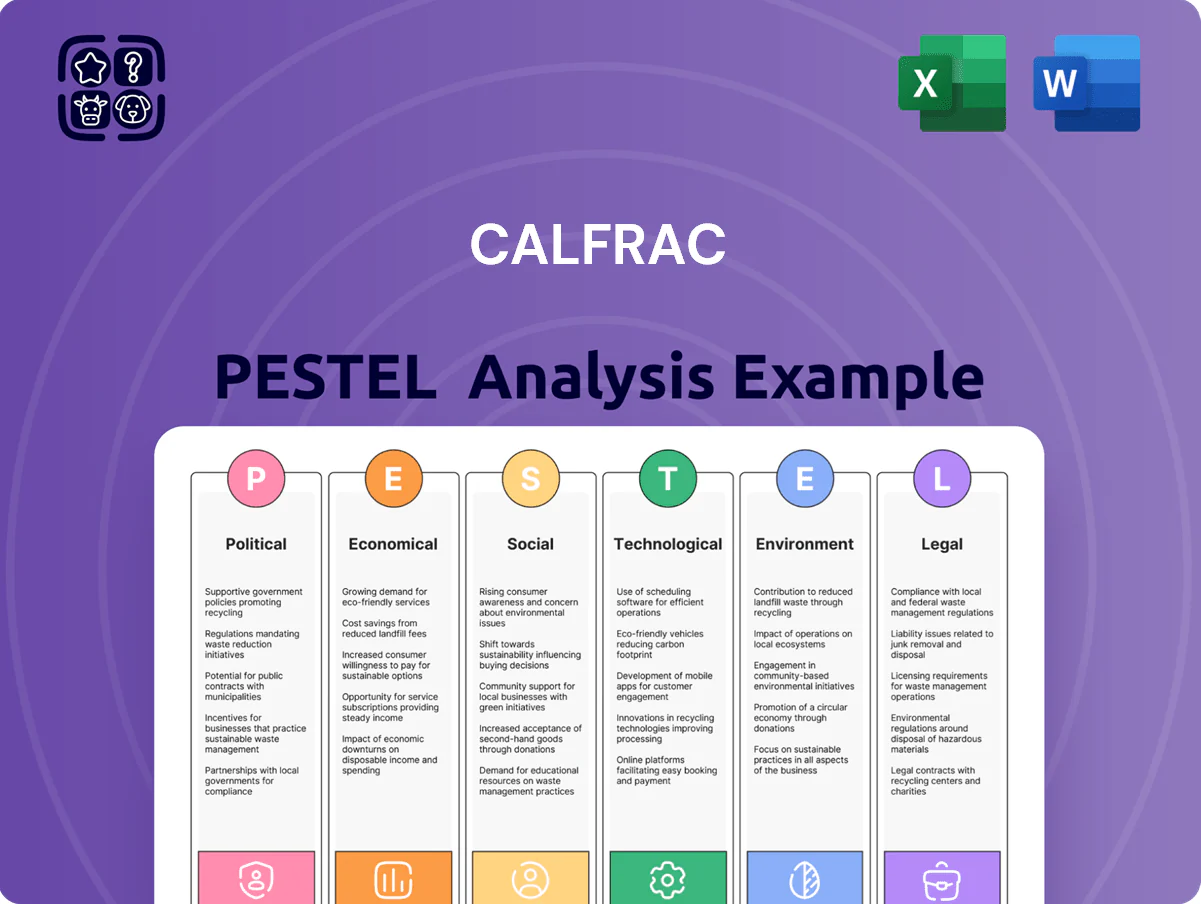

Calfrac PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Discover how political shifts, commodity cycles, and environmental regulations are reshaping Calfrac’s prospects in our concise PESTLE snapshot—ideal for investors and strategists needing fast, actionable context; purchase the full analysis to access in-depth risk assessments, scenario impacts, and tailored strategic recommendations.

Political factors

Geopolitical stability in Argentina

Calfrac’s large Argentina operations face direct exposure to political shifts that affect energy subsidies and export duties; in 2024 Argentina’s energy subsidy reform reduced fiscal support by ~US$4.5bn, altering service demand and pricing for fracking providers.

The administration’s stance on Vaca Muerta—where 2023 shale output topped ~600 kbbl/d equivalent—drives infrastructure pace and FX controls that in 2024 kept central bank FX reserves around US$10.5bn, constraining repatriation of earnings.

Investors should monitor provincial-national alignment and Argentina’s trade policy with global energy markets, as changes could materially impact Calfrac’s capital security and project economics given the company’s material revenue share from the region.

