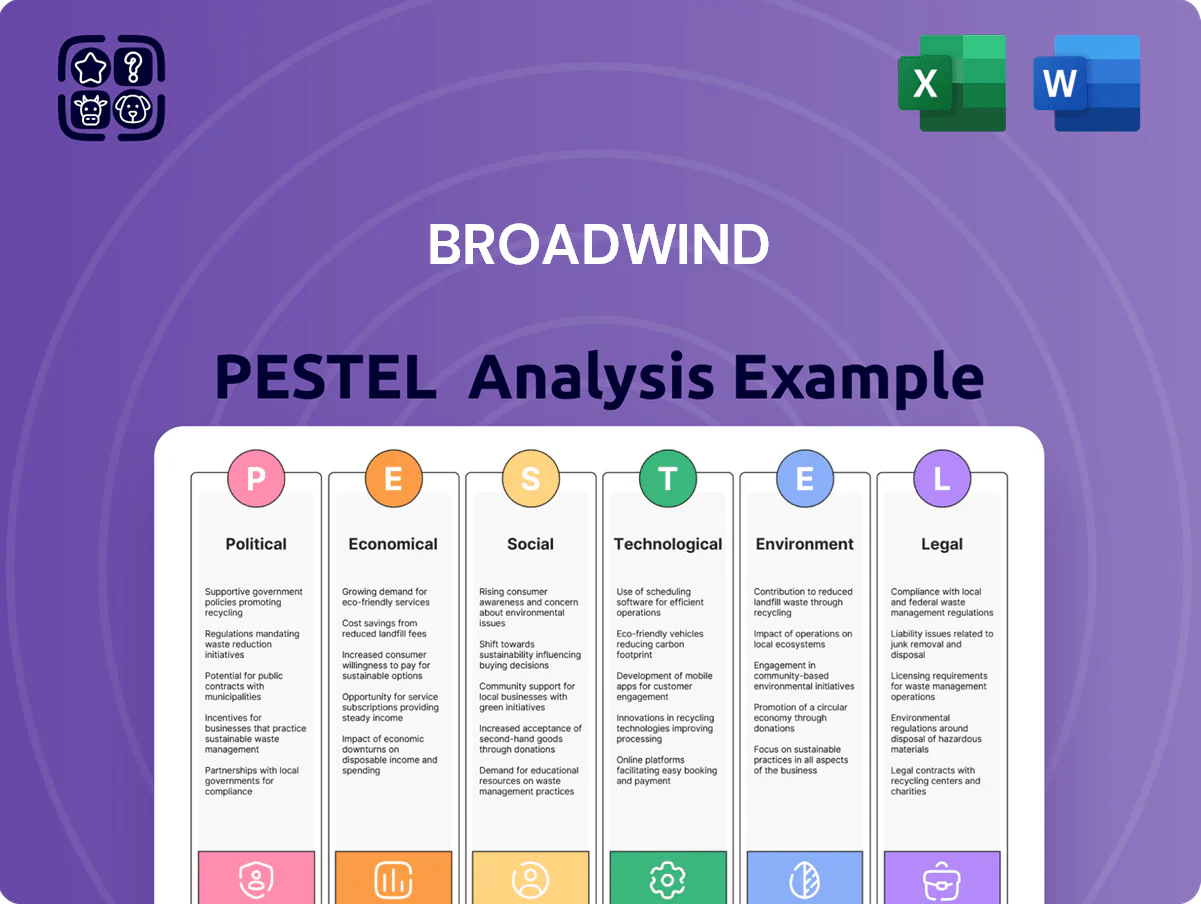

Broadwind PESTLE Analysis

Your Competitive Advantage Starts with This Report

Discover how political shifts, economic cycles, and technological advances are shaping Broadwind’s strategic outlook in our concise PESTLE snapshot—perfect for investors and strategists who need quick, actionable context; purchase the full analysis to access detailed risk assessments, regulatory impacts, and growth opportunities you can use immediately.

Political factors

IRA Policy Continuity

The Inflation Reduction Act remains a primary driver for Broadwind into late 2025, with IRA-linked federal tax credits supporting an estimated $120–180 million of incremental wind tower and clean energy component demand over the next five years.

These advanced manufacturing credits, which helped boost U.S. domestic wind investment by 22% in 2024, give Broadwind multi-year visibility into bookings and justify capacity investments and a targeted $25–40 million capex plan through 2026.

