Caledonia Investments PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

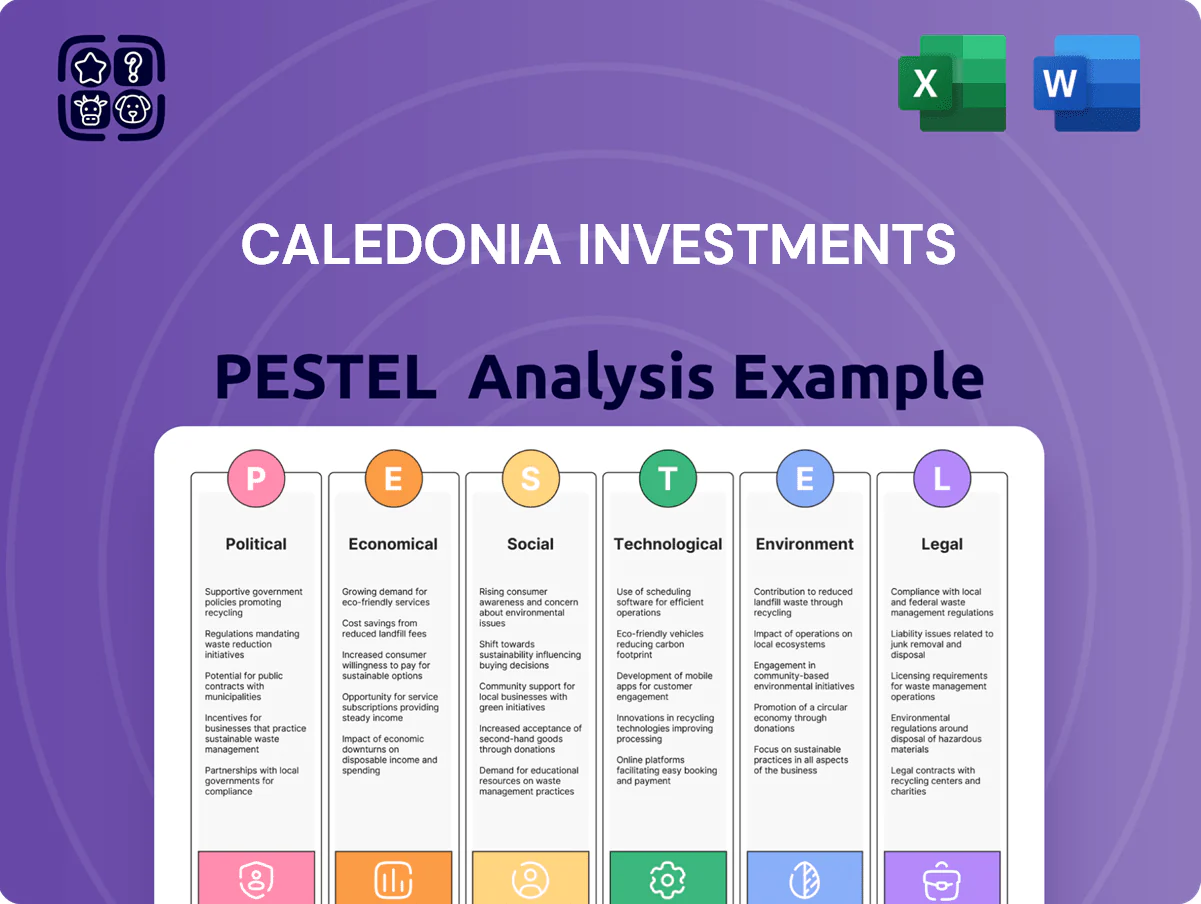

Gain a strategic edge with our PESTLE Analysis of Caledonia Investments—concise, actionable insight into political, economic, social, technological, legal, and environmental forces shaping its future; buy the full report to access deep-dive trends, risk assessments, and ready-to-use recommendations tailored for investors and strategists.

Political factors

UK Government Fiscal Policy

The UK fiscal environment in late 2025 shapes Caledonia's capital allocation and shareholder returns as the OBR projects public sector net borrowing at £126bn for 2025–26 and public sector net debt near 97% of GDP, increasing pressure on taxation and spending choices.

