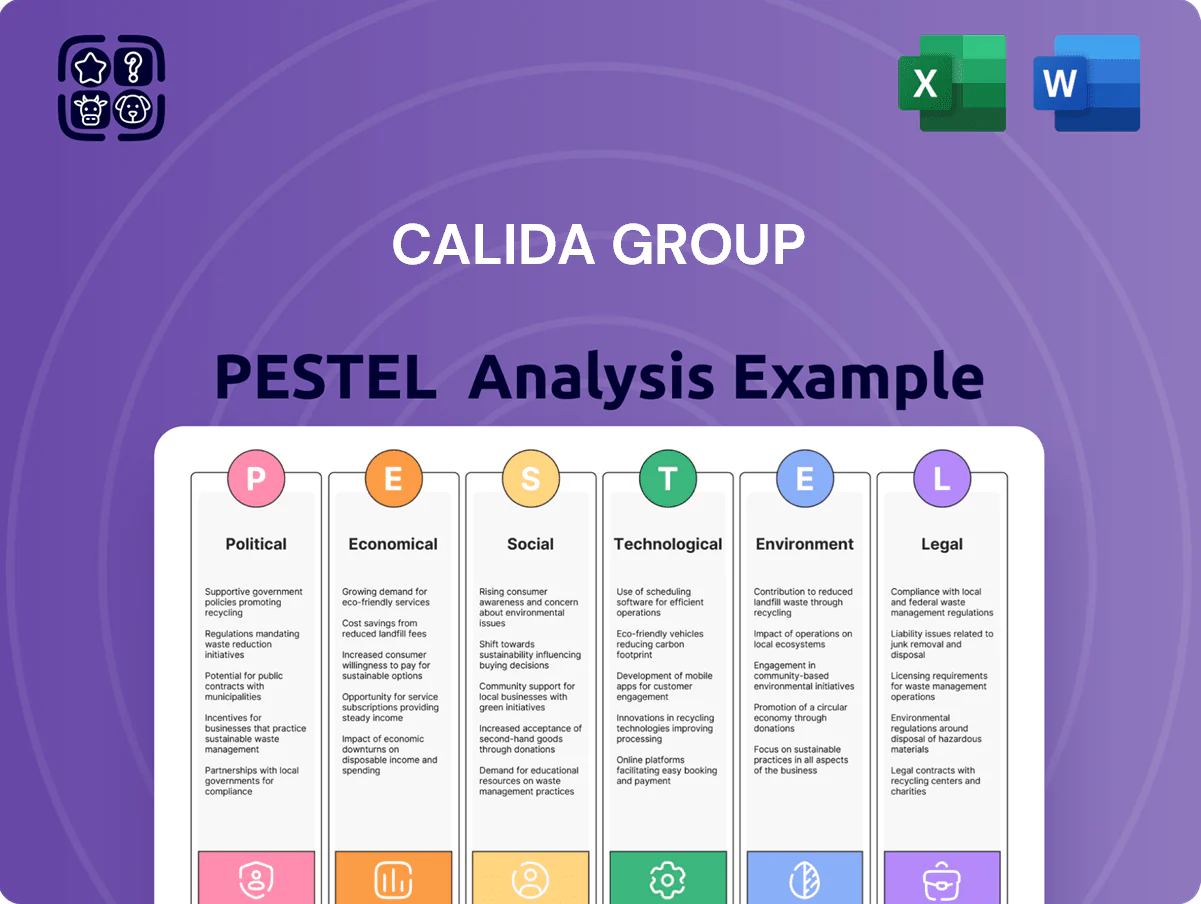

CALIDA Group PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Gain a competitive edge with our targeted PESTLE Analysis of CALIDA Group—unpack how political shifts, economic pressures, social trends, and regulatory changes will shape its strategy and performance; perfect for investors and strategists seeking actionable insights. Purchase the full report to access the complete, exportable analysis and make smarter, faster decisions.

Political factors

Global Trade Policy and Tariffs

As CALIDA Group sells in 90+ countries, shifts in trade agreements and tariffs can squeeze margins; e.g., a 5% tariff on Asian-made garments could raise landed costs by ~€3–5 per unit, impacting FY2024 gross margin of 44.1% reported in 2024.

