Broadwind Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

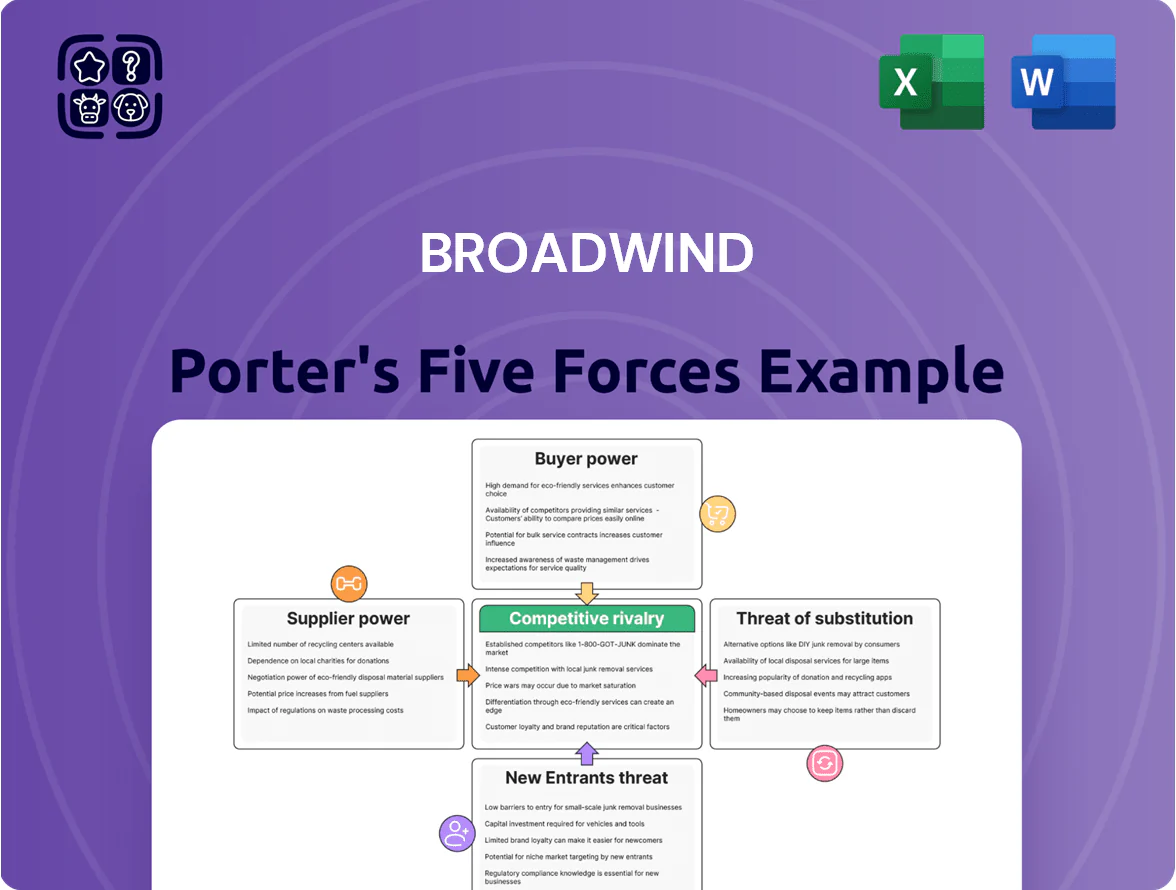

Broadwind faces moderate supplier power due to specialized components, low buyer concentration, and niche barriers that limit new entrants, while substitutes and rivalry hinge on cyclical energy and industrial demand—this snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Broadwind’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Raw material price volatility

Specialized component availability

The Industrial Solutions segment depends on niche electronic and mechanical parts from a small vendor pool, giving suppliers high bargaining power; in 2025 about 60–70% of critical components are single- or dual-sourced, raising price and availability risk.