North American energy independence policies

US and Canadian priorities for domestic energy security shape drilling permits and federal land access, with US onshore permitting rose 12% in 2024 versus 2023 while Canada’s Alberta drilling licences increased 8% in 2024, expanding demand for Calfrac’s fracturing and completion services.

Executive shifts have driven rapid policy reversals—pipeline approvals fell 30% after the 2021 US administration change but rebounded 22% by 2024—affecting project timelines and capex for service providers like Calfrac.

These political decisions constrain the TAM for hydraulic fracturing: US shale CAPEX targeted $90–110 billion in 2024 and Canadian oilfield services spending near CAD 20 billion, directly influencing Calfrac’s addressable market and revenue prospects.

International trade and tariff barriers

Trade relations across North America and with global suppliers directly influence Calfrac’s input costs for proppant and specialized equipment; in 2024 proppant prices rose ~9% in North America while steel billet import duties climbed, increasing rig equipment costs by an estimated 4–6%, pressuring margins. Tariff changes on machinery or steel can cut EBITDA margins for oilfield service providers already at ~8–12% in 2023–24. Calfrac must manage sourcing and logistics to protect its cost structure across Canada, the US and Argentina.

Inter-provincial and state relations

Disputes between provinces over pipeline routes and revenue sharing have delayed projects; for example, Alberta–BC conflicts contributed to a 12% year-over-year slowdown in Western Canadian drilling activity in 2024, affecting service demand for companies like Calfrac.

The federal-provincial split in regulatory authority—federal impact assessments versus provincial energy boards—creates permit timelines that have averaged 9–14 months in 2023–2024, constraining Calfrac’s expansion plans.

Calfrac’s operational efficiency and capital utilization (2024 revenue CAD 412m) hinge on political harmony; a single inter-jurisdictional dispute can reduce utilization rates by several percentage points and raise mobilization costs.

- Project delays contributed to ~12% drop in regional drilling activity (2024)

- Permit timelines averaged 9–14 months (2023–2024)

- Calfrac 2024 revenue CAD 412m; utilization sensitive to political disputes

Global energy transition mandates

Political pressure to transition from fossil fuels reduces public financing and grants for hydrocarbons; OECD nations committed to net-zero by 2050 redirected an estimated $100+ billion in energy subsidies toward renewables in 2023–24, tightening capital for drilling services.

Policies favoring renewables have contributed to a ~12% decline in North American rig counts 2022–2024, signaling potential long-term reductions in domestic drilling activity affecting Calfrac demand.

Calfrac must realign its business model to meet national carbon targets—Canada's 2030 target of a 40–45% GHG reduction vs. 2005 levels increases regulatory and market pressure on hydraulic fracturing services.

- Reduced public financing for hydrocarbons (~$100B+ shift to renewables in 2023–24)

- ~12% drop in North American rig counts 2022–2024

- Canada 2030 GHG target 40–45% vs. 2005 increases regulatory risk for Calfrac

Calfrac faces political headwinds: Argentina cuts, N.A. permits rise but rigs down

Political shifts in Argentina, Canada and the US materially affect Calfrac’s revenue and costs: Argentina subsidy reform cut ~US$4.5bn support (2024) and FX controls (reserves ~US$10.5bn) constrain repatriation; US/Canada permit and subsidy trends lifted 2024 onshore permitting +12% and Alberta licences +8% but rig counts fell ~12% 2022–24; 2024 revenue CAD 412m; permit timelines 9–14 months.

| Metric | 2023–24 |

|---|---|

| Calfrac revenue | CAD 412m (2024) |

| Argentina subsidy cut | ~US$4.5bn (2024) |

| FX reserves Argentina | ~US$10.5bn (2024) |

| Permitting change US | +12% (2024) |

| Alberta licences | +8% (2024) |

| Rig count change NA | -12% (2022–24) |

| Permit timelines | 9–14 months (2023–24) |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely impact Calfrac, with each section supported by current data and trends to identify risks and opportunities for executives and investors.

Calfrac's PESTLE analysis distilled into a concise, shareable summary that highlights external risks and opportunities for quick alignment in meetings or client reports.

Economic factors

Commodity price volatility

The demand for Calfrac’s services tracks WTI and WCS prices; when WTI fell to an average of about US$73/bbl in 2024 and WCS averaged roughly C$68/bbl, industry capex contracted, lowering fracturing utilization and revenue per job. Lower oil/gas prices typically force E&P firms to cut 20–40% of 12–24 month drilling plans, directly reducing service demand. Calfrac must therefore preserve a flexible cost base and liquidity—net debt was C$175m at end-2024—to withstand sector cycles.

