CalAmp PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Unlock strategic clarity with our targeted PESTLE Analysis of CalAmp—discover how political shifts, economic trends, social dynamics, technological advances, legal changes, and environmental factors will shape its trajectory; perfect for investors and strategists seeking actionable insights. Purchase the full report to get a comprehensive, editable analysis you can use immediately to inform decisions and identify growth or risk areas.

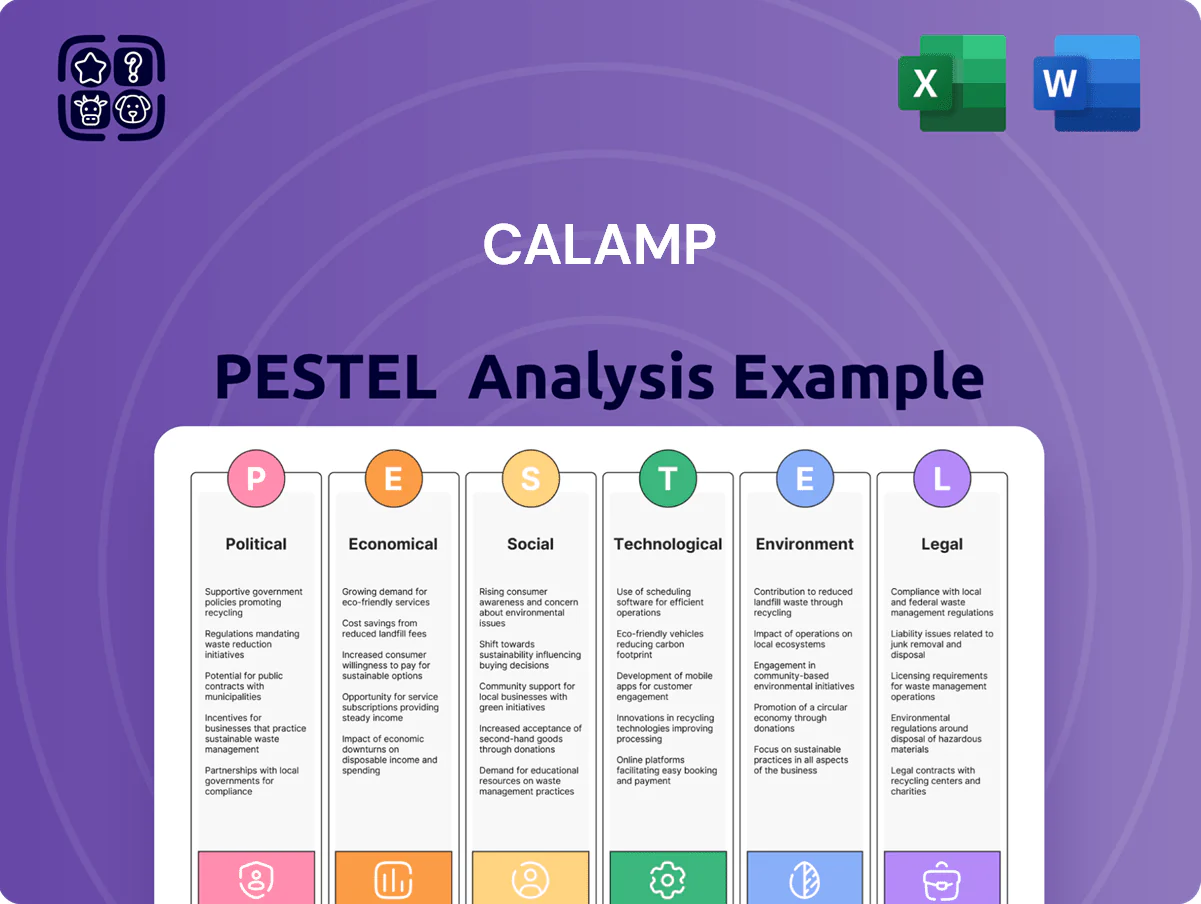

Political factors

Geopolitical Trade Relations

The ongoing US-China trade dynamics materially affect CalAmp’s hardware procurement, with tariffs on electronic components rising up to 25% in prior cycles and contributing to a reported 8–12% increase in COGS for comparable IoT hardware segments in 2023–2024. Tariffs on telecommunication hardware force margin compression or supply-chain shifts toward Southeast Asia; Vietnam and Malaysia sourcing reduced lead times by 15–20% for peers in 2024. Strategic international trade policy shifts through end-2025 remain a primary risk to maintaining CalAmp’s stable cost structure and 2025 gross-margin targets.