Supply disruptions can cause multi-week production delays and 8–12% higher procurement costs observed in 2024–25; Broadwind holds strategic inventory covering 10–14 weeks of critical parts to buffer supplier-driven bottlenecks.

Energy and utility costs

Manufacturing heavy steel structures and precision gears is energy-intensive, making Broadwind vulnerable to electricity and natural gas price spikes; U.S. industrial electricity prices rose ~6% in 2024 and Henry Hub natural gas averaged $3.50/MMBtu in 2024, pressuring margins.

Industrial energy suppliers hold power because Broadwind’s large fabrication sites lack easy fuel or grid-switch options, raising switching costs and outage risk.

Management uses long-term hedges and fixed-price contracts; for example, a 2024 hedging program capped ~60% of expected 2025 gas needs, stabilizing cash flow but locking in costs.

Concentration of steel producers

The consolidation of North American steel producers has cut viable vendors for large industrial projects, concentrating supply among top mills and raising their bargaining power.

Major mills now push harder on payment terms and delivery timing; in 2024 five firms accounted for roughly 68% of US flat-rolled steel capacity, tightening leverage.

Broadwind’s pricing depends on its annual purchase volumes and steel cycles—auto and construction demand swings (±15–25% year-to-year) materially affect spot premiums.

- Fewer vendors → higher supplier leverage

- Top mills set tougher payment/delivery terms

- Broadwind price power tied to volume

- Steel cycle volatility ±15–25% impacts costs

Skilled labor as a supplier service

The 2025 shortage of certified welders and precision machinists constrains Broadwind’s output; national shortage estimates show 8–12% skill gaps in metal fabrication trades, raising delay risk and overtime costs.

Unions and staffing agencies gain leverage, pushing wage premiums (reported +6–10% in 2024–25) and contracting terms; Broadwind needs targeted retention and apprenticeship investment to protect capacity.

Supplier dominance, volatile inputs and labor strains squeeze margins in 2024–25

Suppliers hold high power: steel concentration (five firms = ~68% US flat-rolled capacity in 2024) and 60–70% single/dual sourcing for critical parts raise cost and delivery leverage; steel price volatility (HRC avg ~$950/ton in 2024) and energy/gas spikes (gas ~$3.50/MMBtu, electricity +6% in 2024) can cut margins; labor shortages (8–12% gap) and wage inflation (+6–10%) add pressure.

| Metric | 2024–25 |

|---|---|

| US flat-rolled share (top5) | ~68% |

| Steel HRC price | $~950/ton (2024) |

| Gas price | $3.50/MMBtu (2024) |

| Electricity change | +6% (2024) |

| Single/dual-sourced parts | 60–70% |

| Skilled labor gap | 8–12% |

| Wage inflation | +6–10% |

What is included in the product

Tailored Porter's Five Forces analysis for Broadwind that uncovers competitive drivers, supplier and buyer power, entry barriers, substitutes, and disruptive threats, with industry-backed commentary for strategic decision-making.

A concise Porter’s Five Forces one-sheet for Broadwind—quickly highlights supplier, buyer, and competitive pressures to speed strategic decisions and investor briefings.

Customers Bargaining Power

Concentration of wind turbine OEMs

Long term contract negotiations

Customers push for multi-year supply agreements that lock pricing and set strict performance KPIs; Broadwind reported a $160m backlog at end-2025, giving revenue visibility but constraining mid-cycle price resets.

These contracts lower revenue volatility yet compress margins when input costs rise—Broadwind’s gross margin fell to 12.4% in FY2024 after steel and labor inflation, showing the trade-off.

Sensitivity to federal tax credits

Customer buying power is highly tied to federal tax credits like the Production Tax Credit (PTC) and Investment Tax Credit (ITC); a 2024 IRS rule change and 2025 ITC phase-down forecasts cut some project NPV by ~10–18%, shifting negotiation leverage to buyers.

When PTC/ITC rules change or expire, demand and financing swing quickly—project pipeline contractions reached 22% in Q2 2025 for some US wind developers.

