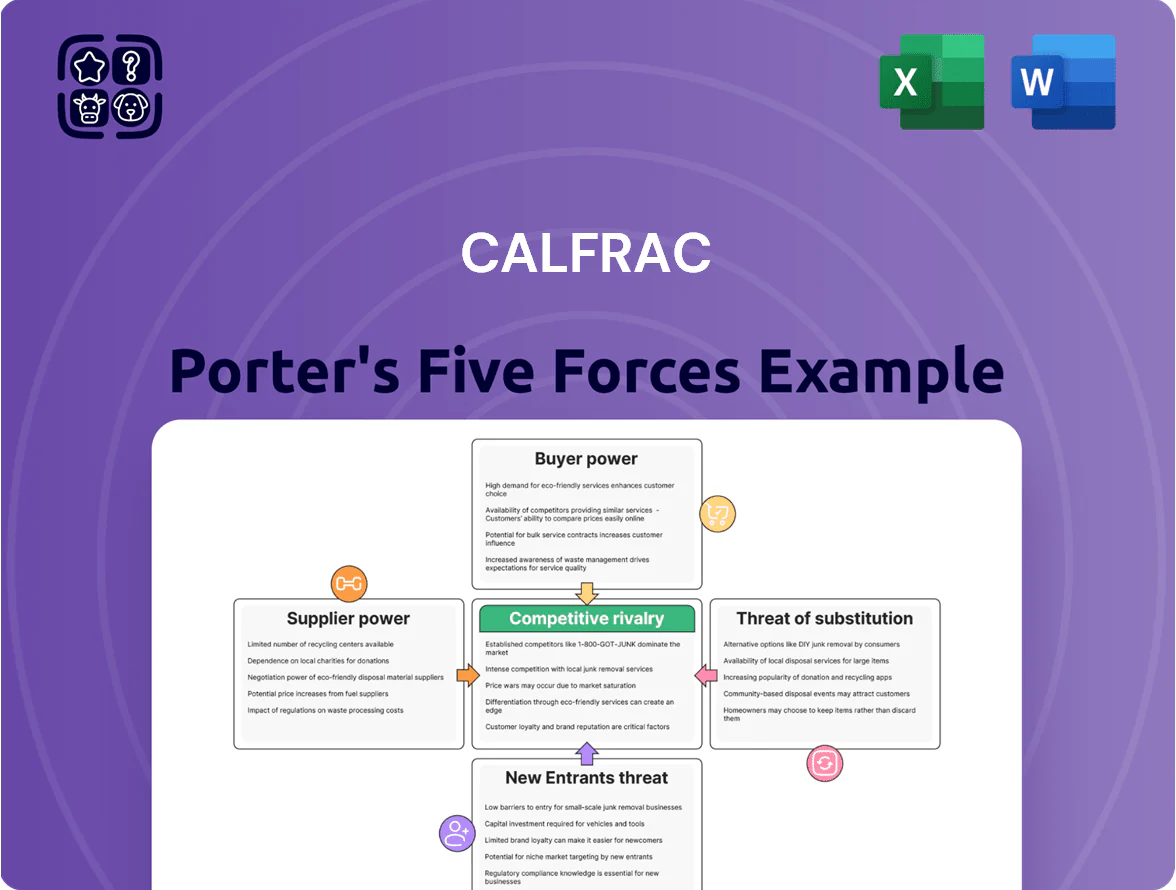

Calfrac Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

Calfrac faces intense competitive pressures from entrenched oilfield service providers, volatile buyer pricing power, and technological shifts that influence service differentiation and cost structures.

This snapshot highlights supplier leverage, the moderate threat of new entrants, and substitute-driven risks from energy transition—factors that shape margins and strategy.

This brief only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Calfrac’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Proppant Suppliers

Proppant suppliers of Northern White sand and premium domestic sand exert strong leverage over Calfrac, as these grades made up about 40% of frac sand demand in North America in 2024 and are geographically concentrated in Minnesota and Alberta.