Geopolitical Stability in Production Hubs

CALIDA Group depends on a global supply chain concentrated in Asia and Eastern Europe; 2024 trade disruptions in Bangladesh and Turkey raised regional lead times by 15–25%, exposing risks to textile brands MILLET and LAFUMA. Supply interruptions in 2023–24 caused inventory shortfalls that pushed logistics costs up ~12% YoY for comparable apparel groups. Diversifying suppliers across 18+ countries and holding 8–10 weeks of buffer stock are strategic levers CALIDA uses to mitigate political-risk-driven shortages.

Swiss-EU Regulatory Alignment

Headquartered in Switzerland but with over 60% of 2024 revenue derived from EU markets, CALIDA must monitor Swiss-EU bilateral talks closely; shifts in relations risk tighter technical barriers to trade and increased compliance costs estimated at up to 1–2% of sales for textile exporters. Changes could also constrain cross-border labor mobility—affecting 25% of CALIDA’s EU workforce—and require corporate-structure adjustments to maintain market access.

Government Sustainability Mandates

By end-2025, EU and US laws pushed corporate supply-chain transparency: the EU Corporate Sustainability Due Diligence Directive and US state laws increased due-diligence reporting, affecting companies with revenues >€150m/€500m thresholds; 78% of large European firms reported enhanced human-rights audits in 2024.

CALIDA Group’s established ESG framework—reporting aligned to GRI and invested ~€2.5m in supplier audits 2023–25—supports compliance, protecting access to EU/NA markets and reducing regulatory risk to revenue.

- Regulatory trend: mandatory human-rights/environmental due diligence across EU/NA by 2025

- Market impact: 78% of large EU firms upgraded audits (2024)

- CALIDA action: €2.5m invested in supplier audits (2023–25)

- Benefit: preserves market access and lowers regulatory risk to sales

Export Control and Sanctions

The volatile global political landscape requires CALIDA to follow evolving sanction regimes restricting trade with countries like Russia and Iran; in 2024 UN/EU/US measures affected apparel imports valued at billions, raising compliance stakes.

With distribution in over 90 countries, CALIDA needs rigorous legal screening—automated checks and KYC—to avoid breaches that could mean fines up to 4% of annual turnover (EU GDPR-like fines) or multi-million-dollar penalties.

Non-compliance risks reputational damage among its premium customer base, potentially hitting sales and brand value; in 2023 supply-chain sanctions disruptions raised apparel sector costs by an estimated 2–5%.

- Operate screenings for 90+ markets

- Monitor changing EU/US/UN sanctions continuously

- Invest in automated export control systems

- Mitigate fines and brand erosion risk

Political risk adds 1–5% costs; CALIDA's €2.5m audits and buffers cut 2023–24 disruption

Political risks (trade barriers, sanctions, labor mobility rules, due-diligence laws) can add 1–5% to costs or compliance spend; CALIDA’s €2.5m supplier-audit investment and 8–10 weeks buffer stock mitigate disruptions that in 2023–24 raised logistics costs ~12% YoY and regional lead times 15–25%, while EU/US due-diligence rules and sanctions expose fines up to 4% turnover.

| Metric | Value |

|---|---|

| Logistics cost rise (2023–24) | ~12% YoY |

| Regional lead-time increase | 15–25% |

| Audit spend (2023–25) | €2.5m |

| Gross margin (FY2024) | 44.1% |

| Potential tariff impact/unit | €3–5 (5% on Asian-made) |

| Max fines | Up to 4% turnover |

What is included in the product

Explores how external macro-environmental factors uniquely affect the CALIDA Group across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends, practical subpoints and forward-looking insights tailored for executives, consultants and investors to identify threats, opportunities and strategic actions in its regional apparel market.

Condenses the CALIDA Group PESTLE into a concise, shareable brief that supports quick alignment in meetings and can be dropped straight into presentations or strategy packs.