Any political shifts that threaten the durability of these subsidies would directly pressure Broadwind’s order book, risking downward revisions to revenue guidance (2025 revenue target stood at $210–230 million) and forcing reallocation of capital away from growth projects.

Trade Policy and Tariffs

Trade protections on imported steel and wind-tower components shape Broadwind's competitiveness versus foreign makers; US tariffs raised steel prices by about 25% after 2018 measures, and Broadwind's 2024 cost of goods sold for tower segments reflected ~12% higher steel input costs versus pre-tariff levels.

Alterations to tariff schedules or anti-dumping duties can swing raw-material costs and domestic fabricators' pricing power; in 2023 US anti-dumping actions on certain steel grades pushed spot coil prices up ~8% year-over-year.

Strategic trade ties with allies—USMCA, UK, EU supply agreements—affect supply-chain resilience; Broadwind sources ~30% of specialty steel from allied markets, making bilateral trade stability crucial for order fulfillment and margin preservation.

Defense Spending Priorities

Broadwind’s Gearing and Heavy Fabrications segments remain tied to federal defense budgets; the FY2026 proposed DoD budget of approximately $858 billion and recent multi-year Shipbuilding allocations increase visibility for large-equipment procurement, supporting backlog growth potential for mission-critical components.

Congressional initiatives like the 2024 CHIPS and Science Act–adjacent industrial base funding and 2025 domestic sourcing incentives boost Broadwind’s qualification prospects for long-term defense contracts, reducing supply-chain risk.

Elevated geopolitical tensions and U.S. policy emphasizing readiness have driven procurement upticks—naval and ground systems spending rose ~6% YoY in 2024—lifting demand for specialized gearing used in maritime and land defense platforms.

State Renewable Mandates

State Renewable Portfolio Standards (RPS) drive localized demand clusters for Broadwind’s wind towers and components; 29 states plus DC had RPS or equivalent targets by 2025, supporting projected U.S. wind additions of ~30 GW in 2024–25 per AWEA/DOE estimates.

Political backing for offshore wind in Atlantic/Great Lakes states and onshore Midwest incentives shifts facility utilization toward coastal manufacturing and Midwest supply chains; U.S. offshore capacity targets reached 30 GW by 2030 under federal goals.

Divergent state rules on land use and transmission—permitting timelines varying from months to years—can accelerate or delay projects, affecting Broadwind revenue timing given multi-year contract lead times and capex cycles.

- 29 states + DC with RPS (2025)

- U.S. projected wind add ~30 GW (2024–25)

- Offshore target ~30 GW by 2030

- Permitting timelines vary months–years

Permitting Reform Legislation

Federal permitting reform efforts—such as proposed legislation in 2024 aiming to cut review times for major energy projects by up to 30%—are critical to clearing Broadwind’s backlog and accelerating tower orders.

Legislative progress or gridlock on environmental review shortcuts directly alters customers’ move from planning to procurement, impacting revenue timing for Heavy Fabrications.

Faster permitting cycles support steadier production schedules, lifting capacity utilization and cost efficiency; a 10–15% reduction in lead times could meaningfully improve margin stability.

- 2024 proposals target ~30% faster reviews

- 10–15% lead-time reduction boosts utilization

- Permitting delays shift revenue timing

IRA, defense funds & wind growth justify $25–40M capex despite steel-cost squeeze

IRA tax credits underpin $120–180M incremental demand through 2029 and justify $25–40M capex to 2026; tariffs raised steel costs ~25% post-2018, adding ~12% to Broadwind tower COGS in 2024; defense budget (~$858B FY2026) and CHIPS-style industrial funding lift Heavy Fabrications backlog; state RPS (29 states + DC) and projected ~30 GW US wind additions (2024–25) drive demand but permitting delays (months–years) risk timing.

| Metric | Value |

|---|---|

| IRA-driven demand | $120–180M (5 yrs) |

| Planned capex | $25–40M (to 2026) |

| Steel cost impact | +25% tariffs; +12% COGS (2024) |

| FY2026 DoD budget | $858B |

| States with RPS | 29 + DC (2025) |

| US wind additions | ~30 GW (2024–25) |

What is included in the product

Explores how external macro-environmental factors uniquely affect Broadwind across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify actionable risks and opportunities.

Condenses Broadwind's full PESTLE into a concise, shareable summary that supports quick alignment in meetings, is easy to drop into presentations, and uses simple language for all stakeholders.