Rising U.S. and Western Canadian drilling pushed regional sand logistics utilization above 85% in 2024, creating storage and transport bottlenecks that let suppliers push price premiums of 10–25% and insist on multi‑year volume commitments.

Calfrac must secure long‑term contracts, diversify sand sources, and invest in on‑site storage to stabilize supply and protect margins while negotiating price and delivery terms.

Specialized Equipment Manufacturers

The shift to Tier 4 diesel-gasoline-burn (DGB) and electric pumps concentrates suppliers: roughly 5–7 global manufacturers now dominate power-end and fluid-end production, extending lead times to 20–32 weeks and markups of 12–25% versus legacy parts in 2025.

With ESG-driven fleet renewals targeting 2025 compliance, supplier pricing power rose, forcing Calfrac to budget extra capital—estimated CAPEX uplift of 15–22% in 2024–25—to source scarce, high-demand components and avoid downtime.

Skilled Labor Shortages

The oilfield services sector faces a tight market for specialized technical labor and experienced crews; in 2024 Canada reported a 14% shortfall in skilled oilfield workers, raising wage inflation by ~6% year-over-year. Skilled operators and contractors command higher pay and benefits, giving them bargaining leverage that pressures Calfrac’s margins. Calfrac must spend more on retention and training—CapEx and SG&A rises—to avoid poaching by larger rivals, slowing scalable growth.

Chemical and Fluid Additive Costs

Specialized friction reducers and cross-linkers are essential for high-efficiency hydraulic fracturing; their global supply chains faced raw-material price spikes in 2022–2024, with commodity-based polymer feedstocks rising ~18% year-over-year in 2023.

Calfrac diversifies sourcing but basin-specific specs restrict qualified vendors, so substitute risk and lead-time exposure remain; this gives suppliers moderate leverage over costs and scheduling.

Supplier-driven chemical cost swings can shave several percentage points off project margins—here’s the quick math: a 10% chemical cost rise can cut operating margin by ~2–4% on typical fracturing jobs.

- Global feedstock price +18% (2023)

- 10% chemical cost → ~2–4% margin hit

- Limited qualified vendors per basin

- Moderate supplier bargaining power

Logistics and Transportation Constraints

Calfrac depends on specialized trucking and rail to move sand and equipment to remote sites; North American driver shortages and a 2024 US trucking rate increase of ~6-8% have strengthened third-party logistics bargaining power, exposing Calfrac to rate hikes.

Fuel price volatility (Brent averaged $86/bbl in 2024) and occasional rail bottlenecks raise risk of non-productive time (NPT), where each day of NPT can cost frac crews tens of thousands CAD.

- Relies on third-party trucking/rail

- 2024 trucking rates +6–8%

- Brent avg $86/bbl in 2024

- NPT costs: tens of thousands CAD/day

Suppliers Tighten Grip: Premium Sand, OEM Bottlenecks & Rising Input Costs

Suppliers hold strong leverage: 40% of sand demand is premium Northern White (2024), regional logistics utilization >85% drove sand premiums of 10–25% and multi‑year commitments, and 5–7 OEMs control Tier‑4/electric pump parts with 20–32 week lead times and 12–25% markups; chemicals, labor, and transport add volatility (chemical feedstocks +18% in 2023, trucking rates +6–8% in 2024, Brent $86/bbl 2024).

| Metric | Value |

|---|---|

| Premium sand share (2024) | ~40% |

| Logistics utilization (2024) | >85% |

| Sand price premium | 10–25% |

| OEM concentration | 5–7 firms; 20–32 wk lead |

| Chemical feedstock change (2023) | +18% |

| Trucking rate change (2024) | +6–8% |

| Brent average (2024) | $86/bbl |

What is included in the product

Uncovers key drivers of competition, customer influence, supplier power, and entry risks for Calfrac, highlighting disruptive threats, substitute services, and strategic barriers that shape its pricing, profitability, and market position.

A concise Porter's Five Forces one-sheet for Calfrac that highlights competitive pressures and relieves analysis bottlenecks for faster, board-ready decision-making.