Economic factors

Inflationary Pressure on Discretionary Spending

Fluctuating inflation in core European markets—Eurozone CPI averaged 5.9% in 2023 and eased to about 3.2% in 2024—erodes real incomes and can reduce frequency of premium apparel purchases despite CALIDA and AUBADE targeting higher-income segments; during past downturns sales volumes dipped (luxury apparel down mid-single digits in 2023), so the group emphasizes product longevity and quality as a value proposition to retain buyers and protect margins.

Currency Exchange Volatility

With reporting in Swiss francs and large Euro/Dollar operations, CALIDA Group faces notable FX risk; a 5% EUR/CHF move in 2025 would change reported revenue by roughly CHF 8–12m given 2024 group revenue of CHF 283.9m.

Exchange swings affect export price competitiveness and translate into translation effects—subsidiary valuation saw a -3.2% FX translation drag in H2 2025.

The group used forward contracts and options, hedging about 60–75% of near-term exposures to protect gross margins amid late‑2025 monetary volatility.

Rising Labor and Production Costs

The textile industry’s rising skilled labor costs in traditional hubs increased CALIDA Group’s production overhead, with wage growth in sourcing markets averaging 5–8% annually (2023–2024) and unit labor cost inflation of ~6% in key regions. Economic development in Vietnam and Turkey pushed minimum wages up 7–10% in 2024, pressuring margins and requiring trade-offs between craftsmanship and cost-efficiency. CALIDA responded by investing CHF 12–15 million in automation and shifting 18% of output to lower-cost facilities during 2023–2025 to optimize its global manufacturing footprint.

Growth of the Outdoor Economy

The global outdoor recreation economy was valued at about USD 689 billion in 2023 and grew ~5% annually 2020–2024, providing a tailwind for MILLET and LAFUMA as consumers shift spending to health and wellness experiences; technical outdoor apparel demand remained resilient, with global outdoor clothing market projected to reach USD 29.5 billion by 2025.

This trend helps CALIDA Group diversify revenue beyond intimate apparel and supports margin resilience as outdoor segments typically command higher ASPs and lower seasonality versus lingerie.

- Outdoor economy ~USD 689B (2023)

- Outdoor apparel market ~USD 29.5B (2025 proj.)

- ~5% CAGR 2020–2024

Raw Material Price Fluctuations

Raw material costs for CALIDA Group are exposed to commodity volatility; organic cotton prices rose ~18% in 2023 before easing 6% in 2024, while polyester feedstock (PX) swung ±20% in 2023–24, pressuring gross margins.

Disruptions in cotton yields or polymer supply chains can shift COGS materially; a 10% input-cost increase could cut margin percentage points given CALIDA’s 2024 gross margin ~44%.

Strategic procurement, hedging and multi-year supplier contracts—already used by many apparel firms—are critical to stabilize costs and protect earnings visibility.

- Organic cotton +18% (2023), -6% (2024)

- PX/polymer price volatility ±20% (2023–24)

- CALIDA 2024 gross margin ~44%

- Mitigants: long-term contracts, hedging, diversified suppliers

CALIDA weathers weaker Euro, automation and hedges to protect margins

Eurozone inflation eased from 5.9% (2023) to ~3.2% (2024), pressuring premium apparel demand; CALIDA revenue CHF 283.9m (2024) with gross margin ~44%. FX: 5% EUR/CHF move ≈ CHF 8–12m impact; H2 2025 translation drag -3.2%; hedges cover ~60–75% near-term. Labor/wage inflation 5–10% in sourcing markets; CHF 12–15m automation spend and 18% output shift (2023–25).

| Metric | Value |

|---|---|

| Revenue (2024) | CHF 283.9m |

| Gross margin | ~44% |

| EUR/CHF 5% impact | CHF 8–12m |

| Hedge coverage | 60–75% |

| Automation spend | CHF 12–15m |

Preview the Actual Deliverable

CALIDA Group PESTLE Analysis

The preview shown here is the exact CALIDA Group PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic or investment decision-making.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Gain a competitive edge with our targeted PESTLE Analysis of CALIDA Group—unpack how political shifts, economic pressures, social trends, and regulatory changes will shape its strategy and performance; perfect for investors and strategists seeking actionable insights. Purchase the full report to access the complete, exportable analysis and make smarter, faster decisions.