Proposed or enacted changes—e.g., 2024/25 capital gains tax consultations and dividend tax receipts of £52bn in 2024–25—could reduce retail and institutional demand for income-focused trusts like Caledonia.

Monitoring government spending trajectories and sovereign debt metrics is vital: higher debt/GDP or fiscal tightening would compress risk appetite and influence asset valuations and exit timing for UK-listed investment trusts.

Post-Brexit Regulatory Alignment

Ongoing adjustments to UK-EU regulatory alignment affect operational ease for Caledonia's international portfolio, with UK-EU trade in goods down 15% and services exposure significant for private capital deals; in 2024 roughly 36% of Caledonia's NAV was in non-UK assets, heightening sensitivity to cross-border frictions. Divergence in financial services rules increases compliance costs—UK FCA and EU regimes enacted ~12 major rule changes since 2020—complicating cross-border transactions. Strategic focus must prioritize regulatory monitoring and legal contingency planning to preserve capital flow and asset management efficiency.

Geopolitical Stability in Key Markets

Caledonia's diversified portfolio faces geopolitical tensions that in 2024 contributed to 6–8% swings in emerging-market equities, risking supply-chain disruptions and weaker market sentiment for holdings in Asia and Africa.

Political instability where portfolio companies operate has driven asset volatility—several mid-cap positions saw 15–25% intrayear price moves in 2024—forcing swift strategic pivots.

The firm must continuously reassess geopolitical risk premiums; adding a 100–200bps premium to discount rates for high-risk jurisdictions preserves long-term capital growth targets amid heightened global uncertainty.

Corporate Tax Rate Changes

Potential UK corporate tax rate increases—set at 25% since April 2023—would lower net profits across Caledonia Investments’ unlisted portfolio, while differing rates in key jurisdictions (e.g., Ireland 12.5%, US federal 21%) create uneven after-tax outcomes.

Higher taxes reduce free cash flow for reinvestment or debt servicing in private capital assets, compressing projected IRRs if not adjusted.

Analysts should model tax-rate scenarios (e.g., +2–5 ppt) to stress-test valuations and preserve target returns.

- UK rate 25% (since Apr 2023)

- Ireland 12.5%, US 21% federal

- Stress scenarios: +2–5 percentage points

Trade Barrier Impacts on Portfolio

The imposition of new tariffs—such as the 2024 EU steel tariffs and US-China levies that raised input costs by up to 8–12% in affected sectors—can compress margins across Caledonia’s industrial and consumer-facing holdings, lowering EBITDA multiples and valuation. Protectionist moves in major markets may force portfolio companies to reshuffle supply chains, raising capex and logistics costs by an estimated 3–6% and prompting market diversification. Active trade-risk hedging and scenario planning are essential to protect valuations of firms with high export/import exposure, which for some Caledonia-backed companies exceed 40% of revenue.

- Tariff-driven input cost increases: 8–12%

- Supply-chain adjustment capex/logistics impact: ~3–6%

- Export/import dependency in some holdings: >40% of revenue

UK fiscal strain, tax drag and rule divergence squeeze income trusts—EM risk premium rises

UK fiscal strain (PSND ~97% of GDP; public sector net borrowing £126bn for 2025–26) plus tax debates (dividend receipts £52bn in 2024–25) pressure demand for income trusts; UK corporate tax 25% (since Apr 2023) vs Ireland 12.5%/US 21% creates uneven after-tax returns; UK-EU rule divergence (≈12 major financial rules since 2020) and trade drops (UK-EU goods -15%) raise compliance and cross-border frictions; geopolitical shocks drove 6–8% EM swings in 2024, suggesting 100–200bps risk-premium adds.

| Metric | Value |

|---|---|

| PSND (% GDP) | ~97% |

| PSNB | £126bn (2025–26) |

| Dividend tax receipts | £52bn (2024–25) |

| UK corp tax | 25% |

| Non-UK NAV | ~36% (2024) |

| EM equity swings | 6–8% (2024) |

What is included in the product

Explores how macro-environmental forces shape Caledonia Investments across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven insights and forward-looking implications for strategy, risk management, and fundraising.