Customers Bargaining Power

Consolidation of E&P Companies

The 2021–2024 wave of E&P mergers cut North American operators; the top 10 producers now control ~45% of US crude output, concentrating buyers and boosting their leverage over service firms like Calfrac.

These mega-clients negotiate volume discounts and centralized contracts, driving competitive bids that compressed fracturing margins industry-wide; Calfrac reported a 2024 gross margin of ~12%, reflecting pricing pressure.

Centralized procurement lets buyers shift risk and extract longer payment terms, so Calfrac must keep uptime, proppant efficiency, and safety metrics high to retain high-volume accounts.

Price Sensitivity and Commodity Cycles

Customer demand for Calfrac well services tracks oil and gas prices; in 2024 WTI averaged about US$80/bbl and North American rig counts rose to ~1,200, boosting activity, but when prices fell to US$60–65/bbl in 2020–2021 E&P capex plunged and dayrates collapsed.

Low commodity cycles force E&P firms to cut spend and demand immediate price concessions from Calfrac, giving buyers leverage to halt projects or renegotiate with little notice; Calfrac’s revenue fell ~40% in 2020 after such cuts.

This cyclicality concentrates bargaining power with price-sensitive customers who prioritize cash flow, leaving Calfrac exposed to abrupt investment shifts and contract renegotiations that materially swing utilization and margins.

Low Switching Costs for Operators

In many standard hydraulic fracturing jobs the service is treated as a commodity, so operators can switch providers easily if a rival offers lower rates or faster equipment availability. If a competitor undercuts price or has rigs ready, operators often move at the end of a well program, creating low switching costs. That forces Calfrac to compete on price and uptime; in 2024 Calfrac reported utilization pressures and revenue sensitivity to pricing shifts of ±5–10%. Calfrac therefore focuses on multi-year strategic partnerships to lock in work and stabilize margins.

Information Transparency and Analytics

- Real-time pricing erodes supplier margins

- 2024 US utilization ~58% fuels buyer discounts

- Calfrac needs data-driven value proof (telemetry, stage costs)

Fleet Specification Demands

Customers demand dual-fuel or electric fleets to hit ESG targets, letting them exclude providers lacking upgrades; in 2024, 28% of North American well operators issued low-carbon fleet tender requirements.

That buying power forces Calfrac to direct capex toward these technologies; missing specs risks immediate share loss—largest operators can reassign 10–25% of volumes within 6 months.

- 2024: 28% operators require low-carbon fleets

- Capex shift: fleet upgrades now a strategic must

- Risk: 10–25% volume reallocation in 6 months

Concentrated buyers squeeze Calfrac—margins, utilization hit; capex needed for low‑carbon rigs

Buyers are concentrated—top 10 US producers now control ~45% of output—so they extract discounts, longer terms, and can reallocate 10–25% volumes within 6 months, pressuring Calfrac’s margins (2024 gross ~12%) and utilization (~58% US 2024).

Digital monitoring and 28% of operators requiring low‑carbon fleets in 2024 raise switching and spec risk, forcing Calfrac toward capex for dual‑fuel/electric rigs.

| Metric | Value (2024) |

|---|---|

| Top 10 US share | ~45% |

| Calfrac gross margin | ~12% |

| US utilization | ~58% |

| Ops requiring low‑carbon fleets | 28% |

| Volume reallocation risk | 10–25% (6 months) |

Same Document Delivered

Calfrac Porter's Five Forces Analysis

This preview shows the exact Calfrac Porter’s Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. It contains the full, professionally formatted assessment of competitive rivalry, supplier and buyer power, threats of substitution and entry, and strategic implications tailored to Calfrac. Upon completing payment you’ll get instant access to this same ready-to-use document. Use it as-is for decision-making or reporting.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

Calfrac faces intense competitive pressures from entrenched oilfield service providers, volatile buyer pricing power, and technological shifts that influence service differentiation and cost structures.

This snapshot highlights supplier leverage, the moderate threat of new entrants, and substitute-driven risks from energy transition—factors that shape margins and strategy.