Political factors

Global Trade Policy and Tariffs

As CALIDA Group sells in 90+ countries, shifts in trade agreements and tariffs can squeeze margins; e.g., a 5% tariff on Asian-made garments could raise landed costs by ~€3–5 per unit, impacting FY2024 gross margin of 44.1% reported in 2024.

Geopolitical Stability in Production Hubs

CALIDA Group depends on a global supply chain concentrated in Asia and Eastern Europe; 2024 trade disruptions in Bangladesh and Turkey raised regional lead times by 15–25%, exposing risks to textile brands MILLET and LAFUMA. Supply interruptions in 2023–24 caused inventory shortfalls that pushed logistics costs up ~12% YoY for comparable apparel groups. Diversifying suppliers across 18+ countries and holding 8–10 weeks of buffer stock are strategic levers CALIDA uses to mitigate political-risk-driven shortages.

Swiss-EU Regulatory Alignment

Headquartered in Switzerland but with over 60% of 2024 revenue derived from EU markets, CALIDA must monitor Swiss-EU bilateral talks closely; shifts in relations risk tighter technical barriers to trade and increased compliance costs estimated at up to 1–2% of sales for textile exporters. Changes could also constrain cross-border labor mobility—affecting 25% of CALIDA’s EU workforce—and require corporate-structure adjustments to maintain market access.

Government Sustainability Mandates

By end-2025, EU and US laws pushed corporate supply-chain transparency: the EU Corporate Sustainability Due Diligence Directive and US state laws increased due-diligence reporting, affecting companies with revenues >€150m/€500m thresholds; 78% of large European firms reported enhanced human-rights audits in 2024.

CALIDA Group’s established ESG framework—reporting aligned to GRI and invested ~€2.5m in supplier audits 2023–25—supports compliance, protecting access to EU/NA markets and reducing regulatory risk to revenue.

- Regulatory trend: mandatory human-rights/environmental due diligence across EU/NA by 2025

- Market impact: 78% of large EU firms upgraded audits (2024)

- CALIDA action: €2.5m invested in supplier audits (2023–25)

- Benefit: preserves market access and lowers regulatory risk to sales

Export Control and Sanctions

The volatile global political landscape requires CALIDA to follow evolving sanction regimes restricting trade with countries like Russia and Iran; in 2024 UN/EU/US measures affected apparel imports valued at billions, raising compliance stakes.

With distribution in over 90 countries, CALIDA needs rigorous legal screening—automated checks and KYC—to avoid breaches that could mean fines up to 4% of annual turnover (EU GDPR-like fines) or multi-million-dollar penalties.

Non-compliance risks reputational damage among its premium customer base, potentially hitting sales and brand value; in 2023 supply-chain sanctions disruptions raised apparel sector costs by an estimated 2–5%.

- Operate screenings for 90+ markets

- Monitor changing EU/US/UN sanctions continuously

- Invest in automated export control systems

- Mitigate fines and brand erosion risk

Political risk adds 1–5% costs; CALIDA's €2.5m audits and buffers cut 2023–24 disruption

Political risks (trade barriers, sanctions, labor mobility rules, due-diligence laws) can add 1–5% to costs or compliance spend; CALIDA’s €2.5m supplier-audit investment and 8–10 weeks buffer stock mitigate disruptions that in 2023–24 raised logistics costs ~12% YoY and regional lead times 15–25%, while EU/US due-diligence rules and sanctions expose fines up to 4% turnover.

| Metric | Value |

|---|---|

| Logistics cost rise (2023–24) | ~12% YoY |

| Regional lead-time increase | 15–25% |

| Audit spend (2023–25) | €2.5m |

| Gross margin (FY2024) | 44.1% |

| Potential tariff impact/unit | €3–5 (5% on Asian-made) |

| Max fines | Up to 4% turnover |

What is included in the product

Explores how external macro-environmental factors uniquely affect the CALIDA Group across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends, practical subpoints and forward-looking insights tailored for executives, consultants and investors to identify threats, opportunities and strategic actions in its regional apparel market.