A concise, shareable PESTLE snapshot of Caledonia Investments that distills external risks and opportunities into clear points for quick inclusion in presentations, meeting briefs, or client reports, easing alignment and strategic decision-making across teams.

Economic factors

Interest Rate Normalization

As global policy rates settle at 3.5–4.0% by late 2025, Caledonia faces higher leverage costs for private investments, pushing portfolio IRR targets to factor increased financing charges.

Stable but elevated rates versus the low-rate 2010s force tighter debt covenants and greater use of fixed-rate or covenant-light structures across the £1.2bn+ private portfolio.

Emphasis shifts to companies with robust free cash flow—cash conversion ratios above 20% and net debt/EBITDA below 2.5x become underwriting priorities.

Private Capital Valuation Trends

The prevailing economic sentiment shifts Caledonia’s exit multiples and entry prices: 2024–25 data show median private equity EV/EBITDA multiples fell from 11.2x in 2021 to ~9.0x in 2023–24, compressing realizations and raising required returns on new deals.

Inflationary Pressure on Margins

Persistent inflation—UK CPI 4.0% in 2024 vs 2.6% in 2023—raises operating costs across Caledonia’s portfolio, pressuring margins where pricing power is weak.

Firms unable to pass on higher input costs risk margin compression and lower EV/EBIT multiples, contributing to downward valuation adjustments seen in 2024 market repricing.

Caledonia focuses on high-quality, defensive holdings—companies with pricing power and recurring revenues—to protect margins and long-term NAV resilience amid prolonged inflationary cycles.

Sterling Exchange Rate Volatility

As a UK-managed trust with substantial US and Eurozone holdings, Caledonia faces sterling volatility; GBP/USD moved ~8% and GBP/EUR ~6% in 2024, creating material NAV translation effects.

Currency swings can produce sizable reported gains or losses—Caledonia reported FX-driven NAV variance of several percent in recent years—prompting use of hedges and geographic diversification to stabilize returns.

- GBP/USD ~8% move in 2024; GBP/EUR ~6% in 2024

- FX can shift NAV by multiple percentage points

- Hedging and geographic diversification employed to mitigate risk

Global Supply Chain Costs

Global logistics and raw material cost shifts materially affect Caledonia Investments’ manufacturing and distribution holdings; world container freight rates rose ~25% YoY in 2024 and steel prices averaged $820/ton in 2025, pressuring margins.

Rising transport costs and sporadic bottlenecks increase inventory days and reduce operational efficiency—ports congestion in 2024 added average lead-time delays of 7–10 days.

By monitoring freight indices, commodity prices and PMI data, Caledonia can work with portfolio management to enhance resilience through dual sourcing, buffer stock and transport renegotiation.

- Freight rates +25% YoY (2024)

- Steel ~$820/ton (2025 avg)

- Port delays +7–10 days (2024)

- Actions: dual sourcing, buffer stock, contract renegotiation

Higher rates, inflation and FX volatility squeeze valuations—seek low‑leverage, cash-rich targets

Higher policy rates (3.5–4.0% by late 2025) raise leverage costs, pushing target IRRs; median PE EV/EBITDA fell ~11% to ~9.0x in 2023–24; UK CPI 4.0% in 2024 up from 2.6% in 2023 compresses margins; GBP moves (~8% vs USD, ~6% vs EUR in 2024) create NAV FX volatility, prompting hedging and focus on cash-generative, low-leverage businesses.

| Metric | Value |

|---|---|

| Policy rates (late 2025) | 3.5–4.0% |

| Median PE EV/EBITDA (2023–24) | ~9.0x |

| UK CPI 2024 | 4.0% |

| GBP/USD move 2024 | ~8% |

Same Document Delivered

Caledonia Investments PESTLE Analysis

The preview shown here is the exact Caledonia Investments PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic or investment decision-making.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Gain a strategic edge with our PESTLE Analysis of Caledonia Investments—concise, actionable insight into political, economic, social, technological, legal, and environmental forces shaping its future; buy the full report to access deep-dive trends, risk assessments, and ready-to-use recommendations tailored for investors and strategists.

