Cabot Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

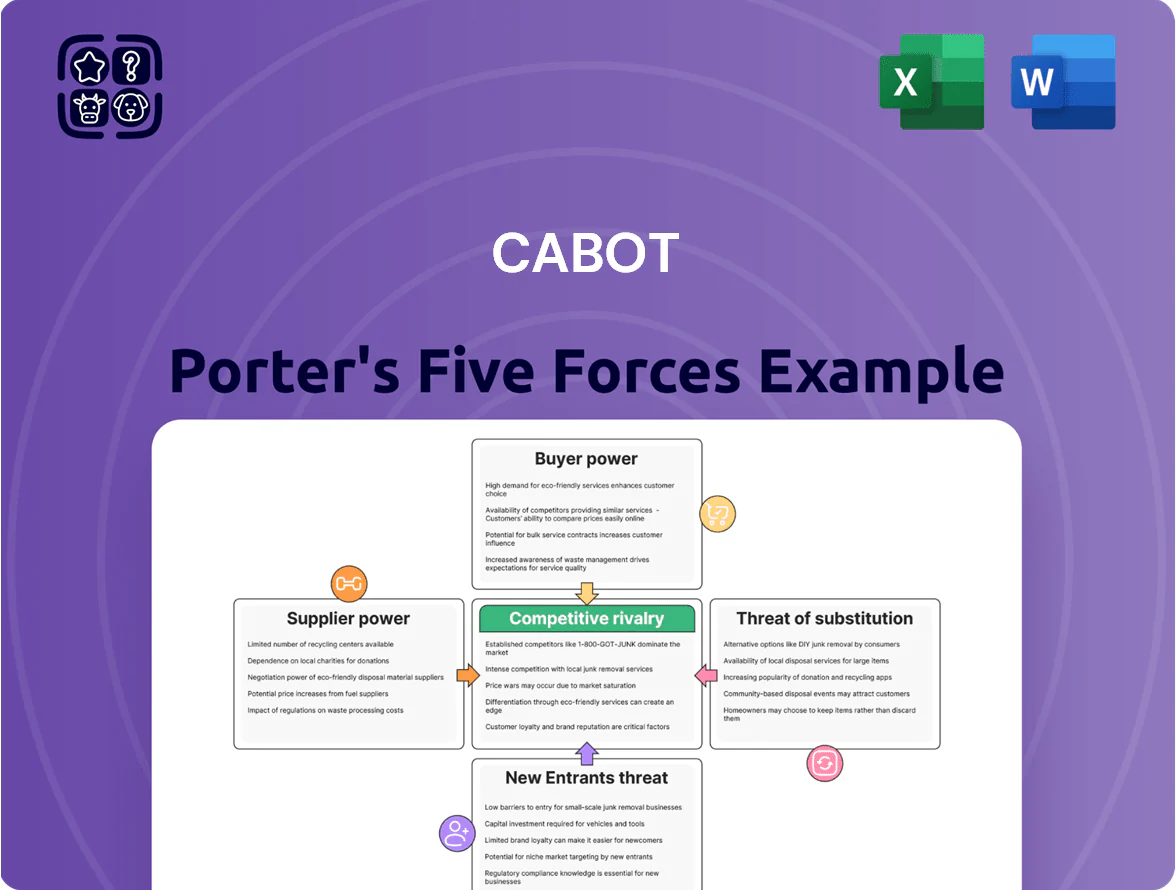

Cabot’s Five Forces snapshot highlights supplier leverage, buyer pressure, competitive rivalry, substitution risks, and entry barriers shaping its market—revealing where strategic focus matters most for margins and growth.

This brief preview only scratches the surface; unlock the full Porter's Five Forces Analysis to get force-by-force ratings, visuals, and actionable insights tailored to Cabot for smarter investment and strategic decisions.

Suppliers Bargaining Power

Feedstock Price Volatility

Cabot depends heavily on carbon black oil and natural gas, commodities whose prices rose ~35% YoY in 2024 and stayed volatile into 2025 amid OPEC+ output shifts and European gas disruptions; suppliers thus wield pricing power that compresses margins.