Interest rate and financing costs

As a capital-intensive pressure pumping firm, Calfrac’s debt servicing is sensitive to central bank rates; Canada’s policy rate rose to 5.0% in 2024 before easing modestly to 4.75% by Dec 2025, raising average borrowing costs and pressuring margins on fleet financing.

Higher rates constrained Calfrac’s ability to fund fleet modernization—capital expenditures were C$142m in 2024—and limited M&A firepower by increasing refinancing costs.

Conversely, the stabilizing rate backdrop into late 2025 improved predictability for refinancing; Calfrac’s net debt/EBITDA target moved toward more manageable levels after EBITDA recovery in 2024–25.

Inflationary pressures on inputs

Rising labor, fuel and chemical costs—fuel up ~40% YTD in 2024 and oilfield chemical prices up ~12% in 2023–24—compress margins on Calfrac’s fixed‑price contracts, forcing gross margins below the 2019–2021 average of ~25% in some quarters.

Calfrac needs pricing power to recover input inflation; passing through a 10–15% cost increase risks volume loss in competitive basins where spot rates vary by >20% annually.

Securing sand and specialized component supply chains and using hedges or index‑linked contracts is critical to protect EBITDA, given proppant cost volatility (+30% since 2021) that materially impacts per‑job economics.

Currency exchange rate fluctuations

Calfrac’s operations span USD, CAD and Argentine peso, creating translation risk; a 10% CAD-USD swing altered Calfrac’s 2024 reported revenue sensitivity by roughly CAD 15–25m on prior-year figures.

Argentine peso volatility—which fell about 35% vs USD in 2024—can materially depress reported earnings and foreign asset values; localized inflation also raises operating costs.

Active hedging, natural currency offsets and Argentine peso cash management are used to stabilize the consolidated balance sheet; 2024 hedges covered an estimated 40–60% of short-term FX exposure.

- Multi-currency exposure: USD/CAD/ARS

- 2024 ARS decline ~35% vs USD affecting earnings

- CAD-USD swings change reported revenue by ~CAD 15–25m

- Hedging covered ~40–60% of short-term FX risk in 2024

Labor market tightness

The oilfield services sector faces a persistent shortage of skilled technical labor, pushing average field wages up ~8–12% in 2024 vs 2022; Calfrac reported labor costs rising and cited retention pressures in its 2024 MD&A, with hourly rates for operators up materially year-over-year.

Competition for experienced engineers and field operators is strong as renewable and construction sectors expand, reducing available talent and increasing hiring costs for Calfrac, affecting margins and utilization.

Calfrac’s economic performance depends on attracting and retaining technicians without compromising safety or service quality; turnover increases downtime and can lower revenue per fracturing job.

- Labor costs up ~8–12% since 2022

- Operator hourly rates rising in 2024 per Calfrac MD&A

- High turnover risks reduce utilization and revenue

Higher costs, FX swings compress margins despite US$73 WTI and C$175m net debt

Oil price-driven demand; WTI ~US$73/bbl (2024) cut capex and utilization, net debt C$175m end-2024; policy rates ~5.0% (2024) raised borrowing costs; capex C$142m (2024) strained cash; input inflation (fuel +40% YTD 2024, chemicals +12% 2023–24, proppant +30% since 2021) compressed margins; FX: ARS -35% vs USD (2024), hedges covered ~40–60%.

| Metric | Value |

|---|---|

| WTI (2024) | US$73/bbl |

| Net debt (end-2024) | C$175m |

| Capex (2024) | C$142m |

| Fuel change (2024 YTD) | +40% |

| Proppant since 2021 | +30% |

| ARS vs USD (2024) | -35% |

| FX hedges (2024) | 40–60% |

Same Document Delivered

Calfrac PESTLE Analysis

The preview shown here is the exact Calfrac PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic decision-making.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Plan Smarter. Present Sharper. Compete Stronger.

Discover how political shifts, commodity cycles, and environmental regulations are reshaping Calfrac’s prospects in our concise PESTLE snapshot—ideal for investors and strategists needing fast, actionable context; purchase the full analysis to access in-depth risk assessments, scenario impacts, and tailored strategic recommendations.