Economic factors

Interest Rate Environment

The cost of capital remains critical for Broadwind's capital-intensive wind and infrastructure projects; US 10-year Treasury yields averaged about 4.2% in 2024, keeping borrowing costs elevated for developers. High interest rates contributed to delayed or canceled projects in 2024, with US renewable project financing activity down roughly 15% year-over-year. A stabilizing trend into late 2025—markets projecting Fed cuts and 10-year yields easing toward 3.5%—would revive investment in large-scale industrial and energy infrastructure.

Steel Price Volatility

As a major consumer of heavy steel plate, Broadwind is highly exposed to steel price volatility; hot-rolled coil averaged about $900/ton in 2024 after peaking near $1,200/ton in mid-2022, creating margin pressure on manufacturing-intensive orders.

Economic shifts that alter steel production costs or demand from sectors like automotive—global steel demand rose ~2.5% in 2024—can squeeze Broadwind’s margins if not managed through indexed contracts.

The company must balance inventory and market timing—carrying costs vs. spot exposure—to mitigate risks from raw-material price spikes, given steel input can represent 20–35% of project costs in heavy equipment manufacturing.

Industrial Production Trends

Broadwind’s revenue correlates with U.S. industrial output—mining, energy, and heavy equipment drove demand for its Gearing segment; U.S. industrial production rose 0.4% month-over-month in Dec 2025 but was down 0.8% year-over-year, signaling mixed momentum for orders.

Labor Cost Inflation

Rising wages for skilled welders, machinists and engineers—US median hourly pay for welders rose ~6% from 2022–2024 to about $21.50/hr—push Broadwind’s fabrication costs higher, tightening margins amid strong demand for skilled labor.

Persistent labor inflation (US private sector wage growth ~4.2% Y/Y in 2024) forces Broadwind to pursue automation, productivity gains or price increases to protect EBITDA.

Balancing retention—turnover costs often 20–30% of salary for specialized roles—and overhead control is critical to sustain competitive margins in fabrication.

- Wage inflation ~6% for welders (2022–2024)

- US private wage growth ~4.2% Y/Y (2024)

- Turnover cost ~20–30% of salary for specialized hires

- Options: automation, price adjustments, productivity programs

Energy Market Dynamics

Natural gas traded around $3.00–4.50/MMBtu in 2024–2025, while onshore wind LCOE averaged $30–45/MWh, keeping wind broadly cost-competitive versus fossil-fired generation in many U.S. and European markets.

Periods of depressed fossil prices can slow renewables deployment, but 2022–2024 volatility and carbon pricing pushed higher investment in wind; Broadwind's growth hinges on wind maintaining LCOE parity or advantage.

- Natural gas: ~$3–4.5/MMBtu (2024–2025)

- Onshore wind LCOE: ~$30–45/MWh

- Higher fossil volatility and carbon pricing accelerate wind uptake

- Broadwind reliant on sustained wind cost-competitiveness

Broadwind margins squeezed by rates, steel, and labor; wind demand holds

High financing costs (US 10y ~4.2% in 2024) and steel volatility (HRC ~$900/ton in 2024) pressured Broadwind margins; labor inflation (welders ~$21.50/hr; private wage growth ~4.2% Y/Y in 2024) raises fabrication costs. Wind LCOE ~$30–45/MWh keeps demand resilient, while project financing down ~15% YoY (2024) risks order delays; automation and indexed contracts mitigate exposure.

| Metric | 2024–25 |

|---|---|

| US 10y | ~4.2% |

| HRC | ~$900/ton |

| Welders pay | ~$21.50/hr |

| Wind LCOE | $30–45/MWh |

| Proj financing | -15% YoY |

Same Document Delivered

Broadwind PESTLE Analysis

The preview shown here is the exact Broadwind PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the content and structure visible in this preview match the final file you’ll instantly download after payment.

Don’t imagine the product—this is the real, finished PESTLE analysis you’ll own upon checkout.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Competitive Advantage Starts with This Report

Discover how political shifts, economic cycles, and technological advances are shaping Broadwind’s strategic outlook in our concise PESTLE snapshot—perfect for investors and strategists who need quick, actionable context; purchase the full analysis to access detailed risk assessments, regulatory impacts, and growth opportunities you can use immediately.