Political factors

UK Government Fiscal Policy

The UK fiscal environment in late 2025 shapes Caledonia's capital allocation and shareholder returns as the OBR projects public sector net borrowing at £126bn for 2025–26 and public sector net debt near 97% of GDP, increasing pressure on taxation and spending choices.

Proposed or enacted changes—e.g., 2024/25 capital gains tax consultations and dividend tax receipts of £52bn in 2024–25—could reduce retail and institutional demand for income-focused trusts like Caledonia.

Monitoring government spending trajectories and sovereign debt metrics is vital: higher debt/GDP or fiscal tightening would compress risk appetite and influence asset valuations and exit timing for UK-listed investment trusts.

Post-Brexit Regulatory Alignment

Ongoing adjustments to UK-EU regulatory alignment affect operational ease for Caledonia's international portfolio, with UK-EU trade in goods down 15% and services exposure significant for private capital deals; in 2024 roughly 36% of Caledonia's NAV was in non-UK assets, heightening sensitivity to cross-border frictions. Divergence in financial services rules increases compliance costs—UK FCA and EU regimes enacted ~12 major rule changes since 2020—complicating cross-border transactions. Strategic focus must prioritize regulatory monitoring and legal contingency planning to preserve capital flow and asset management efficiency.

Geopolitical Stability in Key Markets

Caledonia's diversified portfolio faces geopolitical tensions that in 2024 contributed to 6–8% swings in emerging-market equities, risking supply-chain disruptions and weaker market sentiment for holdings in Asia and Africa.

Political instability where portfolio companies operate has driven asset volatility—several mid-cap positions saw 15–25% intrayear price moves in 2024—forcing swift strategic pivots.

The firm must continuously reassess geopolitical risk premiums; adding a 100–200bps premium to discount rates for high-risk jurisdictions preserves long-term capital growth targets amid heightened global uncertainty.

Corporate Tax Rate Changes

Potential UK corporate tax rate increases—set at 25% since April 2023—would lower net profits across Caledonia Investments’ unlisted portfolio, while differing rates in key jurisdictions (e.g., Ireland 12.5%, US federal 21%) create uneven after-tax outcomes.

Higher taxes reduce free cash flow for reinvestment or debt servicing in private capital assets, compressing projected IRRs if not adjusted.

Analysts should model tax-rate scenarios (e.g., +2–5 ppt) to stress-test valuations and preserve target returns.

- UK rate 25% (since Apr 2023)

- Ireland 12.5%, US 21% federal

- Stress scenarios: +2–5 percentage points

Trade Barrier Impacts on Portfolio

The imposition of new tariffs—such as the 2024 EU steel tariffs and US-China levies that raised input costs by up to 8–12% in affected sectors—can compress margins across Caledonia’s industrial and consumer-facing holdings, lowering EBITDA multiples and valuation. Protectionist moves in major markets may force portfolio companies to reshuffle supply chains, raising capex and logistics costs by an estimated 3–6% and prompting market diversification. Active trade-risk hedging and scenario planning are essential to protect valuations of firms with high export/import exposure, which for some Caledonia-backed companies exceed 40% of revenue.

- Tariff-driven input cost increases: 8–12%

- Supply-chain adjustment capex/logistics impact: ~3–6%

- Export/import dependency in some holdings: >40% of revenue

UK fiscal strain, tax drag and rule divergence squeeze income trusts—EM risk premium rises

UK fiscal strain (PSND ~97% of GDP; public sector net borrowing £126bn for 2025–26) plus tax debates (dividend receipts £52bn in 2024–25) pressure demand for income trusts; UK corporate tax 25% (since Apr 2023) vs Ireland 12.5%/US 21% creates uneven after-tax returns; UK-EU rule divergence (≈12 major financial rules since 2020) and trade drops (UK-EU goods -15%) raise compliance and cross-border frictions; geopolitical shocks drove 6–8% EM swings in 2024, suggesting 100–200bps risk-premium adds.

| Metric | Value |

|---|---|

| PSND (% GDP) | ~97% |

| PSNB | £126bn (2025–26) |

| Dividend tax receipts | £52bn (2024–25) |

| UK corp tax | 25% |

| Non-UK NAV | ~36% (2024) |

| EM equity swings | 6–8% (2024) |

What is included in the product

Explores how macro-environmental forces shape Caledonia Investments across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven insights and forward-looking implications for strategy, risk management, and fundraising.

