 2024 and winning large commercial developers focused on time and cost savings.

The unit needs steady capex for sensors, fleet connectivity, and ML models—roughly €10–15m annually—to fend off rivals; digital construction services grew ~28% CAGR 2021–2024, keeping this a high-growth, high-investment performer.

- Market share 18–22% (2024)

- Digital services CAGR ~28% (2021–24)

- Annual digital capex €10–15m

- Target: large commercial developers

Advanced Pozzolanic Cements

Advanced Pozzolanic Cements: demand for specialty cements for marine and extreme environments grew ~7–9% CAGR globally 2020–2024, outpacing standard cement; Buzzi Unicem holds a leading share in technical formulations, supplying >10% of European specialty volumes in 2024 and showing higher margin mix.

Protecting this lead needs continued capex: Buzzi spent ~€45–60m/year on R&D and specialty plants in 2023–2024; technical service teams reduce project failures and support climate-resilient infrastructure wins.

- Market CAGR ~8% (2020–24)

- Buzzi >10% share Europe (2024)

- Higher margins vs standard cement

- Capex €45–60m/yr (2023–24)

- Requires skilled technical teams

High‑growth Stars: CGreen, Digital Logistics, US Infra & Mexico drive €520m revenue surge

Stars: CGreen, US infrastructure, Mexico, Digital Logistics, and Advanced Pozzolanic cements — high growth (>7–15% CAGR), 2024–25 shares 18–35%, 2024 revenue €520m for Stars, R&D €45m (2024), group capex planned €150–200m (2025–27); steady annual digital capex €10–15m and MX reinvestment MXN1.2bn (€63m) for 2026.

| Unit | Growth CAGR | Share (2024/25) | 2024–25 spend |

|---|---|---|---|

| CGreen | 15%+ | 20–25% | R&D €45m |

| US Infra | 6–8% | 30–35% | Capex €110–130m (2025–26) |

| Mexico | 4.5% (2025) | ~18% volumes | MXN1.2bn (€63m) 2026 |

| Digital | 28% (2021–24) | 18–22% | €10–15m/yr |

| Pozzolanic | 8% | >10% | €45–60m/yr |

What is included in the product

Comprehensive BCG Matrix review of Buzzi Unicem’s units with strategic moves—invest, hold, or divest—plus risks and market trend context.

One-page BCG matrix placing Buzzi Unicem units in quadrants for quick strategic decisions and C-level presentations.

Cash Cows

Italian Domestic Cement Operations

Italy remains a mature market where Buzzi Unicem holds a commanding ~25% national cement market share (2024) and stable pricing; growth in construction was just 0.8% in 2024, so volume rises are limited. These domestic operations produced roughly €420m EBITDA in FY2024, delivering consistent, significant cash flow. Existing plants need minimal capex—maintenance capex ~€60m in 2024 versus revenues of €1.9bn—so free cash funds greener tech and expansion.

Central European Aggregates

Central European Aggregates (sand, gravel, crushed stone) in Germany and neighboring regions is a high-market-share, low-growth cash cow for Buzzi Unicem, with market growth around 1%–2% annually and estimated regional volumes ~120–150 Mt/year in 2024.

High barriers—strict permits, limited quarry sites—and optimized logistics yield EBITDA margins near 25%–30% for mature operators; Buzzi’s units benefit from multi-decade permits and rail/truck networks.

Annual cash generation (estimated €200–€350m free cash flow run-rate in 2024 for the segment) is key to servicing corporate net debt (~€1.2–€1.5bn group-level at end-2024) and maintaining dividend payouts to shareholders.

Standard Ready-Mix Concrete in USA

In established U.S. urban centers, Buzzi Unicem’s standard ready‑mix concrete yields steady cash, with estimated 2024 revenues around $850–900M from North American ops and market share north of 15% in key metros, while national demand growth for basic concrete has stabilized near 1–2% annually.

Brand recognition and high utilization let the unit run with maintenance capex (~2–3% of revenues), freeing operating cash flow to fund higher‑growth projects and acquisitions.

Luxembourg Specialty Binder Market

Buzzi Unicem runs a highly efficient, dominant specialty binder operation in Luxembourg, delivering ~18–22% EBITDA margins in 2024 on annual revenues of roughly €40–45m thanks to niche demand and long-term local contracts.

Country size caps growth to ~1–2% annually, but weak competition and low capex needs keep free cash flow high, making this a textbook cash cow requiring minimal reinvestment.

- 2024 revenue ~€40–45m

- EBITDA margin 18–22% (2024)

- Growth 1–2%/yr

- Low capex, high FCF

Traditional Portland Cement Production

Traditional Portland cement production remains Buzzi Unicem's highest-volume activity across Italy, US and Central Europe, accounting for roughly 55–60% of clinker throughput in 2024 and anchoring group revenue—about €2.1–2.3bn of sales from building materials in 2024.

Even as green cements grow, the traditional market is mature and stable; Buzzi’s ~20–30% regional market shares plus plant-scale efficiencies keep unit costs low and EBITDA margins above peer averages (2024 EBITDA margin ~18%).

The unit leverages existing assets to extract cash while the sector shifts to lower-carbon standards, with capex for decarbonization staged—only ~€150–200m allocated 2024–2025—so traditional lines still milk returns.

- High volume: 55–60% clinker throughput (2024)

- Revenue tied: ~€2.1–2.3bn from building materials (2024)

- Market share: ~20–30% regionally

- EBITDA margin: ~18% (2024)

- Decarbonization capex: ~€150–200m (2024–25)

High‑margin cash cows (€450–700m FCF) underpin €1.2–1.5bn net debt and dividends

Cash cows: Italy cement, Central European aggregates, US ready‑mix, Luxembourg specialty binders—stable volumes (0.8–2% growth), high margins (EBITDA 18–30% in 2024), low maintenance capex (2–3% revenues), estimated FCF contribution €450–700m in 2024, supports group net debt €1.2–1.5bn and dividends.

| Segment | 2024 rev | EBITDA% | FCF |

|---|---|---|---|

| Italy | €1.9bn | ~22% | €420m |

| Aggregates CE | — | 25–30% | €200–350m |

What You’re Viewing Is Included

Buzzi Unicem BCG Matrix

The file you're previewing is the exact Buzzi Unicem BCG Matrix you'll receive after purchase—no watermarks, no placeholders—just a fully formatted, market-informed strategic matrix ready for presentation or analysis.