Political factors

IRA Policy Continuity

The Inflation Reduction Act remains a primary driver for Broadwind into late 2025, with IRA-linked federal tax credits supporting an estimated $120–180 million of incremental wind tower and clean energy component demand over the next five years.

These advanced manufacturing credits, which helped boost U.S. domestic wind investment by 22% in 2024, give Broadwind multi-year visibility into bookings and justify capacity investments and a targeted $25–40 million capex plan through 2026.

Any political shifts that threaten the durability of these subsidies would directly pressure Broadwind’s order book, risking downward revisions to revenue guidance (2025 revenue target stood at $210–230 million) and forcing reallocation of capital away from growth projects.

Trade Policy and Tariffs

Trade protections on imported steel and wind-tower components shape Broadwind's competitiveness versus foreign makers; US tariffs raised steel prices by about 25% after 2018 measures, and Broadwind's 2024 cost of goods sold for tower segments reflected ~12% higher steel input costs versus pre-tariff levels.

Alterations to tariff schedules or anti-dumping duties can swing raw-material costs and domestic fabricators' pricing power; in 2023 US anti-dumping actions on certain steel grades pushed spot coil prices up ~8% year-over-year.

Strategic trade ties with allies—USMCA, UK, EU supply agreements—affect supply-chain resilience; Broadwind sources ~30% of specialty steel from allied markets, making bilateral trade stability crucial for order fulfillment and margin preservation.

Defense Spending Priorities

Broadwind’s Gearing and Heavy Fabrications segments remain tied to federal defense budgets; the FY2026 proposed DoD budget of approximately $858 billion and recent multi-year Shipbuilding allocations increase visibility for large-equipment procurement, supporting backlog growth potential for mission-critical components.

Congressional initiatives like the 2024 CHIPS and Science Act–adjacent industrial base funding and 2025 domestic sourcing incentives boost Broadwind’s qualification prospects for long-term defense contracts, reducing supply-chain risk.

Elevated geopolitical tensions and U.S. policy emphasizing readiness have driven procurement upticks—naval and ground systems spending rose ~6% YoY in 2024—lifting demand for specialized gearing used in maritime and land defense platforms.

State Renewable Mandates

State Renewable Portfolio Standards (RPS) drive localized demand clusters for Broadwind’s wind towers and components; 29 states plus DC had RPS or equivalent targets by 2025, supporting projected U.S. wind additions of ~30 GW in 2024–25 per AWEA/DOE estimates.

Political backing for offshore wind in Atlantic/Great Lakes states and onshore Midwest incentives shifts facility utilization toward coastal manufacturing and Midwest supply chains; U.S. offshore capacity targets reached 30 GW by 2030 under federal goals.

Divergent state rules on land use and transmission—permitting timelines varying from months to years—can accelerate or delay projects, affecting Broadwind revenue timing given multi-year contract lead times and capex cycles.

- 29 states + DC with RPS (2025)

- U.S. projected wind add ~30 GW (2024–25)

- Offshore target ~30 GW by 2030

- Permitting timelines vary months–years

Permitting Reform Legislation

Federal permitting reform efforts—such as proposed legislation in 2024 aiming to cut review times for major energy projects by up to 30%—are critical to clearing Broadwind’s backlog and accelerating tower orders.

Legislative progress or gridlock on environmental review shortcuts directly alters customers’ move from planning to procurement, impacting revenue timing for Heavy Fabrications.

Faster permitting cycles support steadier production schedules, lifting capacity utilization and cost efficiency; a 10–15% reduction in lead times could meaningfully improve margin stability.

- 2024 proposals target ~30% faster reviews

- 10–15% lead-time reduction boosts utilization

- Permitting delays shift revenue timing

IRA, defense funds & wind growth justify $25–40M capex despite steel-cost squeeze

IRA tax credits underpin $120–180M incremental demand through 2029 and justify $25–40M capex to 2026; tariffs raised steel costs ~25% post-2018, adding ~12% to Broadwind tower COGS in 2024; defense budget (~$858B FY2026) and CHIPS-style industrial funding lift Heavy Fabrications backlog; state RPS (29 states + DC) and projected ~30 GW US wind additions (2024–25) drive demand but permitting delays (months–years) risk timing.

| Metric | Value |

|---|---|

| IRA-driven demand | $120–180M (5 yrs) |

| Planned capex | $25–40M (to 2026) |

| Steel cost impact | +25% tariffs; +12% COGS (2024) |

| FY2026 DoD budget | $858B |

| States with RPS | 29 + DC (2025) |

| US wind additions | ~30 GW (2024–25) |

What is included in the product

Explores how external macro-environmental factors uniquely affect Broadwind across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify actionable risks and opportunities.