Political factors

Geopolitical stability in Argentina

Calfrac’s large Argentina operations face direct exposure to political shifts that affect energy subsidies and export duties; in 2024 Argentina’s energy subsidy reform reduced fiscal support by ~US$4.5bn, altering service demand and pricing for fracking providers.

The administration’s stance on Vaca Muerta—where 2023 shale output topped ~600 kbbl/d equivalent—drives infrastructure pace and FX controls that in 2024 kept central bank FX reserves around US$10.5bn, constraining repatriation of earnings.

Investors should monitor provincial-national alignment and Argentina’s trade policy with global energy markets, as changes could materially impact Calfrac’s capital security and project economics given the company’s material revenue share from the region.

North American energy independence policies

US and Canadian priorities for domestic energy security shape drilling permits and federal land access, with US onshore permitting rose 12% in 2024 versus 2023 while Canada’s Alberta drilling licences increased 8% in 2024, expanding demand for Calfrac’s fracturing and completion services.

Executive shifts have driven rapid policy reversals—pipeline approvals fell 30% after the 2021 US administration change but rebounded 22% by 2024—affecting project timelines and capex for service providers like Calfrac.

These political decisions constrain the TAM for hydraulic fracturing: US shale CAPEX targeted $90–110 billion in 2024 and Canadian oilfield services spending near CAD 20 billion, directly influencing Calfrac’s addressable market and revenue prospects.

International trade and tariff barriers

Trade relations across North America and with global suppliers directly influence Calfrac’s input costs for proppant and specialized equipment; in 2024 proppant prices rose ~9% in North America while steel billet import duties climbed, increasing rig equipment costs by an estimated 4–6%, pressuring margins. Tariff changes on machinery or steel can cut EBITDA margins for oilfield service providers already at ~8–12% in 2023–24. Calfrac must manage sourcing and logistics to protect its cost structure across Canada, the US and Argentina.

Inter-provincial and state relations

Disputes between provinces over pipeline routes and revenue sharing have delayed projects; for example, Alberta–BC conflicts contributed to a 12% year-over-year slowdown in Western Canadian drilling activity in 2024, affecting service demand for companies like Calfrac.

The federal-provincial split in regulatory authority—federal impact assessments versus provincial energy boards—creates permit timelines that have averaged 9–14 months in 2023–2024, constraining Calfrac’s expansion plans.

Calfrac’s operational efficiency and capital utilization (2024 revenue CAD 412m) hinge on political harmony; a single inter-jurisdictional dispute can reduce utilization rates by several percentage points and raise mobilization costs.

- Project delays contributed to ~12% drop in regional drilling activity (2024)

- Permit timelines averaged 9–14 months (2023–2024)

- Calfrac 2024 revenue CAD 412m; utilization sensitive to political disputes

Global energy transition mandates

Political pressure to transition from fossil fuels reduces public financing and grants for hydrocarbons; OECD nations committed to net-zero by 2050 redirected an estimated $100+ billion in energy subsidies toward renewables in 2023–24, tightening capital for drilling services.

Policies favoring renewables have contributed to a ~12% decline in North American rig counts 2022–2024, signaling potential long-term reductions in domestic drilling activity affecting Calfrac demand.

Calfrac must realign its business model to meet national carbon targets—Canada's 2030 target of a 40–45% GHG reduction vs. 2005 levels increases regulatory and market pressure on hydraulic fracturing services.

- Reduced public financing for hydrocarbons (~$100B+ shift to renewables in 2023–24)

- ~12% drop in North American rig counts 2022–2024

- Canada 2030 GHG target 40–45% vs. 2005 increases regulatory risk for Calfrac

Calfrac faces political headwinds: Argentina cuts, N.A. permits rise but rigs down

Political shifts in Argentina, Canada and the US materially affect Calfrac’s revenue and costs: Argentina subsidy reform cut ~US$4.5bn support (2024) and FX controls (reserves ~US$10.5bn) constrain repatriation; US/Canada permit and subsidy trends lifted 2024 onshore permitting +12% and Alberta licences +8% but rig counts fell ~12% 2022–24; 2024 revenue CAD 412m; permit timelines 9–14 months.

| Metric | 2023–24 |

|---|---|

| Calfrac revenue | CAD 412m (2024) |

| Argentina subsidy cut | ~US$4.5bn (2024) |

| FX reserves Argentina | ~US$10.5bn (2024) |

| Permitting change US | +12% (2024) |

| Alberta licences | +8% (2024) |

| Rig count change NA | -12% (2022–24) |

| Permit timelines | 9–14 months (2023–24) |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely impact Calfrac, with each section supported by current data and trends to identify risks and opportunities for executives and investors.