Concentration of Raw Material Providers

The global market for high-purity chemical feedstocks is concentrated: about 5–7 major suppliers control roughly 60% of supply capacity for specialty carbon and silica precursors as of 2025, giving them pricing and delivery leverage during negotiations.

That concentration lets suppliers push stricter delivery terms and minimum volumes, raising Cabot Corporation’s procurement risk and working-capital exposure.

Cabot must diversify suppliers, increase long-term contracts, and secure spot-buy buffers; a 10–15% multi-sourcing target reduces single-supplier dependence and limits disruption risk.

Regulatory Pressure on Upstream Suppliers

Regulatory pressure is raising supplier costs: stricter 2023–25 carbon and waste rules mean suppliers passed ~6–9% higher input prices to buyers like Cabot by 2024, raising Cabot’s raw-material bill materially.

Compliance capex shrank some upstream capacity: by 2025 about 12% of traditional suppliers curtailed output during greener-energy transitions, tightening supply and boosting spot prices.

Logistics and Transportation Dependencies

Bulk raw materials move via specialized shipping and pipelines run by third-party logistics (3PL) firms; in 2024 ocean freight rates averaged 1,200 USD/FEU for chemical lanes, so sudden rate hikes give 3PLs short-term leverage over Cabot.

Cabot’s global footprint exposes it to regional port bottlenecks and pipeline constraints; the 2023–24 supply-chain disruptions increased lead times by ~18%, amplifying supplier power during strikes or infrastructure outages.

- 3PLs control specialized assets

- 2024 avg ocean freight ~1,200 USD/FEU

- 2023–24 lead times +18%

- Regional strikes/infrastructure raise costs quickly

Shift Toward Bio-based Feedstocks

- Premiums: 10–30% (2024 market data)

- Supplier scarcity: niche certified suppliers <100 global

- Cabot target: 30% scope-3 cut by 2025

- Strategy: long-term contracts, co-investment, certification

Supplier Power Bites Cabot: 5–7 Firms, +35% Prices, Push for Multi‑sourcing & 30% Scope‑3

Suppliers hold high bargaining power: 5–7 firms supply ~60% of specialty feedstocks (2025), carbon black oil and gas prices rose ~35% YoY in 2024, and 2023–24 lead times increased ~18%, forcing Cabot toward multi-sourcing and long-term contracts (target: 10–15% multi-sourcing, 30% scope-3 cut by 2025).

| Metric | Value (year) |

|---|---|

| Concentration | 5–7 firms, ~60% (2025) |

| Carbon/gas price change | +35% YoY (2024) |

| Lead times | +18% (2023–24) |

| Multi-sourcing target | 10–15% |

| Cabot scope-3 goal | 30% by 2025 |

What is included in the product

Comprehensive Porter's Five Forces review tailored to Cabot, uncovering competitive drivers, supplier and buyer power, entry barriers, substitutes, and emerging disruptive threats to inform strategic decisions and investor materials.

A focused, one-sheet Cabot Porter Five Forces view that translates competitive dynamics into actionable strategy—ideal for quick boardroom decisions and investor memos.

Customers Bargaining Power

Concentration of Global Tire Manufacturers

Demand for Sustainable Product Lines

Customers in automotive and electronics now demand lower-carbon materials, with 78% of OEMs in a 2024 survey requiring supplier Scope 3 reporting and 62% tying purchases to emissions targets; that shifts bargaining power to buyers and forces product roadmaps. Cabot must accelerate R&D and decarbonize feedstocks to retain contracts worth over $400M in annual revenue or risk losing share to rivals with stronger sustainability scores.

Price Sensitivity in Performance Chemicals

Customers treat many high-volume performance chemicals as commodities despite Cabot’s specialty lines; global buyers can compare quotes quickly, so price cuts hit volumes—Cabot’s Q3 2025 sales mix showed ~42% volume-exposed products, increasing exposure to price moves.