Government Infrastructure Spending

Increased federal and state funding—including the $110B Bipartisan Infrastructure Law allocations for public transit and the $5B+ Smart Cities programs through 2024–25—creates strong tailwinds for CalAmp’s public sector fleet management and asset-tracking solutions.

Government procurement preferences for domestic vendors favor CalAmp, as agencies prioritize supply-chain security and traceability, boosting win rates for contracts above $1M in ITS and fleet telematics.

Ongoing ITS investment, with U.S. DOT funding rising ~12% YoY in 2024, enables CalAmp to capture multi-year municipal deployments and recurring revenue from long-term service agreements.

Cybersecurity Policy and Standards

Political emphasis on national cybersecurity resilience forces telematics providers like CalAmp to meet strict data protection standards as US federal agencies increase IoT security requirements; CISA reported a 24% rise in IoT-related incident reports in 2024. Legislative scrutiny on connected devices tied to critical infrastructure—power, transit—has led to proposed mandates affecting $3.5B in government telematics procurement. CalAmp must align its SDLC with evolving NIST and federal frameworks to retain eligibility for public contracts and avoid revenue risks tied to noncompliance.

Regulatory Oversight of Data Sovereignty

Political moves toward data residency force CalAmp to localize storage and processing of telematics data, increasing infrastructure and compliance costs; GDPR fines can reach up to 4% of global turnover (€35.5B fines issued through 2023 across EU regulators).

In markets like the EU and parts of South America, requirements for local hosting raise operational complexity and may slow international expansion, potentially impacting revenue growth in 2024–25 where global IoT market CAGR is ~17% (2024–29).

- Must invest in regional data centers or partners

- GDPR-style penalties up to 4% revenue

- Higher OPEX and slower rollouts in certain markets

Stability in Key Global Markets

Continuous monitoring of political indicators and reallocating resources to stable markets is critical to limit revenue exposure—target capex hedging and regional diversification.

- Emerging-market FX volatility: ±12% (2024)

- Procurement/contract risk: −8% tender volume (2023)

- Mitigation: hedging, regional diversification, political monitoring

Tariffs, security and funding reshape IoT: costs up, supply times down, risks rise

US-China tariffs raised IoT component costs ~8–12% (2023–24) and Southeast Asia sourcing cut lead times 15–20% in 2024; US infrastructure programs (>$115B to 2025) and +12% YoY DOT funding (2024) boost public-sector demand; CISA reported +24% IoT incidents (2024) enforcing stricter security/NIST compliance; LATAM FX volatility ±12% (2024) and 2023 tender cuts −8% pose contract risk.

| Metric | Value |

|---|---|

| Tariff impact on COGS | +8–12% |

| Southeast Asia lead-time reduction | −15–20% |

| US infrastructure funding | >$115B (to 2025) |

| DOT funding change (2024) | +12% YoY |

| IoT incidents (CISA, 2024) | +24% |

| LATAM FX volatility (2024) | ±12% |

| Procurement tender change (2023) | −8% |

What is included in the product

Explores how external macro-environmental factors uniquely affect CalAmp across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section supported by current data and trends to surface risks and opportunities for executives, investors, and strategists.

Compact PESTLE summary tailored for CalAmp that distills regulatory, tech, economic, social, and environmental drivers into a single-page brief—ideal for quick reference in meetings or slide decks.