This brief only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Calfrac’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Proppant Suppliers

Proppant suppliers of Northern White sand and premium domestic sand exert strong leverage over Calfrac, as these grades made up about 40% of frac sand demand in North America in 2024 and are geographically concentrated in Minnesota and Alberta.

Rising U.S. and Western Canadian drilling pushed regional sand logistics utilization above 85% in 2024, creating storage and transport bottlenecks that let suppliers push price premiums of 10–25% and insist on multi‑year volume commitments.

Calfrac must secure long‑term contracts, diversify sand sources, and invest in on‑site storage to stabilize supply and protect margins while negotiating price and delivery terms.

Specialized Equipment Manufacturers

The shift to Tier 4 diesel-gasoline-burn (DGB) and electric pumps concentrates suppliers: roughly 5–7 global manufacturers now dominate power-end and fluid-end production, extending lead times to 20–32 weeks and markups of 12–25% versus legacy parts in 2025.

With ESG-driven fleet renewals targeting 2025 compliance, supplier pricing power rose, forcing Calfrac to budget extra capital—estimated CAPEX uplift of 15–22% in 2024–25—to source scarce, high-demand components and avoid downtime.

Skilled Labor Shortages

The oilfield services sector faces a tight market for specialized technical labor and experienced crews; in 2024 Canada reported a 14% shortfall in skilled oilfield workers, raising wage inflation by ~6% year-over-year. Skilled operators and contractors command higher pay and benefits, giving them bargaining leverage that pressures Calfrac’s margins. Calfrac must spend more on retention and training—CapEx and SG&A rises—to avoid poaching by larger rivals, slowing scalable growth.

Chemical and Fluid Additive Costs

Specialized friction reducers and cross-linkers are essential for high-efficiency hydraulic fracturing; their global supply chains faced raw-material price spikes in 2022–2024, with commodity-based polymer feedstocks rising ~18% year-over-year in 2023.

Calfrac diversifies sourcing but basin-specific specs restrict qualified vendors, so substitute risk and lead-time exposure remain; this gives suppliers moderate leverage over costs and scheduling.

Supplier-driven chemical cost swings can shave several percentage points off project margins—here’s the quick math: a 10% chemical cost rise can cut operating margin by ~2–4% on typical fracturing jobs.

- Global feedstock price +18% (2023)

- 10% chemical cost → ~2–4% margin hit

- Limited qualified vendors per basin

- Moderate supplier bargaining power

Logistics and Transportation Constraints

Calfrac depends on specialized trucking and rail to move sand and equipment to remote sites; North American driver shortages and a 2024 US trucking rate increase of ~6-8% have strengthened third-party logistics bargaining power, exposing Calfrac to rate hikes.

Fuel price volatility (Brent averaged $86/bbl in 2024) and occasional rail bottlenecks raise risk of non-productive time (NPT), where each day of NPT can cost frac crews tens of thousands CAD.

- Relies on third-party trucking/rail

- 2024 trucking rates +6–8%

- Brent avg $86/bbl in 2024

- NPT costs: tens of thousands CAD/day

Suppliers Tighten Grip: Premium Sand, OEM Bottlenecks & Rising Input Costs

Suppliers hold strong leverage: 40% of sand demand is premium Northern White (2024), regional logistics utilization >85% drove sand premiums of 10–25% and multi‑year commitments, and 5–7 OEMs control Tier‑4/electric pump parts with 20–32 week lead times and 12–25% markups; chemicals, labor, and transport add volatility (chemical feedstocks +18% in 2023, trucking rates +6–8% in 2024, Brent $86/bbl 2024).

| Metric | Value |

|---|---|

| Premium sand share (2024) | ~40% |

| Logistics utilization (2024) | >85% |

| Sand price premium | 10–25% |

| OEM concentration | 5–7 firms; 20–32 wk lead |

| Chemical feedstock change (2023) | +18% |

| Trucking rate change (2024) | +6–8% |

| Brent average (2024) | $86/bbl |

What is included in the product

Uncovers key drivers of competition, customer influence, supplier power, and entry risks for Calfrac, highlighting disruptive threats, substitute services, and strategic barriers that shape its pricing, profitability, and market position.