In lower-growth regions like LATAM and parts of EMEA, procurement prioritizes cost: 2024 IMF growth of 1.5% in LATAM raised buyer price sensitivity, forcing Cabot to match global benchmark pricing or risk share loss.

Switching Costs and Technical Integration

Cabot’s materials are often integral to customers’ proprietary formulations, creating moderate switching costs since reformulation can take months and cost 1–3% of product COGS; yet large buyers typically dual-source, limiting Cabot’s leverage.

Dual-sourcing lets major customers shift volumes quickly—Cabot reported top-10 customers ~35% of 2024 sales—so price or service lapses can drive rapid supplier substitution.

- Moderate switching costs: reformulation time 3–12 months

- Dual-sourcing common: top buyers reduce dependency

- Top-10 customers ≈35% of 2024 revenue

- Price/service weakness → quick volume loss risk

Access to Alternative Material Technologies

- By 2025: major OEMs built materials labs

- Materials R&D ~0.5–1% of revenue for some firms

- In‑house validation creates credible alternatives

- Raises buyer negotiation power; compresses supplier margins

Concentrated buyers squeeze margins—OEMs push discounts, in‑house R&D and sustainability raise risk

| Metric | Value |

|---|---|

| Top-10 customers | ≈35% 2024 rev |

| Top-3 buyer discounts | 5–8% est. by 2025 |

| 2023 margin hit | 2.1% |

| OEMs requiring Scope 3 | 78% (2024) |

| Materials R&D by OEMs | 0.5–1% rev |

Same Document Delivered

Cabot Porter's Five Forces Analysis

This preview shows the exact Cabot Porter Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed is the same professionally written, fully formatted analysis you’ll be able to download and use the moment you buy.

No mockups or samples: this is the final, ready-to-use file you’ll get instantly upon payment.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Cabot’s Five Forces snapshot highlights supplier leverage, buyer pressure, competitive rivalry, substitution risks, and entry barriers shaping its market—revealing where strategic focus matters most for margins and growth.

This brief preview only scratches the surface; unlock the full Porter's Five Forces Analysis to get force-by-force ratings, visuals, and actionable insights tailored to Cabot for smarter investment and strategic decisions.

Suppliers Bargaining Power

Feedstock Price Volatility

Cabot depends heavily on carbon black oil and natural gas, commodities whose prices rose ~35% YoY in 2024 and stayed volatile into 2025 amid OPEC+ output shifts and European gas disruptions; suppliers thus wield pricing power that compresses margins.

Concentration of Raw Material Providers

The global market for high-purity chemical feedstocks is concentrated: about 5–7 major suppliers control roughly 60% of supply capacity for specialty carbon and silica precursors as of 2025, giving them pricing and delivery leverage during negotiations.

That concentration lets suppliers push stricter delivery terms and minimum volumes, raising Cabot Corporation’s procurement risk and working-capital exposure.

Cabot must diversify suppliers, increase long-term contracts, and secure spot-buy buffers; a 10–15% multi-sourcing target reduces single-supplier dependence and limits disruption risk.

Regulatory Pressure on Upstream Suppliers

Regulatory pressure is raising supplier costs: stricter 2023–25 carbon and waste rules mean suppliers passed ~6–9% higher input prices to buyers like Cabot by 2024, raising Cabot’s raw-material bill materially.

Compliance capex shrank some upstream capacity: by 2025 about 12% of traditional suppliers curtailed output during greener-energy transitions, tightening supply and boosting spot prices.

Logistics and Transportation Dependencies

Bulk raw materials move via specialized shipping and pipelines run by third-party logistics (3PL) firms; in 2024 ocean freight rates averaged 1,200 USD/FEU for chemical lanes, so sudden rate hikes give 3PLs short-term leverage over Cabot.

Cabot’s global footprint exposes it to regional port bottlenecks and pipeline constraints; the 2023–24 supply-chain disruptions increased lead times by ~18%, amplifying supplier power during strikes or infrastructure outages.