Economic factors

Global Supply Chain Volatility

Global supply chain volatility continues to affect CalAmp, with semiconductor prices easing since 2022 but spot shortages still causing lead-time variability; industry reports show lead times for key automotive-grade chips averaged 20–28 weeks in 2024 versus pre‑pandemic 8–12 weeks. Localized disruptions and commodity price swings (e.g., copper up 15% YTD 2025) can delay hardware shipments, pressuring Q1–Q3 2025 revenue recognition. Maintaining optimized inventory turns and strengthened supplier contracts remains crucial to protect hardware margins and ensure shipment predictability.

Interest Rate Environment

As of late 2025, the US Federal Reserve policy rate near 5.25–5.50% raised CalAmp’s weighted average cost of capital, increasing financing costs for customers; small and mid-size fleets reported a 12–18% reduction in planned telematics CAPEX in 2024–25. High rates delayed large-scale hardware rollouts, while Q3–Q4 2025 signs of rate stabilization and lower 10-year Treasury volatility supported renewed investment in efficiency tech like CalAmp’s platform.

Inflationary Pressure on Operating Costs

Inflation raises CalAmp’s labor costs—US tech wages rose ~5.8% in 2024—pushing higher salaries for software engineers and specialists while cloud and data costs climbed (AWS pricing pressure up ~6–8% YoY in 2024). CalAmp must balance these operating-cost increases with competitive SaaS pricing; implementing cost-containment measures and efficiency gains (automation, multi-cloud optimization) is critical to preserve margins amid sustained inflationary pressure.

Shift Toward Recurring Revenue Models

The economic transition from one-time hardware sales to recurring subscription revenue is central to CalAmp’s strategy, with subscription and services revenue rising to 55% of FY2025 revenue (approx $250M), improving predictability and commanding higher EV/Revenue multiples versus pure hardware peers.

However, the model requires substantial upfront investment in software and cloud platforms—CalAmp reported R&D and S&M spend of ~$90M in FY2025—making subscription growth rate (27% YoY in FY2025) a closely watched KPI by investors and analysts.

- Subscription share: 55% of FY2025 revenue (~$250M)

- Subscription growth: 27% YoY (FY2025)

- R&D + S&M spend: ~$90M (FY2025)

- Higher valuation multiples vs hardware-only peers

Fuel Price Fluctuations

Volatile fuel prices drive demand for telematics that cut route miles and idle time; U.S. diesel rose ~35% from 2022 to 2024 (EIA), boosting ROI for CalAmp’s fleet software which reports typical fuel savings of 10–15% per vehicle.

When diesel spikes, logistics operators accelerate telematics adoption—CalAmp’s addressable market penetration benefits as higher fuel costs shorten payback periods to under 12 months in many fleet cases.

- U.S. diesel +35% (2022–2024, EIA)

- CalAmp fuel savings 10–15% per vehicle

- Payback often <12 months during high fuel periods

CalAmp: Rising subscription revenue offsets macro cost pressures and longer chip lead times

Macroeconomic headwinds—higher rates (Fed 5.25–5.50% late‑2025), inflationary wage/cloud cost pressure (US tech wages +5.8% 2024; AWS +6–8% YoY 2024), and supply‑chain lead times (20–28 weeks avg for auto chips 2024)—raise CalAmp’s operating and financing costs, but subscription revenue (55% of FY2025, ~$250M; +27% YoY) improves cash visibility and valuation.

| Metric | Value |

|---|---|

| Subscription share FY2025 | 55% (~$250M) |

| Sub growth FY2025 | 27% YoY |

| R&D+S&M FY2025 | ~$90M |

| Fed funds (late 2025) | 5.25–5.50% |

| Chip lead times (2024) | 20–28 weeks |

What You See Is What You Get

CalAmp PESTLE Analysis

The preview shown here is the exact CalAmp PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use with no placeholders or surprises.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Plan Smarter. Present Sharper. Compete Stronger.