Condenses Broadwind's full PESTLE into a concise, shareable summary that supports quick alignment in meetings, is easy to drop into presentations, and uses simple language for all stakeholders.

Economic factors

Interest Rate Environment

The cost of capital remains critical for Broadwind's capital-intensive wind and infrastructure projects; US 10-year Treasury yields averaged about 4.2% in 2024, keeping borrowing costs elevated for developers. High interest rates contributed to delayed or canceled projects in 2024, with US renewable project financing activity down roughly 15% year-over-year. A stabilizing trend into late 2025—markets projecting Fed cuts and 10-year yields easing toward 3.5%—would revive investment in large-scale industrial and energy infrastructure.

Steel Price Volatility

As a major consumer of heavy steel plate, Broadwind is highly exposed to steel price volatility; hot-rolled coil averaged about $900/ton in 2024 after peaking near $1,200/ton in mid-2022, creating margin pressure on manufacturing-intensive orders.

Economic shifts that alter steel production costs or demand from sectors like automotive—global steel demand rose ~2.5% in 2024—can squeeze Broadwind’s margins if not managed through indexed contracts.

The company must balance inventory and market timing—carrying costs vs. spot exposure—to mitigate risks from raw-material price spikes, given steel input can represent 20–35% of project costs in heavy equipment manufacturing.

Industrial Production Trends

Broadwind’s revenue correlates with U.S. industrial output—mining, energy, and heavy equipment drove demand for its Gearing segment; U.S. industrial production rose 0.4% month-over-month in Dec 2025 but was down 0.8% year-over-year, signaling mixed momentum for orders.

Labor Cost Inflation

Rising wages for skilled welders, machinists and engineers—US median hourly pay for welders rose ~6% from 2022–2024 to about $21.50/hr—push Broadwind’s fabrication costs higher, tightening margins amid strong demand for skilled labor.

Persistent labor inflation (US private sector wage growth ~4.2% Y/Y in 2024) forces Broadwind to pursue automation, productivity gains or price increases to protect EBITDA.

Balancing retention—turnover costs often 20–30% of salary for specialized roles—and overhead control is critical to sustain competitive margins in fabrication.

- Wage inflation ~6% for welders (2022–2024)

- US private wage growth ~4.2% Y/Y (2024)

- Turnover cost ~20–30% of salary for specialized hires

- Options: automation, price adjustments, productivity programs

Energy Market Dynamics

Natural gas traded around $3.00–4.50/MMBtu in 2024–2025, while onshore wind LCOE averaged $30–45/MWh, keeping wind broadly cost-competitive versus fossil-fired generation in many U.S. and European markets.

Periods of depressed fossil prices can slow renewables deployment, but 2022–2024 volatility and carbon pricing pushed higher investment in wind; Broadwind's growth hinges on wind maintaining LCOE parity or advantage.

- Natural gas: ~$3–4.5/MMBtu (2024–2025)

- Onshore wind LCOE: ~$30–45/MWh

- Higher fossil volatility and carbon pricing accelerate wind uptake

- Broadwind reliant on sustained wind cost-competitiveness

Broadwind margins squeezed by rates, steel, and labor; wind demand holds

High financing costs (US 10y ~4.2% in 2024) and steel volatility (HRC ~$900/ton in 2024) pressured Broadwind margins; labor inflation (welders ~$21.50/hr; private wage growth ~4.2% Y/Y in 2024) raises fabrication costs. Wind LCOE ~$30–45/MWh keeps demand resilient, while project financing down ~15% YoY (2024) risks order delays; automation and indexed contracts mitigate exposure.

| Metric | 2024–25 |

|---|---|

| US 10y | ~4.2% |

| HRC | ~$900/ton |

| Welders pay | ~$21.50/hr |

| Wind LCOE | $30–45/MWh |

| Proj financing | -15% YoY |

Same Document Delivered

Broadwind PESTLE Analysis

The preview shown here is the exact Broadwind PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the content and structure visible in this preview match the final file you’ll instantly download after payment.

Don’t imagine the product—this is the real, finished PESTLE analysis you’ll own upon checkout.