Condenses the CALIDA Group PESTLE into a concise, shareable brief that supports quick alignment in meetings and can be dropped straight into presentations or strategy packs.

Economic factors

Inflationary Pressure on Discretionary Spending

Fluctuating inflation in core European markets—Eurozone CPI averaged 5.9% in 2023 and eased to about 3.2% in 2024—erodes real incomes and can reduce frequency of premium apparel purchases despite CALIDA and AUBADE targeting higher-income segments; during past downturns sales volumes dipped (luxury apparel down mid-single digits in 2023), so the group emphasizes product longevity and quality as a value proposition to retain buyers and protect margins.

Currency Exchange Volatility

With reporting in Swiss francs and large Euro/Dollar operations, CALIDA Group faces notable FX risk; a 5% EUR/CHF move in 2025 would change reported revenue by roughly CHF 8–12m given 2024 group revenue of CHF 283.9m.

Exchange swings affect export price competitiveness and translate into translation effects—subsidiary valuation saw a -3.2% FX translation drag in H2 2025.

The group used forward contracts and options, hedging about 60–75% of near-term exposures to protect gross margins amid late‑2025 monetary volatility.

Rising Labor and Production Costs

The textile industry’s rising skilled labor costs in traditional hubs increased CALIDA Group’s production overhead, with wage growth in sourcing markets averaging 5–8% annually (2023–2024) and unit labor cost inflation of ~6% in key regions. Economic development in Vietnam and Turkey pushed minimum wages up 7–10% in 2024, pressuring margins and requiring trade-offs between craftsmanship and cost-efficiency. CALIDA responded by investing CHF 12–15 million in automation and shifting 18% of output to lower-cost facilities during 2023–2025 to optimize its global manufacturing footprint.

Growth of the Outdoor Economy

The global outdoor recreation economy was valued at about USD 689 billion in 2023 and grew ~5% annually 2020–2024, providing a tailwind for MILLET and LAFUMA as consumers shift spending to health and wellness experiences; technical outdoor apparel demand remained resilient, with global outdoor clothing market projected to reach USD 29.5 billion by 2025.

This trend helps CALIDA Group diversify revenue beyond intimate apparel and supports margin resilience as outdoor segments typically command higher ASPs and lower seasonality versus lingerie.

- Outdoor economy ~USD 689B (2023)

- Outdoor apparel market ~USD 29.5B (2025 proj.)

- ~5% CAGR 2020–2024

Raw Material Price Fluctuations

Raw material costs for CALIDA Group are exposed to commodity volatility; organic cotton prices rose ~18% in 2023 before easing 6% in 2024, while polyester feedstock (PX) swung ±20% in 2023–24, pressuring gross margins.

Disruptions in cotton yields or polymer supply chains can shift COGS materially; a 10% input-cost increase could cut margin percentage points given CALIDA’s 2024 gross margin ~44%.

Strategic procurement, hedging and multi-year supplier contracts—already used by many apparel firms—are critical to stabilize costs and protect earnings visibility.

- Organic cotton +18% (2023), -6% (2024)

- PX/polymer price volatility ±20% (2023–24)

- CALIDA 2024 gross margin ~44%

- Mitigants: long-term contracts, hedging, diversified suppliers

CALIDA weathers weaker Euro, automation and hedges to protect margins

Eurozone inflation eased from 5.9% (2023) to ~3.2% (2024), pressuring premium apparel demand; CALIDA revenue CHF 283.9m (2024) with gross margin ~44%. FX: 5% EUR/CHF move ≈ CHF 8–12m impact; H2 2025 translation drag -3.2%; hedges cover ~60–75% near-term. Labor/wage inflation 5–10% in sourcing markets; CHF 12–15m automation spend and 18% output shift (2023–25).

| Metric | Value |

|---|---|

| Revenue (2024) | CHF 283.9m |

| Gross margin | ~44% |

| EUR/CHF 5% impact | CHF 8–12m |

| Hedge coverage | 60–75% |

| Automation spend | CHF 12–15m |

Preview the Actual Deliverable

CALIDA Group PESTLE Analysis

The preview shown here is the exact CALIDA Group PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic or investment decision-making.