Unlock strategic clarity with our targeted PESTLE Analysis of CalAmp—discover how political shifts, economic trends, social dynamics, technological advances, legal changes, and environmental factors will shape its trajectory; perfect for investors and strategists seeking actionable insights. Purchase the full report to get a comprehensive, editable analysis you can use immediately to inform decisions and identify growth or risk areas.

Political factors

Geopolitical Trade Relations

The ongoing US-China trade dynamics materially affect CalAmp’s hardware procurement, with tariffs on electronic components rising up to 25% in prior cycles and contributing to a reported 8–12% increase in COGS for comparable IoT hardware segments in 2023–2024. Tariffs on telecommunication hardware force margin compression or supply-chain shifts toward Southeast Asia; Vietnam and Malaysia sourcing reduced lead times by 15–20% for peers in 2024. Strategic international trade policy shifts through end-2025 remain a primary risk to maintaining CalAmp’s stable cost structure and 2025 gross-margin targets.

Government Infrastructure Spending

Increased federal and state funding—including the $110B Bipartisan Infrastructure Law allocations for public transit and the $5B+ Smart Cities programs through 2024–25—creates strong tailwinds for CalAmp’s public sector fleet management and asset-tracking solutions.

Government procurement preferences for domestic vendors favor CalAmp, as agencies prioritize supply-chain security and traceability, boosting win rates for contracts above $1M in ITS and fleet telematics.

Ongoing ITS investment, with U.S. DOT funding rising ~12% YoY in 2024, enables CalAmp to capture multi-year municipal deployments and recurring revenue from long-term service agreements.

Cybersecurity Policy and Standards

Political emphasis on national cybersecurity resilience forces telematics providers like CalAmp to meet strict data protection standards as US federal agencies increase IoT security requirements; CISA reported a 24% rise in IoT-related incident reports in 2024. Legislative scrutiny on connected devices tied to critical infrastructure—power, transit—has led to proposed mandates affecting $3.5B in government telematics procurement. CalAmp must align its SDLC with evolving NIST and federal frameworks to retain eligibility for public contracts and avoid revenue risks tied to noncompliance.

Regulatory Oversight of Data Sovereignty

Political moves toward data residency force CalAmp to localize storage and processing of telematics data, increasing infrastructure and compliance costs; GDPR fines can reach up to 4% of global turnover (€35.5B fines issued through 2023 across EU regulators).

In markets like the EU and parts of South America, requirements for local hosting raise operational complexity and may slow international expansion, potentially impacting revenue growth in 2024–25 where global IoT market CAGR is ~17% (2024–29).

- Must invest in regional data centers or partners

- GDPR-style penalties up to 4% revenue

- Higher OPEX and slower rollouts in certain markets

Stability in Key Global Markets

Continuous monitoring of political indicators and reallocating resources to stable markets is critical to limit revenue exposure—target capex hedging and regional diversification.

- Emerging-market FX volatility: ±12% (2024)

- Procurement/contract risk: −8% tender volume (2023)

- Mitigation: hedging, regional diversification, political monitoring

Tariffs, security and funding reshape IoT: costs up, supply times down, risks rise

US-China tariffs raised IoT component costs ~8–12% (2023–24) and Southeast Asia sourcing cut lead times 15–20% in 2024; US infrastructure programs (>$115B to 2025) and +12% YoY DOT funding (2024) boost public-sector demand; CISA reported +24% IoT incidents (2024) enforcing stricter security/NIST compliance; LATAM FX volatility ±12% (2024) and 2023 tender cuts −8% pose contract risk.

| Metric | Value |

|---|---|

| Tariff impact on COGS | +8–12% |

| Southeast Asia lead-time reduction | −15–20% |

| US infrastructure funding | >$115B (to 2025) |

| DOT funding change (2024) | +12% YoY |

| IoT incidents (CISA, 2024) | +24% |

| LATAM FX volatility (2024) | ±12% |

| Procurement tender change (2023) | −8% |

What is included in the product

Explores how external macro-environmental factors uniquely affect CalAmp across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section supported by current data and trends to surface risks and opportunities for executives, investors, and strategists.