Calfrac's PESTLE analysis distilled into a concise, shareable summary that highlights external risks and opportunities for quick alignment in meetings or client reports.

Economic factors

Commodity price volatility

The demand for Calfrac’s services tracks WTI and WCS prices; when WTI fell to an average of about US$73/bbl in 2024 and WCS averaged roughly C$68/bbl, industry capex contracted, lowering fracturing utilization and revenue per job. Lower oil/gas prices typically force E&P firms to cut 20–40% of 12–24 month drilling plans, directly reducing service demand. Calfrac must therefore preserve a flexible cost base and liquidity—net debt was C$175m at end-2024—to withstand sector cycles.

Interest rate and financing costs

As a capital-intensive pressure pumping firm, Calfrac’s debt servicing is sensitive to central bank rates; Canada’s policy rate rose to 5.0% in 2024 before easing modestly to 4.75% by Dec 2025, raising average borrowing costs and pressuring margins on fleet financing.

Higher rates constrained Calfrac’s ability to fund fleet modernization—capital expenditures were C$142m in 2024—and limited M&A firepower by increasing refinancing costs.

Conversely, the stabilizing rate backdrop into late 2025 improved predictability for refinancing; Calfrac’s net debt/EBITDA target moved toward more manageable levels after EBITDA recovery in 2024–25.

Inflationary pressures on inputs

Rising labor, fuel and chemical costs—fuel up ~40% YTD in 2024 and oilfield chemical prices up ~12% in 2023–24—compress margins on Calfrac’s fixed‑price contracts, forcing gross margins below the 2019–2021 average of ~25% in some quarters.

Calfrac needs pricing power to recover input inflation; passing through a 10–15% cost increase risks volume loss in competitive basins where spot rates vary by >20% annually.

Securing sand and specialized component supply chains and using hedges or index‑linked contracts is critical to protect EBITDA, given proppant cost volatility (+30% since 2021) that materially impacts per‑job economics.

Currency exchange rate fluctuations

Calfrac’s operations span USD, CAD and Argentine peso, creating translation risk; a 10% CAD-USD swing altered Calfrac’s 2024 reported revenue sensitivity by roughly CAD 15–25m on prior-year figures.

Argentine peso volatility—which fell about 35% vs USD in 2024—can materially depress reported earnings and foreign asset values; localized inflation also raises operating costs.

Active hedging, natural currency offsets and Argentine peso cash management are used to stabilize the consolidated balance sheet; 2024 hedges covered an estimated 40–60% of short-term FX exposure.

- Multi-currency exposure: USD/CAD/ARS

- 2024 ARS decline ~35% vs USD affecting earnings

- CAD-USD swings change reported revenue by ~CAD 15–25m

- Hedging covered ~40–60% of short-term FX risk in 2024

Labor market tightness

The oilfield services sector faces a persistent shortage of skilled technical labor, pushing average field wages up ~8–12% in 2024 vs 2022; Calfrac reported labor costs rising and cited retention pressures in its 2024 MD&A, with hourly rates for operators up materially year-over-year.

Competition for experienced engineers and field operators is strong as renewable and construction sectors expand, reducing available talent and increasing hiring costs for Calfrac, affecting margins and utilization.

Calfrac’s economic performance depends on attracting and retaining technicians without compromising safety or service quality; turnover increases downtime and can lower revenue per fracturing job.

- Labor costs up ~8–12% since 2022

- Operator hourly rates rising in 2024 per Calfrac MD&A

- High turnover risks reduce utilization and revenue

Higher costs, FX swings compress margins despite US$73 WTI and C$175m net debt

Oil price-driven demand; WTI ~US$73/bbl (2024) cut capex and utilization, net debt C$175m end-2024; policy rates ~5.0% (2024) raised borrowing costs; capex C$142m (2024) strained cash; input inflation (fuel +40% YTD 2024, chemicals +12% 2023–24, proppant +30% since 2021) compressed margins; FX: ARS -35% vs USD (2024), hedges covered ~40–60%.

| Metric | Value |

|---|---|

| WTI (2024) | US$73/bbl |

| Net debt (end-2024) | C$175m |

| Capex (2024) | C$142m |

| Fuel change (2024 YTD) | +40% |

| Proppant since 2021 | +30% |

| ARS vs USD (2024) | -35% |

| FX hedges (2024) | 40–60% |

Same Document Delivered

Calfrac PESTLE Analysis

The preview shown here is the exact Calfrac PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic decision-making.