- 3PLs control specialized assets

- 2024 avg ocean freight ~1,200 USD/FEU

- 2023–24 lead times +18%

- Regional strikes/infrastructure raise costs quickly

Shift Toward Bio-based Feedstocks

- Premiums: 10–30% (2024 market data)

- Supplier scarcity: niche certified suppliers <100 global

- Cabot target: 30% scope-3 cut by 2025

- Strategy: long-term contracts, co-investment, certification

Supplier Power Bites Cabot: 5–7 Firms, +35% Prices, Push for Multi‑sourcing & 30% Scope‑3

Suppliers hold high bargaining power: 5–7 firms supply ~60% of specialty feedstocks (2025), carbon black oil and gas prices rose ~35% YoY in 2024, and 2023–24 lead times increased ~18%, forcing Cabot toward multi-sourcing and long-term contracts (target: 10–15% multi-sourcing, 30% scope-3 cut by 2025).

| Metric | Value (year) |

|---|---|

| Concentration | 5–7 firms, ~60% (2025) |

| Carbon/gas price change | +35% YoY (2024) |

| Lead times | +18% (2023–24) |

| Multi-sourcing target | 10–15% |

| Cabot scope-3 goal | 30% by 2025 |

What is included in the product

Comprehensive Porter's Five Forces review tailored to Cabot, uncovering competitive drivers, supplier and buyer power, entry barriers, substitutes, and emerging disruptive threats to inform strategic decisions and investor materials.

A focused, one-sheet Cabot Porter Five Forces view that translates competitive dynamics into actionable strategy—ideal for quick boardroom decisions and investor memos.

Customers Bargaining Power

Concentration of Global Tire Manufacturers

Demand for Sustainable Product Lines

Customers in automotive and electronics now demand lower-carbon materials, with 78% of OEMs in a 2024 survey requiring supplier Scope 3 reporting and 62% tying purchases to emissions targets; that shifts bargaining power to buyers and forces product roadmaps. Cabot must accelerate R&D and decarbonize feedstocks to retain contracts worth over $400M in annual revenue or risk losing share to rivals with stronger sustainability scores.

Price Sensitivity in Performance Chemicals

Customers treat many high-volume performance chemicals as commodities despite Cabot’s specialty lines; global buyers can compare quotes quickly, so price cuts hit volumes—Cabot’s Q3 2025 sales mix showed ~42% volume-exposed products, increasing exposure to price moves.

In lower-growth regions like LATAM and parts of EMEA, procurement prioritizes cost: 2024 IMF growth of 1.5% in LATAM raised buyer price sensitivity, forcing Cabot to match global benchmark pricing or risk share loss.

Switching Costs and Technical Integration

Cabot’s materials are often integral to customers’ proprietary formulations, creating moderate switching costs since reformulation can take months and cost 1–3% of product COGS; yet large buyers typically dual-source, limiting Cabot’s leverage.

Dual-sourcing lets major customers shift volumes quickly—Cabot reported top-10 customers ~35% of 2024 sales—so price or service lapses can drive rapid supplier substitution.

- Moderate switching costs: reformulation time 3–12 months

- Dual-sourcing common: top buyers reduce dependency

- Top-10 customers ≈35% of 2024 revenue

- Price/service weakness → quick volume loss risk

Access to Alternative Material Technologies

- By 2025: major OEMs built materials labs

- Materials R&D ~0.5–1% of revenue for some firms

- In‑house validation creates credible alternatives

- Raises buyer negotiation power; compresses supplier margins

Concentrated buyers squeeze margins—OEMs push discounts, in‑house R&D and sustainability raise risk

| Metric | Value |

|---|---|

| Top-10 customers | ≈35% 2024 rev |

| Top-3 buyer discounts | 5–8% est. by 2025 |

| 2023 margin hit | 2.1% |

| OEMs requiring Scope 3 | 78% (2024) |

| Materials R&D by OEMs | 0.5–1% rev |

Same Document Delivered

Cabot Porter's Five Forces Analysis

This preview shows the exact Cabot Porter Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed is the same professionally written, fully formatted analysis you’ll be able to download and use the moment you buy.

No mockups or samples: this is the final, ready-to-use file you’ll get instantly upon payment.