Compact PESTLE summary tailored for CalAmp that distills regulatory, tech, economic, social, and environmental drivers into a single-page brief—ideal for quick reference in meetings or slide decks.

Economic factors

Global Supply Chain Volatility

Global supply chain volatility continues to affect CalAmp, with semiconductor prices easing since 2022 but spot shortages still causing lead-time variability; industry reports show lead times for key automotive-grade chips averaged 20–28 weeks in 2024 versus pre‑pandemic 8–12 weeks. Localized disruptions and commodity price swings (e.g., copper up 15% YTD 2025) can delay hardware shipments, pressuring Q1–Q3 2025 revenue recognition. Maintaining optimized inventory turns and strengthened supplier contracts remains crucial to protect hardware margins and ensure shipment predictability.

Interest Rate Environment

As of late 2025, the US Federal Reserve policy rate near 5.25–5.50% raised CalAmp’s weighted average cost of capital, increasing financing costs for customers; small and mid-size fleets reported a 12–18% reduction in planned telematics CAPEX in 2024–25. High rates delayed large-scale hardware rollouts, while Q3–Q4 2025 signs of rate stabilization and lower 10-year Treasury volatility supported renewed investment in efficiency tech like CalAmp’s platform.

Inflationary Pressure on Operating Costs

Inflation raises CalAmp’s labor costs—US tech wages rose ~5.8% in 2024—pushing higher salaries for software engineers and specialists while cloud and data costs climbed (AWS pricing pressure up ~6–8% YoY in 2024). CalAmp must balance these operating-cost increases with competitive SaaS pricing; implementing cost-containment measures and efficiency gains (automation, multi-cloud optimization) is critical to preserve margins amid sustained inflationary pressure.

Shift Toward Recurring Revenue Models

The economic transition from one-time hardware sales to recurring subscription revenue is central to CalAmp’s strategy, with subscription and services revenue rising to 55% of FY2025 revenue (approx $250M), improving predictability and commanding higher EV/Revenue multiples versus pure hardware peers.

However, the model requires substantial upfront investment in software and cloud platforms—CalAmp reported R&D and S&M spend of ~$90M in FY2025—making subscription growth rate (27% YoY in FY2025) a closely watched KPI by investors and analysts.

- Subscription share: 55% of FY2025 revenue (~$250M)

- Subscription growth: 27% YoY (FY2025)

- R&D + S&M spend: ~$90M (FY2025)

- Higher valuation multiples vs hardware-only peers

Fuel Price Fluctuations

Volatile fuel prices drive demand for telematics that cut route miles and idle time; U.S. diesel rose ~35% from 2022 to 2024 (EIA), boosting ROI for CalAmp’s fleet software which reports typical fuel savings of 10–15% per vehicle.

When diesel spikes, logistics operators accelerate telematics adoption—CalAmp’s addressable market penetration benefits as higher fuel costs shorten payback periods to under 12 months in many fleet cases.

- U.S. diesel +35% (2022–2024, EIA)

- CalAmp fuel savings 10–15% per vehicle

- Payback often <12 months during high fuel periods

CalAmp: Rising subscription revenue offsets macro cost pressures and longer chip lead times

Macroeconomic headwinds—higher rates (Fed 5.25–5.50% late‑2025), inflationary wage/cloud cost pressure (US tech wages +5.8% 2024; AWS +6–8% YoY 2024), and supply‑chain lead times (20–28 weeks avg for auto chips 2024)—raise CalAmp’s operating and financing costs, but subscription revenue (55% of FY2025, ~$250M; +27% YoY) improves cash visibility and valuation.

| Metric | Value |

|---|---|

| Subscription share FY2025 | 55% (~$250M) |

| Sub growth FY2025 | 27% YoY |

| R&D+S&M FY2025 | ~$90M |

| Fed funds (late 2025) | 5.25–5.50% |

| Chip lead times (2024) | 20–28 weeks |

What You See Is What You Get

CalAmp PESTLE Analysis

The preview shown here is the exact CalAmp PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use with no placeholders or surprises.