As of late 2025, strict domestic content (IRA) rules drive buyers to favor suppliers meeting Buy America; about 65% of US utility RFPs required domestic content to secure full tax benefits, strengthening buyer leverage.

Quality and precision requirements

Industrial buyers in mining, marine, and energy demand extreme precision and ISO/ASME safety certifications; a single component failure can cost $1M+ in downtime and liability, so customers force audits and traceability.

Broadwind spends to meet specs—capital intensity: recent 2024 capex ~ $15M—so advanced NDT (non‑destructive testing) and metrology are required to retain contracts and prevent churn.

- High failure cost: $1M+ per incident

- 2024 capex: ~$15M

- Requires ISO/ASME, NDT, metrology

Global procurement alternatives

- 25–30% of components sourced from Asia (2024)

- Ocean freight ranges $1,200–$1,800 (2024 spikes)

- Tariffs provide partial protection (Section 232/301)

- Defendable 5–10% domestic premium via logistics and quality

Broadwind squeezed by OEM concentration, modest margins and Buy‑America pressures

| Metric | Value |

|---|---|

| Top OEM share (2024) | 40–60% |

| Wind gross margin (FY2024) | ~12.4% |

| Backlog (end‑2025) | $160m |

| Offshore component share (2024) | 25–30% |

| RFPs requiring domestic content (2025) | ~65% |

Preview Before You Purchase

Broadwind Porter's Five Forces Analysis

This preview shows the exact Broadwind Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders; the file is fully formatted and ready for use.

You're looking at the actual deliverable: the same professionally written, download-ready document will be available to you instantly after payment.

No mockups or samples—this is the complete, ready-to-use analysis file, precisely what you'll get upon buying.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

Broadwind faces moderate supplier power due to specialized components, low buyer concentration, and niche barriers that limit new entrants, while substitutes and rivalry hinge on cyclical energy and industrial demand—this snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Broadwind’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Raw material price volatility

Specialized component availability

The Industrial Solutions segment depends on niche electronic and mechanical parts from a small vendor pool, giving suppliers high bargaining power; in 2025 about 60–70% of critical components are single- or dual-sourced, raising price and availability risk.

Supply disruptions can cause multi-week production delays and 8–12% higher procurement costs observed in 2024–25; Broadwind holds strategic inventory covering 10–14 weeks of critical parts to buffer supplier-driven bottlenecks.

Energy and utility costs

Manufacturing heavy steel structures and precision gears is energy-intensive, making Broadwind vulnerable to electricity and natural gas price spikes; U.S. industrial electricity prices rose ~6% in 2024 and Henry Hub natural gas averaged $3.50/MMBtu in 2024, pressuring margins.

Industrial energy suppliers hold power because Broadwind’s large fabrication sites lack easy fuel or grid-switch options, raising switching costs and outage risk.

Management uses long-term hedges and fixed-price contracts; for example, a 2024 hedging program capped ~60% of expected 2025 gas needs, stabilizing cash flow but locking in costs.

Concentration of steel producers

The consolidation of North American steel producers has cut viable vendors for large industrial projects, concentrating supply among top mills and raising their bargaining power.

Major mills now push harder on payment terms and delivery timing; in 2024 five firms accounted for roughly 68% of US flat-rolled steel capacity, tightening leverage.

Broadwind’s pricing depends on its annual purchase volumes and steel cycles—auto and construction demand swings (±15–25% year-to-year) materially affect spot premiums.

- Fewer vendors → higher supplier leverage

- Top mills set tougher payment/delivery terms

- Broadwind price power tied to volume

- Steel cycle volatility ±15–25% impacts costs

Skilled labor as a supplier service

The 2025 shortage of certified welders and precision machinists constrains Broadwind’s output; national shortage estimates show 8–12% skill gaps in metal fabrication trades, raising delay risk and overtime costs.

Unions and staffing agencies gain leverage, pushing wage premiums (reported +6–10% in 2024–25) and contracting terms; Broadwind needs targeted retention and apprenticeship investment to protect capacity.