A concise Porter's Five Forces one-sheet for Calfrac that highlights competitive pressures and relieves analysis bottlenecks for faster, board-ready decision-making.

Customers Bargaining Power

Consolidation of E&P Companies

The 2021–2024 wave of E&P mergers cut North American operators; the top 10 producers now control ~45% of US crude output, concentrating buyers and boosting their leverage over service firms like Calfrac.

These mega-clients negotiate volume discounts and centralized contracts, driving competitive bids that compressed fracturing margins industry-wide; Calfrac reported a 2024 gross margin of ~12%, reflecting pricing pressure.

Centralized procurement lets buyers shift risk and extract longer payment terms, so Calfrac must keep uptime, proppant efficiency, and safety metrics high to retain high-volume accounts.

Price Sensitivity and Commodity Cycles

Customer demand for Calfrac well services tracks oil and gas prices; in 2024 WTI averaged about US$80/bbl and North American rig counts rose to ~1,200, boosting activity, but when prices fell to US$60–65/bbl in 2020–2021 E&P capex plunged and dayrates collapsed.

Low commodity cycles force E&P firms to cut spend and demand immediate price concessions from Calfrac, giving buyers leverage to halt projects or renegotiate with little notice; Calfrac’s revenue fell ~40% in 2020 after such cuts.

This cyclicality concentrates bargaining power with price-sensitive customers who prioritize cash flow, leaving Calfrac exposed to abrupt investment shifts and contract renegotiations that materially swing utilization and margins.

Low Switching Costs for Operators

In many standard hydraulic fracturing jobs the service is treated as a commodity, so operators can switch providers easily if a rival offers lower rates or faster equipment availability. If a competitor undercuts price or has rigs ready, operators often move at the end of a well program, creating low switching costs. That forces Calfrac to compete on price and uptime; in 2024 Calfrac reported utilization pressures and revenue sensitivity to pricing shifts of ±5–10%. Calfrac therefore focuses on multi-year strategic partnerships to lock in work and stabilize margins.

Information Transparency and Analytics

- Real-time pricing erodes supplier margins

- 2024 US utilization ~58% fuels buyer discounts

- Calfrac needs data-driven value proof (telemetry, stage costs)

Fleet Specification Demands

Customers demand dual-fuel or electric fleets to hit ESG targets, letting them exclude providers lacking upgrades; in 2024, 28% of North American well operators issued low-carbon fleet tender requirements.

That buying power forces Calfrac to direct capex toward these technologies; missing specs risks immediate share loss—largest operators can reassign 10–25% of volumes within 6 months.

- 2024: 28% operators require low-carbon fleets

- Capex shift: fleet upgrades now a strategic must

- Risk: 10–25% volume reallocation in 6 months

Concentrated buyers squeeze Calfrac—margins, utilization hit; capex needed for low‑carbon rigs

Buyers are concentrated—top 10 US producers now control ~45% of output—so they extract discounts, longer terms, and can reallocate 10–25% volumes within 6 months, pressuring Calfrac’s margins (2024 gross ~12%) and utilization (~58% US 2024).

Digital monitoring and 28% of operators requiring low‑carbon fleets in 2024 raise switching and spec risk, forcing Calfrac toward capex for dual‑fuel/electric rigs.

| Metric | Value (2024) |

|---|---|

| Top 10 US share | ~45% |

| Calfrac gross margin | ~12% |

| US utilization | ~58% |

| Ops requiring low‑carbon fleets | 28% |

| Volume reallocation risk | 10–25% (6 months) |

Same Document Delivered

Calfrac Porter's Five Forces Analysis

This preview shows the exact Calfrac Porter’s Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. It contains the full, professionally formatted assessment of competitive rivalry, supplier and buyer power, threats of substitution and entry, and strategic implications tailored to Calfrac. Upon completing payment you’ll get instant access to this same ready-to-use document. Use it as-is for decision-making or reporting.