A concise, shareable PESTLE snapshot of Caledonia Investments that distills external risks and opportunities into clear points for quick inclusion in presentations, meeting briefs, or client reports, easing alignment and strategic decision-making across teams.

Economic factors

Interest Rate Normalization

As global policy rates settle at 3.5–4.0% by late 2025, Caledonia faces higher leverage costs for private investments, pushing portfolio IRR targets to factor increased financing charges.

Stable but elevated rates versus the low-rate 2010s force tighter debt covenants and greater use of fixed-rate or covenant-light structures across the £1.2bn+ private portfolio.

Emphasis shifts to companies with robust free cash flow—cash conversion ratios above 20% and net debt/EBITDA below 2.5x become underwriting priorities.

Private Capital Valuation Trends

The prevailing economic sentiment shifts Caledonia’s exit multiples and entry prices: 2024–25 data show median private equity EV/EBITDA multiples fell from 11.2x in 2021 to ~9.0x in 2023–24, compressing realizations and raising required returns on new deals.

Inflationary Pressure on Margins

Persistent inflation—UK CPI 4.0% in 2024 vs 2.6% in 2023—raises operating costs across Caledonia’s portfolio, pressuring margins where pricing power is weak.

Firms unable to pass on higher input costs risk margin compression and lower EV/EBIT multiples, contributing to downward valuation adjustments seen in 2024 market repricing.

Caledonia focuses on high-quality, defensive holdings—companies with pricing power and recurring revenues—to protect margins and long-term NAV resilience amid prolonged inflationary cycles.

Sterling Exchange Rate Volatility

As a UK-managed trust with substantial US and Eurozone holdings, Caledonia faces sterling volatility; GBP/USD moved ~8% and GBP/EUR ~6% in 2024, creating material NAV translation effects.

Currency swings can produce sizable reported gains or losses—Caledonia reported FX-driven NAV variance of several percent in recent years—prompting use of hedges and geographic diversification to stabilize returns.

- GBP/USD ~8% move in 2024; GBP/EUR ~6% in 2024

- FX can shift NAV by multiple percentage points

- Hedging and geographic diversification employed to mitigate risk

Global Supply Chain Costs

Global logistics and raw material cost shifts materially affect Caledonia Investments’ manufacturing and distribution holdings; world container freight rates rose ~25% YoY in 2024 and steel prices averaged $820/ton in 2025, pressuring margins.

Rising transport costs and sporadic bottlenecks increase inventory days and reduce operational efficiency—ports congestion in 2024 added average lead-time delays of 7–10 days.

By monitoring freight indices, commodity prices and PMI data, Caledonia can work with portfolio management to enhance resilience through dual sourcing, buffer stock and transport renegotiation.

- Freight rates +25% YoY (2024)

- Steel ~$820/ton (2025 avg)

- Port delays +7–10 days (2024)

- Actions: dual sourcing, buffer stock, contract renegotiation

Higher rates, inflation and FX volatility squeeze valuations—seek low‑leverage, cash-rich targets

Higher policy rates (3.5–4.0% by late 2025) raise leverage costs, pushing target IRRs; median PE EV/EBITDA fell ~11% to ~9.0x in 2023–24; UK CPI 4.0% in 2024 up from 2.6% in 2023 compresses margins; GBP moves (~8% vs USD, ~6% vs EUR in 2024) create NAV FX volatility, prompting hedging and focus on cash-generative, low-leverage businesses.

| Metric | Value |

|---|---|

| Policy rates (late 2025) | 3.5–4.0% |

| Median PE EV/EBITDA (2023–24) | ~9.0x |

| UK CPI 2024 | 4.0% |

| GBP/USD move 2024 | ~8% |

Same Document Delivered

Caledonia Investments PESTLE Analysis

The preview shown here is the exact Caledonia Investments PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic or investment decision-making.