Supplier dominance, volatile inputs and labor strains squeeze margins in 2024–25

Suppliers hold high power: steel concentration (five firms = ~68% US flat-rolled capacity in 2024) and 60–70% single/dual sourcing for critical parts raise cost and delivery leverage; steel price volatility (HRC avg ~$950/ton in 2024) and energy/gas spikes (gas ~$3.50/MMBtu, electricity +6% in 2024) can cut margins; labor shortages (8–12% gap) and wage inflation (+6–10%) add pressure.

| Metric | 2024–25 |

|---|---|

| US flat-rolled share (top5) | ~68% |

| Steel HRC price | $~950/ton (2024) |

| Gas price | $3.50/MMBtu (2024) |

| Electricity change | +6% (2024) |

| Single/dual-sourced parts | 60–70% |

| Skilled labor gap | 8–12% |

| Wage inflation | +6–10% |

What is included in the product

Tailored Porter's Five Forces analysis for Broadwind that uncovers competitive drivers, supplier and buyer power, entry barriers, substitutes, and disruptive threats, with industry-backed commentary for strategic decision-making.

A concise Porter’s Five Forces one-sheet for Broadwind—quickly highlights supplier, buyer, and competitive pressures to speed strategic decisions and investor briefings.

Customers Bargaining Power

Concentration of wind turbine OEMs

Long term contract negotiations

Customers push for multi-year supply agreements that lock pricing and set strict performance KPIs; Broadwind reported a $160m backlog at end-2025, giving revenue visibility but constraining mid-cycle price resets.

These contracts lower revenue volatility yet compress margins when input costs rise—Broadwind’s gross margin fell to 12.4% in FY2024 after steel and labor inflation, showing the trade-off.

Sensitivity to federal tax credits

Customer buying power is highly tied to federal tax credits like the Production Tax Credit (PTC) and Investment Tax Credit (ITC); a 2024 IRS rule change and 2025 ITC phase-down forecasts cut some project NPV by ~10–18%, shifting negotiation leverage to buyers.

When PTC/ITC rules change or expire, demand and financing swing quickly—project pipeline contractions reached 22% in Q2 2025 for some US wind developers.

As of late 2025, strict domestic content (IRA) rules drive buyers to favor suppliers meeting Buy America; about 65% of US utility RFPs required domestic content to secure full tax benefits, strengthening buyer leverage.

Quality and precision requirements

Industrial buyers in mining, marine, and energy demand extreme precision and ISO/ASME safety certifications; a single component failure can cost $1M+ in downtime and liability, so customers force audits and traceability.

Broadwind spends to meet specs—capital intensity: recent 2024 capex ~ $15M—so advanced NDT (non‑destructive testing) and metrology are required to retain contracts and prevent churn.

- High failure cost: $1M+ per incident

- 2024 capex: ~$15M

- Requires ISO/ASME, NDT, metrology

Global procurement alternatives

- 25–30% of components sourced from Asia (2024)

- Ocean freight ranges $1,200–$1,800 (2024 spikes)

- Tariffs provide partial protection (Section 232/301)

- Defendable 5–10% domestic premium via logistics and quality

Broadwind squeezed by OEM concentration, modest margins and Buy‑America pressures

| Metric | Value |

|---|---|

| Top OEM share (2024) | 40–60% |

| Wind gross margin (FY2024) | ~12.4% |

| Backlog (end‑2025) | $160m |

| Offshore component share (2024) | 25–30% |

| RFPs requiring domestic content (2025) | ~65% |

Preview Before You Purchase

Broadwind Porter's Five Forces Analysis

This preview shows the exact Broadwind Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders; the file is fully formatted and ready for use.

You're looking at the actual deliverable: the same professionally written, download-ready document will be available to you instantly after payment.

No mockups or samples—this is the complete, ready-to-use analysis file, precisely what you'll get upon buying.